Nyheter

Much ado about nothing

![]() William Shakespeare titled his play this way to emphasize that it was a fluffy enjoyable romantic comedy: No King Lear. What we these days call a summer date flick. This piece deals with a tempest in a teapot. Unfortunately, it is not a funny comedy. Investors falling prey to predatory marketing hype may experience a tradegy of losing money on bad investments.

William Shakespeare titled his play this way to emphasize that it was a fluffy enjoyable romantic comedy: No King Lear. What we these days call a summer date flick. This piece deals with a tempest in a teapot. Unfortunately, it is not a funny comedy. Investors falling prey to predatory marketing hype may experience a tradegy of losing money on bad investments.

Gold marketeers are bending over backward to find ways to try to scare investors into buying gold, into continuing to believe the dream based on an economic nightmare scenario that gold will rise and rise forever to unfathomable heights. The scare tactics used to center on an imminent collapse of the global financial system, or your local bank, failed, despite the best efforts of governments in the United States and Europe to help promote the idea of gold as a safe haven and portfolio diversifier.

Trying to scare people into buying gold based on the threat of hyperinflation also has failed, for the most part. There are still some believers in the inflation thesis out there, but most people have realized that when a significant part of the population does not have jobs that pay them enough to buy things, inflationary pressures tend to remain bottled up.

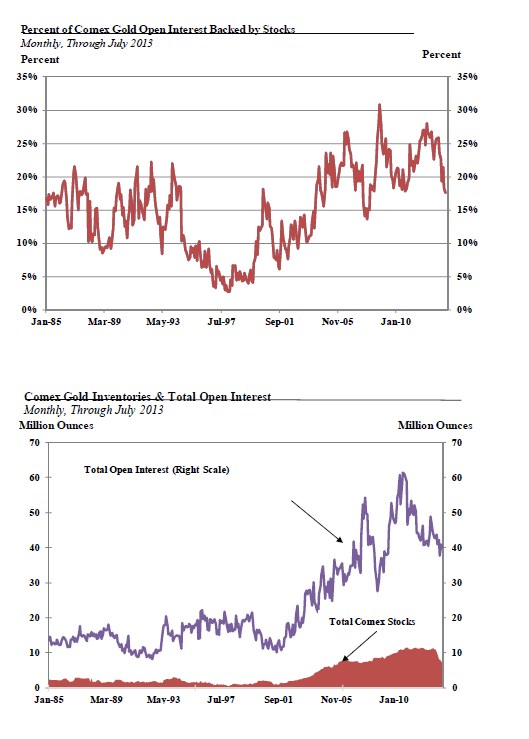

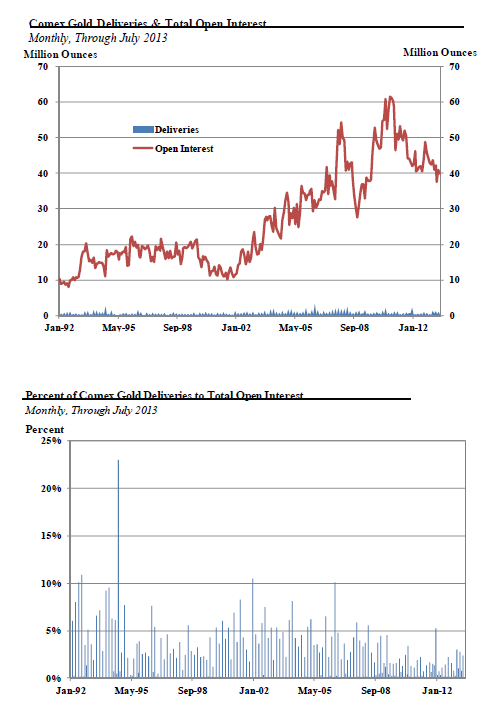

So the marketeers keep trying. Their current spiel focuses on a non-existent threat of insufficient gold in Comex registered and eligible inventories to meet demand, and, related to that, fears of a recently emergence but not really significant backwardation in gold prices. The first part says the more than 60% plunge in registered gold inventories, from 2,147,399 ounces at the end of April to roughly 785,118 ounces on 15 August means that there is not enough gold in the Comex warehouses for market participants to take deliveries. Secondly, the recent $0.10 to $0.20 price backwardation from 6 August through middle of August between thinly traded front months was cited as evidence of strong physical demand, to support the claims that there will be an imminent “default” of Comex paper gold. (The definition the marketeers use of a Comex default is neither legally nor market-wise accurate, but when you are making stuff up, facts like that do not seem to matter.)

These claims cannot be further from the truth. First, registered stocks account for less than a third of total Comex reported gold stocks. While registered stocks have fallen sharply, combined registered and eligible stocks declined at a far less dramatic pace of 14.3% from end of April to 6,967,251 ounces as of 15 August. More importantly, monthly data from the Comex shows that there is a greater ‘cover’ of inventories as a percentage of open interest than there was historically. In July the percentage of open interest backed by total Comex gold inventories stood at 17.5%. While this percentage has been declining since reaching 28.0% in March 2012, stocks are equivalent to a vastly higher percentage of open interest than the period from January 1985 to April 2004, during which time the average was 12.0%. In fact, for much of the past decade the percentage of open interest covered by total stocks was much lower. It moved in a range of 6.1% – 16.8% between August 2000 and April 2004, and dipped to as low as 13.6% as recently as December 2007.

The same is true of deliveries relative to stocks, and deliveries relative to open interest. In both cases, the ratios show that there have been lower rates of deliveries in recent years compared to stocks and open interest than there was prior to 2005. The monthly ratio of deliveries relative to stocks averaged 7.1% from January to July, compared to 25.2% from January 1992 to December 2004. During the same period this year the monthly average ratio of deliveries to open interest was 1.47%, compared to 2.39% from January 1992 to December 2004.

Any talk of delivery problems, shortages, and defaults is totally unfounded based on these historical ratios.

Futures contracts are financial instruments designed to allow commercial entities to hedge the price risks inherent in their businesses, by attracting investors and speculators who are willing to take on that price risk with the hope of making a profit by taking on this risk. Futures contracts are not designed for physical delivery, and they largely are not used in that fashion. This is true across all commodities, and not just gold and silver. In almost all commodities the delivery rates are very low, usually a tiny fraction of the total open interest. The concerns of an imminent shortage of deliverable stocks are uncalled for.

[box]Denna analys är producerad av CPM Group och publiceras med tillstånd på Råvarumarknaden.se.[/box]

Disclaimer

Copyright CPM Group 2012. Not for reproduction or retransmission without written consent of CPM Group. Market Commentary is published by CPM Group and is distributed via e-mail. The views expressed within are solely those of CPM Group. Such information has not been verified, nor does CPM make any representation as to its accuracy or completeness.

Any statements non-factual in nature constitute only current opinions, which are subject to change. While every effort has been made to ensure that the accuracy of the material contained in the reports is correct, CPM Group cannot be held liable for errors or omissions. CPM Group is not soliciting any action based on it. Visit www.cpmgroup.com for more information.

Jeffrey Christian på CPM Group gästar Monex för att prata guld och silver. Det framhålls att vi befinner oss i en tid av extrem osäkerhet, präglad av politiska, ekonomiska och sociala spänningar som bedöms vara mer oroande än under kriserna i slutet av 1970-talet. Detta har drivit investerare mot tryggare tillgångar som guld, silver och även platina.

Priserna på ädelmetaller ligger nu på rekordnivåer, med guld nära 3 900 dollar per uns och silver omkring 48 dollar. Analytiker menar att uppgången främst beror på oro för den globala utvecklingen snarare än tekniska prisnivåer. De bedömer att priserna kommer fortsätta stiga tills det sker en tydlig förbättring i det politiska och ekonomiska klimatet, något som inte förväntas inom den närmaste framtiden.

Samtidigt påpekas att guld och dollarn ibland kan stiga parallellt, vilket tidigare skett under perioder av stor osäkerhet. Den kommande osäkerheten kring ett möjligt amerikanskt regeringsstopp kan enligt bedömare förstärka trenden mot fortsatt stark efterfrågan på ädelmetaller.

Kärnkraftsföretagen Oklo från USA och svenska Blykalla har ingått ett strategiskt partnerskap för att främja tekniksamarbete, samordna leverantörskedjor och dela regulatorisk kunskap mellan länderna. Samarbetet inkluderar att Oklo går in som en av de större investerarna i Blykallas kommande investeringsrunda med ett åtagande på cirka 5 miljoner dollar.

Genom ett gemensamt teknikutvecklingsavtal ska bolagen utbyta insikter om material, komponenter och licensieringspraxis i både USA och Sverige. Målet är att minska kostnader och tidsrisker i utvecklingen av små modulära reaktorer (SMR).

Blykalla utvecklar SEALER, en blykyld snabbreaktor på 55 MWe, medan Oklo fokuserar på natriumkylda reaktorer upp till 75 MWe för industriella och militära tillämpningar i USA.

“Det här samarbetet stärker det växande ekosystemet för avancerade reaktorer i en tid av globalt ökande energibehov,” säger Oklo-grundaren Jacob DeWitte. Blykallas vd Jacob Stedman tillägger: “Vår gemensamma industriella strategi kan hjälpa leverantörer att planera för uppskalning, oavsett vilken sida av Atlanten de befinner sig på.”

Intervju på Bloomberg om samarbetet

Snittpriset på el för höstmånaderna september till november väntas landa på strax under 50 öre per kilowattimme. Det är nästan en fördubbling jämfört med hösten 2024, då snittet låg på drygt 30 öre. Men nivåerna är fortfarande betydligt lägre än under elpriskrisen 2022. Det visar elbolaget Bixias höstprognos.

Att elpriserna är högre än i fjol beror främst på lägre tillgänglighet i kärnkraften och en svagare hydrologisk balans efter en torr sommar. Även om hösten har börjat blött och september ser ut att bli den nederbördsrikaste månaden sedan 2018, räcker det inte till för att vända vattenbalansen.

– Höstens elpriser är stabila, men klart högre än i fjol. Det är framför allt osäkerheten kring kärnkraften som påverkar där Oskarshamn 3 har varit ur drift längre än planerat. Samtidigt har den hydrologiska balansen inte återhämtat sig efter sommarens underskott, trots den blöta inledningen på hösten. Men jämfört med krisåren 2021 och 2022 ligger priserna fortfarande på en låg nivå, säger Johan Sigvardsson, elprisanalytiker på Bixia.

I september bidrog bristen på kärnkraft till att elpriset nästan fördubblades jämfört med samma månad i fjol. Priset landade på cirka 40 öre per kilowattimme, att jämföra med 22 öre i september 2024. Flera reaktorer stod stilla, däribland Oskarshamn 3, Forsmark 1 samt Lovisa 1 och 2 i Finland. Trots mycket regn under månaden var vattennivåerna fortsatt låga efter den torra sommaren, medan blåsiga perioder tillfälligt pressade ner priserna.

I oktober väntas elpriset hamna runt 45 öre per kilowattimme, jämfört med 27 öre i fjol, och i november kring 60 öre, mot 43 öre förra året. Sammantaget ger det ett höstsnitt i system på knappt 50 öre, jämfört med drygt 30 öre samma period i fjol. Under krisåret 2022 låg snittet för höstmånaderna på över 1,15 kronor per kilowattimme, med perioder på upp mot 4 kronor.

Liten risk för höga höstpriser

Bixia bedömer att priserna kan komma att stiga tillfälligt om vädret blir kallare än normalt eller om kärnkraftsreaktorer får fortsatt försening i återstart. Om till exempel Oskarshamn 3, vars återstart redan skjutits på fem gånger, inte kommer igång enligt plan i mitten av oktober, finns risk att priserna ökar under andra halvan av månaden.

– Risken för pristoppar ökar ju längre in på säsongen vi kommer, eftersom förbrukningen stiger när temperaturen sjunker. Men väderprognoserna ser i nuläget gynnsamma ut, och även om det skulle bli kallare än väntat ser vi inte någon risk för extremt höga priser, säger Johan Sigvardsson.

Dyrare el i syd

Södra Sverige har betalat betydligt mer för elen än norra delarna. Priserna har legat på runt 15 öre per kWh i norr under september, medan syd haft priser på omkring 70 öre. En differentierad prisbild väntas även under resten av hösten, särskilt om kärnkraftsproduktionen i söder fortsätter att vara begränsad och det fortsätter att vara gott om vatten i norr.

A sharp weakening at the core of the oil market: The Dubai curve

Guld nära 4000 USD och silver 50 USD, därför kan de fortsätta stiga

OPEC+ will likely unwind 500 kb/d of voluntary quotas in October. But a full unwind of 1.5 mb/d in one go could be in the cards

Blykalla och amerikanska Oklo inleder ett samarbete

Fortsatt stabilt elpris – men dubbelt så dyrt som i fjol

Eurobattery Minerals satsar på kritiska metaller för Europas självförsörjning

Mahvie Minerals i en guldtrend

Guldpriset kan närma sig 5000 USD om centralbankens oberoende skadas

OPEC signalerar att de inte bryr sig om oljepriset faller kommande månader

Volatile but going nowhere. Brent crude circles USD 66 as market weighs surplus vs risk

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanEurobattery Minerals satsar på kritiska metaller för Europas självförsörjning

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMahvie Minerals i en guldtrend

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuldpriset kan närma sig 5000 USD om centralbankens oberoende skadas

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanOPEC signalerar att de inte bryr sig om oljepriset faller kommande månader

-

Analys3 veckor sedan

Analys3 veckor sedanVolatile but going nowhere. Brent crude circles USD 66 as market weighs surplus vs risk

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanAktier i guldbolag laggar priset på guld

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanTyskland har så höga elpriser att företag inte har råd att använda elektricitet