Nyheter

Smart money is rightfully turning to gold

▬ HOW CAN YOU BE BEARISH ON GOLD? ▬

DIFFERENCE BETWEEN TWO GOLD WATCHERS: BUT BOTH BULLISH!

Henk J. Krasenberg

Jim Sinclair is one of the most outspoken commentators on gold. In his long career in the business of metals, mines and money, he has built a prominent record of having been right with his predictions. This has made him a man that many people like to listen to when he speaks. Recently, he has spoken out again and how! Let me quote a part of his recent message:

► “Gold is going to and beyond $3500 based entirely on this initiative certain to become completed as a reality. It is already happening right in front of your eyes, but the world is still blind to it.

This is why gold will rise to $3500 and beyond, but never do a 1980 fall again. This is why silver is a great trading vehicle, but not a great long term holding. This is why I have invested $32,000,000 in my own approach towards gold.

This is why I sold ALL of my personal material treasures to make this investment when only I would do it. This is why I took on large debt to accomplish my plan.

This was the basis for my career interview by Forbes in Dec 2000.

No government fund, no gold bank, and no long cycle analyst can stop the progression of gold. The capitalization of the forces behind gold will overcome all these other bearish considerations. I say this because I know this, not because I think this.

I knew gold’s first most important number was $1650 11 years ahead of time. I did not think it. I am telling you now because I know it that gold will go to and beyond $3500. It will be gold that saves a financially collapsing world of debt.” ◄

I am pretty sure that some of you will recognize the above as a typical gold comment coming from the USA, but like I said, Jim Sinclair is not just a typical USA commentator. He knows what he is talking about and he is not afraid to tell us about his views. I was most impressed when I attended one of his speeches in the past and I have been alert on what he said ever since.

One of the most fascinating part of all the things I do to make up my mind about where gold is and where gold may go, is reading the many reports and comments from other gold watchers and talking and listening to them whenever I meet them at international mining investment events. I can tell you, it is not easy to distillate an own opinion and view out of the big melting pot of all the comments of others. They are so different all together and ranging from the most negative (yes, I do listen to them too…) to the most positive in the interesting arena of the bears and the bulls.

As one of my regular followers, you do know that I have been on the positive side of gold. In fact, all the way since the long term bull market became visible (for the early recognizers, that is…) in 2001. It even made me come back to the business after I had spent 10 years in a self-chosen retirement from the metals and the mines, because they obviously were in a longer than expected period of a downward cycle, best illustrated by prices like under $300 for gold, around $5 for silver and $0.60 for copper. And, like I wrote in my December and January issues of GOLDVIEW, I am still on the side of the ones that see higher prices for gold, silver and some other metals coming over the next few years.

I will not repeat myself about the factors that in my opinion justify the expectations for higher prices and reiterate that the current prices are already a very sound basis for the mining industry to achieve very satisfactory production and earnings results. But I thought that quoting Jim Sinclair here should give you a good impression of what a man like that expects for the future.

Not surprisingly, there is a distinct difference in opinions, views, expectations and the words that the different commentators use in telling us what they think. Just a few days before I read Jim’s report, I had read another worthwhile report. It was an interview that my friend Taki Tsaklanos had in his recent GoldSilverWorlds with Ronald Stoeferle, one of the best gold analysts we have here in Europe. Until very recently, Ronald was working for the Erste Group Bank AG in Vienna, Austria and in that capacity he has been writing about gold (and oil) since 2006. His annual Special Gold Report “In GOLD we TRUST” is one of the best gold reports available, not because it is positive about gold but because it is a very well researched and analysed, almost scientific study of everything that is related to gold. Last December, he left the Erste Bank to become partner in Incrementum AG in Baar/Zug, Switzerland with offices in Liechtenstein and Panama, where he will be managing their gold funds. I can only hope he will be continuing to write his annual gold survey……..

I strongly recommend to you to give your best attention to the interview which is integrally included in this issue –see pages 3-8– as it represents an excellent insight in what we can expect of gold and why. The interview also means a landmark for Taki and his GoldSilverWorlds, a website that since its inception in May 2012 has developed into a very welcome European source of international and first class information reports on gold. More about them at the end of the interview on page 8.

My decision to be willing to bring this quality interview to you in this issue is that the content fully supports my own views on the current situation of gold and what the future brings. The recent developments, with in front the shady agreeing of the Federal Reserve to return the part of the German gold that was asked for, was and is a point of no return for me. For me, it is clear: if the gold is indeed there in good order and shape, why does it take seven years to give it back? The only reason I can think of is that if the gold is there, the Fed is not free to release the gold, it must have other obligations against the gold. That would also explain the high volumes of paper gold that are traded and the regular selling actions that have been suppressing the gold price in the last few months. Against this background, plus my reasoning that gold is still cheap in relation to the adjusted high of $850, it is difficult for me to understand why gold is selling at today’s prices. Hence, my heading of this report: “How can you be bearish on gold?”

As I said, read the interview carefully and judge for yourself. this piece of information could turn out one of your best tools to define your thinking and opinion about gold and instrumental in taking your right decisions to benefit from what will be coming to us in the next few years. With the interview of Taki and Ronald as basis, it may also be easier to bridge the gap with the stronger language that international gold watchers Eric Sprott, James Turk, Doug Casey, John Embry, Jim Rickards and some others tend to use.

Some gold price forecasters become bearish but not gold analyst Ronald Stoeferle,

he is bullish and gives the key drivers why

GoldSilverWorlds’ Taki Tsaklanos interviews Ronald Stoeferle

In this interview with Taki Tsaklanos (◄) of Gold Silver Worlds, Ronald Stoeferle (►) explains in detail why lower gold price forecasts lack insights in the physical gold fundamentals. He is one of the top precious metals analysts worldwide and author of the well known reports “In Gold We Trust”. Stoeferle considers this article the most important one when it comes to gold fundamentals. It is a must read for everyone involved or interested in precious metals.

In this interview with Taki Tsaklanos (◄) of Gold Silver Worlds, Ronald Stoeferle (►) explains in detail why lower gold price forecasts lack insights in the physical gold fundamentals. He is one of the top precious metals analysts worldwide and author of the well known reports “In Gold We Trust”. Stoeferle considers this article the most important one when it comes to gold fundamentals. It is a must read for everyone involved or interested in precious metals.

The new year brings traditionally forecasts. Those are interesting data as they reveal the market sentiment. In general, analysts are revising their outlook for gold downward. Goldman Sachs lowered considerably their outlook in the light of an expected economic recovery. Deutsche Bank and HSBC reduced their gold price outlook, although they still expect a slightly higher price.

The new year brings traditionally forecasts. Those are interesting data as they reveal the market sentiment. In general, analysts are revising their outlook for gold downward. Goldman Sachs lowered considerably their outlook in the light of an expected economic recovery. Deutsche Bank and HSBC reduced their gold price outlook, although they still expect a slightly higher price.

A quote from one of the reports: “Global investment demand for gold has moderated considerably over the past 18 months, largely a function of the apparent success of central bankers in mitigating the risks associated with excessive financial leverage within the Western economic system,” […]“The strength in other more conventional assets, U.S. equities for example, as economic conditions appear to normalize has also resulted in less urgency for investors to buy unorthodox investment instruments such as gold.”

Gold Silver Worlds asked Ronald Stoeferle for his view on the lowered outlook. Stoeferle is a top precious metals analyst and author of the comprehensive series of gold reports “In Gold We Trust”. His high level view: “Gold analysts remain bearish, which is a reliable contrary indicator. I honestly would interpret that as a positive sign. Most of the major investment banks were bullish on gold a while ago. As a contrarian, that made me cautious. The fact that a lot of banks are turning bearish now is a good sign. The bottom must be in soon.” Stoeferle comes to the same conclusion by looking at other gold indicators, including the put/call ratio, COT reports, sentiment indicators and gold stocks. He points to the 2012 edition of his report, quoting the following:

The market opinion held by the analyst community is not exactly over-the-top. Normally, the consensus at the end of a trend should have substantially higher price targets; in the case of gold, however, no such irrational exuberance can be seen. The 24 gold analysts covered by Bloomberg show little signs of excessive optimism: the consensus estimate expects a falling gold price from 2014 onwards. The median price targets are USD 1,720 (in 2012), USD 1,835 (in 2013), USD 1,600 (in 2014) und USD 1,400 (in 2015). This is in stark contrast to the forward price, which signals a gold price of USD 1,650 for 2015. (page 106, July 2012)

The earnings revisions of the Gold Bugs index remain extremely negative. This means that at the moment more analysts revise their earnings estimates downwards than upwards. It highlights the primary analysts’ profound pessimism. 2008 was the last year we saw similarly sharp adjustments of earnings forecasts. By relating earnings revisions to the price development of the Gold Bugs index, we find that the timing of the greatest pessimism tends to provide investors with reliable signals to engage.” (page 94, July 2012)

Contrarian behaviour has proven to be successful in the financial markets. As an example in the stock market, Nomura Research Institute has analyzed forecasts at the beginning of each year for the German DAX index, for the last five years. They measured the bullish vs bearish expectations of analysts on selected German stocks. Interestingly, the most bearish forecasts resulted in the best performances.

However, a contrarian approach is only part of the answer. The gold market fundamentals reveal a much larger truth, which remains largely underexposed in Stoeferle’s view.

Driving fundamental forces: Asian physical gold demand

What the previous forecasts fail to see, is the exploding physical gold demand in Asia and the emerging markets, driven by solid economic fundamentals in those countries. The increasing welfare and the gradually rising propensity to save, i.e. the savings ratio, are the crucial factors. Recent statistics confirm this.

The Federation of Indian Exporters Organisations has said India exported gold jewellery to the tune of $12.12 billion in the first nine months of this fiscal, which was just 30.68% of the value of imported gold. Between April to December 2012, gold imports jumped 40.23% over $28.16 billion imported during the corresponding period of April to December 2011. [Mineweb]

Indians save roughly 30% of their income, as opposed Americans, who save 5%. Plus, Indians are getting richer all the time. Once a very poor country, the rich and middle classes now outnumber the poor in this nation of 1.2 billion. The country has the sixth-largest economy in the world. [LFB]

The net gold flow from Hong Kong to mainland China in November hit its second-highest level in 2012 after April. Hong Kong exported 90.763 tonnes of gold to mainland China in November, an increase of 91 percent on the month. Its gold imports from China rose 23 percent to 27.681 tonnes. The total net gold flow in the first eleven months of the year, at 462.75 tonnes, already exceeded last year’s total of 379.573 tonnes, Reuters calculations showed. [Mineweb]

The Iraqi dinar exchange rate is based on the amount of cash reserves, which include not only money but gold as well. Iraq’s gold holdings quadrupled to 31 tons, the first time something like this has happened in years. [BullionStreet]

Turkish gold exports rose to $12.7 billion in the first eleven months of 2012 compared to the $1.47 billion exported in the whole of the previous year, Economy Minister Zafer Caglayan told a briefing in Istanbul. Around half of the exports – $6.5 billion worth – went to Iran, while $4.2 billion went to the United Arab Emirates. Turkey exported just $54 million worth of gold to Iran in 2011. [Reuters]

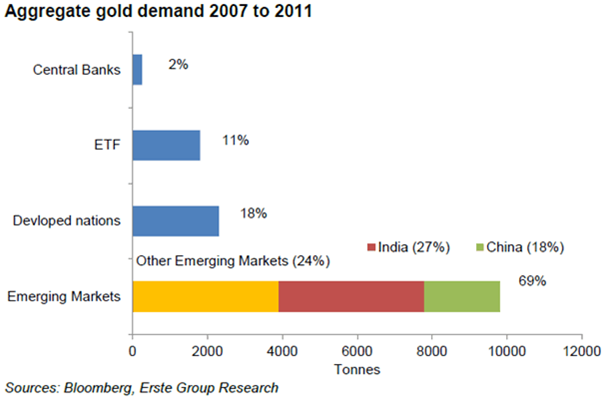

To put things into perspective, the following chart compares demand for physical gold out of Asia and emerging markets with other large purchasers. The strength in the gold market by physical demand out of Asia is unrightfully underexposed or even ignored by most commentators and analysts.

Dynamics in the Asian gold market are simply too strong

Let’s take the above facts and trends one step further by looking at the dynamics within the Asian gold market. All signs point to a continuation of the current trend. What makes Ronald Stoeferle convinced of this expectations, is the strength in the drivers in their economies.

(1) Physical demand is set continue its rise because gold is NOT expensive. China and India as the biggest (gold) markets experienced the same percentage increase in nominal GDP, wages and their currencies’ gold price. Locally, the gold prices did not change when expressed in terms of purchasing power, which is fundamentally different to the West. China has been the trendsetter in their reaction to financial repression (started in 2000). The Chinese population has chosen consciously and hugely for physical gold investments as a way to escape from financial repression.

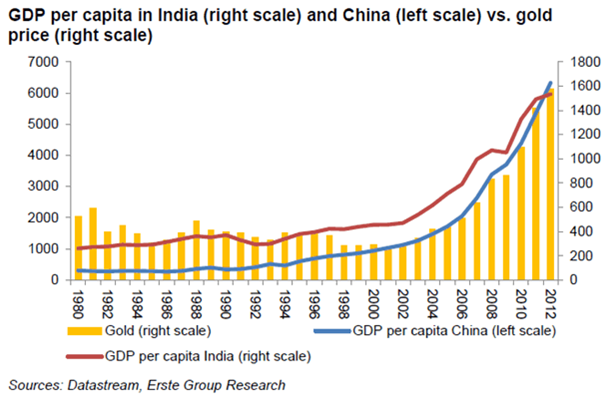

During the interview, Ronald Stoeferle quotes from its 2012 report (page 55): “In view of the fact that Asia already accounts for the majority of gold demand, the US data is of limited significance. Therefore the development of household income in China and India is a crucial factor for physical gold demand. In terms of the Indian rupee, the gold price has posted an average increase of 18% p.a. since 2001, while in Chinese yuan the growth rate was only slightly lower at 16%. Nominal income has been going up at the same rate and pace, which means that the gold price is basically unchanged in real terms for the Chinese and Indian population since 2000. The following chart illustrates the rapid development of Chinese (left scale) and Indian (right scale) GDP per capita.”

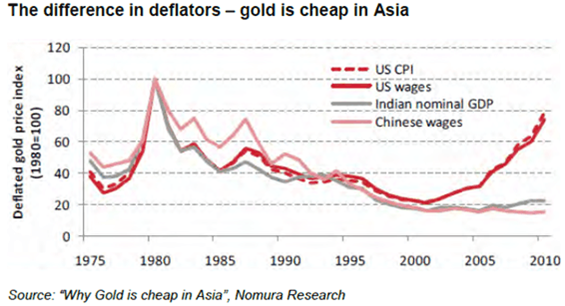

The officially reported inflation in Asia is often a rather vague depiction of reality. Therefore the gold price in terms of disposable income provides more insights. The next chart shows how the gold price in terms of purchasing power in China and India is currently 80% lower than in 1980. Gold is amazingly cheap for them.

(2) Governments stimulate people owning gold. The Indian gold mania has resulted in a decrease of the current account deficit (source) which was a reason for their government to attempt to increase duties on gold trades. The Indians succeeded in changing their policy makers from that idea, after several protests and strikes. Apart from that case, most Asian governments stimulate their citizens to own gold for their protection. It shows the trust from the Indian people to hold gold. China, which accounts for one sixth of world population, is a perfect example. The Turkish government is in the process of creating incentives for the population to deposit their private holdings with the banking system. As the global “run to debase” currencies becomes increasingly apparent, the Asian and emerging markets will undoubtedly continue to stimulate their citizens to hold gold.

(3) Alternative currency. Oil producing countries start dealing their oil with huge purchasers (think Russia, China, Brazil) in alternative currencies, resulting in a lower demand for dollars. A potential rush to the exit is coming from central banks that do not need US dollars anymore, which would lower the value of the dollar, make inflation and interest rates explode. We saw the first proof of this in 2012, where several Asian and BRIC countries began trading oil for gold.

Looking through the noise of the paper market

In addition to all the fundamental forces in Asia, Ronald Stoeferle looks to the day-to-day confusion primarily created in the paper futures market. That’s indeed where the short term price is set, but it’s nothing more than the short term price. “We are witnessing a huge disconnect between the short term price set in the paper market and the long term fundamentals primarily driven by Asian and emerging markets.” This is a concept that most people fail to understand, at least the fundamental impact on it on the gold market.

“Recently this became very blatant to the point I am considering this ridiculous” says Stoeferle. The Tokyo gold futures hit record high in the past days as the Yen slides on monetary easing announcements (source). That is normal market behaviour. Compare this with the five week waterfall decline in dollar gold after the QE4 announcement on December 12th, the most bullish event possible. Unusual large selling orders were placed in very thin trading (overnight) and suppressed the metals prices significantly and counter intuitively. The paper market behaviour can be very misleading to the point that these short term anomalies could be thought of being normal.

The Dow Theory says that the primary trend cannot be ignored. In the case of gold and silver, the long term fundamentals are so strong that manipulation is only possible on a short term basis. So take the opportunity to accumulate on every price dip.

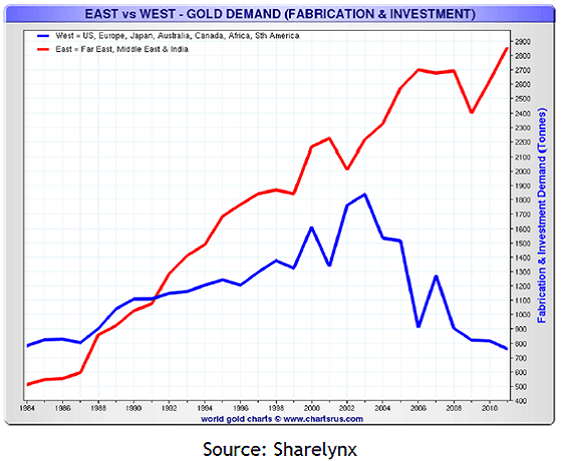

The West fails to understand that gold follows prosperous economies

On the most essential level, people need to understand what gold really stands for. Ronald Stoeferle refers to his report where he wrote on page 52 that gold has always abandoned regions of stagnating wealth, heading for prospering economies and rising savings volumes. In 1980 Europe and the US accounted for 70% of gold demand, since then this share has plummeted to below 20%. Chart courtesy Sharelynx

“Gold goes where the money is; it came to the United States between World Wars I and II, and it was transferred to Europe in the post-war period. It then went to Japan and to the Middle East in the 1970s and 1980s and currently it is going to China and also to India” (quote from James Steel, page 52 in the report).

Conclusion: Gold is often called the investment of doomsayers and chronic pessimists. However, this point of view fails to acknowledge the fact that China and India are the driving factors on the demand side. Real interest rates remain negative in both countries. On top of this the market is clearly underdeveloped with respect to its investment universe. Basically local investors are very limited when it comes to the use of their savings. Gold has been a time-tested store of value for centuries. The traditionally high affinity for gold and the rising net worth will support demand in the long run. Whoever expects incomes in China and India to continue rising and real interest rates to remain negative or low, will by default recognise gold as the beneficiary of these developments.

Impact of a Chinese recession

In closing, we talked about the impact of a Chinese recession on the gold fundamentals discussed in this article. Ronald Stoeferle believes that the fears for a hard landing did not play as some expected. In contrast, most indicators are picking up momentum currently. In his last oil report to premium subscribers he wrote the following:

In our view, the increasingly expansive Chinese monetary policy will cause Chinese oil consumption to regain its momentum in the short term. However, over the long term we continue to believe that an extensive market shakeout will take place. The earlier China allows the necessary break to happen, the less painful it will be. Chinese leadership is facing a difficult task. Due to the exceptionally high capital intensity of the Chinese economy (gross capital expenditures stand at 40% of GDP), future growth will be dependent on the propensity to consume of the Chinese people. To lift China’s domestic demand, the level of real wages would have to increase. However, the low current level of wages in China is the country’s most important competitive advantage which permitted the economy to grow at enormous rates over the past decade. Thus, it is evident that the Chinese government finds itself in a dilemma.

As opposed to the now generally accepted belief in the Chinese economic miracle, we take a more skeptical stance. Merely extrapolating the past into the future can eventually be disastrous. To this point the exorbitant stimuli have been sufficient to prevent an economic collapse. Substantial existing overcapacities have increased further. The governments share in the overall economic performance is gradually rising, state-funded infrastructure projects are responsible for the majority of this growth. In the long run, China will not be able to overturn the fundamental laws of economics and business activity.

This article is based on a Q&A with Ronald Stoeferle. He is born October 27, 1980 in Vienna, Austria, is a Chartered Market Technician (CMT) and a Certified Financial Technician (CFTe). During his studies in business administration and finance at the Vienna University of Economics and the University of Illinois at Urbana-Champaign, he worked for Raiffeisen Zentralbank (RZB) in the field of Fixed Income/Credit Investments. After graduating from University, Stoeferle joined Vienna based Erste Group Bank, covering International Equities, especially Asia. In 2006 he began writing reports on gold and gained media attention when he expected the price of gold to rise to USD 2,300/ounce when the current price was only at USD 500. His six benchmark reports called “In GOLD we TRUST” drew international coverage on CNBC, Bloomberg, the Wall Street Journal, Economist and the Financial Times. He was awarded “2nd most accurate gold analyst” by Bloomberg in 2011. He also writes reports on crude oil. The latest oil report by Stoeferle, entitled “Nothing to Spare” was published earlier this year. Stoeferle is managing two gold mining funds and one fund with silver mining equities. As of December 2012, Stoeferle has left Erste Group in order to become partner of Liechtenstein based Incrementum AG.

Taki Tsaklanos is the owner and editor of GoldSilverWorlds, website with quality information on gold, including fundamental information on ‘Understanding Gold’ and “A Starters Guide”, actual information with “Prices & Charts” and directive information for investors that want to buy gold like “Best Bullion Services” and “Own Bullion in Switzerland”. The website was introduced in May 2012 and has built an impressive following since then, primarily as a result of the flow of Taki’s personal selection of the most insightful articles across all domains on monetary, economic, financial, investing aspects of precious metals.

Taki Tsaklanos has his roots in online business and digital marketing, working for companies like Sony Europe and Vodafone Netherlands. He studied Economics at the University Hasselt and received a Masters Degree from the Université de Liège (both in Belgium). His interest in precious metals was sparked when he started to understand that the bubble economy is driven by government intervention.

The desire to share his observations and guide other people to face the more than difficult times that he is foreseeing to happen, led to starting GoldSilverWorlds.

If you really have read the above interview, you deserve my congratulations. Because you should be a lot wiser now, Ronald Stoeferle has the ability to explain his thinking in such a clear manner that reading about gold is no longer work, it is a pleasure because you sense that you are learning. And my compliments to Taki.

Latest developments supporting companies

ARGONAUT GOLD (TSX:AR) had record gold production in Q4 of 25,805 ounces from the El Castillo Mine in Durango and 6,195 ounces plus 47,890 ounces silver from the La Colorada Mine in Hermosillo, both in Mexico. This brought full year 2012 production to a total of 108,081 ounces of gold. In the meantime, progress is being made at its advanced exploration stage San Antonio project in Mexico and the recently acquired Magino project in Ontario, Canada. www.argonautgold.com

ASTUR GOLD (TSXV:AST) made considerable progress at the Salave mine in Asturias, northern Spain. By changing its plans into producing a high grade flotation concentrate for shipment to a smelter, the use of cyanide was eliminated. A positive Declaration of Impact Assessment was received and 49 conditions have to be met. Last week, a LOI was signed to construct a 2200m long development decline. Astur Gold plans to move towards production as soon as possible. www.asturgold.com

AURCANA CORPORATION (TSXV:AUN) reported a record year to date with silver equivalent production of 2.5 million ounces, up 42% from 2011, at its La Negra mine in Mexico. The increase in production is expected to continue in 2013 with an expansion in the mill capacity at La Negra and production ramp up at the Shafter mine in Texas, USA. Aurcana is making good progress in its pursuit to become a senior silver producer in the next few years.

AVINO SILVER & GOLD MINES (TSXV, NYSE MKT: ASM) continues underground development at its San Gonzalo mine in Durango, Mexico. Samples that are analysed for silver, gold, copper, lead and zinc at the company lab on site, have returned very encouraging results including 34 to 1380g/t silver and 0.19 to 3.45g/t gold over width from 1.26 to 2.22m NW of the old shaft and 13 to 1366g/t silver and 0.09 to 11.32g/t gold over 4.33 to 30.72m SE of the old shaft.

AVRUPA MINERALS (TSXV:AVU) continues its exploration programs in Portugal, Kosovo and Germany and expanded its property base in Portugal. It acquired three new exploration licenses, the Candedo and Sabroso, located in the northern belt of tungsten and gold mineralization and the Sines in the southern Pyrite Belt. The eastern boundary of the Sines is just 6km west of the Alvalade JV, operated by Avrupa and funded by Antofagasta Minerals SA.

BRALORNE GOLD MINES (TSXV:BPM) is continuing its work to reissue its news release announcing the Preliminary Economic Assessment on the Bralorne gold mine project in BC, Canada. The company has been instructed to retract all the results of the economic analysis of the “Postulated Case of Increasing Operations to 250 tpd”. The company was further instructed to comply with disclosure regulations and state that the PEA is based on mineral resources and not reserves.

CANASIL RESOURCES (TSXV:CLZ) received results from a Phase 2 drill program, recently completed by JV partner MAG Silver (TSX:MAG, NYSE-A:MVG) at its Esperanza silver-lead-zinc project in Durango and Zacatecas States in Mexico. The best intercept returned 4.93m of 0.19g/t gold, 104.2g/t silver, 2.57% lead and 7.88% zinc. All the results are currently being reviewed to define plans for future exploration programs on the project.

CORAL GOLD RESOURCES (TSXV:CLH) is still awaiting the response from the Bureau of Land Management to Coral’s submitted Environmental Assessment for its Robertson property in Crescent Valley, Nevada, USA. Upon receipt, Coral will then submit its application for a blanket permit to drill up to 500 holes. The first 60 holes will be part of the pre-feasibility study.

CUORO RESOURCES (TSXV:CUA) continues to develop the high-grade copper potential of its Santa Elena project in Colombia and has refocused its exploration program to expand on the high-grade drill results achieved so far. To date, approximately 23,500m of drilling has been completed and two lenses have been discovered. These lenses have the potential to be part of a much larger VMS system with several deposits.

EXPLOR RESOURCES (TSXV:EXS) has started drill programs on two of its projects in Ontario, Canada. On the Timmins Porcupine West property, a 10,000m drilling program is designed to test and to expand the known near surface gold mineralization to determine the open pit resource potential. At its Kidd Township property, a 3,000m diamond drill program has started, testing an 800x300m area that has not yet been drill tested.

GLOBAL MINERALS (TSXV:CTG) announced the initial results from its on-going underground drill program at its Strieborná silver project in Slovakia, designed to define and expand resources in the upper portion of the mineral deposit in areas where early mine development is planned. The first 8 holes, drilled about 180m below surface, retur ned between 28.3g/t and 1,420g/t in intervals from 0.45 to 7.65m. An updated resource estimate is planned for Q3 of this year.

GREAT PANTHER SILVER (TSX:GPR, NYSE MKT:GPL) reported Q4 and annual 2012 production figures from its two fully-owned silver mining operations, the Guanajuato and Topia in Mexico. Metal production for 2012 increased by 8% to 2.37 million silver equivalent ounces, silver production by 4% to 1.56 million ounces and gold by 36% TO 10,923 ounces. The strong Q4 finished the year with several quarterly and annual production records at both operations.

LOMIKO METALS (TSXV:LMR) was written up up by Christopher Skidmore’s “Beat the Market” investment newsletter. The report extensively elaborates at the drill results at the Quatre Miles East flake graphite property and describes Lomiko as “the cheapest graphite stock with confirmed mining potential”. Christopher likes the Quatre Mile deposit for three major reasons: higher grade, closer to surface and mineralized zones are wider. www.lomiko.com

NEW DAWN MINING (TSX:ND) reported gold production of 37,623 ounces in fiscal 2012 (ended Sep 30), revenues of $61.9 million and eps of $0.05 from its mining operations in Zimbabwe. These results compare favourably with the previous fiscal year, reflecting the addition of the Central African Gold mining assets in 2010. Judging from the production run in Q4, the company may be looking forward to a 45,000-50,000 ounces production level in the 2013 fiscal year.

ORVANA MINERALS (TSX:ORV) reported highlights from its first full year of commercial production at the EVBC mine in northern Spain and nine months of commercial production at the UMZ mine in Bolivia. Total production came to 55,929 ounces of gold, 15.4 million pounds of copper, 716,280 ounces of silver and 636,126 pounds of lead. Orvana’s short-term objective is to optimize operations at the two mines and to further advance the Copperwood Project in Michigan, USA.

PARAMOUNT GOLD & SILVER (TSX:PZG) announced that new core drilling on its 100%-owned Sleeper Gold project in Nevada, USA, is expanding mineralization in the East and South parts of the existing resource. Recent drill results included up to 48.8m of 0.45g/t gold and are likely to increase the in-pit resource and the already robust economics of the PEA, announced in September 2012, predicting a 17 year operation with estimated average gold production of 172,000 ounces. www.paramountgold.com

SCORPIO GOLD (TSXV:SGN) reported its preliminary operating results for Q4 at its 70%-owned Mineral Ridge project in Nevada, USA, representing the strongest quarterly performance to date. In its first year of commercial production, a total of 31,852 ounces of gold was produced. As part of its aggressive growth strategy, both internally and by acquisition, Scorpio acquired the Goldwedge gold property and milling facility and the Pinon gold property, also in Nevada.

SILVERCREST MINES (TSXV:SVL, NYSE MKT:SVLC) reported remarkable 2012 production results from its first full year of commercial production at the Santa Elena mine in Sonora, Mexico. 579,609 ounces of silver were produced, 33% more than estimated, 33,004 ounces of gold, together coming to 2.37 million ounces of silver equivalent. Management looks forward to another exciting year and has expansion plans to double metal production in 2014.

TEMBO GOLD (TSXV:TEM) released results from the first of a planned series of close-spaced drilling at the Ngula 1 target at its Tembo Gold project in the Lake Victoria goldfield of Tanzania, including 4.73g/t over 23m. This follows the results of the first deep hole at this target, which strongly support Tembo’s geological model that mineralization grades will improve with depth, as was the case at the adjacent Bulyanhulu mine of African Barrick Gold.

TIMMINS GOLD (NYSE MKT:TGD, TSX:TMM) reported record production of 94,444 ounces of gold for 2012 and also 56,252 ounces of silver. The Q4 results contributed substantially to the total results, reflecting the success of management’s objective to implement on-going process improvements. In particular, the improved crushing capacity led to a record production month of 9,349 ounces during December. Production for 2013 is forecast between 125,000 and 130,000 ounces.

My overall comment on these latest developments at the Supporting Companies and their projects is that they are confirming that the outlook for the industry is generally quite promising as I have been stating several times in my previous issues. Other than most current share prices of mining and exploration companies may suggest, there are many companies that are making excellent progress. One good measurement of that is to look at the results as they were reported by the emerging producers such as Argonaut Gold, Aurcana, Great Panther, Orvana, Scorpio Gold, SilverCrest and Timmins Gold. They finished 2012 with very satisfactory production and earnings figures and it was remarkable how strong their Q4 results were. A very good way to begin the new year and they are all very confident about the prospects for 2013. I feel pretty sure that these companies will not only sustain their recent developments this year but that they will continue to surprise us. With results like they have and will have, their shares should be among the top performers.

Avino, Bralorne and New Dawn Mining are expected to make a considerable jump onto a stable and growing production performance. They have to get even with some circumstantial factors but if and when they succeed in improving those, they will be joining the group of emerging producers this year.

Right next in line in phase of development come Paramount Gold & Silver, Astur Gold and Global Minerals. All three are working to bring former producers back into production. That is a discipline with its own specific requirement for expertise. But all three have proven to have what it takes to get production back on the track in the foreseeable future. More intensive and skilful work needs to be done but if the results will be in the same range of quality as the results obtained so far, there will be definitely light, or rather gold and silver at the end of the tunnel for them.

As to the exploration companies, I can say that I am very glad with this group. I think they are good representatives of what exploration companies should be like and develop into. Each is having their own characteristics and special attractive features, but they all are companies with substance, real projects with already made discoveries that are waiting to be further exposed. You can believe me when I say that not all exploration companies that are doing their best to win the sympathy and support of the investment public, can say the same.

This said, I am looking ahead at interesting times. Not only as to the results of the companies that I write about, but also as to the things that I have planned for this year; in my January issue, I have outlined some of those plans. Yet, the markets, those of the metals and the mining shares, will eventually be the decisive judge on how “our” industry is doing and will be rewarded. It used to be that the markets were anticipating on the results to come, but these days it looks like the results are waiting for the markets to follow them. Which provides an opportunity to investors to anticipate on what is coming and do well and be rewarded in better times.

Henk J. Krasenberg

[hr]

European Gold Centre

European Gold Centre analyzes and comments on gold, other metals & minerals and international mining and exploration companies in perspective to the rapidly changing world of economics, finance and investments. Through its publications, The Centre informs international investors, both institutional and private, primarily in Europe but also worldwide, who have an interest in natural resources and investing in resource companies.

The Centre also provides assistance to international mining and exploration companies in building and expanding their European investor following and shareholdership.

Henk J. Krasenberg

After my professional career in security analysis, investment advisory, porfolio management and investment banking, I made the decision to concentrate on and specialize in the world of metals, minerals and mining finance. From 1983 to 1992, I have been writing and consulting about gold, other metals and minerals and resource companies.

The depressed metal markets of the early 1990’s led me to a temporary shift. I pursued one of my other hobbies and started an art gallery in contemporary abstracts, awaiting a new cycle in metals and mining. That started to come in the early 2000’s and I returned to metals and mining in 2002 with the European Gold Centre.

With my GOLDVIEW reports, I have built an extensive institutional investor following in Europe and more of a private investor following in the rest of the world. In 2007, I introduced my MINING IN AFRICA publication, to be followed by MINING IN EUROPE in 2010 and MINING IN MEXICO in 2012.

For more information: www.europeangoldcentre.com

Det råder speciella förutsättningar på elmarknaden just nu och allt styrs till största delen av vädret. Sol och bitvis god vindkraftsproduktion under maj, i kombination med svag hydrologi och begränsad kärnkraft har lett till stora svängningar i elpriset. Juni inleds liknande och idag tangerar elpriserna nivåer från krisåret 2022. Dock förväntas elpriserna gå ner då kärnkraften ökar.

Juni börjar med höga elpriser och orsakerna är brist på vindkraft, torra väderprognoser och mindre kärnkraft. Prisuppgången i maj var särskilt tydlig i norra Sverige, elområde 1 och 2, och ligger just nu nära en krona per kWh. I elområdena 3 och 4, södra Sverige, blev månadsmedelspotpriset för maj 35–40 procent högre jämfört med april men har rusat idag till nivåer på mellan 130–160 öre/kWh.

– Dagens höga priser visar tydligt på hur snabbt förändrade väderprognoser får genomslag på elpriset. Sommarens väder påverkar även priserna inför hösten och vintern. Ska det bli mer stabila elpriser behövs ett typiskt svenskt sommarväder, dvs. en blandning av regn, vind och sol, snarare än extremvärme och högtryck. Särskilt viktig är nederbörden i Norge och norra Sverige där vattenkraften dominerar, säger Jonas Stenbeck, privatkundschef på Vattenfall Försäljning.

Den hydrologiska balansen, dvs. det sammanlagda vatteninnehållet i snö, mark och magasin, är väldigt ansträngt efter en snöfattig vinter. Det stora underskottet håller i sig och är starkt beroende av mer nederbörd i närtid. På grund av pågående revisioner, bland annat Ringhals 3 och Forsmark 2, är elproduktionen från svensk kärnkraft begränsad just nu. Oskarshamn 3 har planerad återstart den 10 juni och Ringhals 4, som för närvarande producerar med halv effekt, går upp till full effekt den 12 juni. Det innebär att den installerade effekten då kommer att stiga från 40 till 60 procent i Sverige.

Det geopolitiska läget är fortsatt ett orosmoment men ryktet om ett fredsförslag har lugnat marknaden något. Gas- och oljepriserna fortsätter att falla och de stigande temperaturerna på kontinenten och den stora andelen solkraft kan ha en stabiliserande effekt.

| Medelspotpris | Elområde 1, Norra Sverige | Elområde 2, Norra Mellansverige | Elområde 3, Södra Mellansverige | Elområde 4, Södra Sverige |

| Maj 2026 | 46,36 öre/kWh | 48,95 öre/kWh | 70,86 öre/kWh | 87,05 öre/kWh |

| Maj 2025 | 14,09 öre/kWh | 15,09 öre/kWh | 42,94 öre/kWh | 60,01 öre/kWh |

Snabba väderomslag har präglat elmarknaden i april, med både prisfall och pristoppar som följd. Samtidigt får solkraften allt större påverkan och pressar ner elpriserna, särskilt i södra Sverige.

Månadsmedelpriset för april på den nordiska elbörsen Nord Pool utan påslag och exklusive moms blev 58,66 öre/kWh i elområde 3, södra Mellansverige, och 22,75 öre/kWh i elområde 1, norra Sverige. På kontinenten syns den så kallade ankkurvan tydligt.

– Nu är solen helt klart på gång. I Tyskland har solen under april producerat nästan 2 TWh mer än ifjol vilket även gynnar oss i Sverige. Ankkurvefenomenet innebär att elpriset är lågt mitt på dagen och stiger raskt mot kvällen. Under perioder med soligt och varmare vårväder är solen ett välkommet inslag här hemma och det påverkar elpriserna nedåt. Den ökar produktionen och minskar konsumtionen, säger Jonas Stenbeck, privatkundschef på Vattenfall Försäljning.

De årliga, planerade underhållsarbetena på kärnkraftverken pågår, vilket innebär att den tillgängliga kapaciteten just nu är cirka 60 procent. Vinden var varierande under april, med snabba skiften mellan stilla och blåsiga perioder, vilket märktes på elpriset.

Den hydrologiska balansen i Norden, alltså det sammanlagda vatteninnehållet i snö, mark och magasin, är svag med betydande underskott i södra Norge. Men magasinsnivåerna i Sverige ligger kring normala nivåer för årstiden och har börjat fyllas på.

– Dock förväntas årets vårflod att, givet dagens förutsättningar, bli lägre än normalt då snötäcket är avsevärt mindre än vanliga nivåer. Vädret kommer avgöra hur väl vårfloden fyller magasinen inför sommaren, säger Jonas Stenbeck.

De höga gaspriserna har fallit något, samtidigt som stigande temperaturer på kontinenten och den stora andelen solkraft haft en stabiliserande effekt. Det geopolitiska läget är dock fortsatt ett orosmoment.

– Det vi sett är att marknaden är väldigt nyhetsdriven. Beroende av vad som rapporteras så reagerar marknaden direkt. Det gör att vi befinner oss i en väldigt speciell situation eftersom denna osäkerhet skapar svängiga och oförutsägbara bränslepriser, vilket i slutändan påverkar elpriset. Jag förstår att många känner en oro men i och med att det blir varmare så kommer man inte att behöva lika mycket el, vilket ger en lägre elkostnad, säger Jonas Stenbeck.

| Medelspotpris | April 2025 | April 2026 |

| Elområde 1, Norra Sverige | 14,39 öre/kWh | 26,09 öre/kWh |

| Elområde 2, Norra Mellansverige | 14,21 öre/kWh | 26,85 öre/kWh |

| Elområde 3, Södra Mellansverige | 37,61 öre/kWh | 56,08 öre/kWh |

| Elområde 4, Södra Sverige | 58,35 öre/kWh | 66,55 öre/kWh |

*Ankkurva: Ankkurvan beskriver hur elproduktionen från förnybara energikällor, som solenergi, påverkar elnätet och elanvändningen över en dag. Kurvan har fått sitt namn eftersom grafen under en dag liknar profilen av en anka.

Råvaran olja handlas fortsatt över 100 USD per fat och det är något stökigt med prissättningen. Michel Gubel ger sin syn på läget för oljan, att priskurvan kan vara i contango och backwardation, samt vad som kan hända med olja på längre sikt.

Sommarväder skapar prisrally på elbörsen

Oil product price pain is set to rise as the Strait of Hormuz stays closed into summer

Solkraften pressar elpriserna dagtid

Michel Gubel ger sin syn på oljemarknaden