Analys

A two currency oil market

China today launched its long awaited yuan denominated oil contract at the International Energy Exchange (INE) in Shanghai. Seven crude streams from UAE, Qatar, Oman, Yemen Iraq and China will define the pricing of the contract. There is substantial scepticism towards the contract. Most of the sceptical arguments will in our view dissipate over time as rules, regulations and capital controls are adapted and adjusted as time goes by. The Chinese government likely has plenty of leverage to make the contract a success making it into an Asian oil benchmark representing a vibrant and growing oil demand which today accounts for 27% of global demand.

China today launched its long awaited yuan denominated oil contract at the International Energy Exchange (INE) in Shanghai. Seven crude streams from UAE, Qatar, Oman, Yemen Iraq and China will define the pricing of the contract. There is substantial scepticism towards the contract. Most of the sceptical arguments will in our view dissipate over time as rules, regulations and capital controls are adapted and adjusted as time goes by. The Chinese government likely has plenty of leverage to make the contract a success making it into an Asian oil benchmark representing a vibrant and growing oil demand which today accounts for 27% of global demand.

Bjarne Schieldrop, Chief analyst commodities

The launch of the contract will open up for international participation in China’s commodity market for the first time. International oil players will need to hold renminbi books reflecting an oil market which here onwards will roll on two currency wheels.

The rapidly rising risk that Donald, Mike and John will tear up the current Iranian nuclear deal in mid-May makes it likely that Iran will accept crude oil settlement in renminbi in not too long in order to avert the risk of renewed dollar sanctions which it experienced so painfully from 2012 to 2015.

Price action: Brent jumps while equities fall as Venezuela and Iran supply risk increases on John Bolton

The front month Brent crude oil contract jumped 2.2% on Friday to $70.45/bl on news that John Bolton was replacing Lt. Gen. H:R: McMaster as the US national security advisor. John Bolton is known to be abrasive, undiplomatic, deeply conservative and nationalistic with hawkish views on Iran and North Korea. As such he matches both Donald Trump and his new secretary of state Mike Pompeo. It is now difficult to see how the Iran Nuclear deal can survive beyond mid-May when a new round of US waivers is needed to carry the deal forward yet another quarter, unless of course the deal is significantly re-worked. Apparently however the non-US signatories to the Iran nuclear deal are still in the dark with respect to what and how Donald Trump want’s the deal to be re-written. The May waiver deadline is approaching rapidly and as far as we know there is no real work in progress in order to re-work the deal. The appointment of John Bolton also increases the risk for sanctions towards Venezuela. Venezuela’s oil production and export is already in free fall but hanging on a thread by US refineries who are supplying Venezuela with naphtha in exchange of heavy crude oil. Venezuela would not be able to export much oil without the naphtha or light crude which is critical for diluting its heavy crude to a quality which is exportable. Thus US oil sanctions towards Venezuela would cut the last thread.

A two currency oil market

After years and years of waiting the Chinese Yuan denominated oil contract quoted at the Shanghai International Energy Exchange (INE) is finally here. China did try to launch an oil futures contract back in 1993 but it basically blew up due to uncontrollable price volatility. This time around China has taken good time to prepare the launch of its new oil contract in order to make sure that there is no second round flop like in 1993. China last year became the world’s top oil importer with an average import of 8.4 m bl/d. At the same time it is also the world’s sixth biggest oil producer with an average production last year of 3.8 m bl/d.

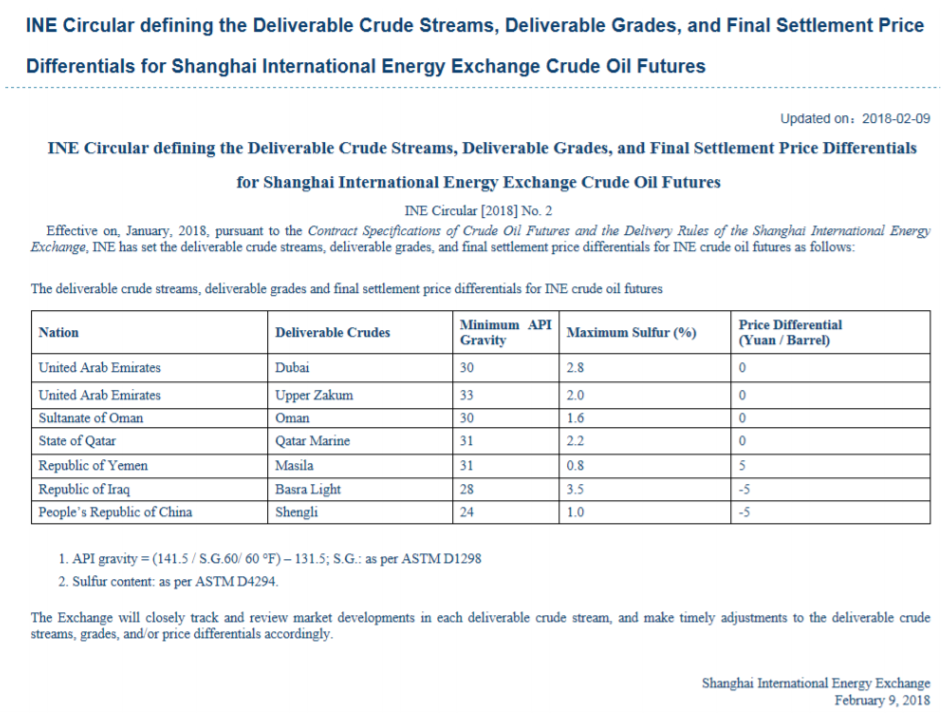

Seven crude streams in the INE contract with characteristics close to the Dubai crude slate

Seven deliverable crude streams in Shanghai will be used to settle the INE crude oil contract. They originate from UAE, Oman, Qatar, Yemen and China itself. The crude streams are distinctly different from the light, sweet crude benchmarks of Brent crude and WTI. The INE crude streams are on average (across the different grades) required to have an API gravity of more than 29.6 and a sulphur content of less than 2%. In comparison the WTI benchmark is very light with an API of 39.6 and only about 0.24% sulphur. As such the INE benchmark is distinctly different from both Brent crude and WTI. It is however very close to the Dubai crude oil marker which has an API of 31 and a sulphur content of 2%. As such one could say that the INE contract is the Dubai marker in Asia quoted in renminbi.

The new INE contract could be a representation of 27 m bl/d of vibrant Asian oil demand

The new Chinese oil contract will likely over time come to represent Asian oil demand in general. In 2018 Asian demand is set to average 27 m bl/d (IEA) or 27% of global consumption. It has been argued that the new benchmark will be a bad price hedge for oil deliveries in other places in Asia than Shanghai. This is based on the assumption that the oil price fundamentally is set either in the US (WTI), in the Gulf (Dubai marker) or in Europe (Brent). And as such it should mathematically be better to hedge with one of these three price points rather than the new Chinese INE contract. However, if the driver of the global oil market and thus oil price dynamics is instead really set by the vibrant oil demand in Asia rather than the three mentioned oil price benchmarks then it would clearly be better to hedge with the INE contract.

In our view the new INE contract is not an effort to replace the existing global crude oil benchmarks. It is instead filling a needed vacuum in the global oil market: A marker for the Asian market. It has been argued that the existing crude benchmarks are successful since they are located at hubs with both large production and consumption. But this is also actually true for the new benchmark with China being the sixth largest oil producer in the world as well as the biggest oil importer in the world.

The INE contract has several disadvantages but these are likely to dissipate over time

To start with the INE contract seems to have several disadvantages. It will have limited trading hours with the last trading slot ending at 0700 am GMT and thus just before the London market opens. The Chinese government has also set crude oil storage costs at twice the global average level in order to avoid excessive price volatility due from potential games between the physical market and the new INE contract. Such high storage costs will be negative for the necessary interplay and price discovery between the local physical market (derived from storage economics) and the INE financial instruments. Another reason for the very high storage cost may be to avoid commodity storage games used for shadow financing and circumvention of capital controls which has flourished for other commodities traded in China. The quotation of the INE contract in renminbi will also be a negative as seen by most current oil market participants in the current dollar dominated oil market. And lastly Chinese capital controls and unpredictable regulations will also be a concern for many potential participants.

Many of these negatives will however dissipate over time. Trading hours will expand, storage costs will normalize, general capital controls will ease and rules and regulations will stabilize. And lastly the renminbi will be more and more accepted currency world-wide. The Chinese government does have time to adjust and the current mode of the INE market is launch phase with some trail and error. The front month INE contract is actually the September 2018 contract allowing plenty of time for adjustment. So we do not think that one should judge the contract in the early phase on the many negative traits which have been highlighted.

Plenty of participants ready to transact – Open interest will be the measure of success

More than 6,000 trading accounts have been opened for the INE contract including China’s largest oil companies and 150 brokerage firms. Larger foreign financial institutions like J.P.Morgan have also opened accounts. To further attract foreign participants the Chinese Government has waived income taxes for foreign investors for the first three years. An addition attraction of the INE oil contract is that it will be the first time foreigners will be able to trade commodities in China.

We agree that over time it will be the size of the number of open contracts and not turnover per se which will be the sign of success for the contract. So the open interest in the INE contract will be the parameter to watch. It will be the fingerprint showing that the INE contract fills a need and is actively used as a hedging tool.

The Chinese government has power to tilt the market towards the new contract

The Chinese government has a lot of power in order to ensure that the INE contract becomes a success with widespread use. The easy way is of course to demand that all domestic crude oil purchasing is done with settlement versus the INE contract benchmark. In that way any oil producer who would like to sell oil to China would have to accept the INE contract and settlement in renminbi. China could of course also lean on the countries who cooperate with China on the Belt and Road Initiative (BRI) with six major infrastructure projects in overdrive this year. Asking the involved countries in these BRI projects to use or support the new INE oil contract could be a natural request.

We think that the launch of the INE contract in China is a natural development reflecting that China is the world’s top oil importer, the sixth largest oil producer and a natural benchmark for oil prices in Asia. However, essentially what it all boils down to is that China wants to be able to purchase its oil in renminbi. There are several countries already on-board: Russia, Venezuela, Nigeria and Angola are all already selling oil to China in renminbi. We assume that UAE, Oman, Qatar, Yemen and Iraq also are accepting renminbi as payment for crude delivered to China since six of the seven crude streams in the INE contract originates from them.

No Iranian crude slates in the INE contract yet but Iran should be a natural participant

It is surprising to see that there are no crude oil streams from Iran in the new INE contract. The Iran Heavy crude stream with API = 30.2 and Sulphur = 1.8% should be a natural match the INE crude slate profile.

Iran is one of the countries which have been heavily hit by the weaponized USD. In 2012 the US applied pressure through the SWIFT system. It blocked clearing for every Iranian bank, froze $100 billion of Iranian assets which together with other measures helped to block Iranian oil exports which roughly dropped 1 m bl/d due to this.

US pressure is building up against the Iran nuclear deal – should naturally drive Iran towards the INE contract

Now pressure is rising rapidly towards Iran. In the US forces are gathering to tear apart the Iran nuclear deal with the recent appointment of Mike Pompeo as US secretary of state and John Bolton as the US national security advisor. Donald Trump together with these two now looks ready to tear apart the current Iran nuclear deal as waivers are up for renewal in mid-May. The Saudi crown prince Mohammed bin Salman also seemed to apply pressure against Iran at his meeting with Donald Trump. Thus Saudi Arabia seems like it is sticking with the US while Iran, Iraq, Oman, UAE, Qatar and Yemen are drifting over towards China. China and the US are at the same time drifting apart amid increasing trade tensions with political tensions in the South China Sea being the icing on the cake so to speak. It seems highly plausible in our view that Iran in not too long with explicitly state that they also accept payment in renminbi for oil sales to China.

Saudi Arabia however seems for the time being to stick even tighter to the dollar-oil deal which the House of Saud presumably struck with Nixon and Kissinger back in 1974 in exchange for protection and geopolitical support.

Crude slates in the INE contract

Ch1: Yes, the INE September contract started to trade first time on 26 March 2018

Ch2: Brent crude went opposite of equities last week

Ch3: Weekly US, EU, Singapore and Floating stocks lower 2nd week

When it starts to move lower it moves rather quickly. Gaza, China, IEA. Brent crude is down 2.1% today to $62/b after having traded as high as $66.58/b last Thursday and above $70/b in late September. The sell-off follows the truce/peace in Gaze, a flareup in US-China trade and yet another bearish oil outlook from the IEA.

A lasting peace in Gaze could drive crude oil at sea to onshore stocks. A lasting peace in Gaza would probably calm down the Houthis and thus allow more normal shipments of crude oil to sail through the Suez Canal, the Red Sea and out through the Bab-el-Mandeb Strait. Crude oil at sea has risen from 48 mb in April to now 91 mb versus a pre-Covid normal of about 50-60 mb. The rise to 91 mb is probably the result of crude sailing around Africa to be shot to pieces by the Houthis. If sailings were to normalize through the Suez Canal, then it could free up some 40 mb in transit at sea moving onshore into stocks.

The US-China trade conflict is of course bearish for demand if it continues.

Bearish IEA yet again. Getting closer to 2026. Credibility rises. We expect OPEC to cut end of 2025. The bearish monthly report from the IEA is what it is, but the closer we get to 2026, the more likely the IEA is of being ball-park right in its outlook. In its monthly report today the IEA estimates that the need for crude oil from OPEC in 2026 will be 25.4 mb/d versus production by the group in September of 29.1 mb/d. The group thus needs to do some serious cutting at the end of 2025 if it wants to keep the market balanced and avoid inventories from skyrocketing. Given that IEA is correct that is. We do however expect OPEC to implement cuts to avoid a large increase in inventories in Q1-26. The group will probably revert to cuts either at its early December meeting when they discuss production for January or in early January when they discuss production for February. The oil price will likely head yet lower until the group reverts to cuts.

Dubai: The Mid-East anchor dragging crude oil lower. Surplus emerging in Mid-East pricing. Crude oil prices held surprisingly strong all through the summer. A sign and a key source of that strength came from the strength in the front-end backwardation of the Dubai crude oil curve. It held out strong from mid-June and all until late September with an average 1-3mth time-spread premium of $1.8/b from mid-June to end of September. The 1-3mth time-spreads for Brent and WTI however were in steady deterioration from late June while their flat prices probably were held up by the strength coming from the Persian Gulf. Then in late September the strength in the Dubai curve suddenly collapsed. Since the start of October it has been weaker than both the Brent and the WTI curves. The Dubai 1-3mth time-spread now only stands at $0.25/b. The Middle East is now exporting more as it is producing more and also consuming less following elevated summer crude burn for power (Aircon) etc.

The only bear-element missing is a sudden and solid rise in OECD stocks. The only thing that is missing for the bear-case everyone have been waiting for is a solid, visible rise in OECD stocks in general and US oil stocks specifically. So watch out for US API indications tomorrow and official US oil inventories on Thursday.

No sign of any kind of fire-sale of oil from Saudi Arabia yet. To what we can see, Saudi Arabia is not at all struggling to sell its oil. It only lowered its Official Selling Prices (OSPs) to Asia marginally for November. A surplus market + Saudi determination to sell its oil to the market would normally lead to a sharp lowering of Saudi OSPs to Asia. Not yet at least and not for November.

The 5yr contract close to fixed at $68/b. Of importance with respect to how far down oil can/will go. When the oil market moves into a surplus then the spot price starts to trade in a large discount to the 5yr contract. Typically $10-15/b below the 5yr contract on average in bear-years (2009, 2015, 2016, 2020). But the 5yr contract is usually pulled lower as well thus making this approach a moving target. But the 5yr contract price has now been rock solidly been pegged to $68/b since 2022. And in the 2022 bull-year (Brent spot average $99/b), the 5yr contract only went to $72/b on average. If we assume that the same goes for the downside and that 2026 is a bear-year then the 5yr goes to $64/b while the spot is trading at a $10-15/b discount to that. That would imply an average spot price next year of $49-54/b. But that is if OPEC doesn’t revert to cuts and instead keeps production flowing. We think OPEC(+) will trim/cut production as needed into 2026 to prevent a huge build-up in global oil stocks and a crash in prices. But for now we are still heading lower. Into the $50ies/b.

Some rebound but not much. Brent crude rebounded 1.5% yesterday to $65.47/b. This morning it is inching 0.2% up to $65.6/b. The lowest close last week was on Thursday at $64.11/b.

The curve structure is almost as week as it was before the weekend. The rebound we now have gotten post the message from OPEC+ over the weekend is to a large degree a rebound along the curve rather than much strengthening at the front-end of the curve. That part of the curve structure is almost as weak as it was last Thursday.

We are still on a weakening path. The message from OPEC+ over the weekend was we are still on a weakening path with rising supply from the group. It is just not as rapidly weakening as was feared ahead of the weekend when a quota hike of 500 kb/d/mth for November was discussed.

The Brent curve is on its way to full contango with Brent dipping into the $50ies/b. Thus the ongoing weakening we have had in the crude curve since the start of the year, and especially since early June, will continue until the Brent crude oil forward curve is in full contango along with visibly rising US and OECD oil inventories. The front-month Brent contract will then flip down towards the $60/b-line and below into the $50ies/b.

At what point will OPEC+ turn to cuts? The big question then becomes: When will OPEC+ turn around to make some cuts? At what (price) point will they choose to stabilize the market? Because for sure they will. Higher oil inventories, some more shedding of drilling rigs in US shale and Brent into the 50ies somewhere is probably where the group will step in.

There is nothing we have seen from the group so far which indicates that they will close their eyes, let the world drown in oil and the oil price crash to $40/b or below.

The message from OPEC+ is also about balance and stability. The world won’t drown in oil in 2026. The message from the group as far as we manage to interpret it is twofold: 1) Taking back market share which requires a lower price for non-OPEC+ to back off a bit, and 2) Oil market stability and balance. It is not just about 1. Thus fretting about how we are all going to drown in oil in 2026 is totally off the mark by just focusing on point 1.

When to buy cal 2026? Before Christmas when Brent hits $55/b and before OPEC+ holds its last meeting of the year which is likely to be in early December.

Brent crude oil prices have rebounded a bit along the forward curve. Not much strengthening in the structure of the curve. The front-end backwardation is not much stronger today than on its weakest level so far this year which was on Thursday last week.

The front-end backwardation fell to its weakest level so far this year on Thursday last week. A slight pickup yesterday and today, but still very close to the weakest year to date. More oil from OPEC+ in the coming months and softer demand and rising inventories. We are heading for yet softer levels.

Down to the lowest since early May. Brent crude has fallen sharply the latest four days. It closed at USD 64.11/b yesterday which is the lowest since early May. It is staging a 1.3% rebound this morning along with gains in both equities and industrial metals with an added touch of support from a softer USD on top.

What stands out the most to us this week is the collapse in the Dubai one to three months time-spread.

Dubai is medium sour crude. OPEC+ is in general medium sour crude production. Asian refineries are predominantly designed to process medium sour crude. So Dubai is the real measure of the balance between OPEC+ holding back or not versus Asian oil demand for consumption and stock building.

A sharp weakening of the front-end of the Dubai curve. The front-end of the Dubai crude curve has been holding out very solidly throughout this summer while the front-end of the Brent and WTI curves have been steadily softening. But the strength in the Dubai curve in our view was carrying the crude oil market in general. A source of strength in the crude oil market. The core of the strength.

The now finally sharp decline of the front-end of the Dubai crude curve is thus a strong shift. Weakness in the Dubai crude marker is weakness in the core of the oil market. The core which has helped to hold the oil market elevated.

Facts supports the weakening. Add in facts of Iraq lifting production from Kurdistan through Turkey. Saudi Arabia lifting production to 10 mb/d in September (normal production level) and lifting exports as well as domestic demand for oil for power for air con is fading along with summer heat. Add also in counter seasonal rise in US crude and product stocks last week. US oil stocks usually decline by 1.3 mb/week this time of year. Last week they instead rose 6.4 mb/week (+7.2 mb if including SPR). Total US commercial oil stocks are now only 2.1 mb below the 2015-19 seasonal average. US oil stocks normally decline from now to Christmas. If they instead continue to rise, then it will be strongly counter seasonal rise and will create a very strong bearish pressure on oil prices.

Will OPEC+ lift its voluntary quotas by zero, 137 kb/d, 500 kb/d or 1.5 mb/d? On Sunday of course OPEC+ will decide on how much to unwind of the remaining 1.5 mb/d of voluntary quotas for November. Will it be 137 kb/d yet again as for October? Will it be 500 kb/d as was talked about earlier this week? Or will it be a full unwind in one go of 1.5 mb/d? We think most likely now it will be at least 500 kb/d and possibly a full unwind. We discussed this in a not earlier this week: ”500 kb/d of voluntary quotas in October. But a full unwind of 1.5 mb/d”

The strength in the front-end of the Dubai curve held out through summer while Brent and WTI curve structures weakened steadily. That core strength helped to keep flat crude oil prices elevated close to the 70-line. Now also the Dubai curve has given in.

Brent crude oil forward curves

Total US commercial stocks now close to normal. Counter seasonal rise last week. Rest of year?

Total US crude and product stocks on a steady trend higher.

The Mid-East anchor dragging crude oil lower

Samtal om sällsynta jordartsmetaller, guld och silver

Brookfield köper bränsleceller för 5 miljarder USD av Bloom Energy för att driva AI-datacenter

Teck Resources kan förse Nordamerika och kanske hela G7 med all germanium som behövs

Leading Edge Materials är på rätt plats i rätt tid

Kinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde

Tyskland har så höga elpriser att företag inte har råd att använda elektricitet

OPEC+ missar produktionsmål, stöder oljepriserna

Ett samtal om guld, olja, fjärrvärme och förnybar energi

Brent crude ticks higher on tension, but market structure stays soft

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanKinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde

-

Nyheter4 veckor sedan

Tyskland har så höga elpriser att företag inte har råd att använda elektricitet

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOPEC+ missar produktionsmål, stöder oljepriserna

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEtt samtal om guld, olja, fjärrvärme och förnybar energi

-

Analys4 veckor sedan

Brent crude ticks higher on tension, but market structure stays soft

-

Analys3 veckor sedan

Are Ukraine’s attacks on Russian energy infrastructure working?

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanGuld nära 4000 USD och silver 50 USD, därför kan de fortsätta stiga

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGuldpriset uppe på nya höjder, nu 3750 USD