Nyheter

Molybdenum’s dramatic price response

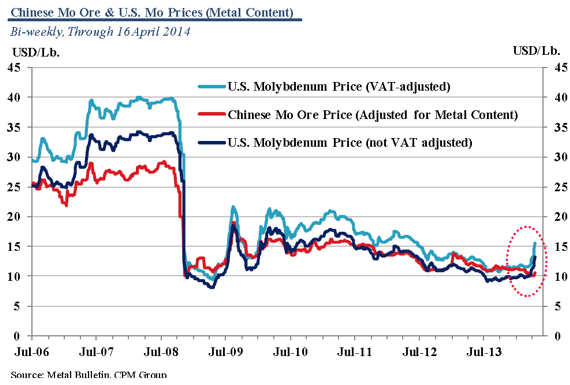

![]() Molybdenum prices in Europe have risen rapidly following the World Trade Organization’s confirmation that the export duties and quotas imposed by China on molybdenum are incompatible with its WTO obligations. This report concludes a dispute initiated in March 2012 when the European Union, Japan, and the United States filed a formal request with the WTO for consultation with China over its restrictions on exports of rare earths, tungsten, and molybdenum. As of 16 April molybdenum prices have jumped nearly 31% to $13.20 (basis Metal Bulletin, US$ per pound Mo contained) since the 26 March report. Prices in China meanwhile are up just 4.2% over this same period.

Molybdenum prices in Europe have risen rapidly following the World Trade Organization’s confirmation that the export duties and quotas imposed by China on molybdenum are incompatible with its WTO obligations. This report concludes a dispute initiated in March 2012 when the European Union, Japan, and the United States filed a formal request with the WTO for consultation with China over its restrictions on exports of rare earths, tungsten, and molybdenum. As of 16 April molybdenum prices have jumped nearly 31% to $13.20 (basis Metal Bulletin, US$ per pound Mo contained) since the 26 March report. Prices in China meanwhile are up just 4.2% over this same period.

China has yet to announce a formal response to the WTO’s ruling. There is a possibility that China may remove the export duties on some molybdenum products as a concession in order to keep duties and quotas on tungsten and rare earths. As part of a January 2013 response to a WTO ruling on a separate case regarding export taxes on silicon metal, silicon carbide, manganese, magnesium, zinc, bauxite, coking coal, fluorspar and yellow phosphorus, the Chinese government removed the 20% duty on the export of EMM as well as some of the duties of other metals.

China may be pushed to reduce or remove the current duties on molybdenum product exports, as had been the case with the electrolytic manganese (EMM) export duty. EMM exports rose strongly in response, possibly due to exporters officially reporting their goods at customs rather than smuggling them out of the country. Official EMM prices also fell.

The case for molybdenum differs from EMM, however, as it is a metal under consideration for a national resource classification. Official regulations for the molybdenum industry could be shifted to the Ministry of Land and Resources, which also manages tungsten and rare earths. There also are government concerns with regard to the price stability of these specialty metal markets. In the past, the Chinese government has adamantly opposed lowering prices for its raw material exports, particularly in instances related to price competition by a large number of domestic exporters. That said, there have been major producers voicing support for lowering trade barriers as they seek to expand sales internationally in response to the lack of orders for the surplus metal in the domestic market.

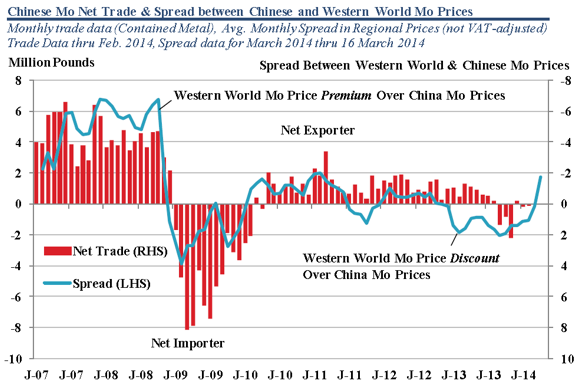

In 2013 China’s domestic molybdenum prices traded at premium (~14.3%) to western world prices so there was no incentive to export molybdenum. This trend remained in place until the run up in western world prices in the first two weeks in April. According to Metal Bulletin, Chinese prices held on average a $0.91 or 9.2% premium over western world price between 1 January and 21 March. Since the ruling, however, western world prices are at a premium to China. As of 16 April, Metal Bulletin reported western world molybdenum at $13.20 and Chinese molybdenum at roughly $10.55, a premium of $2.65 or 20%. Obviously both markets need time to process the news. However, western world prices have risen to levels that will likely encourage exports from China in the near term. Even with current duties in place on various molybdenum products, some of which are as high as 20%, arbitrage opportunities still exist for Chinese exporters. The current sizable price differential may act as an incentive for the Chinese government to keep present taxes in place to help disincentivize exports of their national molybdenum resource.

Furthermore molybdenum prices in the western world are being bolstered by robust demand, which has been strengthening in regions outside of China. This is most notable in Europe and South Korea, which have seen a strong rebound in steel production during first two months of 2014 growing 6.5% and 3.9% year-on-year, respectively, compared to -2.2% and -4.8% in all of 2013. Crude steel production is also strengthening in Japan, with output rising 3.8% in the first two months of 2014 from year ago levels.

[box]Denna analys är producerad av CPM Group och publiceras med tillstånd på Råvarumarknaden.se.[/box]

Disclaimer

Copyright CPM Group 2012. Not for reproduction or retransmission without written consent of CPM Group. Market Commentary is published by CPM Group and is distributed via e-mail. The views expressed within are solely those of CPM Group. Such information has not been verified, nor does CPM make any representation as to its accuracy or completeness.

Any statements non-factual in nature constitute only current opinions, which are subject to change. While every effort has been made to ensure that the accuracy of the material contained in the reports is correct, CPM Group cannot be held liable for errors or omissions. CPM Group is not soliciting any action based on it. Visit www.cpmgroup.com for more information.

Det råder speciella förutsättningar på elmarknaden just nu och allt styrs till största delen av vädret. Sol och bitvis god vindkraftsproduktion under maj, i kombination med svag hydrologi och begränsad kärnkraft har lett till stora svängningar i elpriset. Juni inleds liknande och idag tangerar elpriserna nivåer från krisåret 2022. Dock förväntas elpriserna gå ner då kärnkraften ökar.

Juni börjar med höga elpriser och orsakerna är brist på vindkraft, torra väderprognoser och mindre kärnkraft. Prisuppgången i maj var särskilt tydlig i norra Sverige, elområde 1 och 2, och ligger just nu nära en krona per kWh. I elområdena 3 och 4, södra Sverige, blev månadsmedelspotpriset för maj 35–40 procent högre jämfört med april men har rusat idag till nivåer på mellan 130–160 öre/kWh.

– Dagens höga priser visar tydligt på hur snabbt förändrade väderprognoser får genomslag på elpriset. Sommarens väder påverkar även priserna inför hösten och vintern. Ska det bli mer stabila elpriser behövs ett typiskt svenskt sommarväder, dvs. en blandning av regn, vind och sol, snarare än extremvärme och högtryck. Särskilt viktig är nederbörden i Norge och norra Sverige där vattenkraften dominerar, säger Jonas Stenbeck, privatkundschef på Vattenfall Försäljning.

Den hydrologiska balansen, dvs. det sammanlagda vatteninnehållet i snö, mark och magasin, är väldigt ansträngt efter en snöfattig vinter. Det stora underskottet håller i sig och är starkt beroende av mer nederbörd i närtid. På grund av pågående revisioner, bland annat Ringhals 3 och Forsmark 2, är elproduktionen från svensk kärnkraft begränsad just nu. Oskarshamn 3 har planerad återstart den 10 juni och Ringhals 4, som för närvarande producerar med halv effekt, går upp till full effekt den 12 juni. Det innebär att den installerade effekten då kommer att stiga från 40 till 60 procent i Sverige.

Det geopolitiska läget är fortsatt ett orosmoment men ryktet om ett fredsförslag har lugnat marknaden något. Gas- och oljepriserna fortsätter att falla och de stigande temperaturerna på kontinenten och den stora andelen solkraft kan ha en stabiliserande effekt.

| Medelspotpris | Elområde 1, Norra Sverige | Elområde 2, Norra Mellansverige | Elområde 3, Södra Mellansverige | Elområde 4, Södra Sverige |

| Maj 2026 | 46,36 öre/kWh | 48,95 öre/kWh | 70,86 öre/kWh | 87,05 öre/kWh |

| Maj 2025 | 14,09 öre/kWh | 15,09 öre/kWh | 42,94 öre/kWh | 60,01 öre/kWh |

Snabba väderomslag har präglat elmarknaden i april, med både prisfall och pristoppar som följd. Samtidigt får solkraften allt större påverkan och pressar ner elpriserna, särskilt i södra Sverige.

Månadsmedelpriset för april på den nordiska elbörsen Nord Pool utan påslag och exklusive moms blev 58,66 öre/kWh i elområde 3, södra Mellansverige, och 22,75 öre/kWh i elområde 1, norra Sverige. På kontinenten syns den så kallade ankkurvan tydligt.

– Nu är solen helt klart på gång. I Tyskland har solen under april producerat nästan 2 TWh mer än ifjol vilket även gynnar oss i Sverige. Ankkurvefenomenet innebär att elpriset är lågt mitt på dagen och stiger raskt mot kvällen. Under perioder med soligt och varmare vårväder är solen ett välkommet inslag här hemma och det påverkar elpriserna nedåt. Den ökar produktionen och minskar konsumtionen, säger Jonas Stenbeck, privatkundschef på Vattenfall Försäljning.

De årliga, planerade underhållsarbetena på kärnkraftverken pågår, vilket innebär att den tillgängliga kapaciteten just nu är cirka 60 procent. Vinden var varierande under april, med snabba skiften mellan stilla och blåsiga perioder, vilket märktes på elpriset.

Den hydrologiska balansen i Norden, alltså det sammanlagda vatteninnehållet i snö, mark och magasin, är svag med betydande underskott i södra Norge. Men magasinsnivåerna i Sverige ligger kring normala nivåer för årstiden och har börjat fyllas på.

– Dock förväntas årets vårflod att, givet dagens förutsättningar, bli lägre än normalt då snötäcket är avsevärt mindre än vanliga nivåer. Vädret kommer avgöra hur väl vårfloden fyller magasinen inför sommaren, säger Jonas Stenbeck.

De höga gaspriserna har fallit något, samtidigt som stigande temperaturer på kontinenten och den stora andelen solkraft haft en stabiliserande effekt. Det geopolitiska läget är dock fortsatt ett orosmoment.

– Det vi sett är att marknaden är väldigt nyhetsdriven. Beroende av vad som rapporteras så reagerar marknaden direkt. Det gör att vi befinner oss i en väldigt speciell situation eftersom denna osäkerhet skapar svängiga och oförutsägbara bränslepriser, vilket i slutändan påverkar elpriset. Jag förstår att många känner en oro men i och med att det blir varmare så kommer man inte att behöva lika mycket el, vilket ger en lägre elkostnad, säger Jonas Stenbeck.

| Medelspotpris | April 2025 | April 2026 |

| Elområde 1, Norra Sverige | 14,39 öre/kWh | 26,09 öre/kWh |

| Elområde 2, Norra Mellansverige | 14,21 öre/kWh | 26,85 öre/kWh |

| Elområde 3, Södra Mellansverige | 37,61 öre/kWh | 56,08 öre/kWh |

| Elområde 4, Södra Sverige | 58,35 öre/kWh | 66,55 öre/kWh |

*Ankkurva: Ankkurvan beskriver hur elproduktionen från förnybara energikällor, som solenergi, påverkar elnätet och elanvändningen över en dag. Kurvan har fått sitt namn eftersom grafen under en dag liknar profilen av en anka.

Råvaran olja handlas fortsatt över 100 USD per fat och det är något stökigt med prissättningen. Michel Gubel ger sin syn på läget för oljan, att priskurvan kan vara i contango och backwardation, samt vad som kan hända med olja på längre sikt.

Sommarväder skapar prisrally på elbörsen

Oil product price pain is set to rise as the Strait of Hormuz stays closed into summer

Solkraften pressar elpriserna dagtid

Michel Gubel ger sin syn på oljemarknaden