Analys

SIP Nordic – Råvaruguiden – augusti 2012

Det är inte bara vi människor som tar semester under sommaren. Råvaror har också en tendens att lugna ned sig och dessutom backa en del under sommarens sista månader.

Det är inte bara vi människor som tar semester under sommaren. Råvaror har också en tendens att lugna ned sig och dessutom backa en del under sommarens sista månader.

Sommarmånaderna, med augusti i spetsen, är historiskt sett svaga månader för råvaror. Faktum är att endast två råvaror, av de tretton som vi bevakar, historiskt har presterat bättre under augusti månad jämfört med utvecklingen under sept-dec (hösten).

Med nedtrappningen i den västerländska industrin under slutet av sommaren kommer även större lager av råvaror med sjunkande priser som följd. Till exempel har koppar under de senaste 27 åren haft stigande lager under 24 av dessa i augusti månad. Vilket också visar sig historiskt då koppar underpresterat under augusti jämfört med de fyra sista månaderna av året.

Lägg därtill den minskade aktiviteten från spekulanter vilket till viss del sänker volatiliteten under dessa månader.

De fyra sista månaderna har även historiskt sett varit positiva för de övriga råvaror vi bevakar. Hela 11 av råvarorna har sedan 1997 haft en positiv utveckling under sept-dec. Med ökad industriell aktivitet, återkomsten av spekulanter på marknaden och ett potentiellt QE3 kan vi få se detta mönster upprepa sig under 2012.

Råvaror – Energi

Brent olja

år 2010 till 2012")

- Brentoljan har under 2012 åkt berg och dalbana. För året är brent ned ca 2%.

- Brent har haft en stark period sedan mitten av juni. Brent har sedan mitten av juni stigit med 20%.

- Spekulationer om ett eventuellt QE3 eldar på utvecklingen i oljan. Om Ben Bernanke bestämmer att det krävs en kvantitativ lättnad kan oljan leta sig upp mot topparna i mars.

- Oroligheter i mellanöstern kan också driva brentoljan till högre nivåer.

Naturgas

2 år")

- Naturgas fortsätter sin klättring uppåt och befinner sig nu i en kortsiktigt positiv trend. Naturgas är för året upp drygt 1%.

- Sedan botten i mitten av april har priset på naturgas ökat med drygt 60%.

- En stor anledning till uppgången är att många spekulanter, däribland hedgefonder ligger i korta positioner. Detta kan fortsatt driva priset uppåt.

Råvaror – Metaller

Guld

- För året är guld upp ca 3%.

- Juli månad resulterade inte i några större rörelser. Guld är upp 1,4% under juli månad.

- Thomson Reuters släppte förra månaden sin rapport om ädelmetaller där analytikerna reviderade sin syn för guldpriset under 2012-2013. Analytikerna spår att guldpriset kommer att ligga på samma nivå året ut för att sedan öka något under 2013.

- Guldpriset har i år varit starkt korrelerad med hur den europeiska och amerikanska centralbanken har agerat.. Ett eventuellt QE3 kan få guldet att röra på sig ordentligt.

Silver

- Silver är för året upp knappa 1%.

- Sedan slutet av februari har silver tappat mer än 25,9 %.

- Likt guldet kommer silvers utveckling till stor del styras av huruvida den amerikanska centralbanken trycker nya pengar eller inte.

- Andelen spekulanter som tror på nedgång i silver ökar. Andelen långa kontrakt i silver är nu 2 195 ton. Den lägsta siffran sedan i slutet av 2001.

- Om QE3 blir verklighet kan många spekulanter ligga på fel sida vilket kan få silver att få samma utveckling som under april 2011.

Platina

- Platina är för året upp nästan 3 %.

- Sedan toppen i februari har dock platina tappat nästan 18 %.

- Platina fortsätter at handlas till en billigare kurs än guld.

- Likt silver ökar andelen spekulanter som tror på nedgång i platina.

- Tillgången av platina spås vara oförändrat under 2012 samtidigt som konsumtionen väntas sjunka med 0,2 %.

Koppar

- För året är kopparpriset i princip oförändrat. Upp 0,5 % sedan slutet av december 2011.

- Sommarmånaderna innebär industrisemester vilket historiskt har pressat priset på koppar under augusti månad. Återstår att se vad som händer i år.

- Det finns fortsatt en rädsla för minskad kinesisk tillväxt. Kina står för 40 % av världskonsumtionen.

Zink

- Zink är upp knappa 1,3 % för året.

- Under juli månad har zinkpriset ökat 0,5 %.

- Likt andra metaller har zinkpriset fallit kraftigt sedan månadsskiftet januari/februari.

- Tillgången på zink är stort och priset påverkas negativt av rapporter om stigande lager. Detta kan trycka ned priset ytterligare.

Nickel

- Nickel presterade sämst av alla basmetaller under 2011.

- Nickel fortsätter sin kräftgång under 2012 är för året ned nästan 13 %.

- Sedan toppen i februari har nickel tappat mer än 27 %.

- Nickelmarknaden är mättad med ökande lager.

- Många stora projekt inom nickelproduktion är redan finansierade och irreversibla vilket kommer att öka tillgången av nickel ytterligare.

Råvaror – Jordbruk

Socker

- Jordbruksråvarorna sommarutveckling fortsätter att vara stark.

- Sedan början av juni är socker upp närmare 20 %.

- För året är dock sockerpriset ned dryga 4 %.

- Många spekulanter ligger fel i sina positioner. Många hedgefonder ligger i stora korta positioner vilket pressar priset på socker uppåt.

Bomull

- Bomull är för året ned ca 24 % där merparten av nedgången kom i maj. I maj föll bomullspriset med närmare 20 %.

- Rekordexport av bomull från Indien pressar priset.

- Bomullspriset konsoliderar nu kring 71 cents. Viktig nivå hittar vi kring 66 cents.

- Trots att bomullspriset fallit kraftigt under 2012 är det fortfarande nästan dubbelt så högt som priset för några år sedan. Fallhöjden är således stor.

Majs

- Priset på majs har ökat kraftigt sedan i början av juni. +51 %.

- För året är majs upp 28 %.

- Tidigare spekulationer visade att skörden av majs i USA skulle vara mycket god. Extrem torka gör dock att kommande skörd ser ut att vara mycket dålig vilket driver priset på majs till de högsta nivåerna sedan juni 2011.

- Knappt 40 % av skörden spås vara av god kvalitet.

Vete

- Likt majs rusade vete under juni och juli månad. Upp nästan 51 % sedan mitten av juni

- För året är priset på vete upp 40 %.

- Torkan i USA gör att den kommande skörden inte blir så stor som förutspått.

- Gemensamt för både majs och vete är att de kraftiga uppgångarna skett mycket snabbt vilket har resulterat i en liten rekyl nedåt. Nu konsoliderar vete kring 900. Med viktig nivåer kring 950 och 875.

Apelsinjuice

- Efter återhämtningen under maj-juni har priset på apelsinjuice tappat under juli.

- Apelsinjuice är ned ca 10 % under juli månad vilket gör att priset på apelsinjuice nu har tappat 36 % för året.

- Priset på apelsinjuice är fortfarande 85 % högre än botten 2009. Fallhöjden är således hög.

[box]Denna uppdatering är producerat av SIP Nordic och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta produktblad utgör endast marknadsföring och har sammanställts av SIP Nordic Fondkommission AB.

Innehållet ger inte fullständig information avseende det finansiella instrumentet. Investerare uppmanas att del av prospekt och slutliga villkor, vilka finns tillgängliga på: www.rbsbank.se/markets, innan ett investeringsbeslut tas.

Förekommande exempel är simulerade och baseras på SIP Nordics egna beräkningar och antaganden, en person som använder andra data eller antaganden kan nå andra resultat. Administrativa avgifter och transaktionsavgifter påverkar den faktiska avkastningen.

U.S. commercial crude inventories posted a marginal draw last week, falling by 0.6 million barrels to 414.8 million barrels. Inventories remain 4% below the five-year seasonal average, but the draw is far smaller than last week’s massive 9.3-million-barrel decline. Higher crude imports (+803,000 bl d WoW) and steady refinery runs (93% utilization) helped keep the crude balance relatively neutral.

Yet another drawdown indicates commercial crude inventories continue to trend below the 2015–2022 seasonal norm (~440 million barrels), though at 414.8 million barrels, levels are now almost exactly in line with both the 2023 and 2024 trajectory, suggesting stable YoY conditions (see page 3 attached).

Gasoline inventories dropped by 1.1 million barrels and are now 2% below the five-year average. The decline was broad-based, with both finished gasoline and blending components falling, indicating lower output and resilient end-user demand as we enter the shoulder season post-summer (see page 6 attached).

On the diesel side, distillate inventories declined by 1.7 million barrels, snapping a two-week streak of strong builds. At 125 million barrels, diesel inventories are once again 8% below the five-year average and trending near the low end of the historical range.

In total, commercial petroleum inventories (excl. SPR) slipped by 0.5 million barrels on the week to ish 1,281.5 million barrels. While essentially flat, this ends a two-week streak of meaningful builds, reflecting a return to a slightly tighter situation.

On the demand side, the DOE’s ‘products supplied’ metric (see page 6 attached), a proxy for implied consumption, softened slightly. Total demand for crude oil over the past four weeks averaged 20.5 million barrels per day, up just 0.9% YoY.

Summing up: This week’s report shows a re-tightening in diesel supply and modest draws across the board, while demand growth is beginning to flatten. Inventories remain structurally low, but the tone is less bullish than in recent weeks.

Brent crude rose 1.6% yesterday. After trading in a range of USD 66.1 – 68.09/b it settled at USD 67.63/b. A level which we are well accustomed to see Brent crude flipping around since late August. This morning it is trading 0.5% higher at USD 68/b. The market was expecting an increase of 230 kb/d in Iraqi crude exports from Kurdistan through Turkey to the Cheyhan port but that has so far failed to materialize. This probably helped to drive Brent crude higher yesterday. Indications last evening that US crude oil inventories likely fell 3.8 mb last week (indicative numbers by API) probably also added some strength to Brent crude late in the session. The market continues to await the much heralded global surplus materializing as rising crude and product inventories in OECD countries in general and the US specifically.

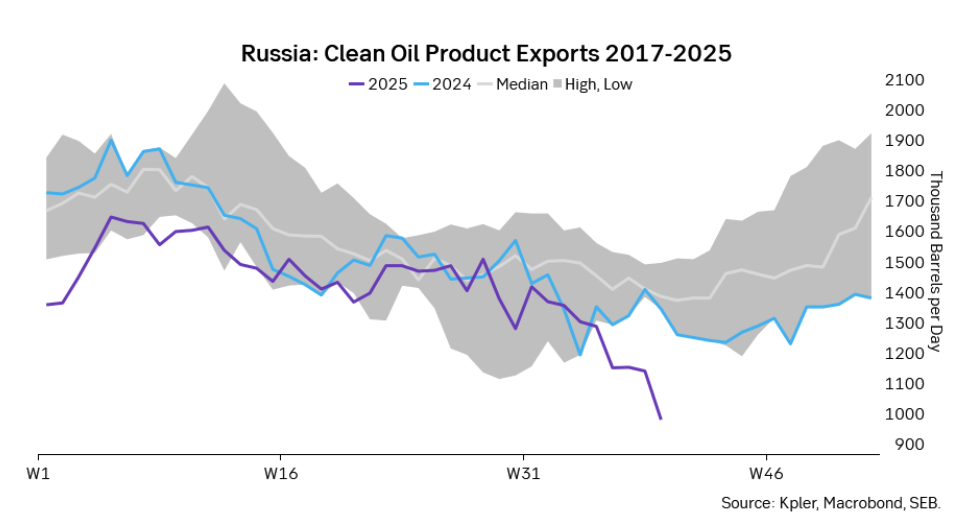

The oil market is starting to focus increasingly on the successful Ukrainian attacks on Russian oil infrastructure. Especially the attacks on Russian refineries. Refineries are highly complex and much harder to repair than simple crude oil facilities like export pipelines, ports and hubs. It can take months and months to repair complex refineries. It is thus mainly Russian oil products which will be hurt by this. First oil product exports will go down, thereafter Russia will have to ration oil product consumption domestically. Russian crude exports may not be hurt as much. Its crude exports could actually go up as its capacity to process crude goes down. SEB’s Emerging Market strategist Erik Meyersson wrote about the Ukrainian campaign this morning: ”Are Ukraine’s attacks on Russian energy infrastructure working?”. Phillips P O’Brian published an interesting not on this as well yesterday: ”An Update On The Ukrainian Campaign Against Russian Refineries”. It is a pay-for article, but it is well worth reading. Amongst other things it highlights the strategic focus of Ukraine towards Russia’s energy infrastructure. A Ukrainian on the matter also put out a visual representation of the attacks on twitter. We have not verified the data representation. It needs to be interpreted with caution in terms of magnitude of impact and current outage.

Complex Russian oil refineries are sitting ducks in the new, modern long-range drone war. Ukraine is building a range of new weapons as well according to O’Brian. The problem with attacks on Russian refineries is thus on the rise. This will likely be an escalating problem for Russia. And oil products around the world may rise versus the crude oil price while the crude oil price itself may not rise all that much due to this.

Russian clean oil product exports as presented by SEB’s Erik Meyersson in his note this morning.

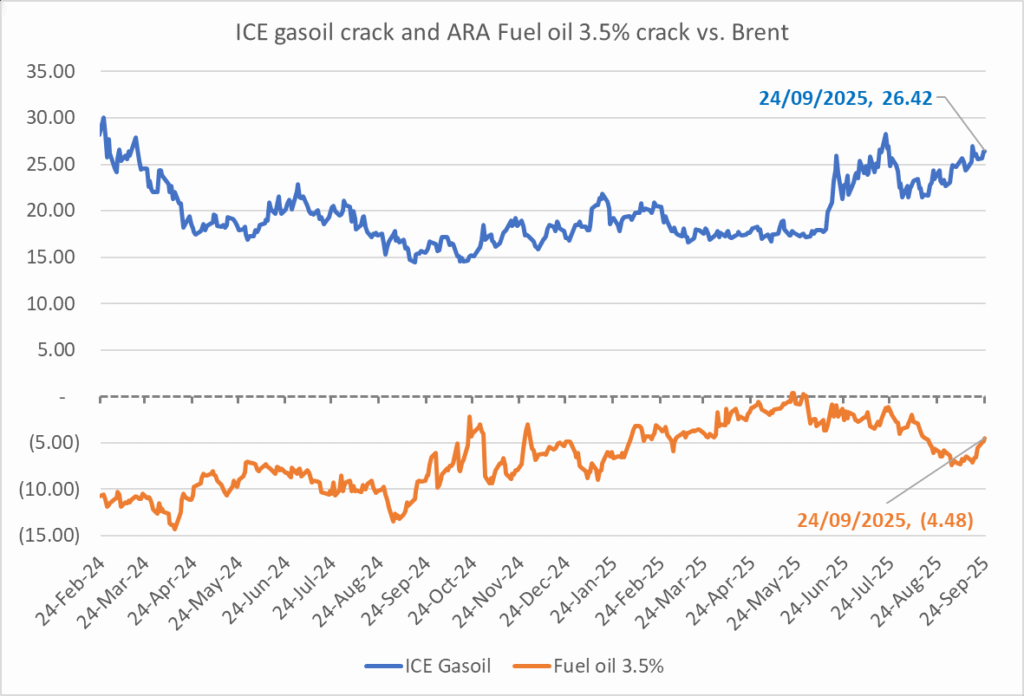

The ICE Gasoil crack and the 3.5% fuel oil crack has been strengthening. The 3.5% crack should have weakened along with rising exports of sour crude from OPEC+, but it hasn’t. Rather it has moved higher instead. The higher cracks could in part be due to the Ukrainian attacks on Russian oil refineries.

Ukrainian inhabitants graphical representation of Ukrainian attacks on Russian oil refineries on Twitter. Highlighting date of attacks, size of refineries and distance from Ukraine. We have not verified the detailed information. And you cannot derive the amount of outage as a consequence of this.

Brent down 0.5% last week with a little bounce this morning. Brent crude fell 0.5% last week to USD 66.68/b with a high of the week of USD 68/69/b set early in the week and the low of USD 66.44/b on Friday. This morning it is up 0.6% and trading at USD 67.1/b and just three dollar below the year to date average of USD 70/b.

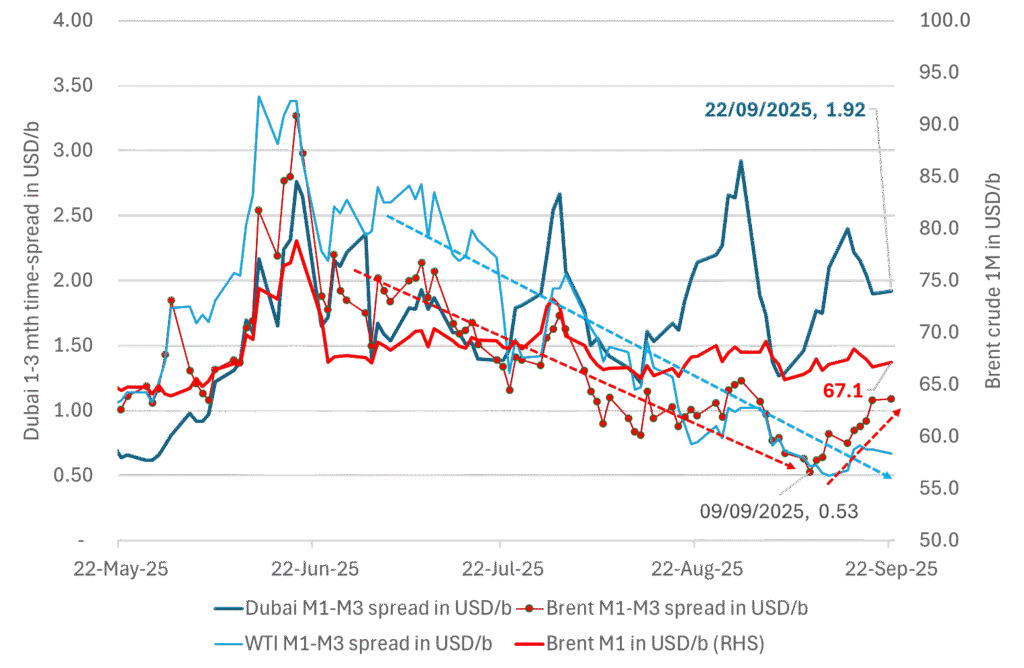

The Dubai crude curve is holding strong. Flat prices will move lower when/if that starts to weaken. The front-end of the Brent crude oil curve has been on a strengthening path since around 10 September, but the front-month contract is more or less at the same level as 10 September. But the overall direction since June has been steadily lower. The recent strengthening in the front-end of the Brent curve is thus probably temporary. The WTI curve has also strengthened a little but much less visibly. What stands out is the robustness in the front-end of the Dubai crude curve. With tapering crude burn for power in the Middle East as we move away from the summer heat together with increasing production by OPEC+, one should have expected to see a weakening in the Dubai curve. The 1 to 3mth Dubai time-spread is however holding strong at close to USD 2/b. When/if the Dubai front-end curve starts to weaken, that is probably when we’ll see flat prices start to taper off and fall lower. Asian oil demand in general and Chinese stockpiling specifically is probably what keeps the the strength in the front-end of the Dubai curve elevated. It is hard to see Brent and WTI prices move significantly lower before the Dubai curve starts to give in.

The 1mth to 3mth time spreads of Brent, WTI and Dubai in USD/b

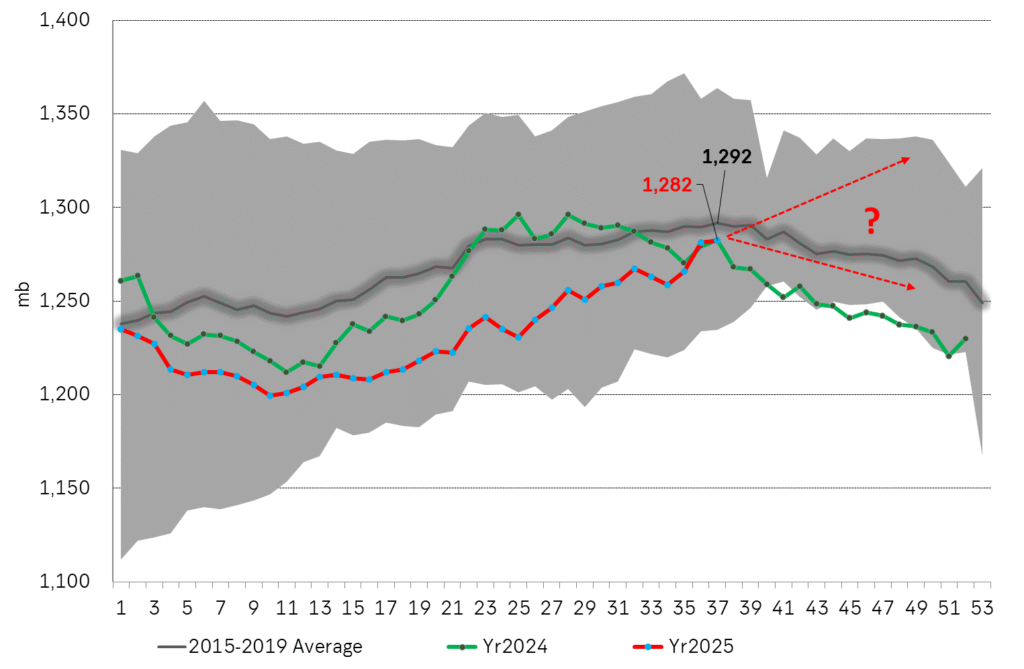

If US oil stocks continues higher in Q4 we’ll start to feel the bearish pressure more intensely. US commercial crude and product stocks have been below normal and below levels from last year as well all until now. Inventories have been rising since week 10 and steadily faster than the normal seasonal trend and today are finally on par with last year and only 10 mb below normal. From here to the end of the year is however is the interesting part as inventories normally decline from now to the end of the year. If US inventories instead continues to rise, then the divergence with normal inventories will be very explicit and help to drive the price lower. So keep a keen eye on US commercial inventories in the coming weeks for such a possible divergence.

US Commercial crude and product stocks in million barrels.

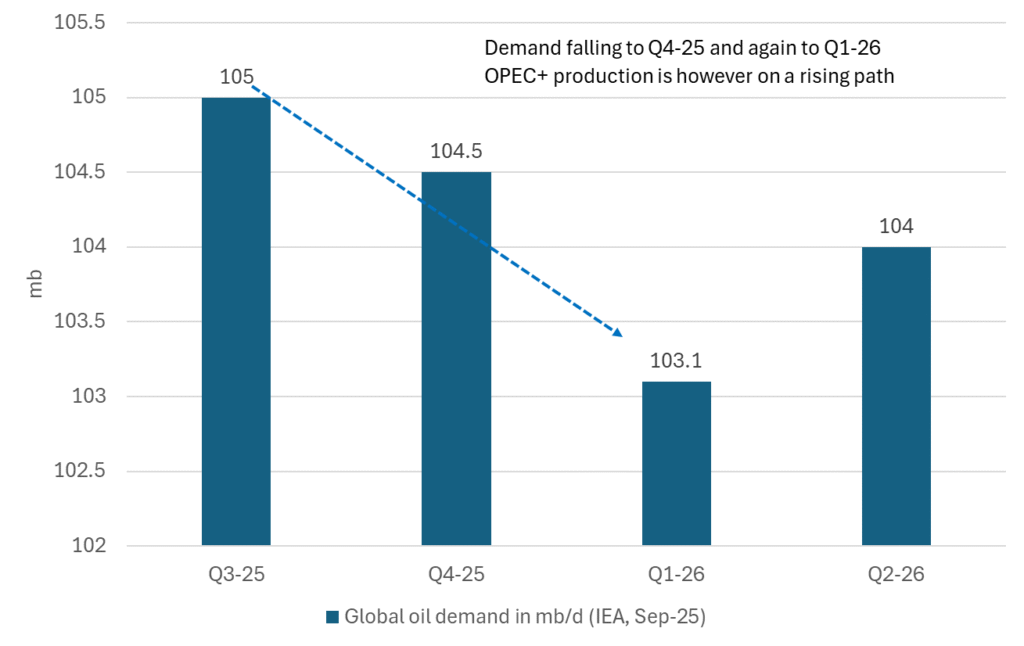

Falling seasonal demand and rising OPEC+ supply will likely drive oil lower in Q4-25. The setup for the oil market is that global oil demand is set to taper off from Q3 to Q4 and again to Q1-26. At the same time production by OPEC+ is on a rising path. The big question this is of course if China will stockpile the increasing surplus or whether the oil price will be pushed lower into the 50ies. We believe the latter.

Outlook for global oil demand by IEA in the OMR September report

OPEC+ missar produktionsmål, stöder oljepriserna

Kanadensiska naturgasproducenter stryper produktionen efter minuspriser

Modest draws, flat demand, and diesel back in focus

ShaMaran återupptar oljeexport genom Irak–Turkiet-pipelinen

Are Ukraine’s attacks on Russian energy infrastructure working?

Eurobattery Minerals satsar på kritiska metaller för Europas självförsörjning

Guldpriset kan närma sig 5000 USD om centralbankens oberoende skadas

Mahvie Minerals i en guldtrend

OPEC+ in a process of retaking market share

Aktier i guldbolag laggar priset på guld

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEurobattery Minerals satsar på kritiska metaller för Europas självförsörjning

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGuldpriset kan närma sig 5000 USD om centralbankens oberoende skadas

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMahvie Minerals i en guldtrend

-

Analys4 veckor sedan

OPEC+ in a process of retaking market share

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAktier i guldbolag laggar priset på guld

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOPEC signalerar att de inte bryr sig om oljepriset faller kommande månader

-

Analys2 veckor sedan

Volatile but going nowhere. Brent crude circles USD 66 as market weighs surplus vs risk

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanKinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde