Analys

SHB Råvarubrevet 1 februari 2013

Råvaror Allmänt

Råvaror Allmänt

Risk On för råvaror

Årets starka inledning för aktiemarknader har nu börjat smitta av sig på råvaror. Under veckan har råvaror äntligen fått sitt genombrott och de konjunkturhandlade råvarorna basmetaller och olja klättrat så gott som varje dag. USA:s BNP för Q4 kom in svagare än väntat under onsdagen och fick guld att hoppa upp i tron att det förlänger penningpolitiska stimulanser i USA. Annars har guld fallit i takt med att investerare viktar om från defensiva positioner som guld till mer offensiva, konjunkturberoende positioner. Denna trend tror vi fortsätter och vi sänker därför Ädelmetaller till negativ och växlar upp Energi från neutral till positiv.

Under veckan fick vi också mer vatten på vår kvarn för fortsatt penningpolitisk stimulans i USA, den enskilt viktigaste faktorn för att hålla det positiva sentimentet uppe i världsekonomin just nu. Chefen för amerikanska centralbanken, Fed Ben Bernanke, signalerade att Fed inte är nära att minska stödköpen som sker för att stimulera ekonomin och minska arbetslösheten.

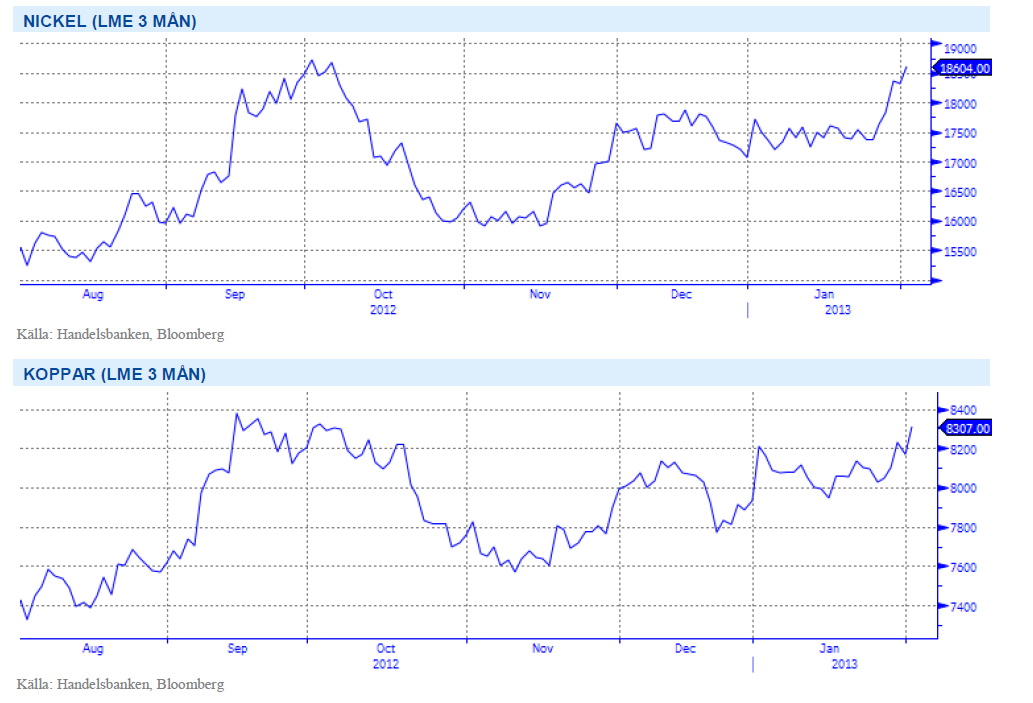

Basmetallerna

Ökad riskaptit gynnar basmetallerna

Basmetallerna lägger en vecka bakom sig med stigande priser, med uppgångar på 2-3 procent. Den metall som sticker ut är nickel som stigit med 6,6 % under veckan, den största ökningen på en vecka sedan november. På året har metallen stigit med hela 8,5 % och det främst ekonomisk data från Kina och USA som driver på uppgången.

Senaste veckan har koppar nått 3-månaders högsta som en följd av nyheter på snabbare ekonomisk tillväxt och vinsthemtagningar för kinesiska industribolag. Jobbsiffror som inte mötte förväntningar höll dock tillbaka uppgången något under fredagen. Kinas återhämtning från konjunkturnedgången går långsamt med säkert. De viktigaste indikatorerna pekar uppåt och BNP för Q4 såg för första gången på 10 kvartal bra ut. Den råvarusektor som är mest beroende av kinas återhämtning är basmetaller och till dessa är vi fortsatt positiva.

Den globala tillväxten har fått ny kraft och gynnar konjunkturkänsliga råvaror som basmetaller. Vi tror på: BASMET H

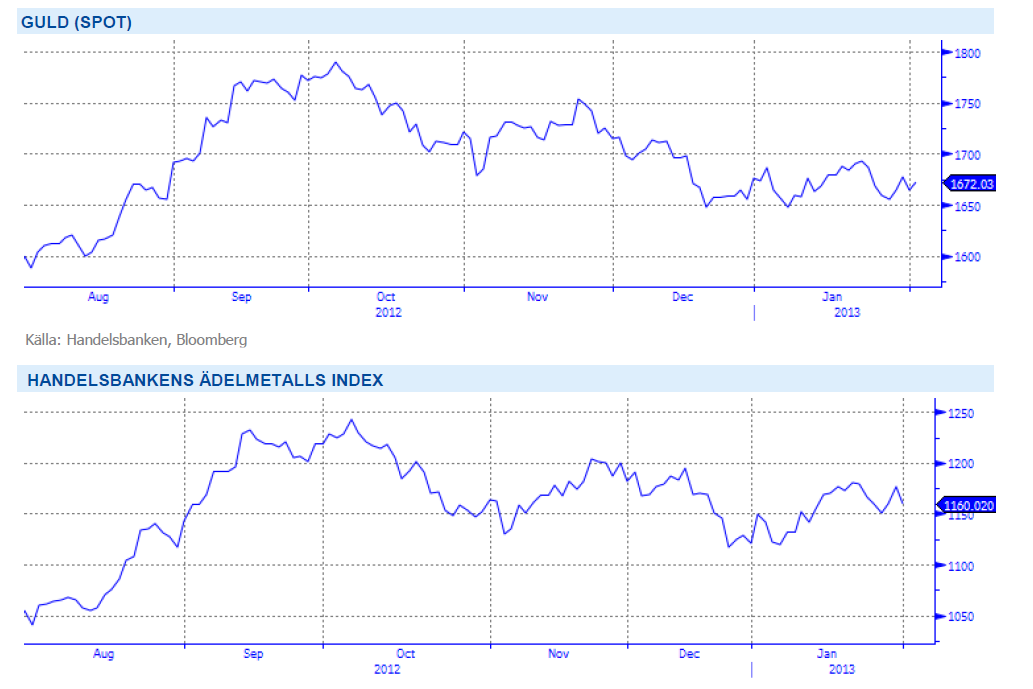

Ädelmetaller

Vi byter fot på guldet!

Efter att ha haft en positiv syn på ädelmetaller ända sedan Fed-chefens tal i Jackson Hole i slutet av augusti börjar vi nu bli betydligt mer tveksamma. Efter Jackson Hole har guldet som högst handlat drygt 8 procent upp, men har sedan toppen i början av oktober glidit lugnt men säkert nedåt. Under 2013 har guldet handlat mellan 1650 och 1700 dollar per uns, vilket är exakt samma nivåer som rådde i augusti.

Vår positiva syn sedan dess har byggt på två hörnstenar, nämligen den extrema stimulans som centralbanker världen över ägnar sig åt, och de stigande inflationsförväntningar som kommer med detta. Årets starka inledning på världens aktiemarknader, och de positiva konjunktursignaler vi fått, och det något minskade fokus som rått på euro-krisen gör att vi tror att det positiva risksentimentet fortsätter. Potentiellt stigande räntenivåer, fortsatt riskaptit kombinerat med utebliven prisuppgång på guldet får oss att tro att nästa stora rörelse kommer att vara nedåt.

Som alltid är timing på sådant här väldigt svårt, men en budgetuppgörelse i USA under februari tror vi kan vara en trigger för en större rörelse på nedsidan. Guldet befinner sig fortfarande på väldigt höga nivåer i ett historiskt perspektiv, varför vi känner oss bekväma att skifta vy 180 grader i detta läge.

Med fortsatt positivt risksentiment och potentiellt stigande räntenivåer ser vi nästa stora rörelse kommer att vara nedåt. Vi tror på GULD S H

Energi

Ökad riskaptit gynnar även oljan

Brent-oljan har handlats i en uppåtgående trend i över 2 veckor och handlas nu över 117-nivån, en nivå vi inte sett sedan mitten av april. Torsdagens löfte från amerikanska centralbanken att fortsätta sina obligationsköp samt positiv makrodata från euroområdet ger ökad riskaptit vilket gynnar oljan. Oljemarknaden stabiliseras av att Saudi nu sänker produktionen för att stabilisera priset. Den säsongsmässigt starka delen av året ligger också framför oss när det gäller oljekonsumtion. Utsläppsrätterna avslutar veckan i princip oförändrad efter kraftig uppgång under fredagen. Det var efter Angela Merkels uttalande att hon stödjer backloadingplanen (en plan för att minska överskott av rätter, ca 30 % till 2015) som priset snabbt steg 30 % och därmed raderade veckans tidigare nedgång.

Som vi tidigare skrivit är det svårt att se hur EU Kommissionen skall agera kring tilldelning och balans för att undvika att förtroendet för marknaden urholkas helt för all framtid. Vidare det mer grundläggande problemet kring svårigheten att få till ett globalt direktiv där man involverar USA och tillväxtmarknaderna vilket är det enda som ger stöd och mening åt den europeiska marknaden. Elmarknaden handlas i stort sett oförändrat över veckan. Då kontinentala elpriser och det tyska i synnerhet är lågt bör det finnas utrymme för nordisk att falla något till från dagens nivå om 35 euro. Vi förväntar oss dock inga större rörelser utan att det mesta diskonterats för varför vi ändrat vår syn från kort till neutral. Inte omöjligt att vi kanske t.o.m får se en liten tillfällig uppgång om det kalla och torra vädret som givit stöd denna vecka består vilket påverkar en redan försvagad energibalans. Prognoserna visar idag att vi får en normal utveckling på slutet av tio dagars perioden.

Den råvarugrupp som är mest beroende av den globala konjunkturen är Energi och med en starkare konjunktur ser vi positivt på utvecklingen för denna sektor. Vi tror på: ENERGI H

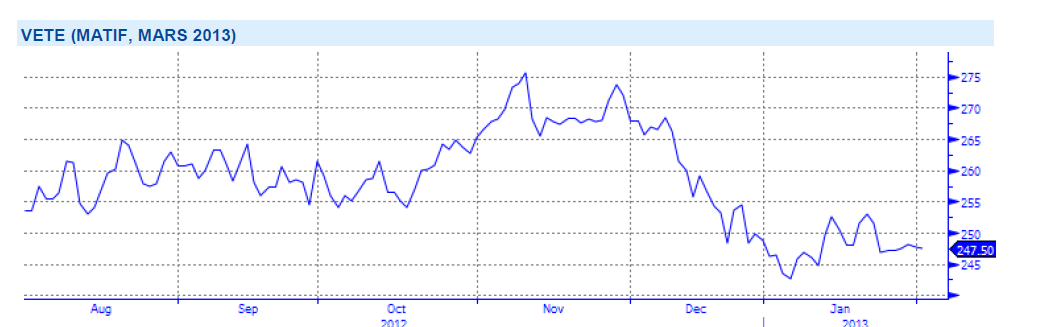

Livsmedel

Försämrat skick på det amerikanska vetet

Priset på vete är svagt upp denna vecka. Än är det torrt och varmt för det amerikanska höstvetet, vilket gör att skicket på grödan fortsätter att försämras. I december månad var låga 25 procent av höstvetet i delstaten Kansas i skicket good/excellent, idag uppskattas samma siffra till rekordlåga 20 procent – vid samma tid förra året var motsvarande siffra mer normala 45 procent. Torrt väder väntas även nästa vecka och det kommer verkligen behövas en gynnsam vår för att grödorna ska återhämta sig någorlunda.

I EU bedöms allt fortfarande vara helt ok, generellt sett bra med snö och varmare temperaturer. I en del områden har snön regnat bort men temperaturen är relativt hög och ser ut att förbli så framöver. I Ukraina steg temperaturen något i slutet av veckan men än finns det generellt sett gott om skyddande snö kvar om kylan återvänder. I Ryssland uppges allt vara ok, beräknad utvintring ligger omkring 10 procent vilket är ganska normalt. Kanadas totala veteareal väntas nå 25,3 miljoner acres, upp från förra årets 23,8 miljoner acres. Höstvetet i USA är alltså i riktigt dåligt skick och någon klar förbättring är inte i sikte. I andra veteregioner i världen råder dock inga större problem vilket håller tillbaka en prisuppgång. Än finns det dessutom tid för regn att falla inför sådd av majs i USA – vilket spannmålsmarknaden kommer lägga stort fokus på under kommande veckor. Givet inga större väderproblem bör vi dock vänta oss fallande priser lite längre fram på året.

Vi ser fortfarande framför oss fallande priser på livsmedelsektor på lite längre sikt. Vi tror på: LIVSMEDEL S H

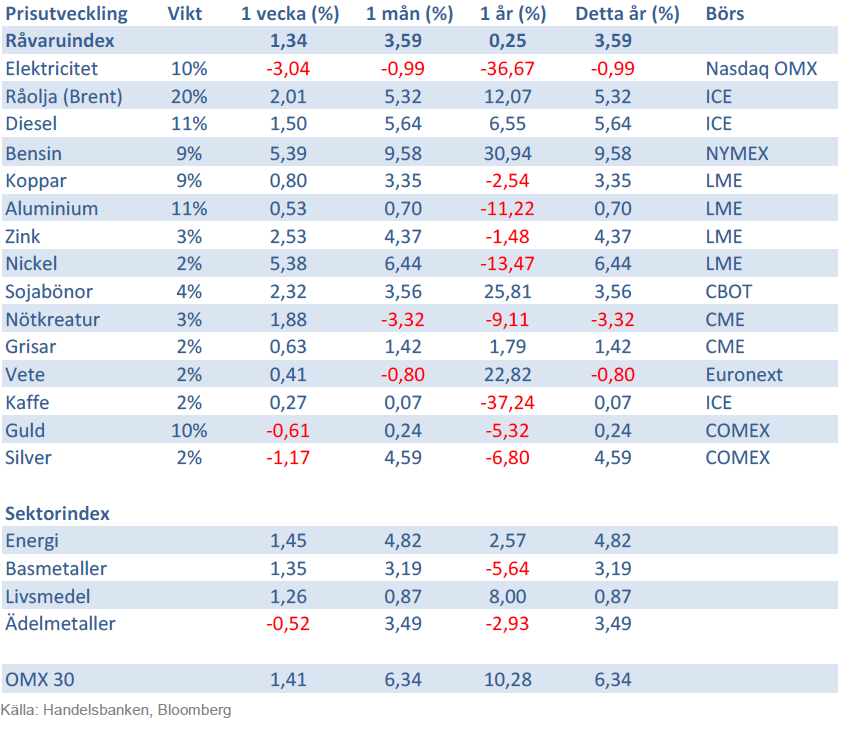

Handelsbankens Råvaruindex

Handelsbankens råvaruindex består av de underliggande indexen för respektive råvara. Vikterna är bestämda till hälften från värdet av global produktion och till hälften från likviditeten i terminskontrakten.

[box]SHB Råvarubrevet är producerat av Handelsbanken och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta material är producerat av Svenska Handelsbanken AB (publ) i fortsättningen kallad Handelsbanken. De som arbetar med innehållet är inte analytiker och materialet är inte oberoende investeringsanalys. Innehållet är uteslutande avsett för kunder i Sverige. Syftet är att ge en allmän information till Handelsbankens kunder och utgör inte ett personligt investeringsråd eller en personlig rekommendation. Informationen ska inte ensamt utgöra underlag för investeringsbeslut. Kunder bör inhämta råd från sina rådgivare och basera sina investeringsbeslut utifrån egen erfarenhet.

Informationen i materialet kan ändras och också avvika från de åsikter som uttrycks i oberoende investeringsanalyser från Handelsbanken. Informationen grundar sig på allmänt tillgänglig information och är hämtad från källor som bedöms som tillförlitliga, men riktigheten kan inte garanteras och informationen kan vara ofullständig eller nedkortad. Ingen del av förslaget får reproduceras eller distribueras till någon annan person utan att Handelsbanken dessförinnan lämnat sitt skriftliga medgivande. Handelsbanken ansvarar inte för att materialet används på ett sätt som strider mot förbudet mot vidarebefordran eller offentliggörs i strid med bankens regler.

Brent crude is essentially flat on the week, but after a volatile ride. Prices started Monday near USD 65.5/bl, climbed steadily to a mid-week high of USD 67.8/bl on Wednesday evening, before falling sharply – losing about USD 2/bl during Thursday’s session.

Brent is currently trading around USD 65.8/bl, right back where it began. The volatility reflects the market’s ongoing struggle to balance growing surplus risks against persistent geopolitical uncertainty and resilient refined product margins. Thursday’s slide snapped a three-day rally and came largely in response to a string of bearish signals, most notably from the IEA’s updated short-term outlook.

The IEA now projects record global oversupply in 2026, reinforcing concerns flagged earlier by the U.S. EIA, which already sees inventories building this quarter. The forecast comes just days after OPEC+ confirmed it will continue returning idle barrels to the market in October – albeit at a slower pace of +137,000 bl/d. While modest, the move underscores a steady push to reclaim market share and adds to supply-side pressure into year-end.

Thursday’s price drop also followed geopolitical incidences: Israeli airstrikes reportedly targeted Hamas leadership in Doha, while Russian drones crossed into Polish airspace – events that initially sent crude higher as traders covered short positions.

Yet, sentiment remains broadly cautious. Strong refining margins and low inventories at key pricing hubs like Europe continue to support the downside. Chinese stockpiling of discounted Russian barrels and tightness in refined product markets – especially diesel – are also lending support.

On the demand side, the IEA revised up its 2025 global demand growth forecast by 60,000 bl/d to 740,000 bl/d YoY, while leaving 2026 unchanged at 698,000 bl/d. Interestingly, the agency also signaled that its next long-term report could show global oil demand rising through 2050.

Meanwhile, OPEC offered a contrasting view in its latest Monthly Oil Market Report, maintaining expectations for a supply deficit both this year and next, even as its members raise output. The group kept its demand growth estimates for 2025 and 2026 unchanged at 1.29 million bl/d and 1.38 million bl/d, respectively.

We continue to watch whether the bearish supply outlook will outweigh geopolitical risk, and if Brent can continue to find support above USD 65/bl – a level increasingly seen as a soft floor for OPEC+ policy.

Brent crude makes some gains as Israel’s attack on Hamas in Qatar rattles markets. Brent crude spiked to a high of USD 67.38/b yesterday as Israel made a strike on Hamas in Qatar. But it wasn’t able to hold on to that level and only closed up 0.6% in the end at USD 66.39/b. This morning it is starting on the up with a gain of 0.9% at USD 67/b. Still rattled by Israel’s attack on Hamas in Qatar yesterday. Brent is getting some help on the margin this morning with Asian equities higher and copper gaining half a percent. But the dark cloud of surplus ahead is nonetheless hanging over the market with Brent trading two dollar lower than last Tuesday.

Geopolitical risk premiums in oil rarely lasts long unless actual supply disruption kicks in. While Israel’s attack on Hamas in Qatar is shocking, the geopolitical risk lifting crude oil yesterday and this morning is unlikely to last very long as such geopolitical risk premiums usually do not last long unless real disruption kicks in.

US API data yesterday indicated a US crude and product stock build last week of 3.1 mb. The US API last evening released partial US oil inventory data indicating that US crude stocks rose 1.3 mb and middle distillates rose 1.5 mb while gasoline rose 0.3 mb. In total a bit more than 3 mb increase. US crude and product stocks usually rise around 1 mb per week this time of year. So US commercial crude and product stock rose 2 mb over the past week adjusted for the seasonal norm. Official and complete data are due today at 16:30.

A 2 mb/week seasonally adj. US stock build implies a 1 – 1.4 mb/d global surplus if it is persistent. Assume that if the global oil market is running a surplus then some 20% to 30% of that surplus ends up in US commercial inventories. A 2 mb seasonally adjusted inventory build equals 286 kb/d. Divide by 0.2 to 0.3 and we get an implied global surplus of 950 kb/d to 1430 kb/d. A 2 mb/week seasonally adjusted build in US oil inventories is close to noise unless it is a persistent pattern every week.

US IEA STEO oil report: Robust surplus ahead and Brent averaging USD 51/b in 2026. The US EIA yesterday released its monthly STEO oil report. It projected a large and persistent surplus ahead. It estimates a global surplus of 2.2 m/d from September to December this year. A 2.4 mb/d surplus in Q1-26 and an average surplus for 2026 of 1.6 mb/d resulting in an average Brent crude oil price of USD 51/b next year. And that includes an assumption where OPEC crude oil production only averages 27.8 mb/d in 2026 versus 27.0 mb/d in 2024 and 28.6 mb/d in August.

Brent will feel the bear-pressure once US/OECD stocks starts visible build. In the meanwhile the oil market sits waiting for this projected surplus to materialize in US and OECD inventories. Once they visibly starts to build on a consistent basis, then Brent crude will likely quickly lose altitude. And unless some unforeseen supply disruption kicks in, it is bound to happen.

US IEA STEO September report. In total not much different than it was in January

US IEA STEO September report. US crude oil production contracting in 2026, but NGLs still growing. Close to zero net liquids growth in total.

Brent crude touched a low of USD 65.07 per barrel on Friday evening before rebounding sharply by USD 2 to USD 67.04 by mid-day Monday. The rally came despite confirmation from OPEC+ of a measured production increase starting next month. Prices have since eased slightly, down USD 0.6 to around USD 66.50 this morning, as the market evaluates the group’s policy, evolving demand signals, and rising geopolitical tension.

On Sunday, OPEC+ approved a 137,000 barrels-per-day increase in collective output beginning in October – a cautious first step in unwinding the final tranche of 1.66 million barrels per day in voluntary cuts, originally set to remain off the market through end-2026. Further adjustments will depend on ”evolving market conditions.” While the pace is modest – especially relative to prior monthly hikes – the signal is clear: OPEC+ is methodically re-entering the market with a strategic intent to reclaim lost market share, rather than defend high prices.

This shift in tone comes as Saudi Aramco also trimmed its official selling prices for Asian buyers, further reinforcing the group’s tilt toward a volume-over-price strategy. We see this as a clear message: OPEC+ intends to expand market share through steady production increases, and a lower price point – potentially below USD 65/b – may be necessary to stimulate demand and crowd out higher-cost competitors, particularly U.S. shale, where average break-evens remain around WTI USD 50/b.

Despite the policy shift, oil prices have held firm. Brent is still hovering near USD 66.50/b, supported by low U.S. and OECD inventories, where crude and product stocks remain well below seasonal norms, keeping front-month backwardation intact. Also, the low inventory levels at key pricing hubs in Europe and continued stockpiling by Chinese refiners are also lending resilience to prices. Tightness in refined product markets, especially diesel, has further underpinned this.

Geopolitical developments are also injecting a slight risk premium. Over the weekend, Russia launched its most intense air assault on Kyiv since the war began, damaging central government infrastructure. This escalation comes as the EU weighs fresh sanctions on Russian oil trade and financial institutions. Several European leaders are expected in Washington this week to coordinate on Ukraine strategy – and the prospect of tighter restrictions on Russian crude could re-emerge as a price stabilizer.

In Asia, China’s crude oil imports rose to 49.5 million tons in August, up 0.8% YoY. The rise coincides with increased Chinese interest in Russian Urals, offered at a discount during falling Indian demand. Chinese refiners appear to be capitalizing on this arbitrage while avoiding direct exposure to U.S. trade penalties.

Going forward, our attention turns to the data calendar. The EIA’s STEO is due today (Tuesday), followed by the IEA and OPEC monthly oil market reports on Thursday. With a pending supply surplus projected during the fourth quarter and into 2026, markets will dissect these updates for any changes in demand assumptions and non-OPEC supply growth. Stay tuned!

Kinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde

Det stigande guldpriset en utmaning för smyckesköpare

Aktier i guldbolag laggar priset på guld

Volatile but going nowhere. Brent crude circles USD 66 as market weighs surplus vs risk

Guld når sin högsta nivå någonsin, nu även justerat för inflation

Meta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

Aker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

Brent sideways on sanctions and peace talks

Ett samtal om koppar, kaffe och spannmål

Sommarens torka kan ge högre elpriser i höst

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMeta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

-

Analys4 veckor sedan

Brent sideways on sanctions and peace talks

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanEtt samtal om koppar, kaffe och spannmål

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSommarens torka kan ge högre elpriser i höst

-

Analys4 veckor sedan

Brent edges higher as India–Russia oil trade draws U.S. ire and Powell takes the stage at Jackson Hole

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMahvie Minerals är verksamt i guldrikt område i Finland

-

Analys3 veckor sedan

Increasing risk that OPEC+ will unwind the last 1.65 mb/d of cuts when they meet on 7 September