Analys

A moment in markets – Commodity returns can be enhanced

In ‘A moment in markets – Are we in a commodity supercycle?’ the promising environment for commodities, especially sectors like industrial metals, was outlined. But for investors who endorse the case for commodities, portfolio implementation is the natural next step to ponder over. In many cases, having a pure beta exposure to commodities makes perfect sense. In some instances, however, smarter approaches present viable alternatives.

The return breakdown

Investors who are not interested in storing physical commodities are likely to seek synthetic exposures to the asset class. Exchange-traded commodity products are either physically-backed or synthetic, i.e., exposed to futures. When it comes to commodity futures exposure, the total return to investors is as follows:

To avoid getting physical delivery of commodities upon expiry of the futures contract, investors maintain their exposure by rolling their futures position to a contract with later maturity. This process can incur a carry return because futures prices may converge to spot prices over time, i.e., there is a gain or loss in carrying the futures contract up or down the curve. When futures curves are in contango, i.e., prices are upward sloping, roll yield is typically negative and when curves are in backwardation, i.e., prices are downwards sloping, roll yield is typically positive.

A pure beta approach would normally provide exposure to contracts towards the front end of the futures curve. Such strategies tend to do well relative to those that are exposed to contracts further out along the futures curve when commodity prices are in a bull run and the spot return component is dominating total returns. This is because contracts at the front end are closer to the spot price and normally experience higher price fluctuation than those further along the curve. The roll return will, however, depend on the shape of the futures curve.

Optimizing the roll return

In contrast to the front-month approach, a dynamic approach to selecting futures contracts that promises a potentially better roll yield can add incremental value to total returns over a longer period. For example, the Bloomberg Commodity Index (BCOM) approach invests in contracts towards the front end of the futures contract.

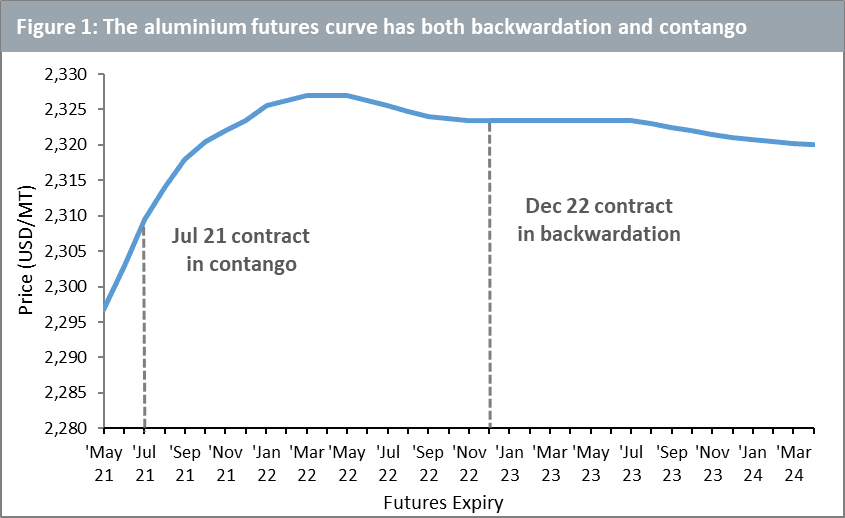

In figure 1 the case of aluminium is currently the July 2021 contract. In contrast, the S&P GSCI Aluminium Dynamic Roll Index, which reassesses its exposure monthly and can go further out on the curve, is currently in the December 2022 contract.

Looking at the shape of aluminium’s futures curve, we can observe that while July 2021 faces contango, the curve is in slight backwardation around the December 2022 contract (see figure 1 below).

Certain approaches give exposure to specific points along the futures curve, e.g., the UBS Bloomberg Constant Maturity Commodity Index (CMCI). Each approach has its own merits and investors should take the time to familiarise themselves with the methodology.

The key distinction for a dynamic approach in the current macro environment is that sharp fluctuations in demand and supply conditions in recent months have caused futures curves to frequently change shape. Aluminium’s entire curve at the end of January was in steep contango before becoming much flatter when supply curtailment from Inner Mongolia in March tightened the market. While there is no single formula to predict which approach will outperform when, it is useful to recognise that curves can change shape, and this can have an impact on roll returns.

The deciding factor

With all the options available to investors, the decision comes down to whether the commodity exposure is a strategic or tactical decision. Enhanced approaches aim to add value by improving the carry return and reducing volatility – as longer tenor contracts tend to exhibit less price fluctuation compared to front-month contracts.

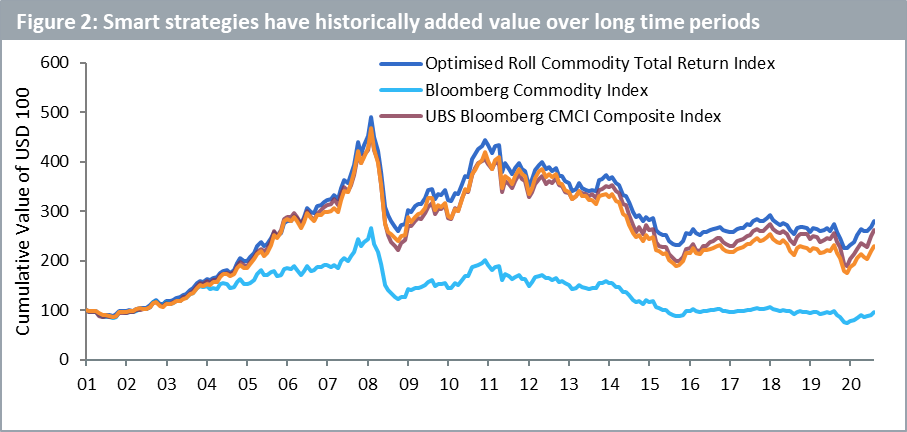

The true benefit of smarter approaches that seek to enhance the risk-return profile of commodities becomes apparent over longer periods (see figure 2). Enhanced approaches are, therefore, better suited to strategic investors looking for broad commodities exposure.

/Mobeen Tahir, Associate Director, Research, WisdomTree

Brent is climbing higher. Front-month is at USD 106.3/bl this morning, close to a weekly high and a USD 9/bl jump from Mondays open. This is the move we flagged as a risk earlier in the week: the market shifting from ”a deal is around the corner” to ”this is going to take longer than we thought”.

Analyst Commodities, SEB

During April, rest-of-year Brent remained remarkably stable around USD 90/bl. A stability which rested on one single assumption: the SoH reopens around 1 May. That assumption is now slowly falling apart.

As we highlighted yesterday: every week of delay beyond 1 May adds (theoretically) ish USD 5/bl to the rest-of-year average, as global inventories draw 100 million barrels per week. i.e., a mid-May reopening implies rest-of-year Brent closer to USD 100/bl, and anything pushing into June or July takes us meaningfully higher.

What’s changed in the last 48 hours:

#1: The US military has formally warned that clearing suspected sea mines from SoH could take up to six months. That is a completely different timescale from what the financial market is pricing. Even a political deal tomorrow does not immediately reopen the strait.

#2: Trump has shifted his tone from urgency to ”strategic patience”. In yesterday’s press conference: ”Don’t rush me… I want a great deal.” The market is reading this as a president no longer feeling pressured by timelines, with the naval blockade running in the background.

#3: So far, the military activity is escalating, not de-escalating. Axios reports Iran is laying more mines in SoH. The US 3rd carrier strike group (USS George H.W. Bush) is arriving with two countermine vessels. Trump yesterday ordered the US Navy to destroy any Iranian boats caught laying mines. While CNN reports that the Pentagon is actively drawing up plans to strike Iranian SoH capabilities and individual Iranian military leaders if the ceasefire collapses. i.e., NOT a attitude consistent with an imminent deal!

Spot crude and product prices eased off the early-April highs on a combination of system rerouting and deal optimism. Both now weakening. Goldman estimates April Gulf output is reduced by 14.5 mbl/d, or 57% of pre-war supply, a number that keeps getting worse the longer this drags on.

Demand-side adaptation is ongoing: S. Korea has cut its Middle East crude dependence from 69% to 56% by pulling more from the Americas and Africa, and Japan is kicking off a second round of SPR releases from 1 May. But SPRs are finite.

Ref. to the negotiations, we should not bet on speed. The current Iranian leadership is dominated by genuine hardliners willing to absorb economic pain and run the clock to extract concessions. That is not a setup for a rapid resolution. US/Israeli media briefings keep framing the delay as ”internal Iranian divisions”, the reality is more complicated and points toward weeks and months, not days.

Our point is that the complexity is large, and higher prices have only just started (given a scenario where the negotiations drag out in time). The market spent April leaning on the USD 90/bl rest-of-year assumption; that case is diminishing by the hour. If ”early May reopening” is replaced by ”June, July or later” over the next week or two, both crude and products have meaningful room to reprice higher from here. There is a high risk being short energy and betting on any immediate political resolution(!).

Down on Friday. Up on Monday. The Brent June crude oil contract traded down 5.1% last week to a close of $90.38/b. It reached a high of $103.87/b last Monday and a low of $86.09/b on Friday as Iran announced that the Strait of Hormuz was fully open for transit. That quickly changed over the weekend as the US upheld its blockade of Iranian oil exports while Iran naturally responded by closing the SoH again. The US blew a hole in the engine room of the Iranian ship TOUSKA and took custody of the ship on Sunday. Brent crude is up 5.6% this morning to $95.4/b.

The cease-fire is expiring tomorrow. The US has said it will send a delegation for a second round of negotiations in Islamabad in Pakistan. But Iran has for now rejected a second round of talks as it views US demands as unrealistic and excessive while the US is also blocking the Strait of Hormuz.

While Brent is up 5% this morning, the financial market is still very optimistic that progress will be made. That talks will continue and that the SoH will fully open by the start of May which is consistent with a rest-of-year average Brent crude oil price of around $90/b with the market now trading that balance at around $88/b.

Financial optimism vs. physical deterioration. We have a divergence where the financial market is trading negotiations, improvements and resolution while at the same time the physical market is deteriorating day by day. Physical oil flows remain constrained by disrupted flows, longer voyage times and elevated freight and insurance costs.

Financial markets are betting that a US/Iranian resolution will save us in time from violent shortages down the road. But every day that the SoH remains closed is bringing us closer to a potentially very painful point of shortages and much higher prices.

The US blockade is also a weapon of leverage against its European and Asian allies. When Iran closed the SoH it held the world economy as a hostage against the US. The US blockade of the SoH is of course blocking Iranian oil exports. But it is also an action of disruption directed towards Europe and Asia. The US has called for the rest of the world to engaged in the war with Iran: ”If you want oil from the Persian Gulf, then go and get it”. A risk is that the US plays brinkmanship with the global oil market directed towards its European and Asian allies and maybe even towards China to force them to engage and take part. Maybe unthinkable. But unthinkable has become the norm with Trump in the White House.

Wild moves yesterday. Brent crude traded to a high of $114.43/b and a low of $96.0/b and closed at $99.94/b yesterday.

US – Iran negotiations ongoing or not? What a day. Donald Trump announced that good talks were ongoing between Iran and the US and that the 48 hour deadline before bombing Iranian power plants and energy infrastructure was postponed by five days subject to success of ongoing meetings. Iranian media meanwhile stated that no meetings were ongoing at all.

Today we are scratching our heads trying to figure out what yesterday was all about.

Friends and family playing the market? Was it just Trump and his friends and family who were playing with oil and equity markets with $580m and $1.46bn in bets being placed by someone in oil and equity markets just 15 minutes before Trump’s announcement?

Was Trump pulling a TACO as he reached his political and economic pain point: Brent at $112/b, US Gas at $4/gal, SPX below 200dma and US 10yr above 4.4%?

Different Iranian factions with Trump talking with one of them? Are there real negotiations going on but with the US talking to one faction in Iran while another, the hardliners, are not involved and are denying any such negotiations going on?

Extending the ultimatum to attack and invade Kharg island next weekend? Or, is the five day delay of the deadline a tactical decision to allow US amphibious assault ships and marines to arrive in the Gulf in the upcoming weekend while US and Israeli continues to degrade Iranian military targets till then. And then next weekend a move by the US/Israel to attack and conquer for example the Kharg island?

We do not really know which it is or maybe a combination of these.

We did get some kind of TACO ydy. But markets have been waiting for some kind of TACO to happen and yesterday we got some kind of TACO. And Brent crude is now trading at $101.5/b as a result rather than at $112-114/b as it did no the high yesterday.

But what really matters in our view is the political situation on the ground in Iran. Will hardliners continue to hold power or will a more pragmatic faction gain power?

If the hardliners remain in power then oil pain should extend all the way to US midterm elections. The hardliners were apparently still in charge as of last week. Iran immediately retaliated and damaged LNG infrastructure in Qatar after Israel hit Iranian South Pars. The SoH was still closed and all messages coming out of Iran indicated defiance. Hardliners continues in power has a huge consequence for oil prices going forward. The regime has played its ’oil-weapon’ (closing or chocking the Strait of Hormuz). It is using it to achieve political goals. Deterrence: it needs to be so politically and economically expensive to attack Iran that it won’t happen again in the future. Or at least that the US/Israel thinks 10-times over before they attack again. The highest Brent crude oil closing price since the start of the war is $112.19/b last Friday. In comparison the 20-year inflation adjusted Brent price is $103/b. So Brent crude last Friday at $112.19/b isn’t a shockingly high price. And it is still far below the nominal high of $148/b from 2008 which is $220/b if inflation adjusted. So once in a lifetime Iran activates its most powerful weapon. The oil weapon. It needs to show the power of this weapon and it needs to reap political gains. Getting Brent to $112/b and intraday high of $119.5/b (9 March) isn’t a display of the power of that weapon. And it is not a deterrence against future attacks.

So if the hardliners remain in power in Iran, then the SoH will likely remain chocked all the way to US midterm elections and Brent crude will at a minimum go above the historical nominal high of $148/b from 2008.

Thus the outlook for the oil price for the rest of the year doesn’t depend all that much of whether Trump pulls a TACO or not. Stops bombing or not. It depends more on who is in charge in Iran. If it is the hardliners, then deterrence against future attacks via chocking of the SoH and high oil prices is the likely line of action. It is impacting the world but the Iranian ’oil-weapon’ is directed towards the US president and the the US midterm elections.

If a pragmatic faction gets to power in Iran, then a very prosperous future is possible. However, if power is shifting towards a more pragmatic faction in Iran then a completely different direction could evolve. Such a faction could possibly be open for cooperation with the US and the GCC and possibly put its issues versus Israel aside. Then the prosperity we have seen evolving in Dubai could be a possible future also for Iran.

So far it looks like the hardliners are fully in charge. As far as we can see, the hardliners are still fully in control in Iran. That points towards continued chocking of the SoH and oil prices ticking higher as global inventories (the oil market buffers) are drawn lower. And not just for a few more weeks, but possibly all the way to the US midterm elections.

Brent crude up USD 9/bl on the week… ”deal around the corner” narrative fades

Market Still Betting on Timely Resolution, But Each Day Raises Shortage Risk

Christian Kopfer om läget för oljan

Marknaden måste börja betrakta de höga kopparpriserna som det nya normala

Det fysiska spotpriset på brentolja har slagit nytt rekord

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

Elpriserna fördubblas, stor osäkerhet inför sommaren

Det fysiska spotpriset på brentolja har slagit nytt rekord

Marknaden måste börja betrakta de höga kopparpriserna som det nya normala

Christian Kopfer om läget för oljan

-

Nyheter3 veckor sedan

Nyheter3 veckor sedan40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanElpriserna fördubblas, stor osäkerhet inför sommaren

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDet fysiska spotpriset på brentolja har slagit nytt rekord

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanMarknaden måste börja betrakta de höga kopparpriserna som det nya normala

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanChristian Kopfer om läget för oljan

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEfter tillväxten: Guldbrev satsar på expansion i Europa

-

Analys5 dagar sedan

Market Still Betting on Timely Resolution, But Each Day Raises Shortage Risk

-

Analys20 timmar sedan

Brent crude up USD 9/bl on the week… ”deal around the corner” narrative fades