Nyheter

David Hargreaves on precious metals, Week 1 2012

David Hargreaves

We warned in the 10/12/2011 issue, but three weeks ago, that the precious metals might retreat. They have. We blamed it on the fear factor receding and it has, so let’s not be surprised if we see more on the downside. The world lost an unpredictable dictator in North Korea’s Kim Jong Il last week and the young replacement in the expensive overcoat will take time to learn the ropes. Iran is muttering about blockading the Straits of Hormuz and thus 20% of the world’s traded oil. This need not worry China, 50% dependant, or Japan 75% reliant on that seaway for their oil imports, because it is where the US 5th Fleet sits. That toy factory has enough fire power to turn Tehran into a moon of Saturn, so no fears there, eh? Anglo American might win its spat with Chile’s Codelco over 49% of a juicy copper mine. Britain has warned Argentina that if it gets ambitious about the Falklands again, the nuclear sub patrol will be put on high alert. This is big boy time. Venezuela has most of its gold back home and worth a lot less than when it called for it. Only one dictator to go (hi Bob!) and his threat to embargo platinum exports can only cheer the South Africans. The fear factor has switched from fisticuffs to financial. The further we lever ourselves into recession, the cheaper goods will become and that includes the precious.

Gold

The price run up in H2 owed much to the Euro crisis whilst the spike which saw it momentarily top $1900/oz mirrored fears of a sovereign debt failure. That gold has now subsided to beneath $1550 on the downside does not indicate that problem has been solved. It has been digested. The world would survive a Euro break up and $1500 would still be its highest ever pre Q2 2011 level. We may be still a long drop from a floor in the next few months of which the US dollar, which exerts an opposite pull, continues to remind us.

Investment demand remains the driver. The other two, jewellery and industrial, have been relatively constant since Q2 2010 whilst much has been made of changes in Central Bank holdings. They are relatively small.

The close of 2010 saw a gold price of $1408/oz, registering the 10th successive annual rise. This continued to the short lived peak of $1900 in mid 2011 until the sobering pull back to $1500 on Dec. 30th. The major structural changes have been in private investment demand, particularly in China, India and other developing countries. Central Bank buying has been noted by developing countries but not the expected surge by China. The significance of such holdings is measured not only in their total tonnage, but as a percentage of total foreign assets. By mid 2011 they showed:

Of perhaps greater significance are total above ground stocks of gold, broadly estimated at 163,000 tonnes. Of these, c.84,000 tonnes is held as jewellery. In December a report by MacQuarie Bank suggested India alone accounted for 17,000 tonnes of this. The Chinese and Indians are displaying similar personal buying tendencies.

Supply

The pattern of mined supply remained similar to the previous five years, with the continuing decline of South Africa but increases from West Africa and Eurasia. The major producing countries remained China (13%), USA (11%), Australia (10%), RSA (8%), Russia (7%) and Peru (6%).

Outlook 2012

Gold. Any return to a major upside for gold will be driven by fear factors, not economic ones. The Middle East basin remains highly unstable and a knee-jerk oil price rise would pull gold along. Iran is clearly itching to put on a show, but unless fear becomes reality we do not see gold challenging its highs again, indeed the reverse. For supply it means South Africa may put on hold its plans to revamp the deep basin deposits and for marginal ventures worldwide to struggle with funding. The majors sit on healthy balance sheets, but cannot expect a market rerating. Of the larger ones:

The final day flip in gold (up $45 to $1578/oz) should not be confused with a rally. Only an ungovernable geological or political event is liable to drive it skywards. The world economy will stabilise and we should remember that as recently as 2008, gold was at $700/oz.

Platinum

This was the year the industry got it wrong. If ever a commodity was ripe for cartel action, in theory it is platinum. A single country, South Africa, supplies 75% of all newly mined metal and with Russia does 85% of all the platinum and palladium combined. Only four companies dominate and just two end uses, autocatalysts and jewellery, account for 70% of demand. Yet there is no cartel. London – based free market, daily fixing pricing dominates. That price has fallen progressively in 2011 from an opening $1745/oz to a closing $1407/oz, a fall of 19%. A weak economy, increased output and more intensive recycling, particularly of spent catalysts, were the culprits. Another feature – of longer term significance – was a round of overgenerous wage settlements, which have saddled the South African industry with untenable costs. This is an industry at a crossroads. A small surplus of c. 200,000 oz is calculated for 2011 from a mined supply of 6,400,000 oz and a total demand of 8,100,000 oz. The balance of supply is made up of recycling. Industrial demand is c. 2,000,000 oz and investment c. 500,000 oz.

The shares had a miserable run:

There is nothing to suggest a short term rally, rather further weakness.

Silver

Silver owes its classification ‘precious’ more to its chemical characteristics than its scarcity. It is mined at an annual rate of c. 23,500 tonnes, or ten times that of gold. Yet its price ratio is far higher. Were it in relation to its production, the price of silver would be c. $160/oz, not $30. Its 2010-2011 open and closing levels of $30/oz and $28/oz disguise a run up in Q3 to over $50, prompting some analysts to call for $200.

This is not going to happen. Why?

- The total volume of silver on surface is vastly greater than its production ratio to gold. It has been mined in large quantities for much longer and was for centuries the world’s currency backing.

- Almost 50% is used industrially which, combined with other fabrication and jewellery accounts for c. 85% of all arisings.

- Ten countries combine to produce 80% of newly mined output and vast quantities are available for dishoarding at the right price.

- Most silver is recovered as a by-product of base metal mining, the few pure silver producers including Fresnillo (5.2% market share), Pan American (3.3%), Hochschild (2.4%) and Coeur D’ Alene (2.3%). We believe silver will continue to track gold at a price ratio of 50:1 – 60:1 with a narrowing in a bull market.

[hr]

About David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.

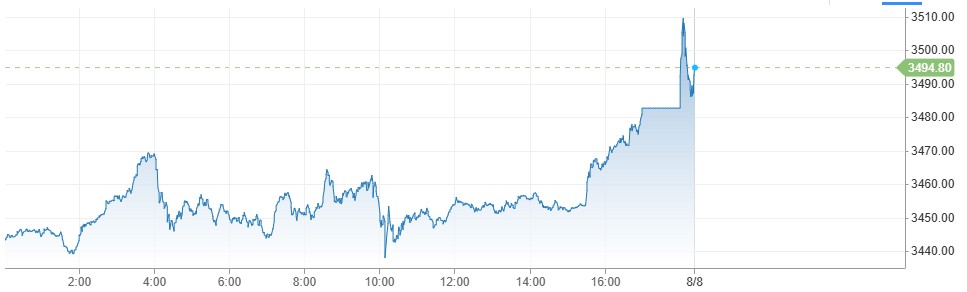

Investerare har den senaste tiden sökt sig till guld som en säker hamn i en konfliktfylld värld. Trumps ständiga attacker på både vänner och fiender har skapat en stor oreda. Med en ökad sannolikhet för en sänkt ränta i USA så blir guld ännu mer tilltalande. Kring midnatt mellan torsdag och fredag svensk tid passerade den gula ädelmetallen 3500 USD per uns på Comex-börsen.

Nyheter

Lyten, tillverkare av litium-svavelbatterier, tar över Northvolts tillgångar i Sverige och Tyskland

Amerikanska Lyten, världsledande inom litium-svavelbatterier, har tecknat ett bindande avtal om att förvärva Northvolts återstående tillgångar i Sverige och Tyskland. I affären ingår batterifabrikerna Northvolt Ett och Ett Expansion i Skellefteå, Northvolt Labs i Västerås samt planerade Northvolt Drei i tyska Heide. Dessutom förvärvas alla immateriella rättigheter (IP) från Northvolt.

De tillgångar Lyten nu tar över har tidigare värderats till cirka 5 miljarder dollar och omfattar 16 GWh i befintlig batteriproduktionskapacitet samt ytterligare 15 GWh under uppbyggnad. Transaktionen, som är helt finansierad med eget kapital från privata investerare, väntas slutföras under det fjärde kvartalet 2025, förutsatt myndighetsgodkännande.

Återstart av verksamheter och jobbtillfällen

Lyten planerar att omedelbart återuppta verksamheten vid anläggningarna i Skellefteå och Västerås efter att affären slutförts. Bolaget har även för avsikt att återanställa en stor del av den personal som tidigare sagts upp från Northvolt och ser långsiktiga sysselsättningsmöjligheter som en nyckel till fortsatt framgång.

– Det här är ett avgörande ögonblick för Lyten. Förvärvet ger oss de anläggningar och den svenska kompetens som krävs för att snabbare möta den kraftigt ökande efterfrågan på våra litium-svavelbatterier, säger Dan Cook, vd och medgrundare av Lyten.

Positivt mottagande från svenska regeringen

Förvärvet välkomnas även från politiskt håll.

– Det här är en vinst för Sverige och för våra ambitioner inom energi och industriell innovation, säger Ebba Busch, Sveriges vice statsminister.

Fortsatt global expansion

Förvärvet i Sverige och Tyskland är en del av Lytens större strategi att bygga en stark närvaro i både Europa och Nordamerika. Tidigare i år har Lyten också köpt Northvolt Dwa i Polen – Europas största tillverkare av batterilagringssystem – samt förvärvat Northvolts IP-portfölj för energilagring. Bolaget har även uttryckt intresse för att ta över Northvolt Six i Quebec, Kanada.

Batterier för framtiden – även i rymden

Lyten har utvecklat en egen teknikplattform baserad på 3D-grafen och fokuserar på nästa generations litium-svavelbatterier – en teknik med potential att revolutionera batteribranschen. Förutom försäljning till drönar- och försvarsindustrin förbereder Lyten även en batterilansering på den internationella rymdstationen ISS senare i år.

En svensk medgrundare, Lars Herlitz

Även om Lyten är amerikanskt så finns det en svensk medgrundare, Lars Herlitz.

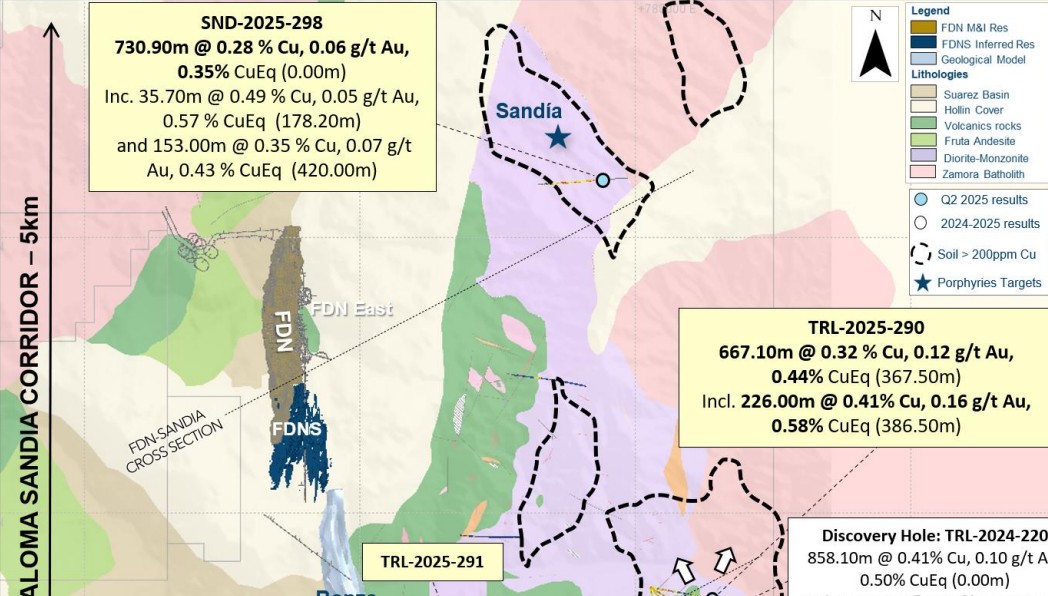

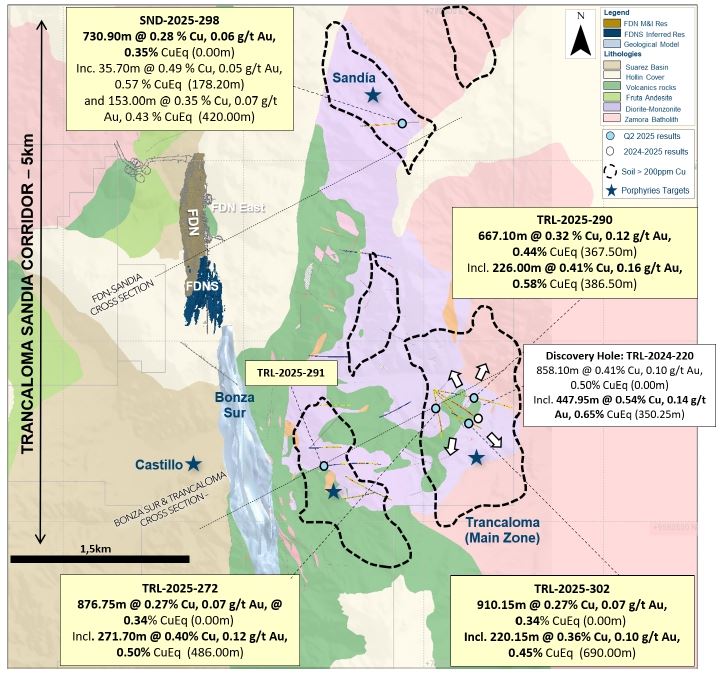

Gruvbolaget Lundin Gold har presenterat starka resultat från sin pågående prospektering vid Fruta del Norte-gruvan i Ecuador. Bolaget meddelar att man har utökat mineraliseringen vid Trancaloma samt upptäckt ett nytt koppar-guld-porfyrsystem vid Sandia, endast fyra kilometer norr om Trancaloma.

Enligt vd Ron Hochstein visar resultaten på den stora, ännu outnyttjade potentialen i området. ”Vi har nu bekräftat att mineraliseringen vid Trancaloma är kontinuerlig och sträcker sig både på djupet och i sidled. Samtidigt har vi upptäckt ett helt nytt system vid Sandia, vilket stärker bilden av en lovande porfyrkorridor direkt intill vår befintliga verksamhet,” säger han.

Bland höjdpunkterna från borrprogrammet märks ett borrhål vid Trancaloma som visade 667 meter med en koppar-ekvivalent (CuEq) på 0,44 %, inklusive 226 meter med 0,58 % CuEq. Vid Sandia påträffades 730 meter med 0,35 % CuEq från markytan, vilket bekräftar förekomsten av ett andra porfyrsystem.

Utforskningsprogrammet för 2025 är det största hittills inom området kring Fruta del Norte, med över 48 000 meter borrning genomförd hittills. Fokus ligger på att identifiera nya fyndigheter i närheten av den befintliga gruvan.

Guld stiger till över 3500 USD på osäkerhet i världen

Lyten, tillverkare av litium-svavelbatterier, tar över Northvolts tillgångar i Sverige och Tyskland

Lundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

Alkane Resources och Mandalay Resources har gått samman, aktör inom guld och antimon

Breaking some eggs in US shale

USA inför 93,5 % tull på kinesisk grafit

Fusionsföretag visar hur guld kan produceras av kvicksilver i stor skala – alkemidrömmen ska bli verklighet

Westinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

Ryska militären har skjutit ihjäl minst 11 guldletare vid sin gruva i Centralafrikanska republiken

Eurobattery Minerals förvärvar majoritet i spansk volframgruva

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUSA inför 93,5 % tull på kinesisk grafit

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFusionsföretag visar hur guld kan produceras av kvicksilver i stor skala – alkemidrömmen ska bli verklighet

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanWestinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanRyska militären har skjutit ihjäl minst 11 guldletare vid sin gruva i Centralafrikanska republiken

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanEurobattery Minerals förvärvar majoritet i spansk volframgruva

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanKopparpriset i fritt fall i USA efter att tullregler presenterats

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanLundin Gold rapporterar enastående borrresultat vid Fruta del Norte

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKina skärper kontrollen av sällsynta jordartsmetaller, vill stoppa olaglig export