Analys

SIP Nordic – Råvaruguiden – Mars 2012

Några villor fyllda med guld

Några villor fyllda med guld

I början av 2011 publicerades en artikel om Sveriges dyraste villor som var ute till försäljning. De fyra dyraste villorna hade ett sammanlagt försäljningspris på runt 1,4 miljarder. En stor summa, men det skulle inte på långa vägar räcka till att köpa all världens guld.

Det som dock är intressant är att all världens guld skulle få plats i dessa villor. Denna månads krönika går i fysikens och matematikens tecken. Varje år produceras 50 miljoner troy ounces guld.

Trots att vi sedan urminnes tider producerat guld så antar jag att vi haft liknande produktion de senaste 110 åren. Det är självklart en siffra tagen ur luften men med tanke på aztekernas och faraonernas kärlek till guld så tror jag inte att den siffran är helt fel.

Således uppskattar jag den totala mängden tillgängligt guld till 9 miljarder troy ounce guld.

Således finns det ungefär 166 miljoner kg guld i världen. Med dagens guldpris motsvarar detta närmare 67 biljoner kronor.

Det kan låta som en otrolig stor mängd och ett astronomsikt värde men faktum är att guldet skulle kunna få plats i de fyra dyraste villorna ute till försäljning under början av förra året.

Guld har en densitet på 19,3 g/kvadratcentimeter. Detta är ekvivalent med 19,3 kg per liter. Eller 19300 kg per kubikmeter. Med en total tillgänglig mängd på 166 miljoner kg guld får vi att all världens guld upptar en volym om ca 8 600 kubikmeter. Vad detta mynnar ut i är att all världens guld ryms i en kub med sidorna 20,5 meter (20,5*20,5*20,5 = 8 600 m3).

De fyra dyraste villorna, ute till försäljning under 2011, hade en sammanlagd boyta på 2 774 kvadratmeter. Dessa fyra villor skulle alltså få plats med all världens guld (2 774* 3,1 = 8 600 m3). Att ha råd med det är en helt annan femma.

Platina – för dig med mindre boende

Världens platinaproduktion uppgår till 3,6 miljoner troy once per år. Med samma metodik som tidigare skulle all producerat platina vara värt runt 4,7 triljoner kronor. Platina har dock en högre densitet och all världens platinaproduktion är ungefär 556 kubikmeter. Detta motsvarar fyra villor på 46 kvadratmeter vardera.

Guld – Trygg hamn eller inte

- Den positiva korrelationen mellan guld och risk fortsätter.

- Guld har under februari svängt kraftigt. Guldpriset följer således den globala marknadens växlande mellan risk på och risk av, till följd av greklandskrisen.

- Den stärkta euron kontra dollar är också en starkt bidragande orsak till att guldpriset ökat. Ben Bernankes tal i slutet av månaden om långsam återhämtning gav dock guldet en liten törn

Platina

- Den positiva korrelationen med guld hjälper platina. Platina har dock utvecklats något starkare än guld under början av 2012.

- Strejken i Impala Rustenburg gruvorna i Sydafrika, världens största platina gruva, fortsätter och det kommer ta tid innan produktionen återgår till det normala.

- Strejken har lett till en ökning av platinapriset. Det har även hjälpt att minska prisskillnaderna mellan guld och platina.

Silver

- Silverpriset har under februari månad ökat och handlas nu på nivåer vi såg i september förra året. Det är dock drygt 12$ kvar till den höga noteringen 50$ under april förra året.

- Analytikerkåren är överens om att ett stigande silverpris är troligt om utsikterna för den globala ekonomin fortsätter att se mörka ut.

- Vi börjar även se att silver diskuteras flitigt utanför analyskåren – är ett liknande scenario som vi hade under våren 2011 på väg att upprepa sig?

Brent olja

- Oljan har efter en trevande start i januari både återhämtat sig och nått upp till nya höga nivåer under februari.

- Hårda väderförhållanden men framförallt ökad spänning mellan Iran och västvärlden drev oljepriset till toppen 125$ den 24 februari.

- Trots rapporter om ökad tillgång och högre produktion, kyls inte oljepriset ned. Oron i Iran och OPEC länderna bidrar till att oljan behåller sin höga kurs.

- Skillnaden mellan Brent oljan och WTI oljan ökar återigen.

- Prognos på pris år 2012 - Analytikerkonsensus")

Naturgas

- Naturgas närmar sig nu historiskt låga nivåer. Så pass låga att produktionskostnaderna nu närmar sig priset på naturgas.

- Medeltemperaturen har varit högre än vanligt i USA. Däremot spås tillgången av naturgas mer än halveras i USA under 2012.

- Spekulanterna är fortsatt i korta positioner (spekulerar i nedgång) men de börjar successivt köpa tillbaka sina positioner vilket kan tyda på en vändning i marknaden.

Koppar

- Koppar har börjat året starkt efter ett ursvagt 2011. Koppar har gått upp ca. 12% i år. (Att jämföra med -21% under 2011)

- Koppar är mycket konjunkturskänsligt och följer ofta negativa aktietrender. Med den positiva starten på aktiemarknaden följer även koppar med.

- Kina, världens största kopparkonsument, sänkte under februari månad bankernas reservkrav vilket påverkade koppar positivt.

Zink

- Likt koppar har zinkpriset kraftigt stigit under den första månaden av 2012.

- Den årliga konsumtionen av zink förväntas växa med 3.6% samtidigt som tillgången bara förväntas växa med 3%. Det uppskattas dock att nuvarande zinktillgång skulle räcka 7,5 veckor, 0,5 veckor längre än 2011.

- Likt andra basmetaller drivs zinkpriset av att riskaptiten nu ökar och utsikterna för den globala ekonomin är inte lika negativ som under början av året. Något som hjälper basmetallerna uppåt.

Nickel

- Nickel presterade sämst av alla basmetaller under 2011.

- Nickel har dock följt med de andra basmetallerna i den positiva uppgången under januari 2012.

- Produktionen väntas överstiga konsumtionen under 2012.

- Mängden utvunnet nickel förväntas stiga med närmare 10% under 2012.

- Trots att tillgången ökar behöver inte nickelpriset falla. Riskaptiten ökar även bland investerare vilket kan driva råvarupriserna mot högre höjder.

Socker

- Dåliga väderförhållanden i Brasilien har fått analytiker att revidera sockerskörden med nästan 20%.

- Det stigande oljepriset driver sockerpriset uppåt under februari månad. Då oljan ökar även produktionen av etanol, vilket framställs av bland annat sockerrör.

- Köparna har återigen kopplat greppet om sockret. Summan av långa och korta positioner är nu positivt vilket tyder på att spekulanter nu i en högre grad tror på et fortsatt stigande sockerpris.

Bomull

- Bomull rör sig nu sidledsgående trend.

- Viktig nivå för uppgång är 100 $/lb.

- Trots extrem torka i USA har goda skördar i Kina och Indien täckt upp detta bortfall. Skördarna i Kina anses dock bli mindre varför Kina kan vara tvungna att importera bomull. Något som skulle kunna driva bomullspriset över 100$/lb.

- Australien har reviderat ner sin skörd på grund av dåliga väderförhållanden.

Majs

- USDA justerade, i början av året, ned sin prognos för den Argentinska skörden. Från tidigare 29 miljoner ton till 26 miljoner ton. Nu ser det ut som att dåliga väderförhållanden fortsatt kan sätta käppar i hjulet för den argentinska skörden.

- Majs konsoliderar mellan 580 och 670 cent /bushel. Nu börjar majs närma sig motståndet på 670 cent. Frågan är om det bryter upp eller vänder ned.

Vete

- Den globala produktionen av vete spås stiga med 5.3% under första halvåret 2012, samtidigt som efterfrågan endast kommer att öka 3.3%, med ett totalt överskott om 10 miljoner ton.

- Vete har tappat närmre 25% under de senaste året men fortfarande är priset på ca. 6,5 dollar tillräckligt attraktivt för att bönder ska fortsätta plantera. Ett ökande överskott är således att vänta.

- Kalla väderförhållanden i Ukraina kan komma att påverka vetepriset positivt. Nettopositionen, dvs summan av köpare och säljare, är fortsatt negativ. Säljarna har alltså fortfarande grepp om vetet.

Apelsinjuice

- Apelsinjuice har stigit med hela 220% sedan 2009.

- Senaste månaden har priset på apelsinjuice ökat kraftigt till följd av att USDA kan komma att förbjuda import av brasilianskt koncentrat. Svampbekämpningsmedel används flitigt i Brasilien men är förbjudet i USA.

- Skörden spås dock bli väldigt god i Florida samtidigt som rapporter visar att efterfrågan på apelsinjuice minskar.

[box]Denna uppdatering är producerat av SIP Nordic och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta produktblad utgör endast marknadsföring och har sammanställts av SIP Nordic Fondkommission AB.

Innehållet ger inte fullständig information avseende det finansiella instrumentet. Investerare uppmanas att del av prospekt och slutliga villkor, vilka finns tillgängliga på: www.rbsbank.se/markets, innan ett investeringsbeslut tas.

Förekommande exempel är simulerade och baseras på SIP Nordics egna beräkningar och antaganden, en person som använder andra data eller antaganden kan nå andra resultat. Administrativa avgifter och transaktionsavgifter påverkar den faktiska avkastningen.

Strong rebound yesterday with further gains today. Brent crude rallied 3.2% with a close of USD 62.15/b yesterday and a high of the day of USD 62.8/b. This morning it is gaining another 0.9% to USD 62.7/b with signs that US and China may move towards trade talks.

Brent went lower on 9 April than on Monday. Looking back at the latest trough on Monday it traded to an intraday low of USD 58.5/b. In comparison it traded to an intraday low of USD 58.4/b on 9 April. While markets were in shock following 2 April (’Liberation Day’) one should think that the announcement from OPEC+ this weekend of a production increase of some 400 kb/d also in June would have chilled the oil market even more. But no.

’ Technically overbought’ may be the explanation. ’Technically overbought’ has been the main explanation for the rebound since Monday. Maybe so. But the fact that it went lower on 9 April than on Monday this week must imply that markets aren’t totally clear over what OPEC+ is currently doing and is planning to do. Is it the start of a flood or a brief period where disorderly members need to be whipped into line?

The official message is that this is punishment versus quota cheaters Iraq, UAE and Kazakhstan. Makes a lot of sense since it is hard to play as a team if the team strategy is not followed by all players. If the May and June hikes is punishment to force the cheaters into line, then there is very real possibility that they actually will fall in line. And voila. The May and June 4x jumps is what we got and then we are back to increases of 137 kb/d per month. Or we could even see a period with no increase at all or even reversals and cuts.

OPEC+ has after all not officially abandoned cooperation. It has not abandoned quotas. It is still an overall orderly agenda and message to the market. This isn’t like 2014/15 with ’no quotas’. Or like full throttle in spring 2020. The latter was resolved very quickly along with producer pain from very low prices. It is quite clear that Saudi Arabia was very angry with the quota cheaters when the production for May was discussed at the end of March. And that led to the 4x hike in May. And the same again this weekend as quota offenders couldn’t prove good behavior in April. But if the offenders now prove good behavior in May, then the message for July production could prove a very different message than the 4x for May and June.

Trade talk hopes, declining US crude stocks, backwardated Brent curve and shale oil pain lifts price. If so, then we are left with the risk for a US tariff war induced global recession. And with some glimmers of hope now that US and China will start to talk trade, we see Brent crude lifting higher today. Add in that US crude stocks indicatively fell 4.5 mb last week (actual data later today), that the Brent crude forward curve is still in front-end backwardation (no surplus quite yet) and that US shale oil production is starting to show signs of pain with cuts to capex spending and lowering of production estimates.

Rebounding from the sub-60-line for a second time. Following a low of USD 59.3/b, the Brent July contract rebounded and closed up 1.8% at USD 62.13/b. This was the second test of the 60-line with the previous on 9 April when it traded to a low of USD 58.4/b. But yet again it defied a close below the 60-line. US ISM Manufacturing fell to 48.7 in April from 49 in March. It was still better than the feared 47.9 consensus. Other oil supportive elements for oil yesterday were signs that there are movements towards tariff negotiations between the US and China, US crude oil production in February was down 279 kb/d versus December and that production by OPEC+ was down 200 kb/d in April rather than up as expected by the market and planned by the group.

All eyes on OPEC+ when they meet on Monday 5 May. What will they decide to do in June? Production declined by 200 kb/d in April (to 27.24 mb/d) rather than rising as the group had signaled and the market had expected. Half of it was Venezuela where Chevron reduced activity due to US sanctions. Report by Bloomberg here. Saudi Arabia added only 20 kb/d in April. The plan is for the group to lift production by 411 kb/d in May which is close to 3 times the monthly planned increases. But the actual increase will be much smaller if the previous quota offenders, Kazakhstan, Iraq and UAE restrain their production to compensate for previous offences.

The limited production increase from Saudi Arabia is confusing as it gives a flavor that the country deliberately aimed to support the price rather than to revive the planned supply. Recent statements from Saudi officials that the country is ready and able to sustain lower prices for an extended period instead is a message that reviving supply has priority versus the price.

OPEC+ will meet on Monday 5 May to decide what to do with production in June. The general expectation is that the group will lift quotas according to plans with 137 kb/d. But recent developments add a lot of uncertainty to what they will decide. Another triple quota increase as in May or none at all. Most likely they will stick to the original plan and decide lift by 137 kb/d in June.

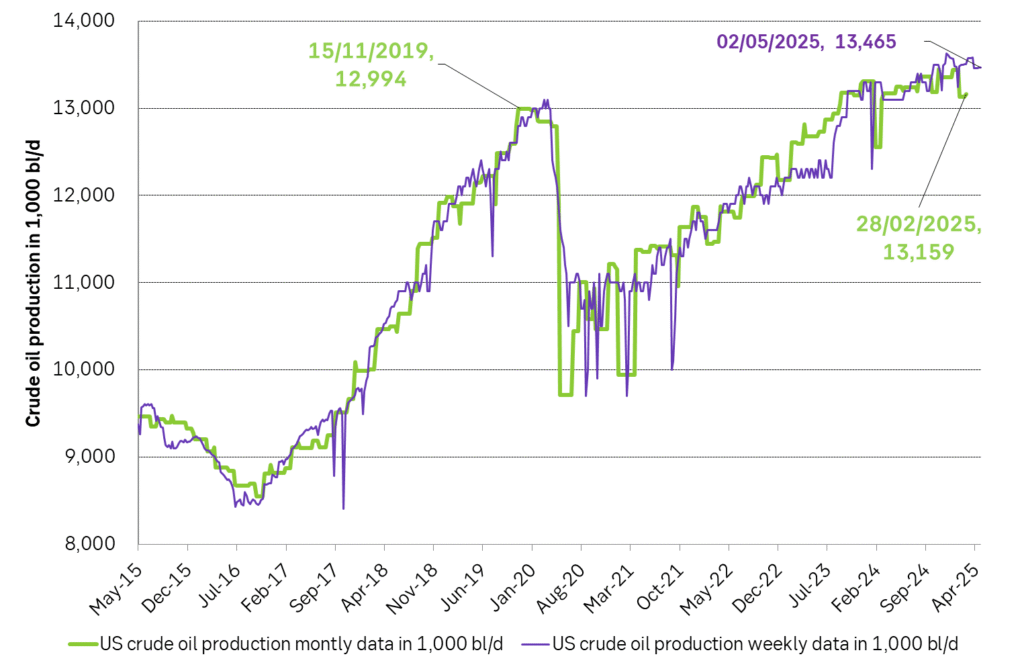

US production surprised on the downside in February. Are prices starting to bite? US crude oil production fell sharply in January, but that is often quite normal due to winter hampering production. What was more surprising was that production only revived by 29 kb/d from January to February. Weekly data which are much more unreliable and approximate have indicated that production rebounded to 13.44 mb/d after the dip in January. The official February production of 13.159 mb/d is only 165 kb/d higher than the previous peak from November/December 2019. The US oil drilling rig count has however not change much since July last year and has been steady around 480 rigs in operation. Our bet is that the weaker than expected US production in February is mostly linked to weather and that it will converge to the weekly data in March and April.

Where is the new US shale oil price pain point? At USD 50/b or USD 65/b? The WTI price is now at USD 59.2/b and the average 13 to 24 mth forward WTI price has averaged USD 61.1/b over the past 30 days. The US oil industry has said that the average cost break even in US shale oil has increased from previous USD 50/b to now USD 65/b with that there is no free cashflow today for reinvestments if the WTI oil price is USD 50/b. Estimates from BNEF are however that the cost-break-even for US shale oil is from USD 40/b to US 60/b with a volume weighted average of around USD 50/b. The proof will be in the pudding. I.e. we will just have to wait and see where the new US shale oil ”price pain point” really is. At what price will we start to see US shale oil rig count starting to decline. We have not seen any decline yet. But if the WTI price stays sub-60, we should start to see a decline in the US rig count.

US crude oil production. Monthly and weekly production in kb/d.

Brent crude falls with strong conviction that trade war will hurt demand for oil. Brent crude sold off 2.4% yesterday to USD 64.25/b along with rising concerns that the US trade war with China will soon start to visibly hurt oil demand or that it has already started to happen. Tariffs between the two are currently at 145% and 125% in the US and China respectively which implies a sharp decline in trade between the two if at all. This morning Brent crude (June contract) is trading down another 1.2% to USD 63.3/b. The June contract is rolling off today and a big question is how that will leave the shape of the Brent crude forward curve. Will the front-end backwardation in the curve evaporate further or will the July contract, now at USD 62.35/b, move up to where the June contract is today?

The unusual ”weird smile” of Brent forward curve implies unusual strong bearish conviction amid current prompt tightness. the The Brent crude oil forward curve has displayed a very unusual shape lately with front-end backwardation combined with deferred contango. Market pricing tightness today but weakness tomorrow. We have commented on this several times lately and Morgan Stanly highlighted how unusual historically this shape is. The reason why it is unusual is probably because markets in general have a hard time pricing a future which is very different from the present. Bearishness in the oil market when it is shifting from tight to soft balance usually comes creeping in at the front-end of the curve. A slight contango at the front-end in combination with an overall backwardated curve. Then this slight contango widens and in the end the whole curve flips to full contango. The current shape of the forward curve implies a very, very strong conviction by the market that softness and surplus is coming. A conviction so strong that it overrules the present tightness. This conviction flows from the fundamental understanding that ongoing trade war is bad for the global economy, for oil demand and for the oil price.

Will OPEC+ switch to cuts or will it leave balancing to a lower price driving US production lower? Add of course also in that OPEC+ has signaled that it will lift production more rapidly and is currently no longer in the mode of holding back to keep Brent at USD 75/b due to an internal quarrel over quotas. That stand can of course change from one day to the next. That is a very clear risk to the upside and oil consumers around should keep that in the back of their minds that this could happen. Though we are not utterly convinced of the imminent risk of this. Before such a pivot happens, Iraq and Kazakhstan probably have to prove that they can live up to their promised cuts. And that will take a few months. Also, OPEC+ might also like to see where the pain-point for US shale oil producers’ price-vise really is today. So far, we have seen no decline in the number of US oil drilling rigs in operation which have steadily been running at around 480 rigs.

With a surplus oil market on the horizon, OPEC+ will have to make a choice. How shale this coming surplus be resolved? Shall OPEC+ cut in order to balance the market or shall lower oil prices drive pain and lower production in the US which then will result in a balanced market? Maybe it is the first or maybe the latter. The group currently has a bloated surplus balance which it needs to slim down at some point. And maybe now is the time. Allowing the oil price to slide. Economic pain for US shale oil producers to rise and US oil production to fall in order to balance the market and make room OPEC+ to redeploy its previous cuts back into the market.

Surplus is not yet here. US oil inventories likely fell close to 2 mb last week. US API yesterday released indications that US crude and product inventories fell 1.8 mb last week with crude up 3.8 mb, gasoline down 3.1 mb and distillates down 2.5 mb. So, in terms of a crude oil contango market (= surplus and rising inventories) we have not yet moved to the point where US inventories are showing that the global oil market now indeed is in surplus. Though Chinese purchases to build stocks may have helped to keep the market tight. Indications that Saudi Arabia may lift June Official Selling Prices is a signal that the oil market may not be all that close to unraveling in surplus.

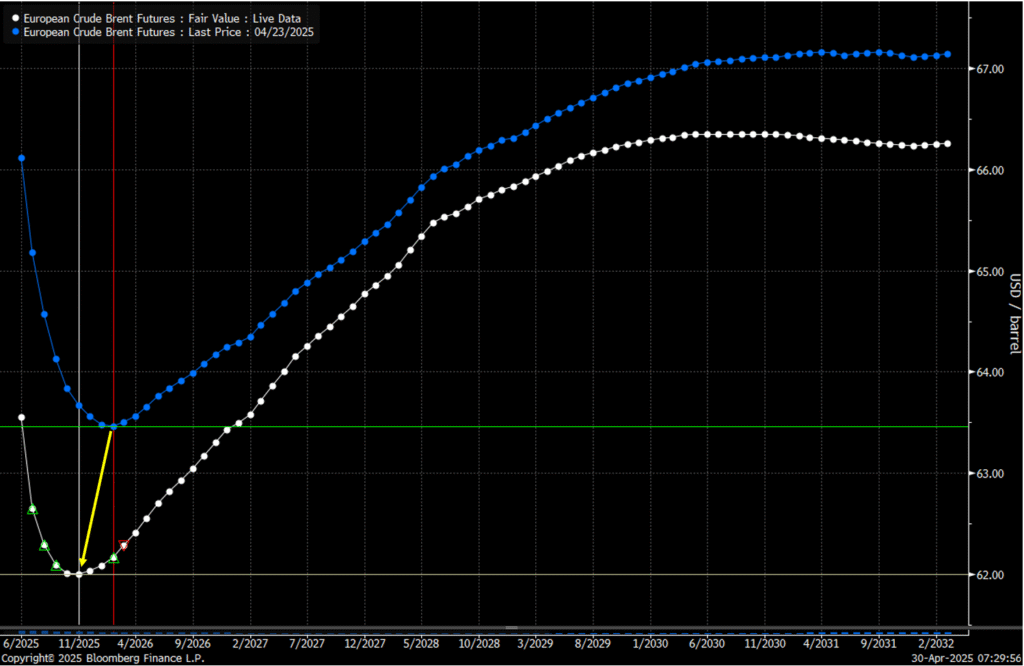

The low point of the Brent crude oil curve is shifting closer to present. A sign that the current front-end backwardation of the Brent crude oil curve is about to evaporate.

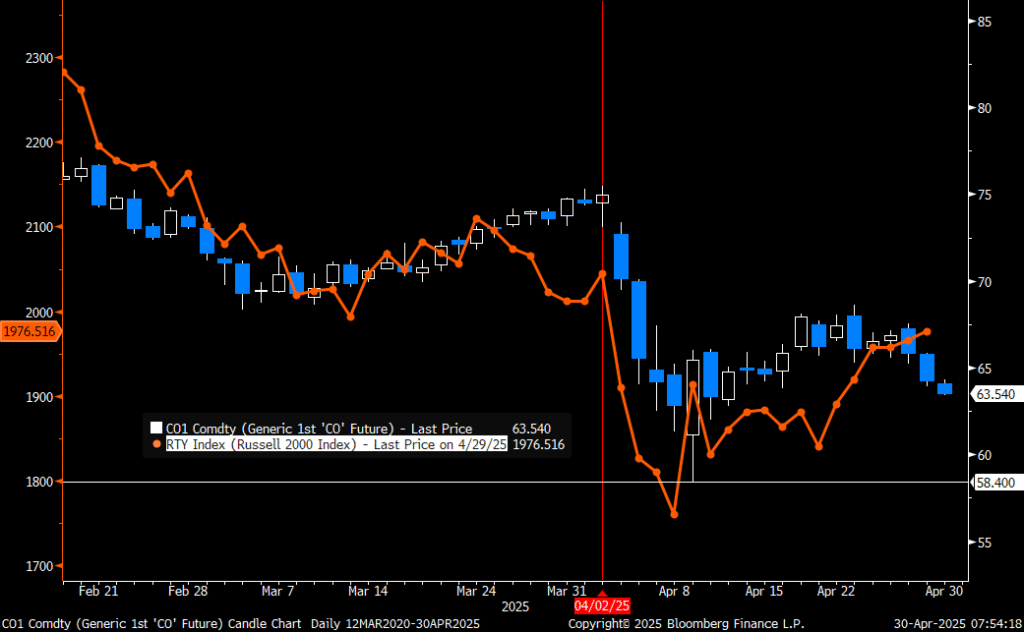

Brent crude versus US Russel 2000 equity index. Is the equity market too optimistic or the oil market too bearish?

Nystart för koppargruvan Viscaria i Kiruna – en av Europas största

Whipping quota cheaters into line is still the most likely explanation

Hur USA blev världens största exportör av propan

Utbudsunderskott och stigande industriell efterfrågan av silver på marknaden

Inflationsjusterat är olja nu billigare än på mitten av 1980-talet

Ingenting stoppar guldets uppgång, nu 3400 USD per uns

Crude oil comment: The forward curve is pricing tightness today and surplus tomorrow

Samtal om läget för guld, kobolt och sällsynta jordartsmetaller

Agnico Eagle siktar på toppen – två av världens största guldgruvor i sikte

Lägre elpriser och många minustimmar fram till midsommar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanIngenting stoppar guldets uppgång, nu 3400 USD per uns

-

Analys2 veckor sedan

Crude oil comment: The forward curve is pricing tightness today and surplus tomorrow

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSamtal om läget för guld, kobolt och sällsynta jordartsmetaller

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAgnico Eagle siktar på toppen – två av världens största guldgruvor i sikte

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanLägre elpriser och många minustimmar fram till midsommar

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKina slår nytt rekord i produktion av kol

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanSaudiarabien informerar att man är ok med ett lägre oljepris

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDen viktiga råvaruvalutan USD faller kraftigt