Analys

Crude oil comment: Big money and USD 80/b

Brent crude was already ripe for a correction lower. Brent closed down 0.8% yesterday at USD 80.15/b and traded as low as USD 79.42/b intraday. Brent is trading down another 0.4% this morning to USD 79.9/b. It is hard to track and assign exactly what from Donald Trump’s announcements yesterday which was impacting crude oil prices in different ways. But crude oil was already ripe for a correction lower as it recently went into strongly overbought territory. So, Brent would probably have sold off a bit anyhow, even without any announcements from Trump.

Extending the life of US oil and gas. The Brent 5-year contract rose yesterday. For sure he wants to promote and extend the life of US oil and gas. Longer dated Brent prices (5-yr) rose 0.5% yesterday to USD 68.77/b. Maybe in a reflection of that.

Lifting the freeze on LNG exports will be good for US gas producers and global consumers in five years. Trumps lifting of Bidens freeze on LNG exports will is positive for global nat gas consumers which may get lower prices, but negative for US consumers which likely will get higher prices. Best of all is it for US nat gas producers which will get an outlet for their nat gas into the international market. They will produce more and get higher prices both domestically and internationally. But it takes time to build LNG export terminals. So immediate effect on markets and prices. But one thing that is clear is that Donald Trump by this takes the side of rich US nat gas producers and not the average man in the street in the US which will have to pay higher nat gas prices down the road.

Removing restrictions on federal land and see will likely not boost US production. But maybe extend it. Donald Trump will likely remove restrictions on leasing of federal land and waters for the purpose of oil and gas exploration and production. But this process will likely take time and then yet more time before new production appears. It will likely extend the life of the US fossil industry rather than to boost production to higher levels. If that is, if the president coming after Trump doesn’t reverse it again.

Donald to fill US Strategic Reserves to the brim. But they are already filled at maximum rate. Donald Trump wants to refill the US Strategic Petroleum Reserves (SPR) to the brim. Currently standing at 394 mb. With a capacity of around 700 mb it means that another 300 mb can be stored there. But Donald Trump’s order will likely not change anything. Biden was already refilling US SPR at its maximum rate of 3 mb per month. The discharge rate from SPR is probably around 1 mb/d, but the refilling capacity rate is much, much lower. One probably never imagined that refilling quickly would be important. The solution would be to rework the pumping stations going to the SPR facilities.

New sanctions towards Iran and Venezuela in the cards but will likely be part of a total strategic puzzle involving Russia/Ukraine war, Biden-sanctions on Russia and new sanctions on Iran and Venezuela. All balanced to end the Russia/Ukraine war, improve the relationship between Putin and Trump, keep the oil price from rallying while making room for more oil exports of US crude oil into the global market. Though Donald Trump looks set to also want to stay close to Muhammed Bin Salman of Saudi Arabia. So, allowing more oil to flow from both Russia, Saudi Arabia and the US while also keeping the oil price above USD 80/b should make everyone happy including the US oil and gas sector. Though Iran and Venezuela may not be so happy. Trumps key advisers are looking at a big sanctions package to hit Iran’s oil industry which could possibly curb Iranian oil exports by up to 1 mb/d. Donald Trump is also out saying that the US probably will stop buying oil from Venezuela. Though US refineries really do want that type of oil to run their refineries.

Big money and USD 80/b or higher. Donald Trump holding hands with US oil industry, Putin and Muhammed Bin Salman. They all want to produce more if possible. But more importantly they all want an oil price of USD 80/b or higher. Big money and politics will probably talk louder than the average man in the street who want a lower oil price. And when it comes to it, a price of USD 80/b isn’t much to complain about given that the 20-year average nominal Brent crude oil price is USD 77/b, and the inflation adjusted price is USD 102/b.

Analys

Higher on confidence OPEC+ won’t lift production. Taking little notice of Trump sledgehammer to global free trade

Ticking higher on confidence that OPEC+ won’t lift production in April. Brent crude gained 0.8% yesterday with a close of USD 75.84/b. This morning it is gaining another 0.7% to USD 76.3/b. Signals the latest days that OPEC+ is considering a delay to its planned production increase in April and the following months is probably the most important reason. But we would be surprised if that wasn’t fully anticipated and discounted in the oil price already. News this morning that there are ”green shots” to be seen in the Chinese property market is macro-positive, but industrial metals are not moving. It is naturally to be concerned about the global economic outlook as Donald Trump takes a sledgehammer smashing away at the existing global ”free-trade structure” with signals of 25% tariffs on car imports to the US. The oil price takes little notice of this today though.

Kazakhstan CPC crude flows possibly down 30% for months due to damaged CPC pumping station. The Brent price has been in steady decline since mid-January but seems to have found some support around the USD 74/b mark, the low point from Thursday last week. Technically it is inching above the 50dma today with 200dma above at USD 77.64/b. Oil flowing from Kazakhstan on the CPC line may be reduced by 30% until the Krapotkinskaya oil pumping station is repaired. That may take several months says Russia’s Novak. This probably helps to add support to Brent crude today.

The Brent crude 1mth contract with 50dma, 100dma, 200dma and RSI. Nothing on the horizon at the moment which makes us expect any imminent break above USD 80/b

Analys

Brent looks to US production costs. Taking little notice of Trump-tariffs and Ukraine peace-dealing

Brent crude hardly moved last week taking little notice of neither tariffs nor Ukraine peace-dealing. Brent crude traded up 0.1% last week to USD 74.74/b trading in a range of USD 74.06 – 77.29/b. Fluctuations through the week may have been driven by varying signals from the Putin-Trump peace negotiations over Ukraine. This morning Brent is up 0.4% to USD 75/b. Gain is possibly due to news that a Caspian pipeline pumping station has been hit by a drone with reduced CPC (Kazaksthan) oil flows as a result.

Brent front-month contract rock solid around the USD 75/b mark. The Brent crude price level of around USD 75/b hardly moved an inch week on week. Fear that Trump-tariffs will hurt global economic growth and oil demand growth. No impact. Possibility that a peace deal over Ukraine will lead to increased exports of oil from Russia. No impact. On the latter. Russian oil production at 9 mb/band versus a more normal 10 mb/d and comparably lower exports is NOT due to sanctions by the EU and the US. Russia is part of OPEC+, and its production is aligned with Saudi Arabia at 9 mb/d and the agreement Russia has made with Saudi Arabia and OPEC+ under the Declaration of Cooperation (DoC). Though exports of Russian crude and products has been hampered a little by the new Biden-sanctions on 10 January, but that effect is probably fading by the day as oil flows have a tendency to seep through the sanction barriers over time. A sharp decline in time-spreads is probably a sign of that.

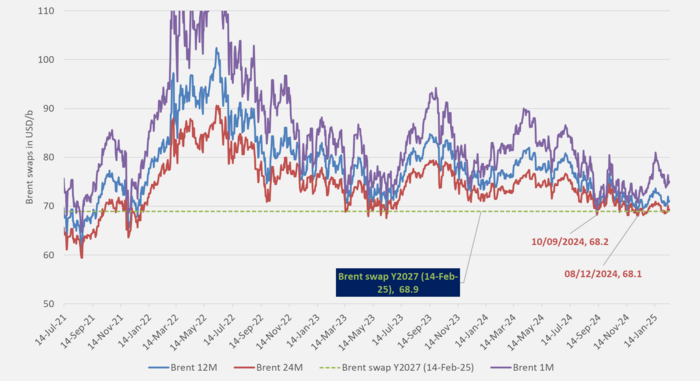

Longer-dated prices zoom in on US cost break-evens with 5yr WTI at USD 63/b and Brent at USD 68-b. Argus reported on Friday that a Kansas City Fed survey last month indicated an average of USD 62/b for average drilling and oil production in the US to be profitable. That is down from USD 64/b last year. In comparison the 5-year (60mth) WTI contract is trading at USD 62.8/b. Right at that level. The survey response also stated that an oil price of sub-USD 70/b won’t be enough over time for the US oil industry to make sufficient profits with decline capex over time with sub-USD 70/b prices. But for now, the WTI 5yr is trading at USD 62.8/b and the Brent crude 5-yr is trading at USD 67.7/b.

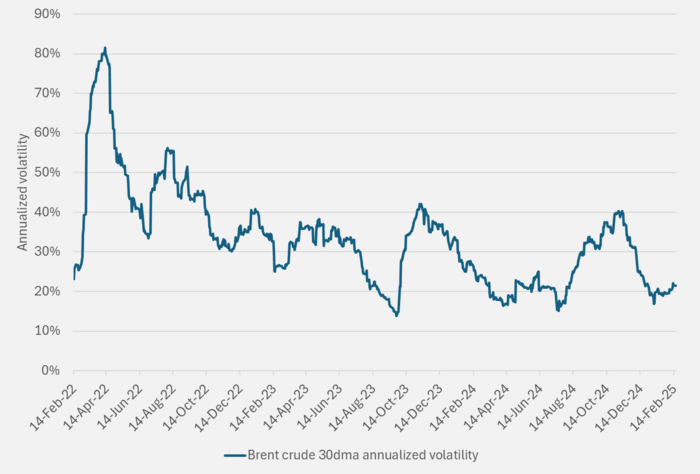

Volatility comes in waves. Brent crude 30dma annualized volatility.

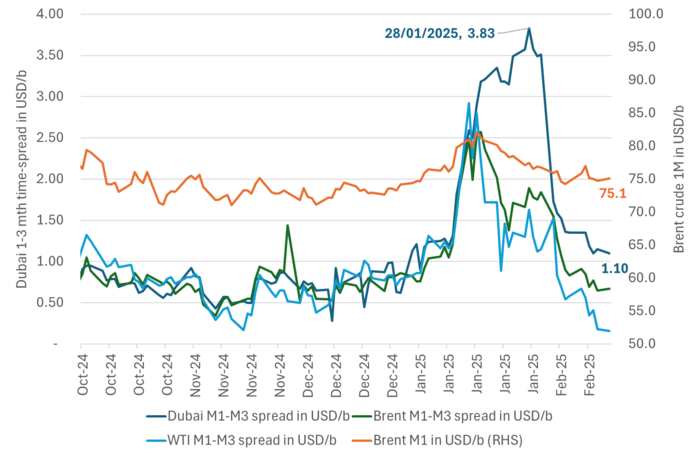

1 to 3 months’ time-spreads have fallen back sharply. Crude oil from Russia and Iran may be seeping through the 10 Jan Biden-sanctions.

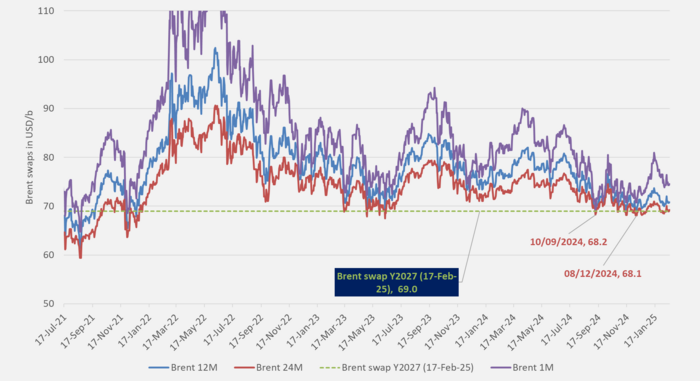

Brent crude 1M, 12M, 24M and Y2027 prices.

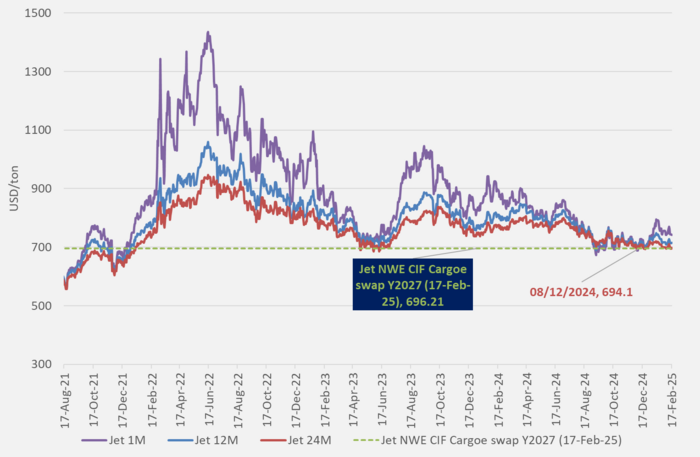

ARA Jet 1M, 12M, 24M and Y2027 prices.

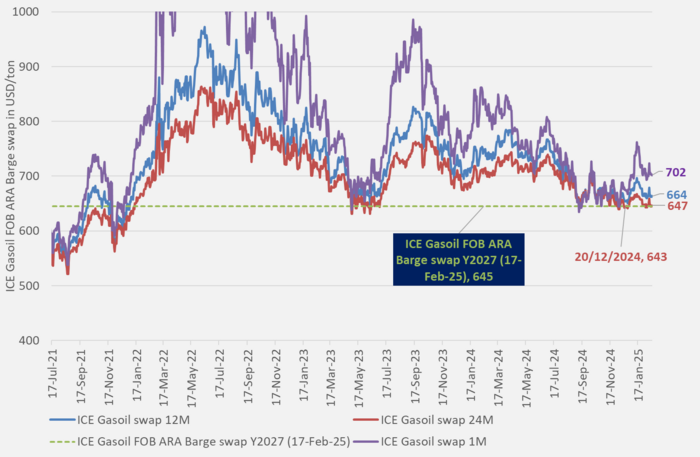

ICE Gasoil 1M, 12M, 24M and Y2027 prices.

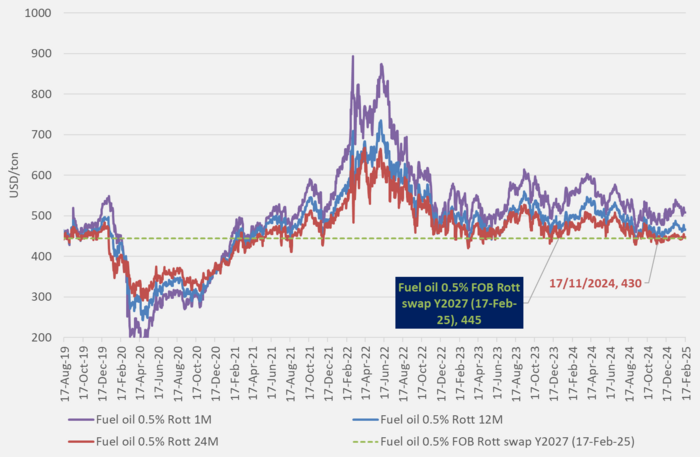

Rotterdam Fuel oil 0.5% 1M, 12M, 24M and Y2027 prices.

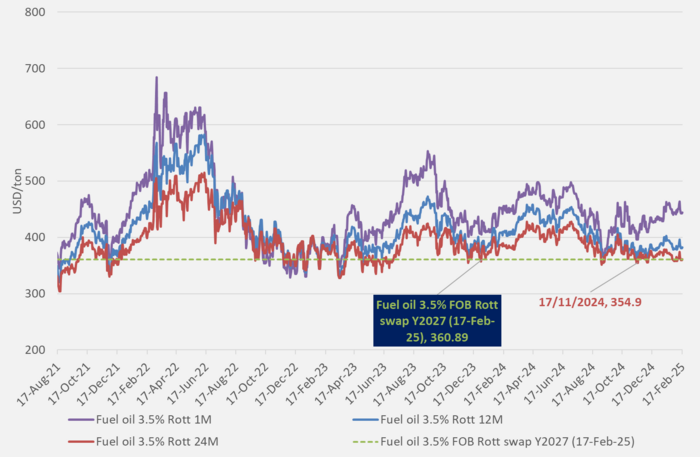

Rotterdam Fuel oil 3.5% 1M, 12M, 24M and Y2027 prices.

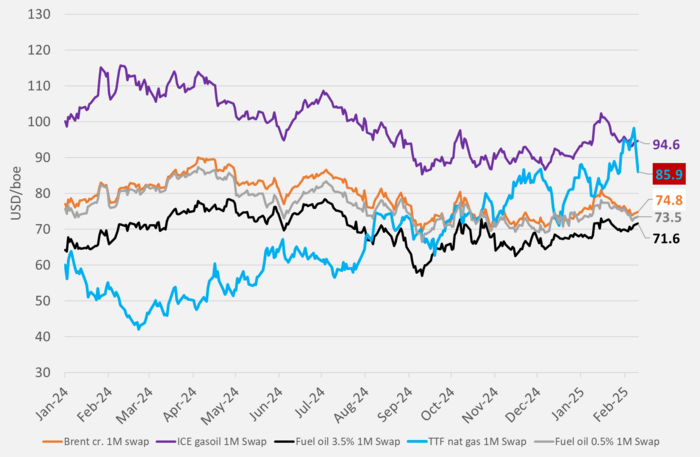

Ticking higher along with softer USD and gains in metals and equities. Brent traded down marginally (-0.2%) yesterday to USD 72.02/b following a 2.4% decline on Wednesday. This morning it is ticking up 0.5% to USD 75.4/b, well aligned with a 0.4% softer USD and solid gains in equities and industrial metals. Technically it is neither overbought nor oversold with RSI at 45. Though it is flirting with the 100dma also being below both the 50dma and the 200dma. So, no obvious strength either. The bullish tailwind from nat gas is fading a bit with TTF nat gas falling sharply to below the price of ICE Gasoil (”diesel”).

Longer-dated prices supported at USD 68/b. But looks like a process of fading strength. The longer-dated contracts for Brent keep trading down towards the high 60ies around USD 68/b but are rejected repeatedly. The pricing for these contracts looks like a process of fading strength. Just oozing closer to the USD 68/b level with smaller and smaller bounces each time. Very clear consumer buying interest for oil products when Brent crude prices move towards the USD 68-70/b level. This support level may thus to some degree come from the consumer side of the market. If oil consuming industry loses confidence in the economy, we might see the longer dated prices break below USD 68-70/b. But oil producers may also have limited interest in hedging downside risk at around the 68-mark. So, selling from that side of the market is probably also fading at that level. But also, sellers/producers may change if the global economy was to look shakier.

Microscopic changes in IEA forecast. OPEC(+) still needs to cut in 2025 to balance market. The IEA made only microscopic adjustments to its oil market balance yesterday. Adjusting production in OECD Europe and FSU production slightly lower resulting in call-on-OPEC going up by 0.2 mb/d versus the previous report. Call-on-OPEC is still set to decline from 27.1 mb/d in 2024 to 26.7 mb/d in 2025. A y-y decline of 0.4 mb/d implying that the group will have to cut production comparably in 2025. OPEC+ is of course planning to lift production by 120 kb/d/month from April onwards. Nope, says the IEA. It has to reduce supply instead.

Front-month and longer dated Brent crude oil prices in USD/b bouncing off the USD 68-70/b level.

European TTF front-month price trading sharply lower following signals that nat gas inventories in Europe may not need to mandatory fill to 90% by 1 November anyhow.

Eric Strand kommenterar vad som händer med guld och silver

Higher on confidence OPEC+ won’t lift production. Taking little notice of Trump sledgehammer to global free trade

Blykalla erhåller 17,5 miljoner euro från EU:s acceleratorprogram

Brent looks to US production costs. Taking little notice of Trump-tariffs and Ukraine peace-dealing

Christian Kopfer om guld, olja och stål

Belgien gör en u-sväng, går från att lägga ner kärnkraft till att bygga ny

Fondförvaltare köper aktier i kanadensiska guldproducenter när valutan faller

Brent testing the 200dma at USD 78.6/b with API indicating rising US oil inventories

Epiroc-aktien är ett bra sätt att få exponering mot gruv- och råvarusektorn

Crude oil comment: Big money and USD 80/b

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanBelgien gör en u-sväng, går från att lägga ner kärnkraft till att bygga ny

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFondförvaltare köper aktier i kanadensiska guldproducenter när valutan faller

-

Analys4 veckor sedan

Brent testing the 200dma at USD 78.6/b with API indicating rising US oil inventories

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanEpiroc-aktien är ett bra sätt att få exponering mot gruv- och råvarusektorn

-

Analys3 veckor sedan

Brent rebound is likely as Biden-sanctions are creating painful tightness

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanPrisskillnaden mellan råoljorna WCS och WTI vidgas med USA:s tariffkrig

-

Analys4 veckor sedan

Crude oil comment: Deferred contracts still at very favorable levels as latest rally concentrated at front-end

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVirke, råvaran som är Kanadas trumfkort mot USA