Nyheter

World´s largest silver producer and a lot more than that

Enormous exploration potential secures future growth

Enormous exploration potential secures future growth

According to the Silver Institute, Mexico maintained it long-time position as the world’s largest silver producer with a production of 128.6 millions of ounces in 2010. But as said, it is a lot more than that. It ranks 11th in the list of the world’s largest gold producers, 9th in the list of the world’s largest copper producers, 6th in the list of the world’s largest zinc producers, 5th in the list of the world’s largest lead producers and 16th in the list of the world’s largest iron ore producers. Historically, mining and exploration has been a significant activity in many parts of the country and often a main source for families to make a living. The industry was very fragmented, also due to the old mining laws that were in force. In a report that I wrote a few years ago, I illustrated the silver mining industry by mentioning that there were many, many silver producers but that 75% of the total production was coming from the top-3 mines. That situation has been changing in the last few years. A new mining law was adopted which gave much more flexibility to mining companies to build their property portfolios with larger entities. Many foreign, mostly Canadian companies finally could develop their plans so that today, the mining industry is a much more modern industry than ever before. Moreover, as described above, the production of other metals has become increasingly important. I have followed the developments in Mexico for many years and I believe that its mining and exploration industry is facing a long term and very prospective future in view of fundamental economic factors relating to the international use of metals and minerals, I am confident that Mexico will retain and even enhance its prominent position in the world of metals and mining. That is why I decided to initiate this new MINING IN MEXICO publication.

After about the 10 years of indulgence, frustration, cost-consciousness, scraping finances, lacklustre share prices, in short: surviving, that characterized the world of mining and metals in the 1990’s, the current period of recovery started in 2002. Almost everywhere in the world, mining and exploration activities stepped up considerably as a result of the new hunger for metals. If there is one country in the world where exploration activities have come to a frenzy again, it is Mexico. From a country that had been in a severe economic turmoil, triggered by the devaluation of the peso in late 1994, which threw the country in its worst recession in over half a century, Mexico turned into a country of reorganization and remarkable revival. The mining industry played a significant role in that. Not surprisingly, because there were, and still are, several obvious factors present that made and make the choice for Mexico a very logic one:

- Mexico has a mining history of almost 500 years. But already in the ancient times, thousands of years ago, the Mayans and Aztecs built complex civilizations using gold and silver. It was also ’plata’ that made the Spanish rulers stay there from 1521 to 1821 when independence came. This all has built a deep-rooted tradition of extensive mining expertise;

- the political situation is considered to be a most stable one, although the outbursts of violence between the drug lords and their gangs have become a factor of concern over the last few years. President Felipe Calderon has made combating this organised crime a priority and has been quite successful in removing some top leaders;

- the government has been and is very friendly towards mining and exploration activities and welcomes foreign corporate entities and capital to be applied to the benefit of the country and its people;

- the legal and regulatory circumstances for mining and exploration have significantly improved by implementation of the National Mining Development Plan, released in 2002 and updated in 2007 and the 2005 amendment of the Mexican Mining Law;

- foreign companies can own 100% of Mexican companies, freely import and export capital and new land ownership regulations have made an end to the historical highly fragmented ownership of mining claim areas;

- there are no taxes or levies imposed specifically on the mining industry. Companies pay the standard corporate income tax rates;

- the country has an excellent infrastructure of air, road and rail transport facilities. There are approximately 365,000 km of paved roads and 27,000 km of railroads, several major maritime ports and numerous international airlines serving the country;

- due to Mexico’s a long time record of mining and exploration activities, experienced labour forces are readily available;

- currency risks have been diminished since the Mexican peso is pegged to the US$;

- and most importantly, the ready availability of known under-explored mineral properties and projects with available records of past exploration.

Mexico is generally considered to be one of the most attractive and easiest accessible destinations for mining and exploration companies in the world. In several studies, Mexico has been ranked among the most desirable countries for applying exploration capital. In a study of the Metals Economics Group, Mexico came right behind the top three, Canada, Australia and the United States. Therefore, it is not surprising that now over 250 foreign mining companies are active in this industry: around 75% are Canadian, 14% hail from the United States, the balance is made up by England, Australia, Japan, China and Korea. Mining and exploration are spread over practically all over Mexico. In several regions, it looks as if the mining operations are almost next door to each other. From the north-west, three rich gold and silver belts run adjacently downwards through about 70% over half of the country’s territory, on both sides of the Sierra Madre Occidental mountain chains. The map on the page 5 of this report gives a good impression of the density of mining in the country. Looking at the production companies, the leader of the pack is the established Mexican Fresnillo (LSE, MSE: FRES), the world’s largest primary silver producer and the second largest gold producer of Mexico. The company is determined to maintain that position and strives to produce 65 million ounces of silver and over 400,000 ounces of gold by 2018.

[quote]Mexico has been the largest silver producing country in the world since long with production having increased from 91.7 million ounces of silver produced in 2002 to 128.6 million ounces in 2010[/quote]

During the last 10 years, several younger companies have joined the ranks of producers, either through extensive exploration programs on their projects or by taking over and refurbishing former producers. In the silver sector, companies like Pan American Silver* (TSX: PAAS) Coeur d’Alene (NYSE:CDE, TSX:CDM), Endeavour Silver (NYSE:EXK), TSX:EDR), Great Panther Silver** (TSX:GPR, NYSE:GPL), First Majestic (TSX:FR, NYSE:AG), Excellon* (TSX:EXN) and Aurcana (TSXV: AUN) have made great progress by developing their companies from one of the many exploration companies to the more prominent ranks of silver producers.

[quote]Mexico has been emerging as a significant gold producer, having almost tripled its production from 685.000 ounces in 2002 to over 1.750,000 ounces in 2010[/quote]

However, as said in the heading of this report, Mexico should not only be seen as a leading silver producer. In the last decade, Mexico has also emerged as a significant gold producer. Having almost tripled its gold production, it is very likely that Mexico will continue to move up in the ranks of world gold producers and enter the top-10 list of producers in the next few years. In the gold sector, the largest production company is Goldcorp (NYSE:GG, TSX:G), which brought its Peñaquito mine to production in 2010, to be Mexico’s largest open pit mine, containing gold, silver, lead and zinc. Together with the producing

Los Filos and El Sauzal mines, total production is expected to further increase considerably. Of course, also here Fresnillo has to be mentioned. As stated above, it is the second largest gold producer in the country. Other emerging gold producers are Alamos Gold (TSX:AGI), Agnico-Eagle (NYSE, TSX:AEM), AuRico Gold (TSX, NYSE:AUQ) -the former Gammon Gold-, Minefinders* which made the headlines last week with the announcement that it will be acquired by Pan American and thus become a part of a very powerful gold and silver producing combination, Newgold* (TSX:NGD), Timmins Gold** (NYSE:TGD, TSX:TMM) and the newest kid on the gold production block, Argonaut Gold (TSX:AR).

To take a quick peek into the near future, there are three companies that are currently moving rapidly towards their initial production stage. First of all, the never to be ignored, newly formed McEwen Mining (NYSE, TSX:MUX) -originating from the U.S. Gold and Minera Andes combination- that will be joining the producers group this year when its El Gallo mine will be completed and commissioned, then NWM Mining (TSXV:NWM) that is commissioning its completed mine and Vista Gold* (NYSE, TSX:VGZ) which is now in the permitting stage.

This review of the companies that are currently producing silver and gold does not pretend to be complete but gives, in my opinion, a good view of what is happening today in Mexico in this fascinating sector. I do hope it shows you that the launch of this new publication is a sensible thing to do. And of course that you will find it worthwhile to give it your attention. On the next page you will find a map of Mexico which shows the most important locations of production projects. I think it is warranted to say that there is hardly another country to be found in the world, where there is this kind of density of resource activities. Certainly giving me enough to talk and write about in the forthcoming issues.

In the next issue of MINING IN MEXICO I will give you a review of the most interesting exploration companies and projects. That report will also include an overview of The Centre’s Having looked closely at what is going on in Mexico and in line with my firm belief that the overall mining and exploration industry is facing very prospective longterm future in view of fundamental economic factors relating to the international use of metals and minerals, I am confident that Mexico will not only retain but significantly enhance its leading position in the world’s mining and exploration scene. International investors have been paying attention and should continue to do so.

* these companies were signalled in their early stage of developments in previous reporting and coverage of The Centre

** these companies are current Supporting Companies of The Centre and will be described extensively in Corporate Reports, to be published in the near future, and updated later this year.

Henk J. Krasenberg

European Gold Centre

[hr]

European Gold Centre

European Gold Centre analyzes and comments on gold, other metals & minerals and international mining and exploration companies in perspective to the rapidly changing world of economics, finance and investments. Through its publications, The Centre informs international investors, both institutional and private, primarily in Europe but also worldwide, who have an interest in natural resources and investing in resource companies.

The Centre also provides assistance to international mining and exploration companies in building and expanding their European investor following and shareholdership.

Henk J. Krasenberg

After my professional career in security analysis, investment advisory, porfolio management and investment banking, I made the decision to concentrate on and specialize in the world of metals, minerals and mining finance. From 1983 to 1992, I have been writing and consulting about gold, other metals and minerals and resource companies.

The depressed metal markets of the early 1990’s led me to a temporary shift. I pursued one of my other hobbies and started an art gallery in contemporary abstracts, awaiting a new cycle in metals and mining. That started to come in the early 2000’s and I returned to metals and mining in 2002 with the European Gold Centre.

With my GOLDVIEW reports, I have built an extensive institutional investor following in Europe and more of a private investor following in the rest of the world. In 2007, I introduced my MINING IN AFRICA publication, to be followed by MINING IN EUROPE in 2010 and MINING IN MEXICO in 2012.

For more information: www.europeangoldcentre.com

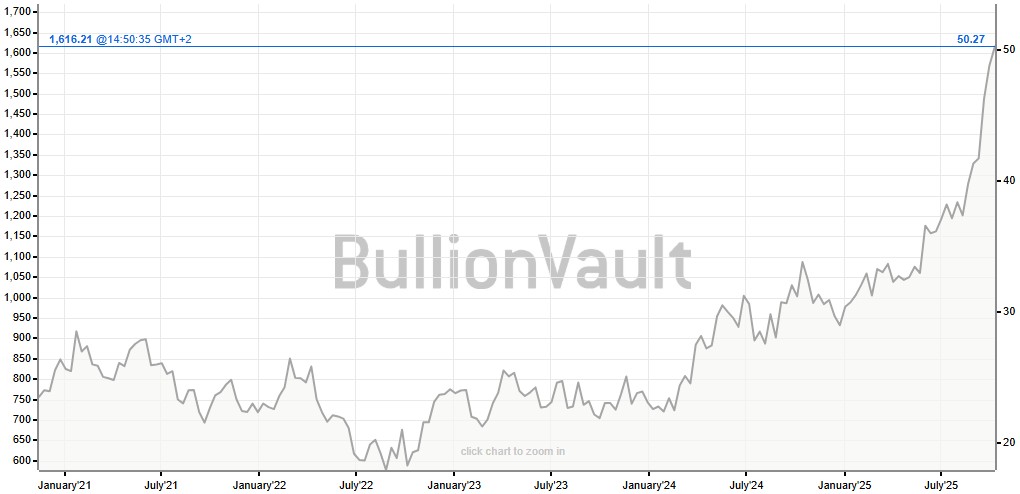

Ädelmetallen silver spränger en smått magisk gräns och handlas nu över 50 USD per uns. Priset har verkligen exploderat. Silver följer med i ett bredare rally där fult nyligen sprängde 4000 USD per uns-nivån. Priset för att låna silver har också skjutit i höjden på senare tid vilket indikerar att tillgången på silver på den fysiska marknaden har börjat bli lågt. Samtidig är efterfrågan från industrin bra och räntorna låga. Och på toppen av det kan vi lägga geopolitisk oro som gör att fler letar sig till fysiska tillgångar som silver.

Blykalla, Evroc och Studsvik har undertecknat ett samförståndsavtal för att undersöka möjligheten att utveckla Sveriges första kärnkraftsdrivna datacenter vid Studsviks licensierade kärnkraftsanläggning i Nyköping.

Blykalla utvecklar avancerade blykylda kärnreaktorer för att leverera säker, kostnadseffektiv och hållbar basenergi. Evroc bygger hyperscale-moln- och AI-infrastruktur för att driva Europas digitala framtid. Studsvik driver en licensierad kärnkraftsanläggning i Nyköping och tillhandahåller livscykeltjänster för kärnkraftssektorn, inklusive bränsle, material och avfallshantering. Tillsammans kombinerar de teknik, infrastruktur och anläggningsexpertis för att påskynda utbyggnaden av kärnkraftsdrivna datacenter.

Det finns en växande internationell efterfrågan på kärnkraftsdrivna datacenter, driven av parallella krav från AI och elektrifiering. Med sin kapacitet att leverera ren, pålitlig baskraft och inbyggd redundans är små modulära reaktorer särskilt väl lämpade för att möta detta behov.

Belastar inte elnätet

En stor fördel med att bygga datacenter och kärnkraftverk bredvid varandra är att elnätet inte belastas. Det gör totalpriset för elektriciteten blir lägre, samtidigt som det inte tillkommer investeringskostnader för operatören av elnätet.

Vill etablera Sverige som en föregångare

Med detta avtal strävar parterna efter att etablera Sverige som en föregångare i denna globala omställning, genom att utnyttja Studsviks licensierade anläggning, Evrocs digitala infrastruktur och Blykallas avancerade SMR-teknik.

”Detta samarbete är en möjlighet för Sverige att bli ledande inom digital infrastruktur. Det ger oss möjlighet att visa hur små modulära reaktorer kan tillhandahålla den stabila, fossilfria energi som krävs för AI-revolutionen”, säger Jacob Stedman, vd för Blykalla. ”Studsviks anläggning och evrocs ambitioner erbjuder rätt förutsättningar för ett banbrytande projekt.”

Samförståndsavtalet fastställer en ram för samarbete mellan de tre parterna. Målet är att utvärdera den kommersiella och tekniska genomförbarheten av att samlokalisera datacenter och SMR på Studsviks licensierade anläggning, samarbeta med kommuner och markägare samt definiera hur en framtida kommersiell struktur för elköpsavtal skulle kunna se ut.

”Den ständigt växande efterfrågan på AI understryker det akuta behovet av att snabbt bygga ut en massiv hyperskalig AI-infrastruktur. Genom vårt samarbete med Blykalla och Studsvik utforskar vi en modell där Sverige kan ta ledningen i byggandet av en klimatneutral digital infrastruktur”, kommenterar Mattias Åström, grundare och VD för Evroc.

”Studsvik erbjuder en unik plattform med anläggningsinfrastruktur och unik kompetens för att kombinera avancerad kärnkraft med nästa generations industri. Detta samförståndsavtal är ett viktigt steg för att utvärdera hur sådana synergier kan realiseras i Sverige”, kommenterar Karl Thedéen, vd för Studsvik.

Parterna kommer nu att inrätta en gemensam styrgrupp för att utvärdera anläggningen och affärsmodellen, med målet att inleda formella partnerskapsförhandlingar senare i år. Deras fortsatta samarbete ska möjliggöra ren och säker energi för Europas AI-infrastruktur och digitala infrastruktur.

Sveriges regering arrangerade på tisdagen ett toppmöte om framtidens kärnkraft i Östersjöregionen tillsammans med Finland. Ministrar från Polen, Lettland och Estland deltog, liksom investerare, banker och kärnkraftsbolag. EFN:s reporter Thomas Arnroth rapporterar från mötet.

Energi- och näringsminister Ebba Busch betonade att målet är att göra Sverige till regionens ledande kärnkraftsnation och en hub för kärnkraft i Östersjöområdet.

Tanken är att länderna ska samarbeta och se regionen som en gemensam marknad, vilket kan påskynda och sänka kostnaderna för nya reaktorer. Kunskap kan användas gemensamt över hela regionen och en reaktortyp skulle bara behöva godkännas en gång.

Silver spränger den magiska gränsen, kostar nu över 50 USD per uns

Blykalla, Evroc och Studsvik vill bygga kärnkraftsdrivna datacenter i Sverige

Toppmöte om framtidens kärnkraft runt Östersjön hölls idag

Nytt prisrekord, guld stiger över 4000 USD

Goldman Sachs höjer prognosen för guld, tror priset når 4900 USD

Mahvie Minerals i en guldtrend

Volatile but going nowhere. Brent crude circles USD 66 as market weighs surplus vs risk

Aktier i guldbolag laggar priset på guld

Kinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde

Tyskland har så höga elpriser att företag inte har råd att använda elektricitet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMahvie Minerals i en guldtrend

-

Analys4 veckor sedan

Analys4 veckor sedanVolatile but going nowhere. Brent crude circles USD 66 as market weighs surplus vs risk

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAktier i guldbolag laggar priset på guld

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanKinas elproduktion slog nytt rekord i augusti, vilket även kolkraft gjorde

-

Nyheter3 veckor sedan

Tyskland har så höga elpriser att företag inte har råd att använda elektricitet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuld når sin högsta nivå någonsin, nu även justerat för inflation

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDet stigande guldpriset en utmaning för smyckesköpare

-

Analys3 veckor sedan

Brent crude ticks higher on tension, but market structure stays soft