Nyheter

Gold: how we value the precious metal

Gold is a unique asset class. Indeed, many investors even question whether it is an asset class. Is it a commodity, or a currency? What’s also interesting about gold is that even though it has been viewed as a form of investment for several millennia, there’s little consensus on how to actually value it.

In this article, we’ll look at how we value gold at WisdomTree and explain how we use historic price behaviour to generate gold price forecasts for the future.

The difficulty in valuing gold

It’s easy to understand why valuing gold is complex.

For a start, gold does not generate cash flow like other assets do, so traditional valuation techniques such as discounted cash flow (DCF) models don’t work.

Another complication lies in the fact that there have been many regime shifts in relation to the precious metal over the years. For example, between 1933 and 1974, investment in gold bullion was all-but barred in the US after President Franklin D. Roosevelt signed Executive Order 61021. Similarly, in China, gold bullion investment was effectively prohibited between 1950 and 20042. Today, these two countries are among the largest bullion investing nations in the world. So, clearly, using extremely long timeseries of data to calibrate a gold valuation model is not appropriate.

With little consensus on valuation methods, financial commentators are often quite emotive in their projections for the metal. There are the ‘gold bugs,’ who tend to be perma-bulls, while there are also gold bears who believe that the metal has little value.

The WisdomTree gold model

At WisdomTree, our goal has been to develop a robust, impartial gold model.

We recognise that many factors affect the price of gold, so we have modelled the precious metal in a multivariate fashion. We have been able to build a basic model with four key explanatory variables and our gold price forecasts can be positive, negative, or neutral, depending on the direction of these underlying variables. Notably, our model describes gold as more of a monetary asset than a commodity.

In our gold model, we show that changes in US Dollar gold prices are driven by (direction in parenthesis):

- Changes in the US Dollar basket (-)

- Consumer Price Index (CPI) inflation (+)

- Changes in nominal yields on 10-year US Treasuries (-)

- Investor sentiment (measured by speculative positioning in the futures market) (+)

We chose to put both inflation and nominal yields into the model as a proxy for real yields, rather than real yields directly so that we could use a longer data set (Treasury Inflation Protected Securities have only been around since 1997), and our model goes back to 1995 when Commodity Futures Trading Commission (CFTC) data on speculative futures market positioning first starts.

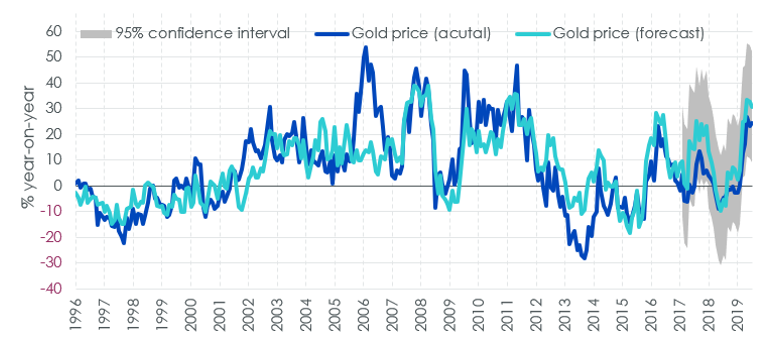

Figure 1 shows forecasts when calibrating our model using data from April 1996 to April 2017.

Figure 1. Gold price model in ”out of sample” test

As you can see, our model tracks the actual price of gold quite well. However, we have also added new variables to the model to see if they enhance its explanatory power.

Additional variables

To this base model we added a number of extra variables over the April 1995 to April 2018 period. Here’s what we found:

- Equity markets: Year-on-year changes in gold prices were negatively related to year-on-year changes in the S&P 500 and including the equity market indicator in the model weakened the significance of nominal yields. So, we chose not to include an equity market factor in our final model.

- Volatility: Changes in the option implied volatility of the S&P500 (CBOE Volatility Index, VIX) did not help explain gold prices. Many people regard gold as a hedge against surprises, but we found that the VIX didn’t have a significant impact in our model. This may have been related to the monthly frequency of our model as surprises are often too short-lived to be picked up in a monthly model.

- ETP assets: Gold prices appeared to be negatively associated with changes in gold exchange traded product (ETP) assets under management (measured in ounces) and the results cast doubt on the popular assertion that rising gold ETP demand has been responsible for higher gold prices.

- US Federal Reserve (Fed) balance sheet: Changes in the Fed’s balance sheet size and changes in US M2 money supply growth were also not a significant factor in explaining gold prices. This was a surprising result, given the focus on monetary expansion in the context of gold price movements. However, it could just be the case that the US Dollar basket picks up most of the relationship. Changes in the combined balance sheets of the Fed, European Central Bank, Bank of Japan and Swiss National Bank were also not significant.

Does physical demand matter?

We also looked at whether non-ETP demand for gold (jewellery, technology, bullion, and central bank purchases) can explain gold price movements. To do this, we switched to a quarterly model of gold prices in order to incorporate the quarterly gold demand data from the World Gold Council, and shortened the span of the model to 2005 due to data limitations.

Here, our research indicated that physical gold demand is also not a relevant factor in explaining gold prices.

What has been the most important driver of gold prices in the past?

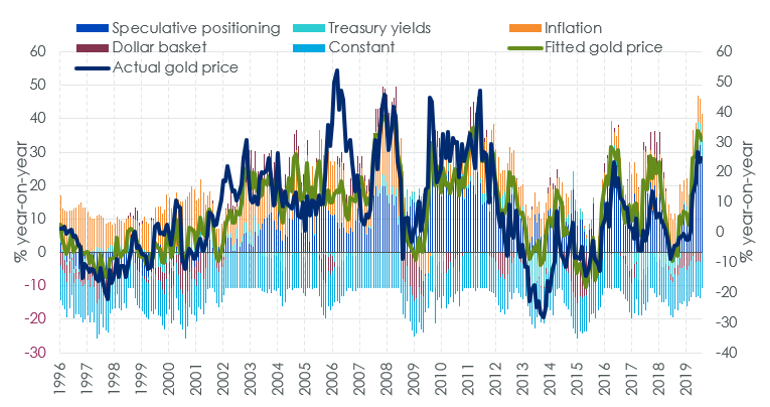

This is a question that comes up regularly and unfortunately, it’s not a simple question to answer. This is because, as shown in Figure 2, at times a variable can have a large impact on the price of gold and at other times its impact can be minimal.

Figure 2. The impact of each variable: attribution of fitted results vs. actual price

How we use our gold model

Ultimately, understanding gold’s historic behaviour allows us to make future gold price forecasts, as long as we have a view on the explanatory variables.

By analysing key macroeconomic factors, including Federal Reserve policy, Treasury yields, and exchange rates, our gold model can be used to produce gold price forecasts.

For those interested, we will shortly be releasing our updated outlook for gold prices up to Q2 2020.

By: Nitesh Shah, Director, Research, WisdomTree

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Gruvbolaget Boliden överträffade analytikernas förväntningar med bred marginal när man presenterade resultatet för det tredje kvartalet. Mikael Staffas, vd för Boliden, kommenterar kvartalet och hur han ser på råvarumarknaden och bolagets olika gruvprojekt.

USA:s president Donald Trump och Australiens premiärminister Anthony Albanese undertecknade på måndagen ett avtal som ska tillföra miljarder dollar till projekt inom kritiska mineraler.

Länderna kommer tillsammans att bidra med 1-3 miljarder dollar till projekten under de kommande sex månaderna. Den totala projektportföljen är värd 8,5 miljarder dollar, enligt regeringarna.

Galliumraffinaderi med kapacitet för 5x USA:s efterfrågan

Som en del av avtalet kommer det amerikanska försvarsdepartementet även att investera i ett galliumraffinaderi i västra Australien med en kapacitet på 100 ton per år. För närvarande importerar USA omkring 21 ton gallium, vilket motsvarar hela den inhemska konsumtionen, enligt den amerikanska geologiska myndigheten.

Initiativet kommer samtidigt som Kina har infört exportrestriktioner på vissa mineraler, däribland sällsynta jordartsmetaller, som är avgörande för tillverkningen av elektronik och elmotorer. Gallium används till exempel i mikrovågskretsar samt blå och violetta lysdioder (LED), vilka kan användas för att skapa kraftfulla lasrar.

Guldpriset har nyligen nått rekordnivåer, över 4 000 dollar per uns. Denna uppgång är inte bara ett resultat av spekulation, utan speglar djupare förändringar i den globala ekonomin. Bloomberg analyserar hur detta hänger samman med minskad tillit till dollarn, geopolitisk oro och förändrade investeringsmönster.

Guldets roll som säker tillgång har stärkts i takt med att förtroendet för den amerikanska centralbanken minskat. Osäkerhet kring Federal Reserves oberoende, inflationens utveckling och USA:s ekonomiska stabilitet har fått investerare att söka alternativ till fiatvalutor. Donald Trumps handelskrig har också bidragit till att underminera dollarns status som global reservvaluta.

Samtidigt ökar den geopolitiska spänningen, särskilt mellan USA och Kina. Kapitalflykt från Kina, driven av oro för övertryckta valutor och instabilitet i det finansiella systemet, har lett till ökad efterfrågan på guld. Även kryptovalutor som bitcoin stiger i värde, vilket tyder på ett bredare skifte mot hårda tillgångar.

Bloomberg lyfter fram att derivatmarknaden för guld visar tecken på spekulativ överhettning. Positioneringsdata och avvikelser i terminskurvor tyder på att investerare roterar bort från aktier och obligationer till guld. ETF-flöden och CFTC-statistik bekräftar denna trend.

En annan aspekt är att de superrika nu köper upp alla tillgångsslag – aktier, fastigheter, statsobligationer och guld – vilket bryter mot traditionella investeringslogiker där vissa tillgångar fungerar som motvikt till andra. Detta tyder på att marknaden är ur balans och att kapitalfördelningen är skev.

Sammanfattningsvis är guldets prisrally ett tecken på en värld i ekonomisk omkalibrering. Det signalerar misstro mot fiatvalutor, oro för geopolitisk instabilitet och ett skifte i hur investerare ser på risk och trygghet.

Sell the rally. Trump has become predictable in his unpredictability

Gruvbolaget Boliden överträffade analytikernas förväntningar

Australien och USA investerar 8,5 miljarder USD för försörjningskedja av kritiska mineraler

Brent crude set to dip its feet into the high $50ies/b this week

Vad guldets uppgång egentligen betyder för världen

OPEC+ missar produktionsmål, stöder oljepriserna

Goldman Sachs höjer prognosen för guld, tror priset når 4900 USD

Blykalla och amerikanska Oklo inleder ett samarbete

Guld nära 4000 USD och silver 50 USD, därför kan de fortsätta stiga

Leading Edge Materials är på rätt plats i rätt tid

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanOPEC+ missar produktionsmål, stöder oljepriserna

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGoldman Sachs höjer prognosen för guld, tror priset når 4900 USD

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBlykalla och amerikanska Oklo inleder ett samarbete

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGuld nära 4000 USD och silver 50 USD, därför kan de fortsätta stiga

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanLeading Edge Materials är på rätt plats i rätt tid

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanNytt prisrekord, guld stiger över 4000 USD

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEtt samtal om guld, olja, koppar och stål

-

Analys3 veckor sedan

Analys3 veckor sedanOPEC+ will likely unwind 500 kb/d of voluntary quotas in October. But a full unwind of 1.5 mb/d in one go could be in the cards