Analys

Brent crude marches on with accelerating strength coming from Mid-East time-spreads

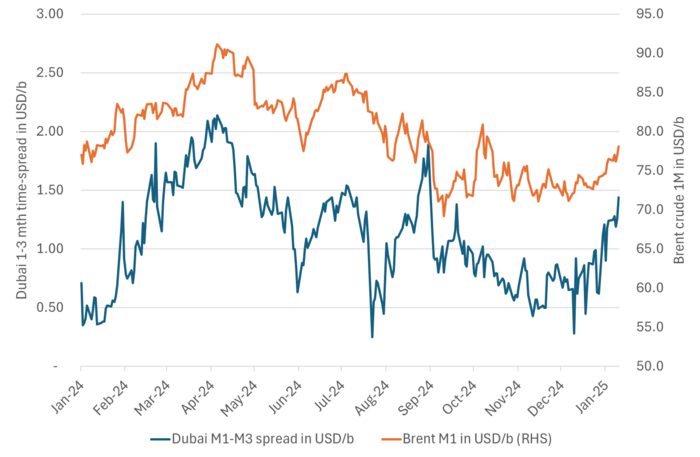

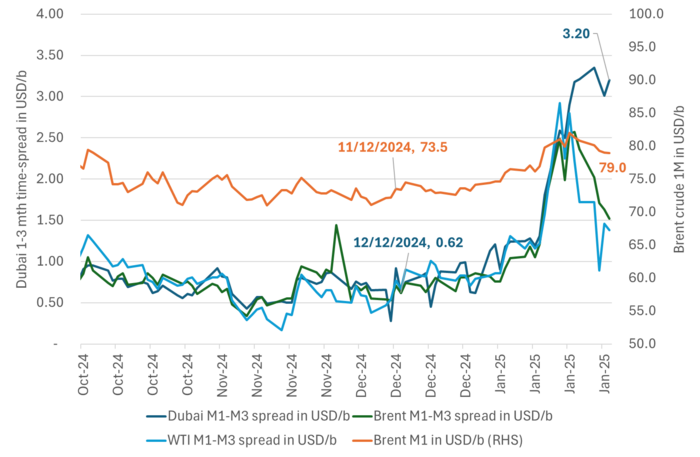

Fueled higher with strength seemingly coming from Mid-East benchmarks. Following a setback on Wednesday, Brent crude gained 1% yesterday with a close at USD 76.92/b. This morning it is jumping up another 1.5% to USD 78.1/b. Strength looks like it continues to come from the Middle East where the 1-3 Dubai time-spread this morning has moved to USD 1.44/b and its highest level since late August. The strength in this measure looks like it is accelerating rather than fading and if so, it will likely drive flat prices for all crude grades yet higher.

The ”missing barrels” in Q3-24. Current strength could be reality rather than just a flash in the pan. One of the issues discussed in November was the ”missing barrels”. The IEAs supply/demand balance for Q3 didn’t match the visible, and measured changes in oil inventories. IEA’s supply/demand balance implied an inventory draw of 0.38 m b/d in Q3-24 while the observed draw was 1.16 m b/d. The actual data was 0.78 m b/d tighter than IEA’s estimates. The supply/demand balance of IEA is to a large degree and Excel exercise with large uncertainties as it is fed with data with considerable lags and revisions. If inventory changes in Q3-24 was telling the true story of the global supply/demand balance, then 2025 could be revised significantly tighter without any other changes in the fundamentals than revision of data. The current strength in crude oil could thus be the real face of the supply/demand balance in the global oil market rather than just a temporary flash in the pan. Here is the Bloomberg story on the topic from Nov.

Looks set to break above the 200dma for first time since July. Prices in the 80is then in the cards. The technical picture is still on the verge of overbought with the RSI at 67.6 this morning and quite close to the 70 overbought level. But if further gains are coming gradually rather than rapidly, then this measure could stay below the 70-line. The 200dma is getting closer and closer. With its value today at USD 79/b it won’t take much to jump above. If so, it will be the first move above since July last year and quite a bullish feat and price levels above USD 80/b should then probably be in play.

Brent crude front-month in USD/b versus the Dubai 1-3 month time-spread. The Dubai measure of tightness is accelerating.

Brent crude front-month technical picture. Getting close to break above the 200dma for first time since July last year. But RSI is getting pretty close to ”overbought” territory.

Rebounding after yesterday’s drop but stays within recent bearish trend. Brent crude sold off 1.8% yesterday with a close of USD 77.08/b. It hit a low on the day of USD 76.3/b. This morning it is rebounding 0.8% to USD 77.7/b. That is still below the 200dma at USD 78.4/b and the downward trend which started 16 January still looks almost linear. A stronger rebound than what we see this morning is needed to break the downward trend.

Saudi won’t break with OPEC+ to head calls for more oil from Trump. OPEC+ will likely stick to its current production plan as it meets next week. The current plan is steady production in February and March and then a gradual, monthly increase of 120 kb/d/mth for 18 months starting in April. These planned increases will however highly likely be modified along the way just as we saw the group’s plans change last year. When they are modified the focus will be to maintain current prices as the primary goal with production growth coming second in line. There is very little chance that Saudi Arabia will unilaterally increase production and break the OPEC+ cooperation in response to recent calls from Trump. If it did, then the rest of OPEC+ would have no choice but to line up and produce more as well with the result that the oil price would totally collapse.

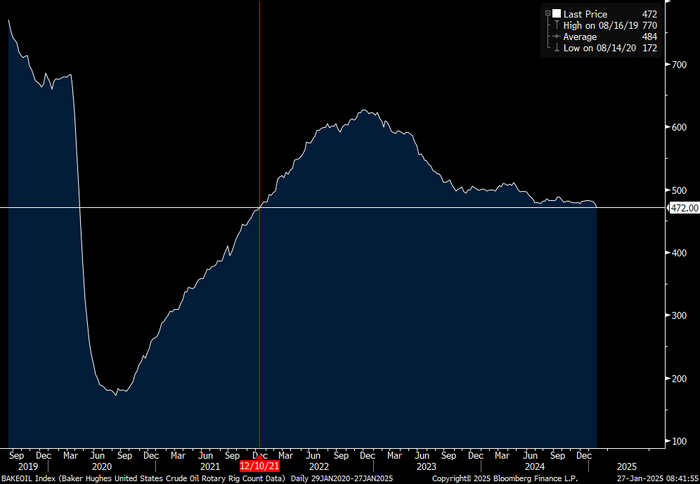

US shale oil producers have no plans to ramp up activity in response to calls from Trump. There are no signs that Trump’s calls for more oil from US producers are bearing any fruits. US shale oil producers are aiming to slow down rather than ramp up activity as they can see the large OPEC+ spare capacity of 5-6 mb/d sitting idle on the sideline. Even the privately held US shale oil players who account for 27% of US oil production are planning to slow down activity this year according to Jefferies Financial Group. US oil drilling rig count falling 6 last week to lowest since Oct 2021 is a reflection of that.

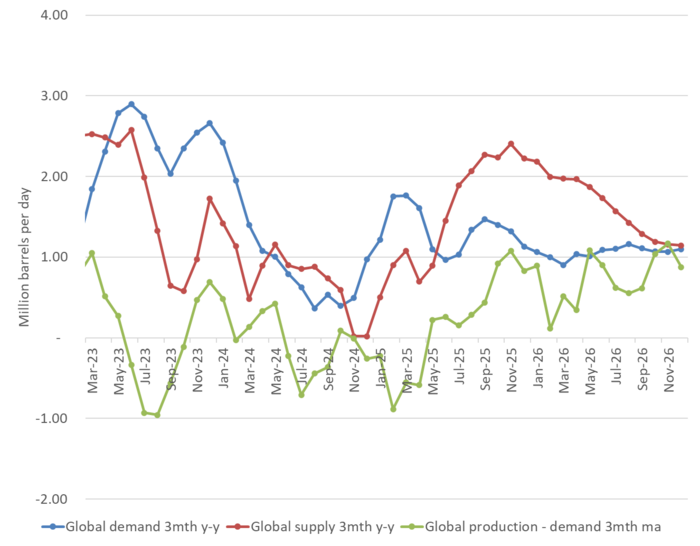

The US EIA projects a problematic oil market from mid-2025. Stronger demand would be the savior. Looking at the latest forecast from the US EIA in its January STEO report one can see why US shale oil producers are reluctant to ramp up production activity. If EIA forecast pans out, then either OPEC+ has to reduce production or US shale oil producers have to if they want to keep current oil prices. The savior would be global economic acceleration and higher oil demand growth.

Saudi Arabia to lift prices for March amid tight Mid-East crude market. But right now, the market is very tight for Mid-East crude due to Biden-sanctions. The 1-3mth Dubai time-spread is rising yet higher this morning. Saudi Arabia will highly likely lift its Official Selling Prices for March in response.

US EIA January STEO report. Global demand and supply growth given as 3mth average y-y diff in mb/d and the outright 3mth average demand diff to 3mth average supply in mb/d. Projects a surplus market where either US shale oil producers have to produce less, or OPEC+ has to produce less.

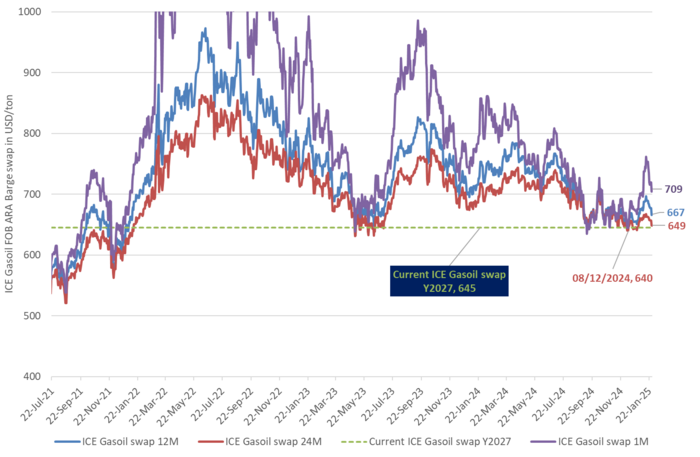

Forward prices for ICE gasoil swaps in USD/ton. Deferred contracts at very affordable levels.

Bearish week last week and dipping lower this morning on China manufacturing and Trump-tariffs. Brent crude traded down 4 out of five days last week and lost 2.8% on a Friday-to-Friday basis with a close of USD 78.5/b. It hit the low of USD 77.8/b on Friday while it managed to make a small 0.3% gain at the end of the week with a close that was marginally below the 200dma. This morning it is trading down 0.4% at USD 78.2/b amid general market bearishness. China manufacturing PMI down to 49.1 for January versus 50.1 in December is pulling copper down 1.3%. Trump threatening Colombia with tariffs.

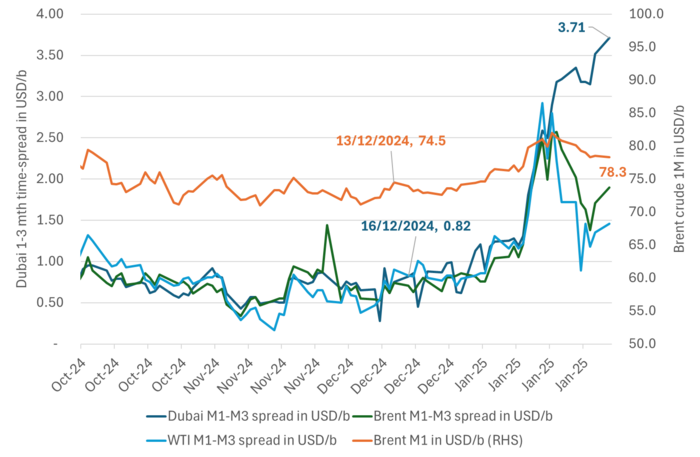

Rebound in crude prices likely as Dubai time-spreads rises further. The Dubai 1-3mth time-spread is rising to a new high this morning of USD 3.7/b. It is a sign that the Biden-sanctions towards Russia is making the medium sour crude market very tight. Brent crude is unlikely to fall much lower as long as these sanctions are in place. Will likely rebound.

Asian buyers turning to the Mid-East to replace Russian barrels. Amin Nasser, CEO of Saudi Aramco, said that the new sanctions are affecting 2 out of 3.4 mb/d of Russian seaborne crude oil exports. Strong bids for Iraqi medium and heavy crudes are sending spot prices to Asia to highest premiums versus formula pricing since August 2023. And Europe is seeing spot premiums to formula pricing at highest since 2021 (Argus).

Strong rise in US oil production is a losing hand. A lot of Trump-talk about a 3 mb/d increase in US oil production. Occidental Petroleum CEO Vicki Hollub commented in Davos that it is possible given the US resource base, but it is not the right thing to do since the global market is oversupplied (Argus). Everyone knows that OPEC+ has a spare capacity of 5-6 mb/d on hand. The comfort zone is probably to have a spare capacity of around 3 mb/d. FIRST the group needs to re-deploy some 3 mb/d of its current spare capacity and THEN the US and the rest of non-OPEC+ can start to think about acceleration in supply growth again. Vicki Hollub understands this and highly likely all the other oil CEOs in the US understands this as well. Donald Trump calling for more US oil will not be met before market circumstances allows it. Even sanctions on Iran forcing 1.5-2.0 mb/d of its crude exports out of the market will first be covered by existing surplus spare capacity within OPEC6+ and not the US.

US oil drilling rig count fell by 6 to 472 last week and lowest since October 2021. Current decline could be due to winter weather in the US but could also be like Hollub commented in Davos arguing that US oil production growth is not the right thing to do.

1-3mth time-spreads in USD/b. Dubai to yet higher level this morning. Even Brent and WTI are rebounding. Could be some extra spike since we are moving towards the end of the month. But it is still indicating a very tight market for medium sour crude as a result of the latest Biden-sanctions.

US oil drilling rig count down 6 last week to lowest level since October 2021

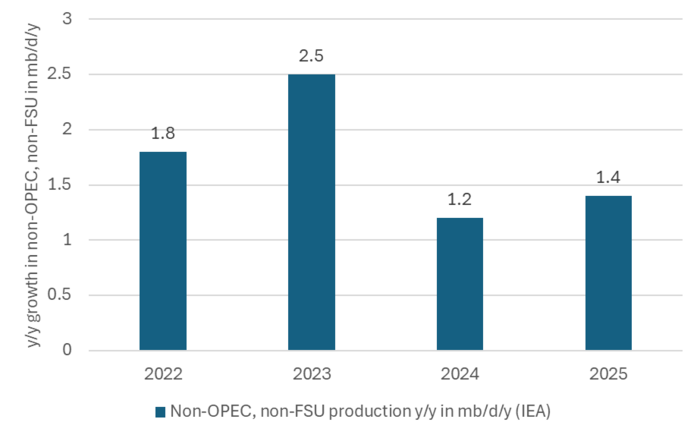

Non-OPEC, non-FSU production to grow 1.4 mb/d in 2025. Third weakest in 4 years. Though still a bit more than total expected global oil demand growth of 1.1 mb/d/y (IEA)

Brent touching down to the 200dma. Brent crude traded down for a fifth day yesterday with a decline of 0.4% to USD 70/b. This morning it has traded as low as USD 78.6/b and touched down and tested the 200dma at USD 78.6/b before jumping back up and is currently trading up 0.2% on the day at USD 79.1/b.

The Dubai 1-3mth time-spread is holding up close to recent highs. The 1-3mth time spreads for WTI and Brent crude have eased significantly. The Dubai 1-3mth spread is however holding up close to latest high. Indian refiner Bharat is reported to struggle to get Russian crude for March delivery (Blbrg). The Biden-sanctions are clearly having physical market effects. So, the Dubai 1-3mth time-spread holding on to recent high makes a lot of sense. I.e. it was not just a spike on fears.

US oil inventories may have risen 6 mb last week (API). Actual data later today. The US DOE will release US oil data for last week later today. The US API last night indicated that US crude and product stocks may have risen close to 6 mb last week. This may be weighing on the oil price today.

Brent and WTI 1-3mths time-spreads have fallen back while Dubai is holding up

Brent crude is no longer overbought. Down touching the 200dma before bouncing back up a lilttle.

Det helt unika fusionskraftsföretaget Helion får ytterligare 5 miljarder kronor i finansiering

Nu bygger LKAB anläggning för kritiska mineral – den första i sitt slag i Europa

Saudi won’t break with OPEC+ to head calls for more oil from Trump

Fyra av Storbritanniens åldrande kärnkraftverk kan förlängas in på 30-talet

Brent rebound is likely as Biden-sanctions are creating painful tightness

Priset på nötkreatur det högsta någonsin i USA

The rally continues with good help from Russian crude exports at 16mths low

Christian Kopfer om olja, koppar, guld och silver

Crude oil comment: Pulling back after technical exhaustion and disappointing US inventory data. Low Cushing stocks lifting eyebrows

Darwei Kung på DWS ger sin syn på råvaror inför 2025 – mest positiv till guld

-

Nyheter4 veckor sedan

Priset på nötkreatur det högsta någonsin i USA

-

Analys3 veckor sedan

The rally continues with good help from Russian crude exports at 16mths low

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanChristian Kopfer om olja, koppar, guld och silver

-

Analys3 veckor sedan

Crude oil comment: Pulling back after technical exhaustion and disappointing US inventory data. Low Cushing stocks lifting eyebrows

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDarwei Kung på DWS ger sin syn på råvaror inför 2025 – mest positiv till guld

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanNy upptäckt av sällsynta jordartsmetaller i Småland

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanTre bra aktier inom koppar med fokus på stabila lågkostnadsprojekt

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMöjligheten att etablera kärnkraft i Motala undersöks