Analys

SEB – Råvarukommentarer, 29 april 2013

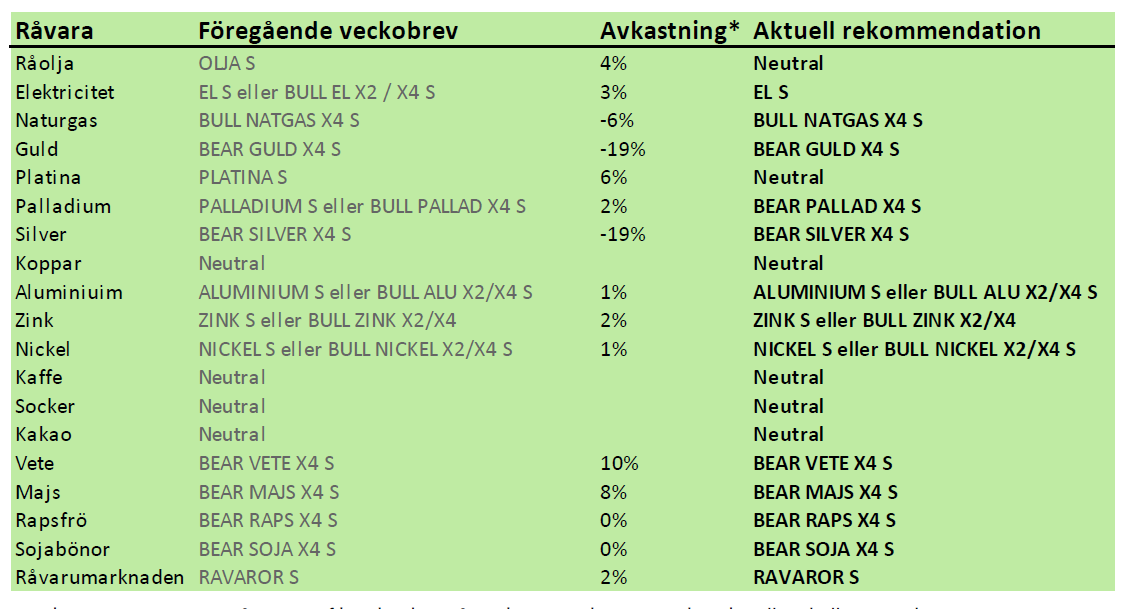

Rekommendationer

*) Avkastningen avser 1:1 råvarucertifikat där de ingår i rekommendationen. I den aktuella tabellen ovan har jag tagit prisförändringen den senaste veckan sedan det förra veckobrevet publicerades.

Inledning

Vi tror att guld, silver, platina och palladium, liksom olja står inför en korrektion nedåt i veckan som kommer. Om detta sker, kan dock priserna ha kommit ner så pass att det kan bli intressant att köpa dem på lite längre sikt.

Sådden av majs i USA har inte kunnat ske på grund av den sena våren. Deadline, som anses vara den 10 maj närmar sig. Väderleksprognosen visar dock ett ”fönster” av gott väder, där sådden kan ske innan dess. De närmaste dagarnas väderutveckling kommer att ha ett avgörande inflytande över prisutvecklingen. Den kinesiska fågelinfluensan har sänkt konsumtionen av kyckling med upp till 80%. Det sänker efterfrågan på sojabönor i världen. Vi tror alltjämt på sjunkande priser på alla jordbruksprodukter. Grispriset i USA testar dock tekniska motståndsnivåer, möjligen just beroende på fågelinfluensan i Kina.

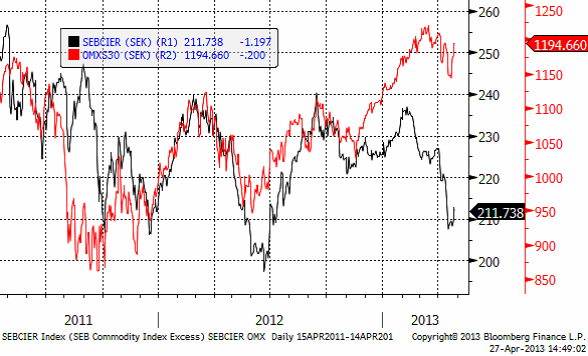

Råvaruindex

I diagrammet nedan ser vi SEB:s råvaruindex i svenska kronor och OMXS30 aktieindex. Båda återhämtade sig i veckan som gick. Vi tror att prisfallen på råvaror kommer att fortsätta i veckan som kommer. Det börjar dock närma sig botten och vi börjar söka efter möjligheter att gå in på köpsidan.

Den som vill investera i indexet och den investeringsstrategi som ligger bakom kan läsa mer om certifikatet RAVAROR S.

Råolja – Brent

Oljepriset rekylerade uppåt i veckan som gick. Vi ser det som en reaktion mot den allmänna pristrenden, och väntar oss att priset vänder ner igen. Vi går därför temporärt ur OLJA S, för att kunna komma in billigare senare.

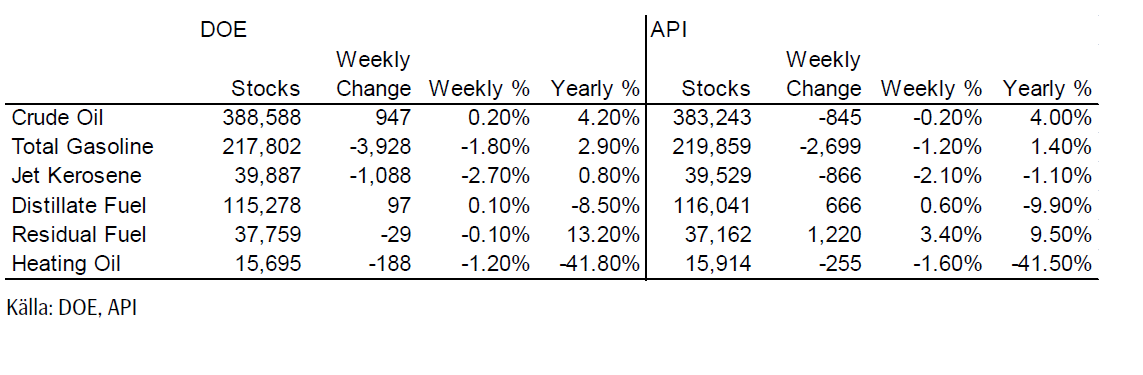

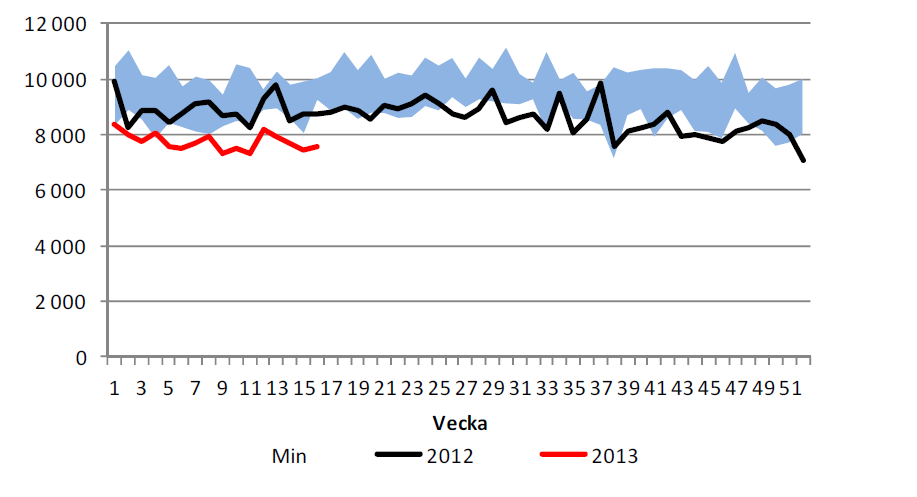

Lagren och lagerförändringarna i USA den senaste rapportveckan ser vi nedan, enligt Department of Energy och American Petroleum Institute. Notera minskningen i råoljelagren!

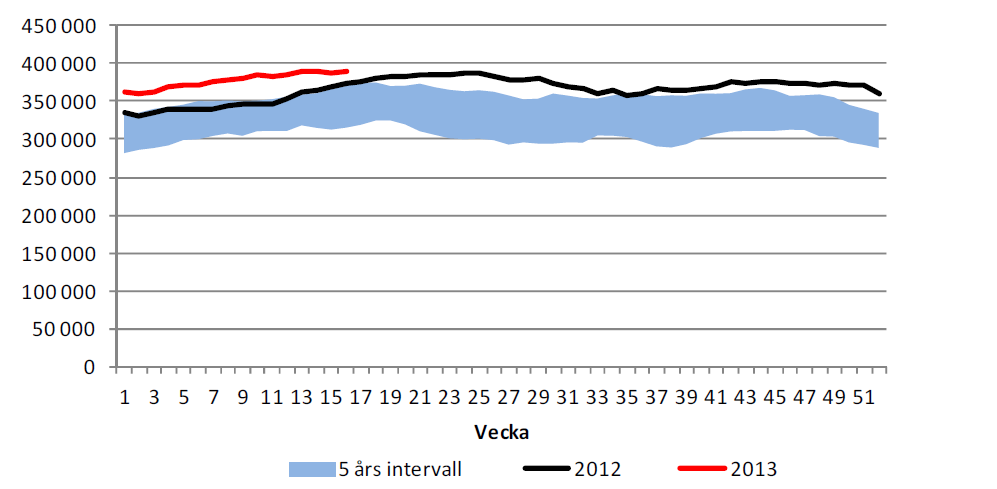

Nedan ser vi amerikanska råoljelager enligt DOE i tusen fat. Den svarta kurvan är 2012 års lagernivåer vecka för vecka och den lilla röda linjen är 2013 års nivå.

Importen har minskat för andra veckan i rad och ligger nu stadigt under 8 mbbl/dag. Vi ligger alltså neutralt i veckan som kommer för att förhoppningsvis kunna komma in billigare i OLJA S.

Elektricitet

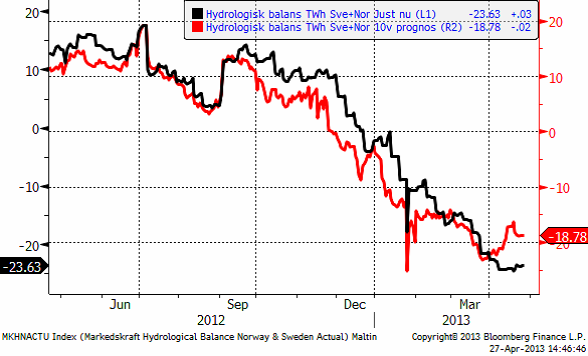

Priset på el rekylerade upp förra veckan. Marknaden står och väger just nu. Hydrologin har planat ut. Det väger ungefär lika tungt i båda vågskålarna för köpsidan och säljsidan. Vi tror dock mer på en stigande trend på lite längre sikt, än att priset ska falla tillbaka nedåt. Därför ligger vi kvar i EL S.

Den hydrologiska balansen har planat ut och prognosen har slutat falla och planat ut den också. Slutsatsen är alltså att vi ligger kvar i EL S.

Naturgas

Nedan ser vi juli-kontraktet på naturgas i USA. Uppgången har mognat ,men vi tror det kommer en sväng uppåt till mot 4.40 dollar per mmBtu. Det kan vara ett bra tillfälle att ta hem vinsten på de köpta BULL NATGAS X4 S vi rekommenderat köp av tidigare.

Guld och Silver

Det har varit hög aktivitet på den svenska marknaden för investeringsguld. I början av veckan var det övervägande köp av GULD S, ett certifikat som följer guldpriset på samma sätt som en guldtacka. Mot slutet av veckan gick placerare ur sina positioner. GULD S och dess familjemedlemmar med högre hävstång, BULL och BEAR, går att använda för kortsiktigare handel än fysiskt guld eftersom transaktionskostnaden är så låg. Vi kan tolka marknadens beteende som att den tror på lägre priser på kort sikt. Samtidigt har vi kunnat läsa rapporter om att såväl the US Mint som Storbritanniens motsvarighet sålt slut på sitt fysiska guld. Långsiktiga investerare tror alltså att priset är lågt nu.

Vi tror också att priset kortsiktigt kommer att vända ner och testa den lägsta noteringen i april. Marknadspsykologins två drivkrafter rädsla och hopp spelar stor roll här. Det är väldigt få personer i samhället som äger guld som en finansiell placering, men för dem som gör det är det sannolikt en stor del av portföljen. Det beror bland annat på att guldpriset stigit så mycket i värde, samtidigt som aktier och andra tillgångar inte gjort det. Många guldinvesterare upplever det här prisfallet på samma sätt som aktiesparare upplevde börskrascherna 1987, 2001 och 2008, dvs med rädsla för att förlora mycket pengar. Att förlora mycket pengar ger större utslag på känslomätaren än att vinna lika mycket pengar. Det vore därför fullständigt naturligt om många nu väljer att minska sina placeringar, när priset har repat sig från bottennoteringarna efter prisraset med 100 dollar per ozt. Även långsiktiga köpare av fysisk metall borde tycka att 100 dollar mer än för ett par veckor sedan är i dyraste laget.

Man ser ofta den här typen av rekyl efter ett initialt prisfall. Det följs i regel, men inte alltid, av ytterligare en nedgångsfas. Ska man gissa, så måste man därför gissa, att priset kommer att vända ner nu igen och att vi står inför ytterligare en rejäl prisnedgång.

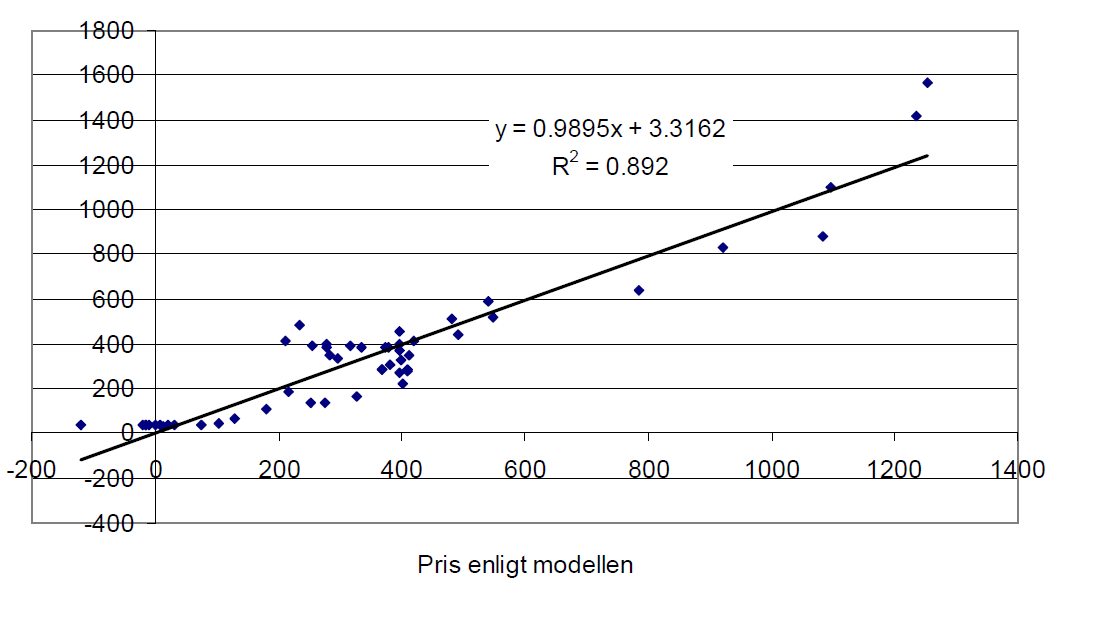

Vi kan dock notera att långsiktigt förklaras guldpriset av demografiska faktorer – ökade inkomster i tillväxtländer. Nedan ser vi guldpriset förklarat av BNP i länder med BNP / capita mellan 2000 och 13000 dollar i dagens penningvärde. Varje punkt markerar ett år sedan 1960 till 2011.

De två högsta noteringarna avser åren 2010 och 2011. Vi ser att dessa år ligger priset på guld över den långsiktiga relationen för BNP i dessa länder. Det beror, skulle jag hävda på ökningen av penningmängden, framförallt i USA. Quantitative Easing, har skapat pengar att parkera någonstans och med en ränta nära noll är inte alternativkostnaden för en placering i guld så hög.

Man ska också reflektera över att den här ”demografiska” indikatorn, som förklarar guldprisets nivå så väl, kommer att minska när Kina går över 13000 dollar i BNP per capita, på samma sätt som skedde på tidigt 80-tal när den stora populationen i Europa, Japan och USA gick över 13000 dollar i BNP per capita och började konsumera tjänster i stället för att öka efterfrågan på råvaror / saker när de fick mer pengar. Det är dock ännu många år innan Kinas tillväxt har tagit BNP / capita över den nivån och det talar för ett fortsatt högt guldpris ännu ett tag.

Produktionskostnaden ligger strax under dagens pris. Gruvbolaget Newmont säger att ”all-in sustaining cash costs” är 1,100 – 1,200 dollar / ozt. Barrick säger att det är 1,000 – 1,100 dollar. IamGold, som är en högkostnadsproducent, ligger på 1,558 dollar. Det kanadensiska bolaget Dundee Capital Markets gjorde en sammanställning av ”all-in cost”. De säger att medelvärdet för de 20 största producenterna är 1,306 dollar. På basis av en kostnadskurva publicerad den 4 april i ”GFMS Gold Survey 2013” kan vi utläsa att så mycket som 20% av alla gruvor är olönsamma vid den här prisnivån. Tendensen att minska utbudet och få marknadens utbud mer i balans med efterfrågan borde få priset att hitta stöd inte långt under dagens guldpris.

Nedan ser vi kursdiagrammet för silver i dollar per troy ounce.

Vi ligger korta guld och silver. Det har kostat i veckan som gick, men eftersom vi tror att det kommer en till vända ner, ligger vi självklart kvar med köpt position i BEAR GULD X4 S och BEAR SILVER X4 S.

Platina & Palladium

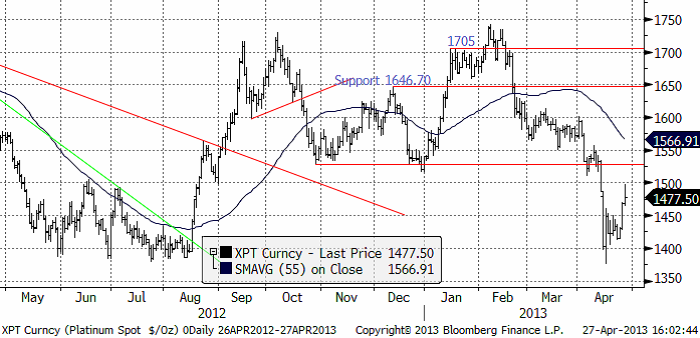

Platinapriset har rekylerat uppåt, i likhet med guld och silver. Vi tror att det handlar om en rekyl mot den allmänna pristrenden och därför ett bra tillfälle att temporärt stänga positioner i Platina.

Prisfallet i palladium har stannat av och inte lyckats ta sig uppåt. Det ser ännu svagare ut än de andra. Vi tvingas därför vänta fot och gå kort. Rekommendationen ändras alltså till köp av BEAR PALLAD X4 S. Målkursen är 600 dollar.

Basmetaller

Prissättningen av derivat på metallmarknaden indikerar en ökad volatilitet. Något som också visat sig i faktiska prisrörelser under veckan. Veckan inleddes som väntat svagare, men köparna kom in kring stödnivåerna och vi såg en rejäl uppgång i mitten av veckan. Det såg stabilt ut vid lunchtid i fredags. Den amerikanska BNP-siffran fick dock marknaderna att surna till på eftermiddagen (+2,5 % för Q1 mot väntat 3.0). Sent på kvällen såldes metallerna ner kraftigt, delvis p.g.a. positionskorrigeringar inför Kinas långhelg (stängt i 3 dagar i samband med 1:a maj). En stor del av veckouppgången raderades snabbt ut.

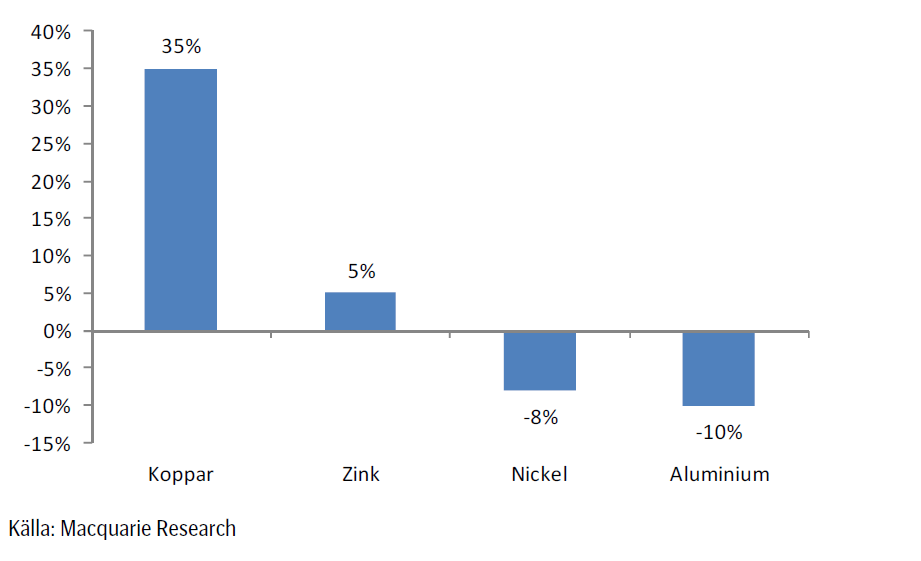

Vi tidigare skrivit om metallernas olika läge med tanke på pris i förhållande till kostnader. Alu, zink och nickel befinner sig i närheten kostnadsnivån för de 10 % producenterna med högst kostnader, d.v.s. där produktion på marginal blir olönsam, och därmed förr eller senare faller bort (se diagram nedan).

Diagrammet nedan visar metallpriset i förhållande till produktionskostnadskurvans 90%-percentil.

Som vi också återkommande skrivit om, ligger fortfarande kopparpriset högt i förhållande till kostnaderna för att producera metallen. Koppar brukar betraktas som den ledande metallen (LME:s flaggskepp). Kinas stora kopparbehov har förstärkt den positionen. Det är också till stor del Kinas importbehov som skapat ”premien”. När Kina sviktar, ja då sviktar kopparn. Utbudet ökar också nu efter att i flera år ha släpat efter. Dessutom har det finansiella kollektivet tagit fasta på läget och positionerat sig för nedgång. Tekniskt sett har man nu fått ”vatten på sin kvarn”. Så länge stämningsläget är negativt gentemot kopparn blir det svårt för övriga metaller att ta fart. Kopparn har behövt en korrigering, och det är den vi ser nu. Den stora frågan för hela metallmarknaden blir därför hur lågt kan kopparn gå?

Koppar

Vi skrev i förra veckan att det dags att börja bevaka en eventuell vändning. Priset tog sig upp till motståndsnivåerna kring $7200. Veckan stänger upp 1,4 % trots fredagens utförsäljning inför den kinesiska långhelgen.

Tekniskt sett så (se grafen nedan) kommer nästa stor stödnivå in kring $6500. I vårt tycke har marknaden förmodligen korrigerat tillräckligt, med en anpassning till den ”nya” fundamentala situationen. Det blir nu extra intressant att följa Kinas import. Prisskillnaden mellan LME och Shanghai är till LME:s fördel, vilket brukar ledan till att kineserna ”passar på” att köpa. Frågan är dock hur stark efterfrågan är lokalt i Kina. Marknaden är lite tveksam. Vi bevakar nu kopparn och förbereder oss för att vända från neutral till köp.

Den tekniska bilden har gett stöd till vår neutrala position. Vi är positiva till basmetaller på sikt men har avvaktat bättre köptillfällen alternativt väljer någon annan basmetall. Vi bevakar nu den nya stödnivån kring $6500.

Som vi skrivit tidigare tyder mycket på ökat utbud för koppar, vilket riskerar att begränsa uppgångspotentialen. Vi rekommenderar fortsatt en neutral position, men sätter koppar på bevakning för köp. För den som vill satsa på ett starkare tillväxtscenario (än konsensus) i Kina är koppar däremot alltid ett intressant alternativ.

Aluminium

Aluminium har visat styrka ett par veckor i samband med svagheten för koppar. Varje ”dipp” under $1900 har mött starkt köpintresse från industriella aktörer. I fredags såg det länge ut som vi skulle få en stark stängning över den första motståndsnivån kring $1930. Prisfallet för metaller generellt på fredagskvällen tog dock ner metallen förvånansvärt mycket, ända ned till $1878. Veckan kommer att inledas med ett nytt bra köpläge. För den riskbenägne kan det vara läge för att köpa ett kontrakt med hävstång (BULL ALU X2 eller X4). Långsiktigt är nivån väldigt intressant för kontraktet Aluminium S (utan hävstång).

Zink

Zinken följde i stort sett övriga metaller under veckan, och får en ganska neutral stängning på veckan. Produktionsstatistik från Kina är lite oroväckande för zinkens fundamentala balans. Smältverksproduktionen ökar i Kina, delvis som en effekt av stort gruvutbud (höjda smältlöner till smältverken). Risken finns att det behövs ännu lägre priser för att påverka gruvutbudet. Risken är att det dröjer innan priset vänder upp på allvar. Vi bedömer ändå zinken som fundamentalt ”billig” ur ett kostnadsperspektiv och nuvarande nivåer är mycket intressanta på lite längre sikt (6-12 månader). I det perspektivet är Zink S (utan hävstång) att föredra.

Nickel

Även nickel följde den allmänna trenden under veckan. Metallen balanserar farligt nära de viktiga stödnivåerna. Det finns ett lite oroväckande negativt stämningsläge kring nickelmarknaden just nu, baserat på känslan av ett alltför stort överskott (LME-lagret är ett synligt tecken på detta). Den rostfria stålindustrin som förbrukar ca 60 % av allt nickel, vill inte riktigt ta fart. Den förväntade lagerbyggnadsfasen har inte materialiserats under Q1, som den normalt gör. Problemet är delvis att tillgången i Kina är alltför god med tanke på utbudet av nickel Pig Iron. Det kan därför ta lite längre tid än beräknat. Vi bedömer ändå nivåerna som väldigt intressant ur ett kostnadsperspektiv (den första produktionen som förväntas tas ur marknaden är just Nickel Pig Iron i Kina). Frågan är om det finns utrymmer för ett brott om $15000. Vi studerar därför det långsiktiga veckodiagrammet nedan. Med nuvarande fundamentala situation har vi väldigt svårt att se marknaden gå ner till 2008-års katastrofnivåer (då efterfrågan mer än halverades). Om vi får en dipp under $15000 tror vi den blir kortvarig, och ett ypperligt köpläge av en metall som på sikt har stor uppgångspotential.

Kaffe

Kaffepriset (maj 2013) vände tvärt ner efter att Starbucks sade att de är försiktiga med inköpen och bara köper så mycket som behövs för stunden. Det indikerar att de tror på lägre priser på kaffe.

Conselho Nacional do Café, en sammanslutning av brasilianska kaffebönder, har bett regeringen i Brasilia om “akut” stöd. Värdet av den brasilianska kaffeproduktionen har halverats till ca 8 miljarder dollar i år. Kaffeodling är den verksamhet som sysselsätter flest människor på den brasilianska landsbygden. Sockerrörsodling, som också drabbats av fallande priser, är inte alls lika arbetsintensivt. För två år sedan besökte jag gården Café Héléna i delstaten São Paulo. Gården på 100 ha sysselsatte 14 personer på heltid. Enligt Conselho Nacional do Café har 655,000 familjer sin utkomst från kaffeodlingen.

Av 2012 års skörd är ungefär 70% sålt nu och ett normalt år borde det 90% redan vara sålt. Av 2013 års skörd är bara 10% sålt, medan det normalt sett borde vara 30%.

Socker

Sockerpriset (september 2013) fortsätter att rasa, med ytterligare ett kliv nedåt i veckan som gick. Sockerrör har blivit en populär gröda i Brasilien och trängt undan kaffeodling. Klondyke-stämningen i sockerproduktionen har nu gått över och det börjar talas om konkurser för svagare ”crushers”. Möjligen kan detta också bli ett tecken på botten för priserna när det sker.

Vi fortsätter med neutral rekommendation.

[box]SEB Veckobrev Veckans råvarukommentar är producerat av SEB Merchant Banking och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Disclaimer

The information in this document has been compiled by SEB Merchant Banking, a division within Skandinaviska Enskilda Banken AB (publ) (“SEB”).

Opinions contained in this report represent the bank’s present opinion only and are subject to change without notice. All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, expressed or implied, is made with respect to the completeness or accuracy of its contents and the information is not to be relied upon as authoritative. Anyone considering taking actions based upon the content of this document is urged to base his or her investment decisions upon such investigations as he or she deems necessary. This document is being provided as information only, and no specific actions are being solicited as a result of it; to the extent permitted by law, no liability whatsoever is accepted for any direct or consequential loss arising from use of this document or its contents.

About SEB

SEB is a public company incorporated in Stockholm, Sweden, with limited liability. It is a participant at major Nordic and other European Regulated Markets and Multilateral Trading Facilities (as well as some non-European equivalent markets) for trading in financial instruments, such as markets operated by NASDAQ OMX, NYSE Euronext, London Stock Exchange, Deutsche Börse, Swiss Exchanges, Turquoise and Chi-X. SEB is authorized and regulated by Finansinspektionen in Sweden; it is authorized and subject to limited regulation by the Financial Services Authority for the conduct of designated investment business in the UK, and is subject to the provisions of relevant regulators in all other jurisdictions where SEB conducts operations. SEB Merchant Banking. All rights reserved.

Wild moves yesterday. Brent crude traded to a high of $114.43/b and a low of $96.0/b and closed at $99.94/b yesterday.

US – Iran negotiations ongoing or not? What a day. Donald Trump announced that good talks were ongoing between Iran and the US and that the 48 hour deadline before bombing Iranian power plants and energy infrastructure was postponed by five days subject to success of ongoing meetings. Iranian media meanwhile stated that no meetings were ongoing at all.

Today we are scratching our heads trying to figure out what yesterday was all about.

Friends and family playing the market? Was it just Trump and his friends and family who were playing with oil and equity markets with $580m and $1.46bn in bets being placed by someone in oil and equity markets just 15 minutes before Trump’s announcement?

Was Trump pulling a TACO as he reached his political and economic pain point: Brent at $112/b, US Gas at $4/gal, SPX below 200dma and US 10yr above 4.4%?

Different Iranian factions with Trump talking with one of them? Are there real negotiations going on but with the US talking to one faction in Iran while another, the hardliners, are not involved and are denying any such negotiations going on?

Extending the ultimatum to attack and invade Kharg island next weekend? Or, is the five day delay of the deadline a tactical decision to allow US amphibious assault ships and marines to arrive in the Gulf in the upcoming weekend while US and Israeli continues to degrade Iranian military targets till then. And then next weekend a move by the US/Israel to attack and conquer for example the Kharg island?

We do not really know which it is or maybe a combination of these.

We did get some kind of TACO ydy. But markets have been waiting for some kind of TACO to happen and yesterday we got some kind of TACO. And Brent crude is now trading at $101.5/b as a result rather than at $112-114/b as it did no the high yesterday.

But what really matters in our view is the political situation on the ground in Iran. Will hardliners continue to hold power or will a more pragmatic faction gain power?

If the hardliners remain in power then oil pain should extend all the way to US midterm elections. The hardliners were apparently still in charge as of last week. Iran immediately retaliated and damaged LNG infrastructure in Qatar after Israel hit Iranian South Pars. The SoH was still closed and all messages coming out of Iran indicated defiance. Hardliners continues in power has a huge consequence for oil prices going forward. The regime has played its ’oil-weapon’ (closing or chocking the Strait of Hormuz). It is using it to achieve political goals. Deterrence: it needs to be so politically and economically expensive to attack Iran that it won’t happen again in the future. Or at least that the US/Israel thinks 10-times over before they attack again. The highest Brent crude oil closing price since the start of the war is $112.19/b last Friday. In comparison the 20-year inflation adjusted Brent price is $103/b. So Brent crude last Friday at $112.19/b isn’t a shockingly high price. And it is still far below the nominal high of $148/b from 2008 which is $220/b if inflation adjusted. So once in a lifetime Iran activates its most powerful weapon. The oil weapon. It needs to show the power of this weapon and it needs to reap political gains. Getting Brent to $112/b and intraday high of $119.5/b (9 March) isn’t a display of the power of that weapon. And it is not a deterrence against future attacks.

So if the hardliners remain in power in Iran, then the SoH will likely remain chocked all the way to US midterm elections and Brent crude will at a minimum go above the historical nominal high of $148/b from 2008.

Thus the outlook for the oil price for the rest of the year doesn’t depend all that much of whether Trump pulls a TACO or not. Stops bombing or not. It depends more on who is in charge in Iran. If it is the hardliners, then deterrence against future attacks via chocking of the SoH and high oil prices is the likely line of action. It is impacting the world but the Iranian ’oil-weapon’ is directed towards the US president and the the US midterm elections.

If a pragmatic faction gets to power in Iran, then a very prosperous future is possible. However, if power is shifting towards a more pragmatic faction in Iran then a completely different direction could evolve. Such a faction could possibly be open for cooperation with the US and the GCC and possibly put its issues versus Israel aside. Then the prosperity we have seen evolving in Dubai could be a possible future also for Iran.

So far it looks like the hardliners are fully in charge. As far as we can see, the hardliners are still fully in control in Iran. That points towards continued chocking of the SoH and oil prices ticking higher as global inventories (the oil market buffers) are drawn lower. And not just for a few more weeks, but possibly all the way to the US midterm elections.

A brief sigh of relief yesterday as oil infra at Kharg wasn’t damaged. But higher today. Brent crude dabbled around a bit yesterday in relief that oil infrastructure at Iran’s Kharg island wasn’t damaged. It traded briefly below the 100-line and in a range of $99.54 – 106.5/b. Its close was near the low at $100.21/b.

No easy victorious way out for Trump. So no end in sight yet. Brent is up 3.2% today to $103.4/b with no signs that the war will end anytime soon. Trump has no easy way to declare victory and mission accomplished as long as Iran is in full control of the Strait of Hormuz while also holding some 440 kg of uranium enriched to 60% and not far from weapons grade at 90%. As long as these two factors are unresolved it is difficult for Trump to pull out of the Middle East. Naturally he gets increasingly frustrated over the situation as the oil price and US retail gas prices keeps ticking higher while the US is tied into the mess in the Middle East. Trying to drag NATO members into his mess but not much luck there.

When commodity prices spike they spike 2x, 3x, 4x or 5x. Supply and demand for commodities are notoriously inflexible. When either of them shifts sharply, the the price can easily go to zero (April 2022) or multiply 2x, 3x, or even 5x of normal. Examples in case cobalt in 2025 where Kongo restricted supply and the price doubled. Global LNG in 2022 where the price went 5x normal for the full year average. Demand for tungsten in ammunition is up strongly along with full war in the middle east. And its price? Up 537%.

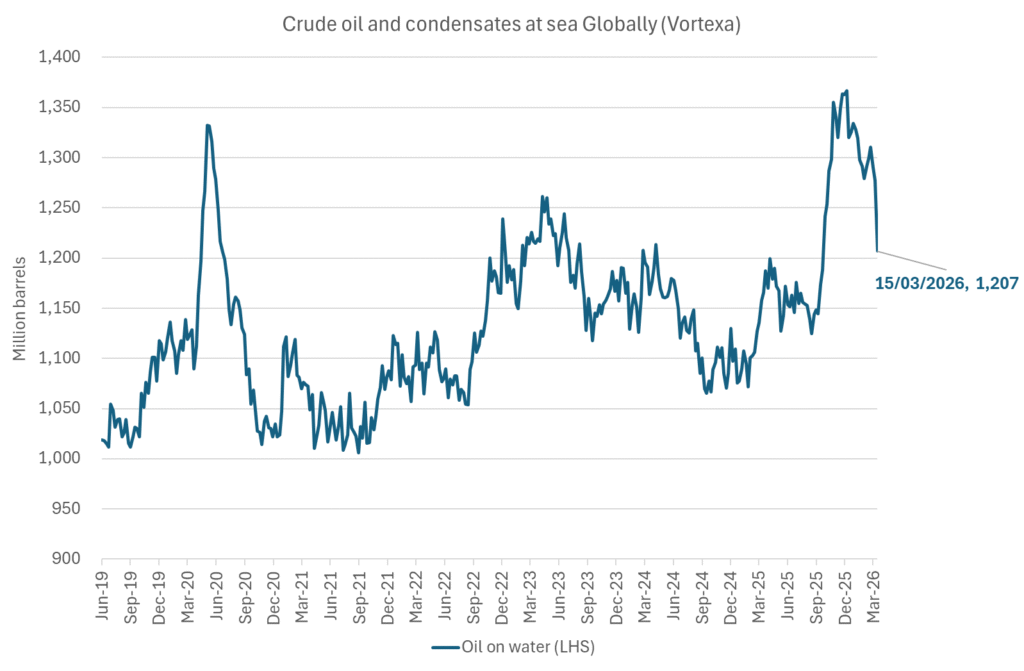

Why hasn’t the Brent crude oil price gone 2x, 3x, 4x or 5x versus its normal of $68/b given close to full stop in the flow of oil of the Strait of Hormuz? We are after all talking about close to 20% of global supply being disrupted. The reason is the buffers. It is fairly easy to store oil. Commercial operators only hold stocks for logistical variations. It is a lot of oil in commercial stocks, but that is predominantly because the whole oil system is so huge. In addition we have Strategic Petroleum Reserves (SPRs) of close to 2500 mb of crude and 1000 mb of oil products. The IEA last week decided to release 400 mb from global SPR. Equal to 20 days of full closure of the Strait of Hormuz. Thus oil in commercial stocks on land, commercial oil in transit at sea and release of oil from SPRs is currently buffering the situation.

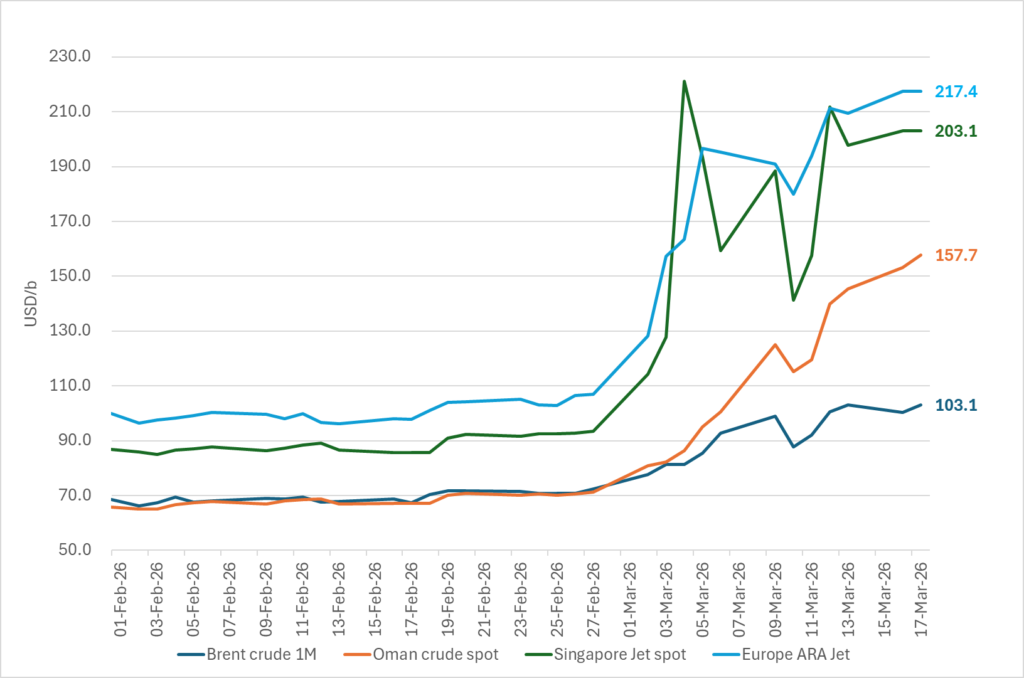

But we are running the buffers down day by day. As a result we see gradually increasing stress here and there in the global oil market. Asia is feeling the pinch the most. It has very low self sufficiency of oil and most of the exports from the Gulf normally head to Asia. Availability of propane and butane many places in India (LPG) has dried up very quickly. Local prices have tripled as a result. Local availability of crude, bunker oil, fuel oil, jet fuel, naphtha and other oil products is quickly running down to critical levels many places in Asia with prices shooting up. Oman crude oil is marked at $153/b. Jet fuel in Singapore is marked at $191/b.

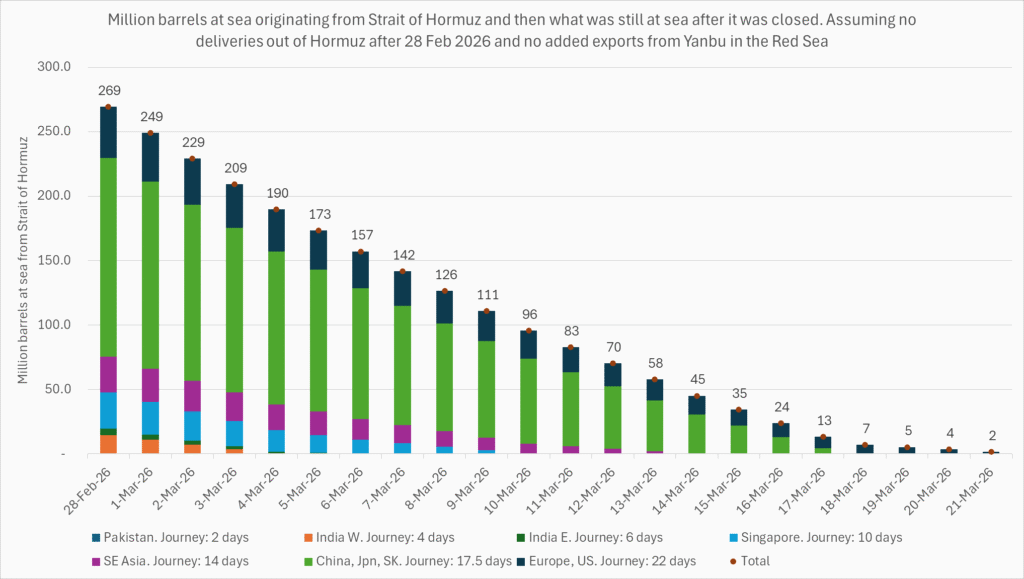

Oil at sea originating from Strait of Hormuz from before 28 Feb is rapidly emptied. Oil at sea is a large pool of commercial oil. An inventory of oil in constant move. If we assume that the average journey from the Persian Gulf to its destinations has a volume weighted average of 13.5 days then the amount of oil at sea originating from the Persian Gulf when the the US/Israel attacked on 28 Feb was 13.5 days * 20 mb/d = 269 mb. Since the strait closed, this oil has increasingly been delivered at its destinations. Those closest to the Strait, like Pakistan, felt the emptying of this supply chain the fastest. Propane prices shooting to 3x normal there already last week and restaurants serving cold food this week is a result of that. Some 50-60% of Asia’s imports of Naphtha normally originates from the Persian Gulf. So naphtha is a natural pain point for Asia. The Gulf also a large and important exporter of Jet fuel. That shut in has lifted jet prices above $200/b.

To simplify our calculations we assume that no oil has left the Strait since that date and that there is no increase in Saudi exports from Yanbu. Then the draining of this inventory at sea originated from the Persian Gulf will essentially look like this:

The supply chain of oil at sea originating from the Strait of Hormuz is soon empty. Except for oil allowed through the Strait of Hormuz by Iran and increased exports from Yanbu in the Red Sea. Not included here.

Oil at sea is falling fast as oil is delivered without any new refill in the Persian Gulf. Waivers for Russian crude is also shifting Russian crude to consumers. Brent crude will likely start to feel the pinch much more forcefully when oil at sea is drawn down another 200 mb to around 1000 mb. That is not much more than 10 days from here.

Oil and oil products are starting to become very pricy many places. Brent crude has still been shielded from spiking like the others.

Closing at highest since Aug 2022. Brent crude gained 9.2% yesterday. The trading range was limited to $95.2 – 101.85/b with a close at $100.46/b and higher than the Monday close of $98.96/b. Ydy close was the highest close since August 2022. This morning Brent is up 2% to $102.4/b and is trading at the highest intraday level since Monday when it high an intraday high of $119.5/b.

A military hit at Iran’s Kharg island would be a big, big bang for the oil price. The big, big risk for the weekend is that oil infrastructure could be damaged. For example Iran’s Kharg island which is Iran’s major oil export hub. If damaged we would have a longer lasting loss of supply stretching way beyond Trump’s announced ”two more weeks”. It will make the spot price spike higher and it will lift the curve. Brent crude 2027 swap would jump above $80/b immediately. An attack on Kharg island would naturally lead Iran to strike back at other oil infrastructures in the Gulf. Especially those belonging to countries who harbor US military bases. I.e. countries who essentially are supporting the attack by US and Israel towards Iran. Though if not in spirit, then in practical operational terms. An attack on Kharg island would not just lead to a lasting outage of supply from Iran until it would be repaired. It would immediately endanger other oil infrastructure in the region as well and additional lasting loss of supply.

No one in their right mind would dare to sit short oil over the coming weekend. Oil is thus set to close the week at a very strong note today.

Prepare for another 400 mb SPR release next week. This week’s announcement of a 400 mb release from Strategic Oil Reserves totally underwhelmed the market with the oil price going higher rather than lower following the announcement. For one it means that the market expects the war and the closure of the Strait of Hormuz to last longer than Trump’s recent announced ”two more weeks”. 400 mb only amounts to 20 days of lost supply to the world through Hormuz and we are already at day 14. So next week when we are getting close to the 20 day mark, we are likely to see another announcement of another 400 mb release of SPR stocks to the market. Preparing for the next 20 days of war.

Global oil logistics in total disarray. We have previously addressed the issue of the huge logistical web of the global oil market which is now in total disarray. The logistical disruption started to fry the oil market at the end of last week. Helped to spike the oil market on Monday. What we hear from our shipping clients is that the problems with supply of fuels locally in Korea, Singapore, India and Africa are getting worse with physical availability of fuels there drying up. It is getting increasingly difficult to find physical supply of bunker oil with local, physical prices shooting way higher than financial benchmarks. To the point that biofuels have become the cheap option many places. Availability of fuels in the US is still good. Not so surprising as the US is self-sufficient with crude and refineries.

The disruption in global oil logistics doesn’t seem to improve. Rather the opposite. If you cannot get fuel to run your ships, then how can you distribute fuels to where it is needed.

Buy Brent Dec-2026 calls with strike $150/b!! As the days goes by the oil price is ticking higher while Trump is getting one day closer to US midterm elections. Trump was betting that he could put this war to bead well before November. But that will probably not be up to him to decide. It will be up to Iran to decide when to reopen the Strait of Hormuz. It is very hard to imagine that Iran will let Trump easily off the hock after he has killed its Supreme Leader. This will likely go all the way to November. Buy Brent Dec-2026 calls with strike $150/b!!

Brent closed at highest since 2022 ydy. Will end this Friday at a very strong note! Consumers still dreaming of $60/b oil

Christian Kopfer om läget för oljan

Marknaden måste börja betrakta de höga kopparpriserna som det nya normala

Det fysiska spotpriset på brentolja har slagit nytt rekord

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

Efter tillväxten: Guldbrev satsar på expansion i Europa

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

Elpriserna fördubblas, stor osäkerhet inför sommaren

MP Materials, USA:s svar på Kinas dominans över sällsynta jordartsmetaller

Det fysiska spotpriset på brentolja har slagit nytt rekord

Studsvik har idag ansökt om att få bygga 1200-1600 MW kärnkraft i Valdemarsvik

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanElpriserna fördubblas, stor osäkerhet inför sommaren

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMP Materials, USA:s svar på Kinas dominans över sällsynta jordartsmetaller

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDet fysiska spotpriset på brentolja har slagit nytt rekord

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanStudsvik har idag ansökt om att få bygga 1200-1600 MW kärnkraft i Valdemarsvik

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMarknaden måste börja betrakta de höga kopparpriserna som det nya normala

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMatproduktion är beroende av gödsel, Gulfkriget skapar brist

-

Analys4 veckor sedan

TACO (or Whatever It Was) Sends Oil Lower — Iran Keeps Choking Hormuz