Analys

SHB Råvarubrevet 26 april 2013

Råvaror allmänt

Råvaror allmänt

Makrotunga veckor – Råvarorna vänder upp

Denna vecka började med en ny kalldusch, råvarunegativ makrodata. Nu i form av preliminära inköpschefssiffror som från Kina, USA och Tyskland var sämre än väntat. I sällskap av mer dålig makrodata så bidrog dock dataskörden så småningom till att öka förväntningarna på att ECB ska sänka räntan den 2:a maj och det fick i sin tur råvarupriserna att rekylera på bred front under sista delen av veckan. Centralbanksstödet fortsätter, nu med Bank of Japan i förarsätet och vi tror att ECB kommer att haka på inom kort.

Vi tycker generellt att råvarunedgången har varit överdriven givet hur makrodata har utvecklat sig. Flera råvarusektorer är klart köpvärda. Vi väntar dock på att ekonomer och analytiker ska hinna ta till sig den sämre dataskörden och därmed bidra till att förväntansbilden sänks innan vi tror att den stora rekylen uppåt kommer.

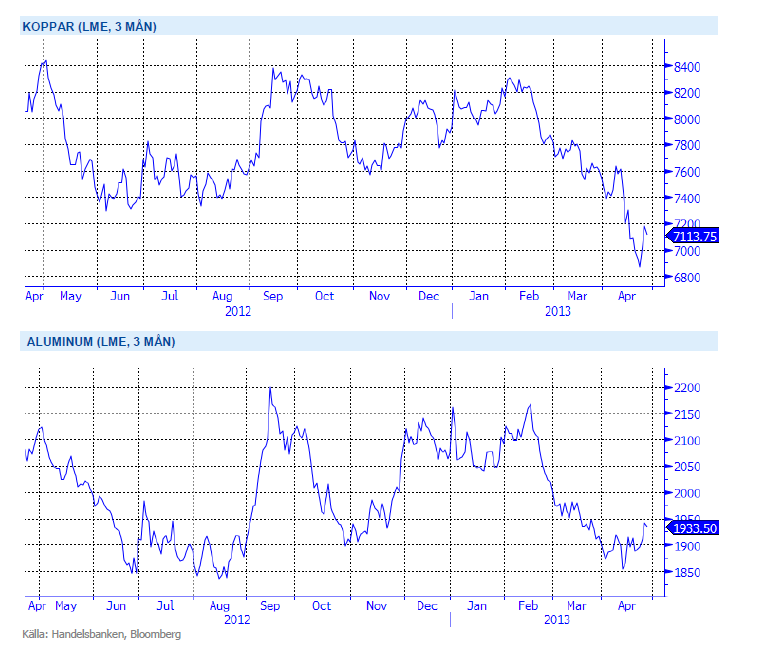

Basmetallerna

Stark vecka för basmetallerna

Basmetallerna har blivit väldigt tekniskt handlade i den negativa miljön. Vi har samlat ett antal indikatorer från den fysiska marknaden som ser ganska bra ut och vi tror att basmetaller är den råvarusektor som har störst potential att studsa upp efter vårens ras. Ännu vågar vi dock inte slå på stora trumman utan avvaktar ytterligare dålig makrodata som vi tror ligger i luften.

Basmetallerna har visat på styrka under veckan som gått. Koppar vände på 6854, före senaste årens botten under 2011 på 6635. Aluminium nådde 30-dagars högsta men även nickel och zink har visat på en klar vändning.

Trots fortsatt svag makromiljö och fortsatt risk på nedsidan ser vi ändå basmetaller som köpvärda på dessa nivåer. Vi tror på: LONG BASMET H

Ädelmetaller

Guldet rekylerar upp, har det vänt nu?

Guldet har – tillsammans med de flesta råvaror – rekylerat upp denna vecka. Rekylen har varit ganska kraftig, över 4 % upp sedan förra fredagen, eller 8 % från botten måndagen den 15 april. Det är inget konstigt i det, då guldet föll rekordsnabbt för två veckor sedan, och vi står alltjämt 13 % lägre än början på året. Silver, guldets sprallige lillebror, har också studsat upp, men ligger över 20 % ner på året trots detta. Köpläge eller säljläge?

Vi tror fortfarande att guldets glans falnat en hel del, det ska studsa lite efter ett så kraftigt fall vi såg för två veckor sedan, och nu hör vi tal om att centralbanker världen över köpt guld senaste veckan. Det är värt att påminna om att centralbanker som har bestämmelser om hur stor andel av reserverna som ska ligga i guld de facto MÅSTE köpa guld när det har fallit så kraftigt, annars minskar guldets andel i reserven. Omvänt måste de sälja om priset stiger.

Guldets huvudproblem kvarstår, alla som köper gör det för att sälja dyrare, alltså även världens centralbanker. Centralbankerna har dock lyxen att slippa sälja när priset faller. Åtminstone tills någon säger att man ska minska sin andel guld i reserven.

Köp inte guld. För den som är tekniskt intresserad kan nämnas att rekylen nu vände på exakt 61,8 % retracement, en viktig s.k. Fibonacci-nivå.

Trots det största raset på 30 år tror vi att förtroendet för guld håller på urholkas och att trenden nedåt fortsätter. Vi tror på: SHRT GULD H

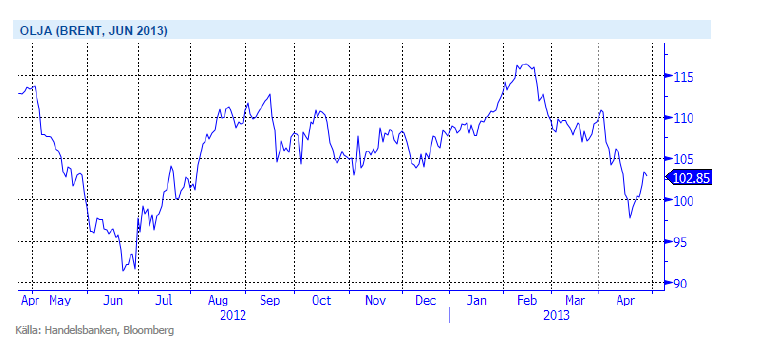

Energi

Brent oljan över 100 dollar igen

Priset på el har under veckan fortsatt att stiga efter nedgången från föregående vecka. Variationer i väderprognoser och nyheter kring utsläppsrätterna har varit i fokus denna vecka. På väderfronten gav prognoser med torrare och kallare väder stöd åt elpriset veckans första dagar. Nya prognoser med mer nederbörd än normalt fick priset att falla tillbaka något. För utsläppsrätterna verkar det som de blir en ny omröstning i slutet på juli om den s.k. backloadingplanen. Under veckan har det även auktionerats ut hela 25 miljoner rätter (!), vilket marknaden ändå klarat av förhållandevis bra. Veckan bjöd även på besked om att ministerrådet följer parlamentets beslut att integrera flygtrafik in och ur EU i systemet för handel med utsläppsrätter.

Oljepriset har också studsat under veckan. OPEC har dragit ner produktionen under året och bidrar till att stabilisera priset. Q2 är säsongsmässigt en svag period då många raffinaderier går in i underhåll efter mellan vintern och sommarens högproduktion. Under hösten har Nordsjön har också stabiliserat produktionen efter de låga nivåerna.

OPEC har tidigare aktivt och framgångsrikt försvarat prismålet 100-110 USD och vi väntar oss handling snarare än besked från kartellen inom kort. Konfliken mellan Israel och Iran är nästa skäl att förvänta sig högre oljepriser under H2. Vi tror på: LONG OLJA H

Livsmedel

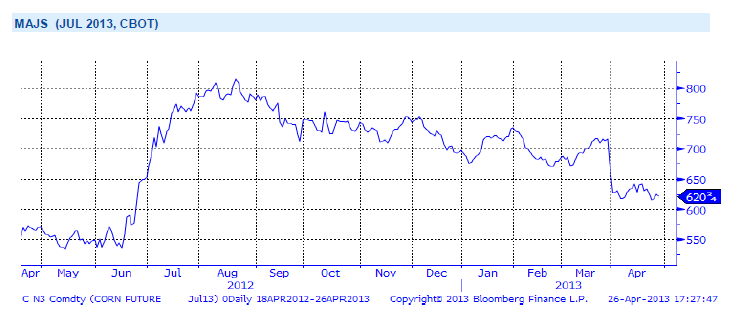

Bättre väder för sådden i USA

Priserna på majs i Chicago har gått ned under veckan, delvis som följd av förbättrad väderlek för den amerikanska majssådden. Fortfarande faller en del småskurar men temperaturen har stigit och den relativt sena sådden kan nu öka i takt, liknande förhållanden ser ut att råda åtminstone en bit in i nästa vecka. Än finns det gott om tid kvar och inga skäl att tro på annat än en väldigt stark återhämtning för den amerikanska majsproduktionen efter förra årets torka. Globala majsproduktionen för säsongen 2013/14 uppskattar International Grains Council, IGC, till 939 miljoner ton, att jämföra med 851 miljoner ton innevarande säsong – upp drygt 10 procent.

Priserna på sojabönor i Chicago noteras ned sedan förra veckan. I dagsläget är det svårt att tro på annat än en ökad sojaproduktion i USA för nästa säsong, vilket tillsammans med ökad produktion även i andra delar av världen bör ge press nedåt på priset längre fram på året. International Grains Council, IGC, upp skattar kommande säsongs globala sojaskörd till 265 miljoner ton, drygt 10 procent upp från innevarande säsong. Även bättre väder för den fortsatta sojasådden i USA, tillsammans med vikande amerikanska exportsiffror, har gett press nedåt på priset.

Då priserna har på de stora jordbruksråvarorna soja, majs och vete har fallit tillbaka till nivåer före torkan i USA, tror vi att en nedsida är begränsad på kort sikt och därför är vi neutrala till utvecklingen för denna sektor.

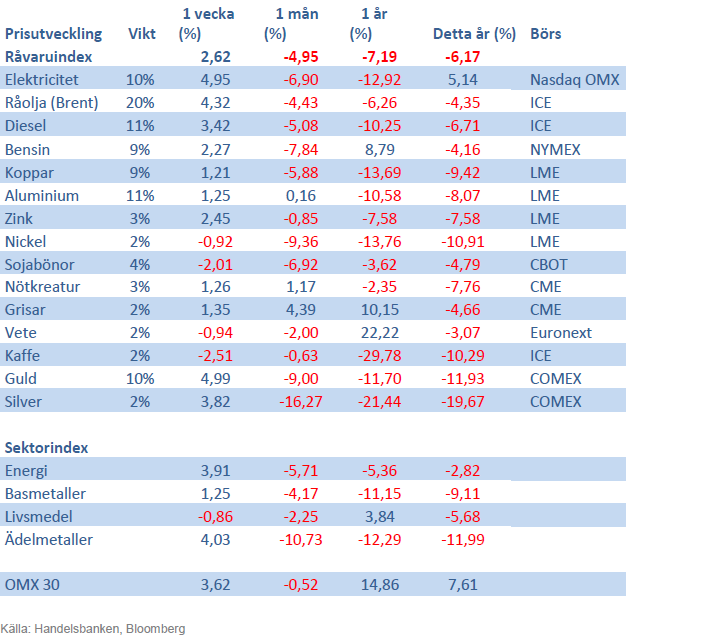

Handelsbankens Råvaruindex

Handelsbankens råvaruindex består av de underliggande indexen för respektive råvara. Vikterna är bestämda till hälften från värdet av global produktion och till hälften från likviditeten i terminskontrakten.

[box]SHB Råvarubrevet är producerat av Handelsbanken och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta material är producerat av Svenska Handelsbanken AB (publ) i fortsättningen kallad Handelsbanken. De som arbetar med innehållet är inte analytiker och materialet är inte oberoende investeringsanalys. Innehållet är uteslutande avsett för kunder i Sverige. Syftet är att ge en allmän information till Handelsbankens kunder och utgör inte ett personligt investeringsråd eller en personlig rekommendation. Informationen ska inte ensamt utgöra underlag för investeringsbeslut. Kunder bör inhämta råd från sina rådgivare och basera sina investeringsbeslut utifrån egen erfarenhet.

Informationen i materialet kan ändras och också avvika från de åsikter som uttrycks i oberoende investeringsanalyser från Handelsbanken. Informationen grundar sig på allmänt tillgänglig information och är hämtad från källor som bedöms som tillförlitliga, men riktigheten kan inte garanteras och informationen kan vara ofullständig eller nedkortad. Ingen del av förslaget får reproduceras eller distribueras till någon annan person utan att Handelsbanken dessförinnan lämnat sitt skriftliga medgivande. Handelsbanken ansvarar inte för att materialet används på ett sätt som strider mot förbudet mot vidarebefordran eller offentliggörs i strid med bankens regler.

Lower as OPEC+ keeps fast-tracking redeployment of previous cuts. Brent closed down 1.3% yesterday to USD 68.76/b on the back of the news over the weekend that OPEC+ (V8) lifted its quota by 547 kb/d for September. Intraday it traded to a low of USD 68.0/b but then pushed higher as Trump threatened to slap sanctions on India if it continues to buy loads of Russian oil. An effort by Donald Trump to force Putin to a truce in Ukraine. This morning it is trading down 0.6% at USD 68.3/b which is just USD 1.3/b below its July average.

Only US shale can hand back the market share which OPEC+ is after. The overall picture in the oil market today and the coming 18 months is that OPEC+ is in the process of taking back market share which it lost over the past years in exchange for higher prices. There is only one source of oil supply which has sufficient reactivity and that is US shale. Average liquids production in the US is set to average 23.1 mb/d in 2025 which is up a whooping 3.4 mb/d since 2021 while it is only up 280 kb/d versus 2024.

Taking back market share is usually a messy business involving a deep trough in prices and significant economic pain for the involved parties. The original plan of OPEC+ (V8) was to tip-toe the 2.2 mb/d cuts gradually back into the market over the course to December 2026. Hoping that robust demand growth and slower non-OPEC+ supply growth would make room for the re-deployment without pushing oil prices down too much.

From tip-toing to fast-tracking. Though still not full aggression. US trade war, weaker global growth outlook and Trump insisting on a lower oil price, and persistent robust non-OPEC+ supply growth changed their minds. Now it is much more fast-track with the re-deployment of the 2.2 mb/d done already by September this year. Though with some adjustments. Lifting quotas is not immediately the same as lifting production as Russia and Iraq first have to pay down their production debt. The OPEC+ organization is also holding the door open for production cuts if need be. And the group is not blasting the market with oil. So far it has all been very orderly with limited impact on prices. Despite the fast-tracking.

The overall process is nonetheless still to take back market share. And that won’t be without pain. The good news for OPEC+ is of course that US shale now is cooling down when WTI is south of USD 65/b rather than heating up when WTI is north of USD 45/b as was the case before.

OPEC+ will have to break some eggs in the US shale oil patches to take back lost market share. The process is already in play. Global oil inventories have been building and they will build more and the oil price will be pushed lower.

A Brent average of USD 60/b in 2026 implies a low of the year of USD 45-47.5/b. Assume that an average Brent crude oil price of USD 60/b and an average WTI price of USD 57.5/b in 2026 is sufficient to drive US oil rig count down by another 100 rigs and US crude production down by 1.5 mb/d from Dec-25 to Dec-26. A Brent crude average of USD 60/b sounds like a nice price. Do remember though that over the course of a year Brent crude fluctuates +/- USD 10-15/b around the average. So if USD 60/b is the average price, then the low of the year is in the mid to the high USD 40ies/b.

US shale oil producers are likely bracing themselves for what’s in store. US shale oil producers are aware of what is in store. They can see that inventories are rising and they have been cutting rigs and drilling activity since mid-April. But significantly more is needed over the coming 18 months or so. The faster they cut the better off they will be. Cutting 5 drilling rigs per week to the end of the year, an additional total of 100 rigs, will likely drive US crude oil production down by 1.5 mb/d from Dec-25 to Dec-26 and come a long way of handing back the market share OPEC+ is after.

The OPEC+ subgroup V8 this weekend decided to fully unwind their voluntary cut of 2.2 mb/d. The September quota hike was set at 547 kb/d thereby unwinding the full 2.2 mb/d. This still leaves another layer of voluntary cuts of 1.6 mb/d which is likely to be unwind at some point.

Higher quotas however do not immediately translate to equally higher production. This because Russia and Iraq have ”production debts” of cumulative over-production which they need to pay back by holding production below the agreed quotas. I.e. they cannot (should not) lift production before Jan (Russia) and March (Iraq) next year.

Argus estimates that global oil stocks have increased by 180 mb so far this year but with large skews. Strong build in Asia while Europe and the US still have low inventories. US Gulf stocks are at the lowest level in 35 years. This strong skew is likely due to political sanctions towards Russian and Iranian oil exports and the shadow fleet used to export their oil. These sanctions naturally drive their oil exports to Asia and non-OECD countries. That is where the surplus over the past half year has been going and where inventories have been building. An area which has a much more opaque oil market. Relatively low visibility with respect to oil inventories and thus weaker price signals from inventory dynamics there.

This has helped shield Brent and WTI crude oil price benchmarks to some degree from the running, global surplus over the past half year. Brent crude averaged USD 73/b in December 2024 and at current USD 69.7/b it is not all that much lower today despite an estimated global stock build of 180 mb since the end of last year and a highly anticipated equally large stock build for the rest of the year.

What helps to blur the message from OPEC+ in its current process of unwinding cuts and taking back market share, is that, while lifting quotas, it is at the same time also quite explicit that this is not a one way street. That it may turn around make new cuts if need be.

This is very different from its previous efforts to take back market share from US shale oil producers. In its previous efforts it typically tried to shock US shale oil producers out of the market. But they came back very, very quickly.

When OPEC+ now is taking back market share from US shale oil it is more like it is exerting a continuous, gradually increasing pressure towards US shale oil rather than trying to shock it out of the market which it tried before. OPEC+ is now forcing US shale oil producers to gradually back off. US oil drilling rig count is down from 480 in Q1-25 to now 410 last week and it is typically falling by some 4-5 rigs per week currently. This has happened at an average WTI price of about USD 65/b. This is very different from earlier when US shale oil activity exploded when WTI went north of USD 45/b. This helps to give OPEC+ a lot of confidence.

Global oil inventories are set to rise further in H2-25 and crude oil prices will likely be forced lower though the global skew in terms of where inventories are building is muddying the picture. US shale oil activity will likely decline further in H2-25 as well with rig count down maybe another 100 rigs. Thus making room for more oil from OPEC+.

The latest weekly report from the US DOE showed a substantial drawdown across key petroleum categories, adding more upside potential to the fundamental picture.

Commercial crude inventories (excl. SPR) fell by 5.8 million barrels, bringing total inventories down to 415.1 million barrels. Now sitting 11% below the five-year seasonal norm and placed in the lowest 2015-2022 range (see picture below).

Product inventories also tightened further last week. Gasoline inventories declined by 2.1 million barrels, with reductions seen in both finished gasoline and blending components. Current gasoline levels are about 3% below the five-year average for this time of year.

Among products, the most notable move came in diesel, where inventories dropped by almost 4.1 million barrels, deepening the deficit to around 20% below seasonal norms – continuing to underscore the persistent supply tightness in diesel markets.

The only area of inventory growth was in propane/propylene, which posted a significant 5.1-million-barrel build and now stands 9% above the five-year average.

Total commercial petroleum inventories (crude plus refined products) declined by 4.2 million barrels on the week, reinforcing the overall tightening of US crude and products.

Guld stiger till över 3500 USD på osäkerhet i världen

Lyten, tillverkare av litium-svavelbatterier, tar över Northvolts tillgångar i Sverige och Tyskland

Lundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

Alkane Resources och Mandalay Resources har gått samman, aktör inom guld och antimon

Breaking some eggs in US shale

USA inför 93,5 % tull på kinesisk grafit

Fusionsföretag visar hur guld kan produceras av kvicksilver i stor skala – alkemidrömmen ska bli verklighet

Westinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

Ryska militären har skjutit ihjäl minst 11 guldletare vid sin gruva i Centralafrikanska republiken

Eurobattery Minerals förvärvar majoritet i spansk volframgruva

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUSA inför 93,5 % tull på kinesisk grafit

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFusionsföretag visar hur guld kan produceras av kvicksilver i stor skala – alkemidrömmen ska bli verklighet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanWestinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanRyska militären har skjutit ihjäl minst 11 guldletare vid sin gruva i Centralafrikanska republiken

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanEurobattery Minerals förvärvar majoritet i spansk volframgruva

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanKopparpriset i fritt fall i USA efter att tullregler presenterats

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanLundin Gold rapporterar enastående borrresultat vid Fruta del Norte

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKina skärper kontrollen av sällsynta jordartsmetaller, vill stoppa olaglig export