Analys

SHB Råvarubrevet 25 maj 2012

Marknaden har fortsatt att präglas av svalare riskaptit sedan förra veckobrevet. Råvaror tillsammans med börser och räntor har fallit. Oron för en grekisk närtida exit får sägas ha ökat, ratingnedgraderingarna har stått som spön i backen, spanska problemlån klättrar snabbt medan makrostatistiken inte gett några skäl till optimism. Kinadata har fortsatt att vara besvikelser med banken HSBCs preliminära inköpschefsindex för maj som senaste exempel. Vi tror på en kommande stark återhämtning för kinaexponerade råvaror – men inte ännu!

Marknaden har fortsatt att präglas av svalare riskaptit sedan förra veckobrevet. Råvaror tillsammans med börser och räntor har fallit. Oron för en grekisk närtida exit får sägas ha ökat, ratingnedgraderingarna har stått som spön i backen, spanska problemlån klättrar snabbt medan makrostatistiken inte gett några skäl till optimism. Kinadata har fortsatt att vara besvikelser med banken HSBCs preliminära inköpschefsindex för maj som senaste exempel. Vi tror på en kommande stark återhämtning för kinaexponerade råvaror – men inte ännu!

Parallellt med de negativa rubrikerna så har förväntansbilden skruvats ned kraftigt och det minskar risken för att makrodata blir besvikelser i närtid. När tillgångar har falligt med 10 – 15 % (OMX 30 och Brent) på mindre än två månader så brukar det komma en kort rekyl när köpintresset ökar igen.

Vi konstaterar att mycket dålig data kommit på kort tid och tryckt ner marknaden. Vi ser fortfarande flera nedåtrisker på 2 månaders sikt men tycker att detta kan vara ett intressant läge för den riskvillige att kortsiktigt söka avkastning i en annars dyster miljö. Vi favoriserar då mindre kinaexponerade råvaror som olja, som vi dessutom tycker har starkast fundamentalt stöd utav råvarorna.

Energi (neutral)

Olja

Oljemarknaden (Brent) som backade med ytterligare 3 procent ned till 105 dollar under inledningen av veckan återhämtar delar av rörelsen mot slutet vilket får ses som en korrektion. Fokus på Europa och lägre riskaptit för råvaror överlag men ser vi till det fundamentala lär även förbrukningsprognoser för den amerikanska marknaden skrivas ned något ytterligare inom den närmaste framtiden. En del stöd från amerikanska bensinlager som fortsatte ned och totalt nu fallit med 30 miljoner fat de senaste tre månaderna. Inga stora nyheter kring Iran där diskussionerna kring kärnvapenprogrammet flyttas fram till nästa månad. En nyhet om 300,000 fat mindre Iransk olja till marknaden med ett potentiellt scenario om 1 miljoner bortfall skulle tidigare givit ett ordentligt stöd åt köparna men i denna pessimistiska miljö påverkar det knappt alls. Trots en tekniskt väldigt översåld marknad verkar det fortsatt som risken finns på nedsidan på kort sikt.

Elmarknaden

Den försvagade energibalansen som bidrog till förra veckans uppgång genererade även inledningsvis av denna vecka en del köpintressen i marknaden. Överskottet om närmare 12 TWh har krympt till 6TWh på lite drygt en månad. Kvartalet Q3 2012 som är underliggande för SHB Power Index och våra sparprodukter handlas dock oförändrat efter att sentimentet försvagades något i mitten av veckan till följd av den allmänna utvecklingen på börserna. Mot slutet av veckan pekar prognoserna fortsatt på ett något torrare scenario där vi förväntas få mellan 2-4 TWh vilket därmed är något under normalen om 4.2 TWh för perioden. Denna högtrycksuppbyggnad och torra period har balanserats något av den svaga kolmarknaden där ett stort överskott och en stark dollar verkat negativt för kol och dämpa utvecklingen på el. En viss rekyl på både kol (där brytpriset för kolkraft stigit med ca 1 euro) och utsläppsrätter mot slutet av veckan men vi bedömer detta som tillfälligt och förväntar oss ingen vidare uppgång, snarare tvärtom.

Ser vi till den korta kurvan så är spotpriserna riktigt låga och väntas så vara även under nästa vecka. De höga temperaturerna gör att vattenproducenter har svårt att upprätthålla spotpriset på någon högre nivå till följd av den kraftiga snösmältningen. För att sammanfatta läget talar flera faktorer för att vi kommer att ligga kvar på dessa låga nivåer och om inte prognoserna slår om till betydligt torrare än de vi ser idag bör Q3 2012 kunna falla tillbaka någon euro under inledningen av nästa vecka.

Basmetaller (neutral)

Kopparpriset har pendlat upp och ner i pris under veckan för att stänga på ungefär oförändrat. Sedan årets början är priset ned ca 1.7 %. Koppar har den senaste tiden tagit stryk på grund av oron kring Grekland och världsekonomin. Som bekant anses metallen vara en ledande indikator för världskonjunkturen.

Kopparlagren från LME ökade för första gången på 7 veckor. Nyligen släppta produktionssiffror visar på att brytningen av koppar kommer överstiga efterfrågan redan i år och även 2014. I den andra vågskålen hittar vi siffror från världens största kopparproducent, chilenska Codelco. Företaget har producerat 10 % mindre koppar första kvartalet jämfört med första kvartalet 2011. Den främsta anledningen sägs vara minskade kopparhalter i malmen. Sammantaget är vi neutrala till kopparpriset.

Aluminiumpriset har under veckan gått ned med 2.4 %. Nedgången hittills i år är 2.8 %. Priset ligger i skrivande stund på 2 018 USD/ton. Ett flertal kunder har visst intresse att köpa strax över 2 000 USD-nivån. Cash-cost, det vill säga kostnaden för att få fram ett ton, ligger runt 1 900 enligt flera bedömare. Att kunna säkra in sin exponering på något över 2 000 har lockat in köparna.

Om vi försöker hitta positiva signaler kring världsekonomin så hittar vi det faktiskt i aluminiummarknaden. Leveranser till japanska förbrukare är upp för den tredje månaden i rad. Vi även snappat upp att importen av bauxit (råvaran till aluminium) till Kina har gått 49 % jämfört med förra året. Vi är neutrala till metaller och aluminium prismässigt, men tror att aluminium har bäst potential för prisuppgång på sikt.

Ädelmetaller

I slutet av förra veckan studsade guldet upp ganska ordentligt från nya årslägsta-nivåer, men denna veckan har vi sett det glida tillbaks med 2 %. Även övriga ädelmetaller har fallit i samma storleksordning, under en lugn vecka. Vi håller fast vår negativa syn på sektorn baserat på avsaknad av performance i den riskaverta miljö vi haft under senare tid.

Softs

Kaffe

Marknaden inväntar de brasilianska arabica skördarna vilka fortskrider något långsammare i år än tidigare år p.g.a. regn. Skördarna förväntas bli goda till följd av gynnsamma väderförhållanden under gångna säsongen men det råder fortsättningsvis en ovisshet beträffande landets kommande exportvolym då man ser en ökad inhemsk konsumtion. Efterfrågan på arabica kaffet har varit låg då flertalet köpare haft välfyllda lager inför skörden 2012/13.

Priset på arabica bönan har sjunkit drygt 20 % under 2012 inväntandes 2011/12 skörden vi nu står inför, kaffekonsumtionen förväntas öka globalt de kommande åren och skörden 2013-14 benämns som ett ”off” år i arabicakaffets skördecykler (högre/lägre skörd vartannat år).

Socker

Socker handlades upp något i början av veckan till följd av det något torrare vädret i Brasilien och därmed risk för sämre skördar. Även en något ökad efterfrågan och rapporter om ökat antal lastfartyg vid de brasilianska hamnarna redo för lastning av råvaran fick priset att stiga. Det ekonomiska läget i Europa fick priset på socker att sjunka igen mot mitten av veckan och handlas fortsättningsvis lågt. Marknaden är något avvaktande inför brasilianska skördeperioden som inleds om bara några veckor, och inväntar även handeln inför ramadan som hittills varit modest. Ramadan inleds i juli och de muslimska länderna brukar fylla sina lager innan dess. Indien som förra veckan beslöt att tillåta obegränsad export av socker har inte publicerat sin planerade exportvolym. Indiens skördar är goda i år och det socker de inte exporterar i år har de möjlighet att lagra för export nästa år, vilket i sin tur kan påverka priset på sikt.

Apelsinjuice

Priset på apelsinjuice fortsätter på sin låga nivå till följd av ökat utbud och den rådande ekonomiska situationen i Europa håller efterfrågan på fortsatt låga nivåer. Väderförhållandena har varit gynnsamma och skördarna är goda. Florida närmar sig orkansäsongen och antalet namngivna orkaner motsvarar tidigare år även om man i år inväntar orkaner något tidigare på säsongen. Även om säsongens tidiga orkaner i sig inte verkar utgöra något större hot för skörden påminner de marknaden om risken och tillfälliga uppgångar i priset har setts. Brasiliens Real har tappat 5,5 % mot USD sedan jan 2012.

Handelsbankens Råvaruindex

Handelsbankens råvaruindex består av de underliggande indexen för respektive råvara. Vikterna är bestämda till hälften från värdet av global produktion och till hälften från likviditeten i terminskontrakten.

Handelsbankens råvaruindex består av de underliggande indexen för respektive råvara. Vikterna är bestämda till hälften från värdet av global produktion och till hälften från likviditeten i terminskontrakten.

[box]SHB Råvarubrevet är producerat av Handelsbanken och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Ansvarsbegränsning

Detta material är producerat av Svenska Handelsbanken AB (publ) i fortsättningen kallad Handelsbanken. De som arbetar med innehållet är inte analytiker och materialet är inte oberoende investeringsanalys. Innehållet är uteslutande avsett för kunder i Sverige. Syftet är att ge en allmän information till Handelsbankens kunder och utgör inte ett personligt investeringsråd eller en personlig rekommendation. Informationen ska inte ensamt utgöra underlag för investeringsbeslut. Kunder bör inhämta råd från sina rådgivare och basera sina investeringsbeslut utifrån egen erfarenhet.

Informationen i materialet kan ändras och också avvika från de åsikter som uttrycks i oberoende investeringsanalyser från Handelsbanken. Informationen grundar sig på allmänt tillgänglig information och är hämtad från källor som bedöms som tillförlitliga, men riktigheten kan inte garanteras och informationen kan vara ofullständig eller nedkortad. Ingen del av förslaget får reproduceras eller distribueras till någon annan person utan att Handelsbanken dessförinnan lämnat sitt skriftliga medgivande. Handelsbanken ansvarar inte för att materialet används på ett sätt som strider mot förbudet mot vidarebefordran eller offentliggörs i strid med bankens regler.

Wild moves yesterday. Brent crude traded to a high of $114.43/b and a low of $96.0/b and closed at $99.94/b yesterday.

US – Iran negotiations ongoing or not? What a day. Donald Trump announced that good talks were ongoing between Iran and the US and that the 48 hour deadline before bombing Iranian power plants and energy infrastructure was postponed by five days subject to success of ongoing meetings. Iranian media meanwhile stated that no meetings were ongoing at all.

Today we are scratching our heads trying to figure out what yesterday was all about.

Friends and family playing the market? Was it just Trump and his friends and family who were playing with oil and equity markets with $580m and $1.46bn in bets being placed by someone in oil and equity markets just 15 minutes before Trump’s announcement?

Was Trump pulling a TACO as he reached his political and economic pain point: Brent at $112/b, US Gas at $4/gal, SPX below 200dma and US 10yr above 4.4%?

Different Iranian factions with Trump talking with one of them? Are there real negotiations going on but with the US talking to one faction in Iran while another, the hardliners, are not involved and are denying any such negotiations going on?

Extending the ultimatum to attack and invade Kharg island next weekend? Or, is the five day delay of the deadline a tactical decision to allow US amphibious assault ships and marines to arrive in the Gulf in the upcoming weekend while US and Israeli continues to degrade Iranian military targets till then. And then next weekend a move by the US/Israel to attack and conquer for example the Kharg island?

We do not really know which it is or maybe a combination of these.

We did get some kind of TACO ydy. But markets have been waiting for some kind of TACO to happen and yesterday we got some kind of TACO. And Brent crude is now trading at $101.5/b as a result rather than at $112-114/b as it did no the high yesterday.

But what really matters in our view is the political situation on the ground in Iran. Will hardliners continue to hold power or will a more pragmatic faction gain power?

If the hardliners remain in power then oil pain should extend all the way to US midterm elections. The hardliners were apparently still in charge as of last week. Iran immediately retaliated and damaged LNG infrastructure in Qatar after Israel hit Iranian South Pars. The SoH was still closed and all messages coming out of Iran indicated defiance. Hardliners continues in power has a huge consequence for oil prices going forward. The regime has played its ’oil-weapon’ (closing or chocking the Strait of Hormuz). It is using it to achieve political goals. Deterrence: it needs to be so politically and economically expensive to attack Iran that it won’t happen again in the future. Or at least that the US/Israel thinks 10-times over before they attack again. The highest Brent crude oil closing price since the start of the war is $112.19/b last Friday. In comparison the 20-year inflation adjusted Brent price is $103/b. So Brent crude last Friday at $112.19/b isn’t a shockingly high price. And it is still far below the nominal high of $148/b from 2008 which is $220/b if inflation adjusted. So once in a lifetime Iran activates its most powerful weapon. The oil weapon. It needs to show the power of this weapon and it needs to reap political gains. Getting Brent to $112/b and intraday high of $119.5/b (9 March) isn’t a display of the power of that weapon. And it is not a deterrence against future attacks.

So if the hardliners remain in power in Iran, then the SoH will likely remain chocked all the way to US midterm elections and Brent crude will at a minimum go above the historical nominal high of $148/b from 2008.

Thus the outlook for the oil price for the rest of the year doesn’t depend all that much of whether Trump pulls a TACO or not. Stops bombing or not. It depends more on who is in charge in Iran. If it is the hardliners, then deterrence against future attacks via chocking of the SoH and high oil prices is the likely line of action. It is impacting the world but the Iranian ’oil-weapon’ is directed towards the US president and the the US midterm elections.

If a pragmatic faction gets to power in Iran, then a very prosperous future is possible. However, if power is shifting towards a more pragmatic faction in Iran then a completely different direction could evolve. Such a faction could possibly be open for cooperation with the US and the GCC and possibly put its issues versus Israel aside. Then the prosperity we have seen evolving in Dubai could be a possible future also for Iran.

So far it looks like the hardliners are fully in charge. As far as we can see, the hardliners are still fully in control in Iran. That points towards continued chocking of the SoH and oil prices ticking higher as global inventories (the oil market buffers) are drawn lower. And not just for a few more weeks, but possibly all the way to the US midterm elections.

A brief sigh of relief yesterday as oil infra at Kharg wasn’t damaged. But higher today. Brent crude dabbled around a bit yesterday in relief that oil infrastructure at Iran’s Kharg island wasn’t damaged. It traded briefly below the 100-line and in a range of $99.54 – 106.5/b. Its close was near the low at $100.21/b.

No easy victorious way out for Trump. So no end in sight yet. Brent is up 3.2% today to $103.4/b with no signs that the war will end anytime soon. Trump has no easy way to declare victory and mission accomplished as long as Iran is in full control of the Strait of Hormuz while also holding some 440 kg of uranium enriched to 60% and not far from weapons grade at 90%. As long as these two factors are unresolved it is difficult for Trump to pull out of the Middle East. Naturally he gets increasingly frustrated over the situation as the oil price and US retail gas prices keeps ticking higher while the US is tied into the mess in the Middle East. Trying to drag NATO members into his mess but not much luck there.

When commodity prices spike they spike 2x, 3x, 4x or 5x. Supply and demand for commodities are notoriously inflexible. When either of them shifts sharply, the the price can easily go to zero (April 2022) or multiply 2x, 3x, or even 5x of normal. Examples in case cobalt in 2025 where Kongo restricted supply and the price doubled. Global LNG in 2022 where the price went 5x normal for the full year average. Demand for tungsten in ammunition is up strongly along with full war in the middle east. And its price? Up 537%.

Why hasn’t the Brent crude oil price gone 2x, 3x, 4x or 5x versus its normal of $68/b given close to full stop in the flow of oil of the Strait of Hormuz? We are after all talking about close to 20% of global supply being disrupted. The reason is the buffers. It is fairly easy to store oil. Commercial operators only hold stocks for logistical variations. It is a lot of oil in commercial stocks, but that is predominantly because the whole oil system is so huge. In addition we have Strategic Petroleum Reserves (SPRs) of close to 2500 mb of crude and 1000 mb of oil products. The IEA last week decided to release 400 mb from global SPR. Equal to 20 days of full closure of the Strait of Hormuz. Thus oil in commercial stocks on land, commercial oil in transit at sea and release of oil from SPRs is currently buffering the situation.

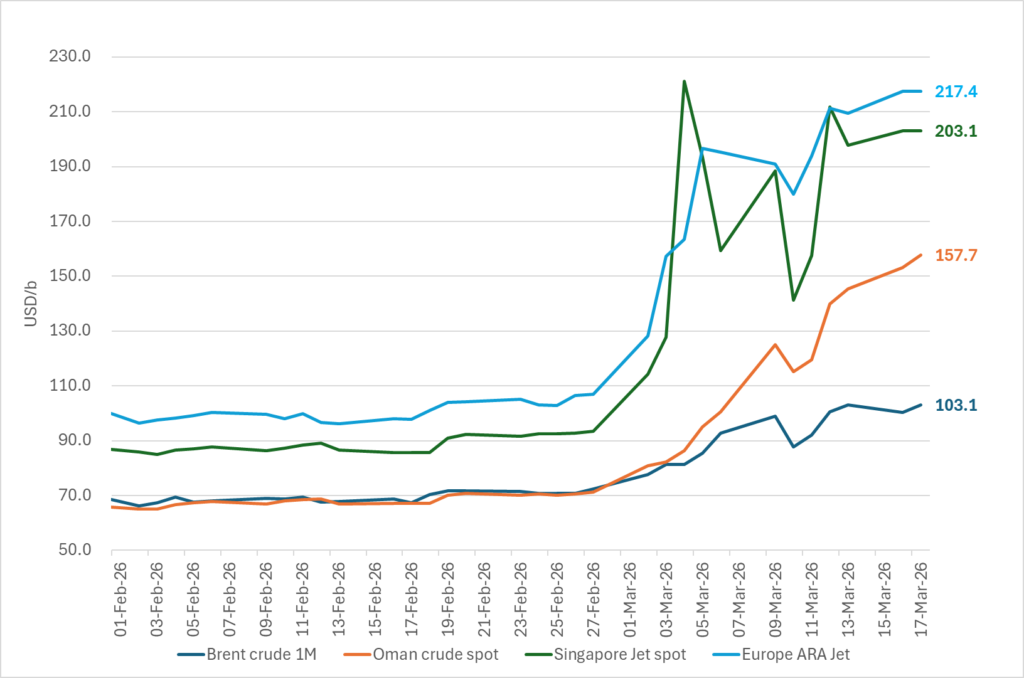

But we are running the buffers down day by day. As a result we see gradually increasing stress here and there in the global oil market. Asia is feeling the pinch the most. It has very low self sufficiency of oil and most of the exports from the Gulf normally head to Asia. Availability of propane and butane many places in India (LPG) has dried up very quickly. Local prices have tripled as a result. Local availability of crude, bunker oil, fuel oil, jet fuel, naphtha and other oil products is quickly running down to critical levels many places in Asia with prices shooting up. Oman crude oil is marked at $153/b. Jet fuel in Singapore is marked at $191/b.

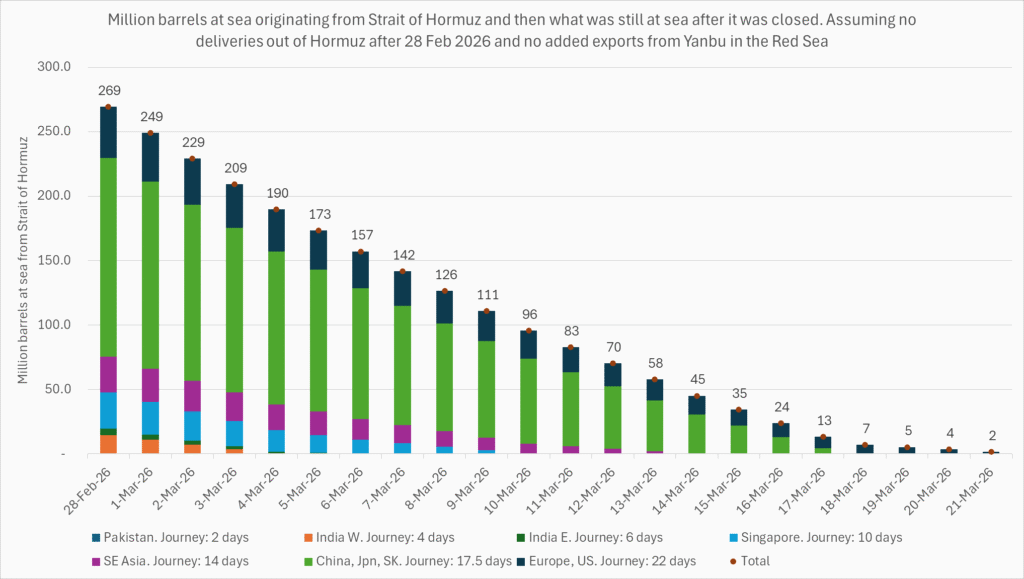

Oil at sea originating from Strait of Hormuz from before 28 Feb is rapidly emptied. Oil at sea is a large pool of commercial oil. An inventory of oil in constant move. If we assume that the average journey from the Persian Gulf to its destinations has a volume weighted average of 13.5 days then the amount of oil at sea originating from the Persian Gulf when the the US/Israel attacked on 28 Feb was 13.5 days * 20 mb/d = 269 mb. Since the strait closed, this oil has increasingly been delivered at its destinations. Those closest to the Strait, like Pakistan, felt the emptying of this supply chain the fastest. Propane prices shooting to 3x normal there already last week and restaurants serving cold food this week is a result of that. Some 50-60% of Asia’s imports of Naphtha normally originates from the Persian Gulf. So naphtha is a natural pain point for Asia. The Gulf also a large and important exporter of Jet fuel. That shut in has lifted jet prices above $200/b.

To simplify our calculations we assume that no oil has left the Strait since that date and that there is no increase in Saudi exports from Yanbu. Then the draining of this inventory at sea originated from the Persian Gulf will essentially look like this:

The supply chain of oil at sea originating from the Strait of Hormuz is soon empty. Except for oil allowed through the Strait of Hormuz by Iran and increased exports from Yanbu in the Red Sea. Not included here.

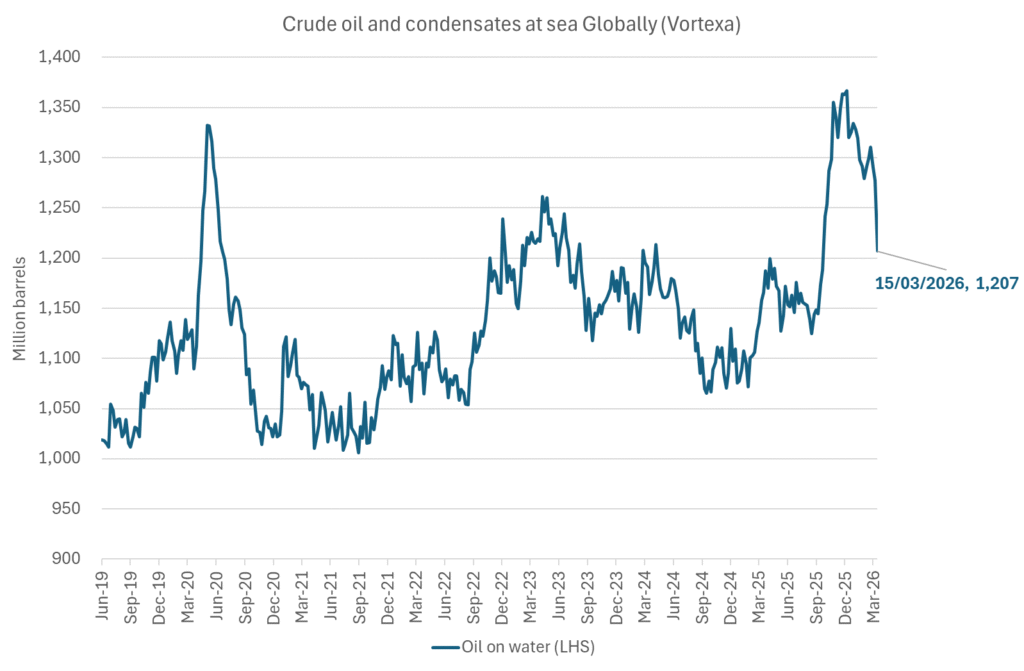

Oil at sea is falling fast as oil is delivered without any new refill in the Persian Gulf. Waivers for Russian crude is also shifting Russian crude to consumers. Brent crude will likely start to feel the pinch much more forcefully when oil at sea is drawn down another 200 mb to around 1000 mb. That is not much more than 10 days from here.

Oil and oil products are starting to become very pricy many places. Brent crude has still been shielded from spiking like the others.

Closing at highest since Aug 2022. Brent crude gained 9.2% yesterday. The trading range was limited to $95.2 – 101.85/b with a close at $100.46/b and higher than the Monday close of $98.96/b. Ydy close was the highest close since August 2022. This morning Brent is up 2% to $102.4/b and is trading at the highest intraday level since Monday when it high an intraday high of $119.5/b.

A military hit at Iran’s Kharg island would be a big, big bang for the oil price. The big, big risk for the weekend is that oil infrastructure could be damaged. For example Iran’s Kharg island which is Iran’s major oil export hub. If damaged we would have a longer lasting loss of supply stretching way beyond Trump’s announced ”two more weeks”. It will make the spot price spike higher and it will lift the curve. Brent crude 2027 swap would jump above $80/b immediately. An attack on Kharg island would naturally lead Iran to strike back at other oil infrastructures in the Gulf. Especially those belonging to countries who harbor US military bases. I.e. countries who essentially are supporting the attack by US and Israel towards Iran. Though if not in spirit, then in practical operational terms. An attack on Kharg island would not just lead to a lasting outage of supply from Iran until it would be repaired. It would immediately endanger other oil infrastructure in the region as well and additional lasting loss of supply.

No one in their right mind would dare to sit short oil over the coming weekend. Oil is thus set to close the week at a very strong note today.

Prepare for another 400 mb SPR release next week. This week’s announcement of a 400 mb release from Strategic Oil Reserves totally underwhelmed the market with the oil price going higher rather than lower following the announcement. For one it means that the market expects the war and the closure of the Strait of Hormuz to last longer than Trump’s recent announced ”two more weeks”. 400 mb only amounts to 20 days of lost supply to the world through Hormuz and we are already at day 14. So next week when we are getting close to the 20 day mark, we are likely to see another announcement of another 400 mb release of SPR stocks to the market. Preparing for the next 20 days of war.

Global oil logistics in total disarray. We have previously addressed the issue of the huge logistical web of the global oil market which is now in total disarray. The logistical disruption started to fry the oil market at the end of last week. Helped to spike the oil market on Monday. What we hear from our shipping clients is that the problems with supply of fuels locally in Korea, Singapore, India and Africa are getting worse with physical availability of fuels there drying up. It is getting increasingly difficult to find physical supply of bunker oil with local, physical prices shooting way higher than financial benchmarks. To the point that biofuels have become the cheap option many places. Availability of fuels in the US is still good. Not so surprising as the US is self-sufficient with crude and refineries.

The disruption in global oil logistics doesn’t seem to improve. Rather the opposite. If you cannot get fuel to run your ships, then how can you distribute fuels to where it is needed.

Buy Brent Dec-2026 calls with strike $150/b!! As the days goes by the oil price is ticking higher while Trump is getting one day closer to US midterm elections. Trump was betting that he could put this war to bead well before November. But that will probably not be up to him to decide. It will be up to Iran to decide when to reopen the Strait of Hormuz. It is very hard to imagine that Iran will let Trump easily off the hock after he has killed its Supreme Leader. This will likely go all the way to November. Buy Brent Dec-2026 calls with strike $150/b!!

Brent closed at highest since 2022 ydy. Will end this Friday at a very strong note! Consumers still dreaming of $60/b oil

Christian Kopfer om läget för oljan

Marknaden måste börja betrakta de höga kopparpriserna som det nya normala

Det fysiska spotpriset på brentolja har slagit nytt rekord

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

Efter tillväxten: Guldbrev satsar på expansion i Europa

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

Elpriserna fördubblas, stor osäkerhet inför sommaren

MP Materials, USA:s svar på Kinas dominans över sällsynta jordartsmetaller

Det fysiska spotpriset på brentolja har slagit nytt rekord

Studsvik har idag ansökt om att få bygga 1200-1600 MW kärnkraft i Valdemarsvik

-

Nyheter2 veckor sedan

Nyheter2 veckor sedan40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanElpriserna fördubblas, stor osäkerhet inför sommaren

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMP Materials, USA:s svar på Kinas dominans över sällsynta jordartsmetaller

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDet fysiska spotpriset på brentolja har slagit nytt rekord

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanStudsvik har idag ansökt om att få bygga 1200-1600 MW kärnkraft i Valdemarsvik

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMarknaden måste börja betrakta de höga kopparpriserna som det nya normala

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMatproduktion är beroende av gödsel, Gulfkriget skapar brist

-

Analys4 veckor sedan

TACO (or Whatever It Was) Sends Oil Lower — Iran Keeps Choking Hormuz