Analys

SHB Veckans råvarukommentar 23 januari 2015

Händelserik vecka på markoarenan

Händelserik vecka på markoarenan- Vårt aluminiumcase håller än

- Oljepriset stabiliserar sig

- Utbudsstörning skulle få oljan att rusa

- Guldet fortsatt upp efter tillflykt till säker hamn

- Nederbördsrikt och milt väder håller elpriset nere

Vi lägger en händelserik vecka med stora rörelser på makroarenan bakom oss. ECB lanserade slutligen QE och Kina släppte makrodata som var i linje eller något bättre än förväntat. Fortfarande är dock fastighetssektorn svag och koppar med flera basmetaller handlas svagt efter Kinadata. Järnmalm är en annan råvara med stark koppling till Kinas byggnation och malmen har fallit till ny lägstanivå i denna prisrörelse, nu på 66,7 USD/ton.

Vårt case på aluminium från 15/1 har börjat bra, ligger 5 % upp och vi flaggar för att vara redo att ta vinsten. Caset har en potential på max 10 % i rådande marknad så med några ytterligare bra handelsdagar tycker vi man ska vara nöjd.

Oljepriset har stabiliserat sig på knappt USD 50 de senaste två veckorna och OPEC har slutat prata ned priset vid sina framträdande. Det ser alltså ut som att vi har nått botten men det finns inga tydliga tecken på att oljan ska handla upp snart. Terminskurvan prissätter brent kring USD 58 i december så en återgång till nivåer där en större del av skifferproducenterna är lönsamma är redan inprisad. Investeringar bland skifferbolagen pekar mot en kraftig avmattning i USA:s oljeproduktion under slutet av 2015. Antalet sysselsatta riggar har fallit dramatiskt de senaste veckorna men har ännu inte fått någon effekt i produktionen som steg till nytt rekord förra veckan. Det är alltid de minst produktiva riggarna som först ställs av, varför det dröjer innan produktionen minskar. De gamla prisnivåerna kring 80-90 USD ser vi som otänkbara då de åter kommer attrahera hela spannet av skifferproducenter. OPEC:s aktion för lägre pris har kostat mycket pengar och om inte resultatet blir att konkurrensen från marginalproducenter slås ut så var hela aktionen meningslös. Vi landar därmed i att dagens pris kommer eliminera för mycket nödvändiga återinvesteringar men att USD 80 är för högt.

Riskbilden i denna analys ligger dock på uppsidan då flera länder riskerar att destabiliseras med rådande oljepris under 2015. Venezuela är största risken där marknaden prisätter 86 % risk för default under 2015. Nigeria är nästa risk utöver ökade spänningar i Mellanöstern. En större utbudsstörning skulle sannolikt få marknaden att rusa från dagens nedtryckta nivåer.

Under veckan har Saudiarabiens kung Abdullah avlidit och spekulation om att det öppnar för förändrad policy från Saudiarabien fick oljan att stiga. Vi tror inte att det är så sannolikt då det kommer vara viktigt för kungahuset att visa en enad front efter att kronprins Salman tar över som ny kung.

Gårdagens besked från ECB om QE har lett till ytterligare försvagning av euron, och därtill kopplad förstärkning av dollarn. Euron har nu fallit med över 7 % under det nya året, och med nästan 18 % sedan i somras, mot amerikanska dollarn, och detta ligger naturligtvis som en våt filt över dollarnoterade råvaror. Guldet har dock handlat upp till 1300 USD per ounce trots dollarförstärkningen, drivet av en flykt till säkra tillgångar efter bl.a. Schweiz valutachock i förra veckan, och av den fortsatta nedgången i globala räntor. Handelsbankens syn är alltjämt att Fed kommer att höja tidigare än vad marknaden just nu prisar in. Vi ser därför nuvarande nivåer på guldet som höga, och att risken i priset är på nedsidan, även om vi är lite förundrade över att priset hållit sig på dessa nivåer trots dollarns styrka och fallet i framför allt oljepriset.

Elpriset, närmare bestämt kvartal Q215 (underliggande till våra certifikat), har under årets inledande handel fastnat i ett lägre intervall mellan 26-27 EUR/MWh då det milda och nederbördsrikt vädret i kombination med allt lägre kolpriser fortsätter att överraska. Hydrologin har också förbättrats nämnvärt där vi inför årsskiftet hade ett underskott kring 8 TWh och som nu närmare sig +2 TWh. Det fanns en viss förhoppning om högre elpriser inför EU-kommissionens omröstning av förslaget att införa en stabilitetsreserv redan 2017 istället för år 2021 för att minska överskottet på utsläppsrätter. Förslaget röstades dock ned vilket gjorde att utsläppsrätterna föll och drog med sig elmarknaden. Nu måste miljögruppen inom kommissionen omarbeta förslaget som parlamentet och rådet får ta ställning till, nästa möte den 24/2 så det lär inte hända så värst mycket fram till dess. För att blicka framåt är det svårt att motivera någon kraftig uppgång på el under dessa milda förhållanden där spotpriset också ser ut vara under kontroll. Senaste väderprognosen pekar dessutom på hela 6 TWh nederbörd den kommande veckan vilket är 2 TWh över normalt. Det finns dock tecken på kyla mot slutet av perioden och kolpriset signalerar en uppgång från extremt låga nivåer vilket i kombination med en starkare USD kan driva upp priset under den kommande veckan.

Läs vårt Trading Case på Aluminium här (från 15 jan)

[box]SHB Råvarukommentar är producerat av Handelsbanken och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta material är producerat av Svenska Handelsbanken AB (publ) i fortsättningen kallad Handelsbanken. De som arbetar med innehållet är inte analytiker och materialet är inte oberoende investeringsanalys. Innehållet är uteslutande avsett för kunder i Sverige. Syftet är att ge en allmän information till Handelsbankens kunder och utgör inte ett personligt investeringsråd eller en personlig rekommendation. Informationen ska inte ensamt utgöra underlag för investeringsbeslut. Kunder bör inhämta råd från sina rådgivare och basera sina investeringsbeslut utifrån egen erfarenhet.

Informationen i materialet kan ändras och också avvika från de åsikter som uttrycks i oberoende investeringsanalyser från Handelsbanken. Informationen grundar sig på allmänt tillgänglig information och är hämtad från källor som bedöms som tillförlitliga, men riktigheten kan inte garanteras och informationen kan vara ofullständig eller nedkortad. Ingen del av förslaget får reproduceras eller distribueras till någon annan person utan att Handelsbanken dessförinnan lämnat sitt skriftliga medgivande. Handelsbanken ansvarar inte för att materialet används på ett sätt som strider mot förbudet mot vidarebefordran eller offentliggörs i strid med bankens regler.

Oil prices are likely to fall for a fourth straight year as OPEC+ unwinds cuts and retakes market share. We expect Brent crude to average USD 55/b in Q4/25 before OPEC+ steps in to stabilise the market into 2026. Surplus, stock building, oil prices are under pressure with OPEC+ calling the shots as to how rough it wants to play it. We see natural gas prices following parity with oil (except for seasonality) until LNG surplus arrives in late 2026/early 2027.

Oil market: Q4/25 and 2026 will be all about how OPEC+ chooses to play it

OPEC+ is in a process of unwinding voluntary cuts by a sub-group of the members and taking back market share. But the process looks set to be different from 2014-16, as the group doesn’t look likely to blindly lift production to take back market share. The group has stated very explicitly that it can just as well cut production as increase it ahead. While the oil price is unlikely to drop as violently and lasting as in 2014-16, it will likely fall further before the group steps in with fresh cuts to stabilise the price. We expect Brent to fall to USD 55/b in Q4/25 before the group steps in with fresh cuts at the end of the year.

Natural gas market: Winter risk ahead, yet LNG balance to loosen from 2026

The global gas market entered 2025 in a fragile state of balance. European reliance on LNG remains high, with Russian pipeline flows limited to Turkey and Russian LNG constrained by sanctions. Planned NCS maintenance in late summer could trim exports by up to 1.3 TWh/day, pressuring EU storage ahead of winter. Meanwhile, NE Asia accounts for more than 50% of global LNG demand, with China alone nearing a 20% share (~80 mt in 2024). US shale gas production has likely peaked after reaching 104.8 bcf/d, even as LNG export capacity expands rapidly, tightening the US balance. Global supply additions are limited until late 2026, when major US, Qatari and Canadian projects are due to start up. Until then, we expect TTF to average EUR 38/MWh through 2025, before easing as the new supply wave likely arrives in late 2026 and then in 2027.

Price action contained withing USD 2/b last week. Likely muted today as well with US closed. The Brent November contract is the new front-month contract as of today. It traded in a range of USD 66.37-68.49/b and closed the week up a mere 0.4% at USD 67.48/b. US oil inventory data didn’t make much of an impact on the Brent price last week as it is totally normal for US crude stocks to decline 2.4 mb/d this time of year as data showed. This morning Brent is up a meager 0.5% to USD 67.8/b. It is US Labor day today with US markets closed. Today’s price action is likely going to be muted due to that.

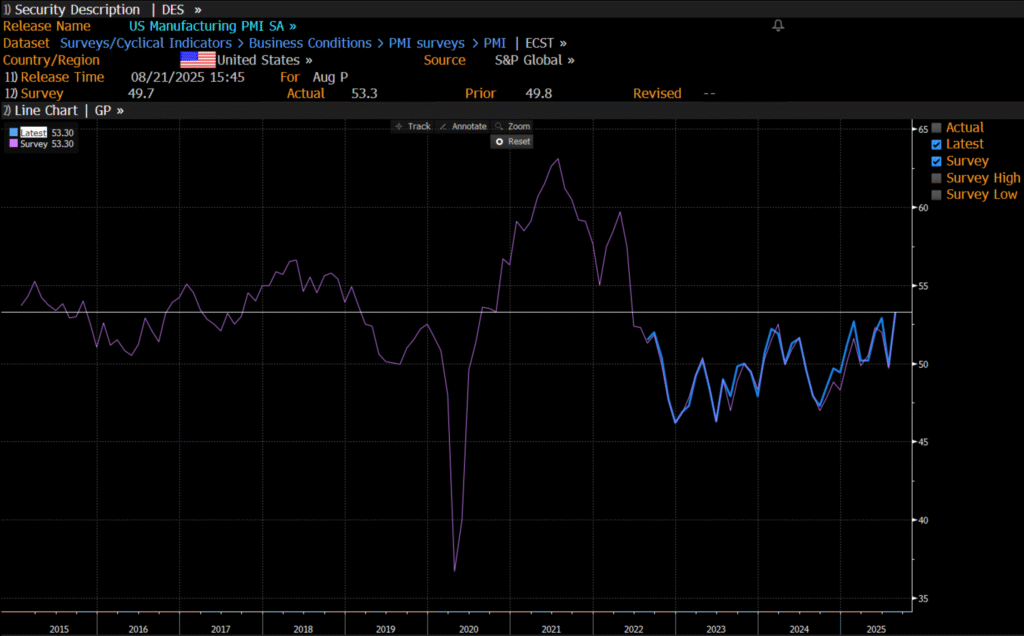

Improving manufacturing readings. China’s manufacturing PMI for August came in at 49.4 versus 49.3 for July. A marginal improvement. The total PMI index ticked up to 50.5 from 50.2 with non-manufacturing also helping it higher. The HCOB Eurozone manufacturing PMI was a disastrous 45.1 last December, but has since then been on a one-way street upwards to its current 50.5 for August. The S&P US manufacturing index jumped to 53.3 in August which was the highest since 2022 (US ISM manufacturing tomorrow). India manufacturing PMI rose further and to 59.3 for August which is the highest since at least 2022.

Are we in for global manufacturing expansion? Would help to explain copper at 10k and resilient oil. JPMorgan global manufacturing index for August is due tomorrow. It was 49.7 in July and has been below the 50-line since February. Looking at the above it looks like a good chance for moving into positive territory for global manufacturing. A copper price of USD 9935/ton, sniffing at the 10k line could be a reflection of that. An oil price holding up fairly well at close to USD 68/b despite the fact that oil balances for Q4-25 and 2026 looks bloated could be another reflection that global manufacturing may be accelerating.

US manufacturing PMI by S&P rose to 53.3 in August. It was published on 21 August, so not at all newly released. But the US ISM manufacturing PMI is due tomorrow and has the potential to follow suite with a strong manufacturing reading.

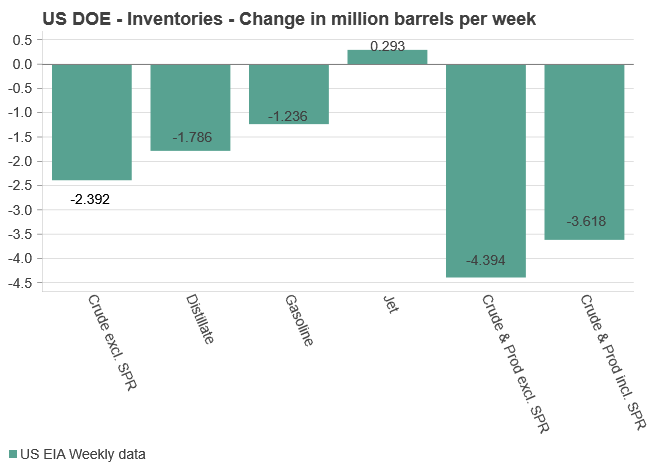

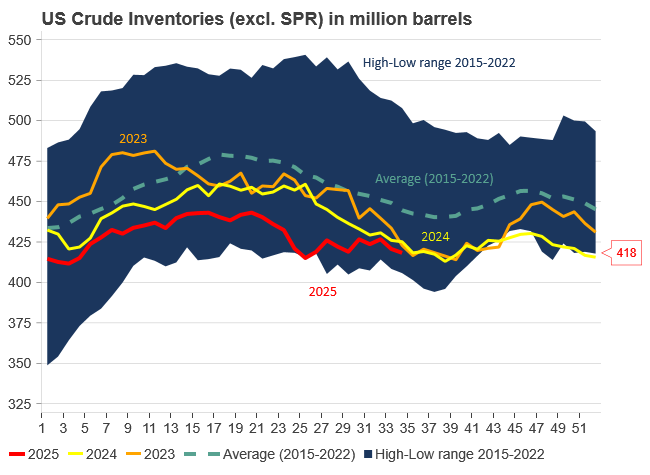

U.S. commercial crude inventories posted another draw last week, falling by 2.4 million barrels to 418.3 million barrels, according to the latest DOE report. Inventories are now 6% below the five-year seasonal average, underlining a persistently tight supply picture as we move into the post-peak demand season.

While the draw was smaller than last week’s 6 million barrel decline, the trend remains consistent with seasonal patterns. Current inventories are still well below the 2015–2022 average of around 449 million barrels.

Gasoline inventories dropped by 1.2 million barrels and are now close to the five-year average. The breakdown showed a modest increase in finished gasoline offset by a decline in blending components – hinting at steady end-user demand.

Diesel inventories saw yet another sharp move, falling by 1.8 million barrels. Stocks are now 15% below the five-year average, pointing to sustained tightness in middle distillates. In fact, diesel remains the most undersupplied segment, with current inventory levels at the very low end of the historical range (see page 3 attached).

Total commercial petroleum inventories – including crude and products but excluding the SPR – fell by 4.4 million barrels on the week, bringing total inventories to approximately 1,259 million barrels. Despite rising refinery utilization at 94.6%, the broader inventory complex remains structurally tight.

On the demand side, the DOE’s ‘products supplied’ metric – a proxy for implied consumption – stayed strong. Total product demand averaged 21.2 million barrels per day over the last four weeks, up 2.5% YoY. Diesel and jet fuel were the standouts, up 7.7% and 1.7%, respectively, while gasoline demand softened slightly, down 1.1% YoY. The figures reflect a still-solid late-summer demand environment, particularly in industrial and freight-related sectors.

Guldpriset kan närma sig 5000 USD om centralbankens oberoende skadas

Råvaror har nästan aldrig varit så här billiga

Världens största sandbatteri invigt i Finland

Gurkodling får 3 MW el-effekt i södra Sverige

Eurobattery Minerals satsar på kritiska metaller för Europas självförsörjning

Omgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

Meta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

What OPEC+ is doing, what it is saying and what we are hearing

Aker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

Brent sideways on sanctions and peace talks

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanOmgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMeta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

-

Analys4 veckor sedan

What OPEC+ is doing, what it is saying and what we are hearing

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

-

Analys3 veckor sedan

Brent sideways on sanctions and peace talks

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEtt samtal om koppar, kaffe och spannmål

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSommarens torka kan ge högre elpriser i höst

-

Analys2 veckor sedan

Brent edges higher as India–Russia oil trade draws U.S. ire and Powell takes the stage at Jackson Hole