Analys

US shale oil production growth to slow sharply in 2020

Baker Hughes US oil rig count has declined by 178 rigs since the recent peak of 888 rigs in mid-November 2018 with latest count now at 710. If anything the rig count decline has accelerated since July as investors have closed their pockets for debt based production growth with no profit to show for.

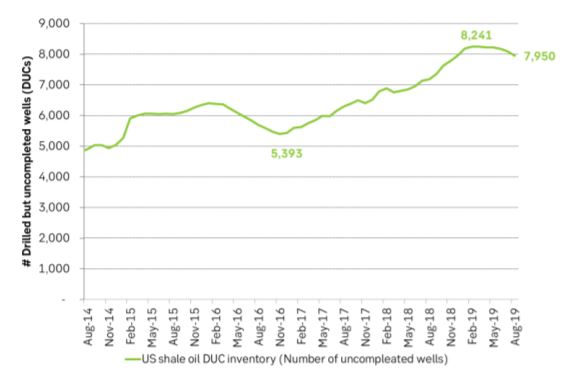

US oil rig count is now drawing down by about 3.5% per month. US shale oil producers are now completing more wells than they are drilling. As a consequence the DUC inventory of Drilled but uncompleted wells which ballooned from 5400 wells in late 2016 to a peak of 8246 in March 2019 has now been drawing down since April and is now drawing down at an accelerating pace.

The more the rig count falls the faster will be the DUC inventory draw-down be as producers work hard to maintain the monthly rate of well completions. In the end producers will have no other choice than to reduce the monthly rate of completed wells or to increase drilling activity and that is the point in time when US shale oil production growth will start to slow sharply. We think that in the end a higher oil price is needed to drive drilling activity higher.

If we assume that the drilling rig count continues to fall by 20 rigs per month to the end of this year and then stabilizes then marginal US shale oil production growth is likely to slow sharply from March 2020 before contracting in September 2020.

The US EIA has a very simplistic method of calculating shale oil drilling productivity. The consequence is that they underestimate productivity in periods when the DUC inventory is growing (Dec-2016 to Mar-2019) and overestimate it when the DUC inventory is declining as it has been doing now since April. As a consequence they also have too high production forecasts when the DUC inventory is drawing down like it is now.

The US EIA is now probably overestimating US oil production for 2020 by some 300 k bl/d with a projection that production will average 13.17 m bl/d in 2020 (US EIA STEO report released yesterday). They did reduce their 2020 US production forecast yesterday from 13.23 m bl/d in their September STEO forecast to 13.17 m bl/d yesterday but they are probably still some 300 k bl/d too high.

US shale oil production is still growing by a marginal, annualized pace of 0.9 m bl/d (75 k bl/d/mth) now in October according to the latest US EIA DPR report in September. Thus the current very strong marginal US production growth still gives a very strong bearish impulse to the global oil market. This bearish impulse is however going to slow sharply from March onwards next year and potentially go to neutral and turn to bullish in September next year.

Year on year production growth in the US is still going to be significant in 2020 due to base effects. The US EIA STEO report yesterday projects a US liquids production growth of 1.56 m bl/d y/y from 2019 to 2020. We think that this is probably in the ball-park some 0.3 m bl/d to high. That still leaves a very strong 1.2 m bl/d y/y average growth in 2020. The monthly production growth and thus marginal bearish impulse to the global oil market is however likely going to slow sharply from March next year. On a Jan-2020 to Jan-2021 basis the US crude oil production is probably not going to increase by more than 100 k bl/d unless drilling picks up.

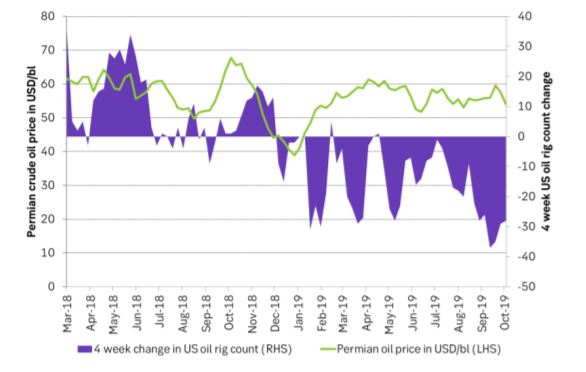

In order to instigate an expansion again in US drilling rig count the shale oil players will need a higher oil price than we have now. The Permian oil price has averaged $56/bl during the oil rig draw-down since January. The WTI price has averaged $57/bl and the 18 month forward WTI price has averaged $55/bl. These prices probably need to move up to $65-70/bl in order to instigate an expansion US shale oil drilling again. Right now we have Permian = $54/bl, WTI 1mth = $53/bl and WTI 18mth = $49.9/bl. I.e. all these prices are today lower than what they have been on average during the rig count draw down since January so further draw down in US oil rig count should be expected.

Ch1: Local Permian oil price in USD/bl versus 4 weeks change in US oil rig count. The Permian oil price has averaged $56/bl during the draw-down phase and probably needs to move up by some $10/bl in order to instigate drilling rig count expansion again. Latest Permian oil price is $54/bl

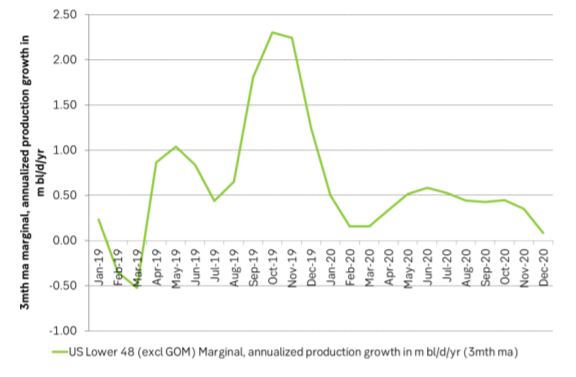

Ch2: The US EIA’s latest STEO report is also forecasting a sharply lower marginal, annualized production growth in US Lower 48 states (excl GOM) which is mostly shale oil production. They are forecasting a marginal, annualized production growth rate of 0.3 m bl/d/yr on average in 2020 versus an average growth rate of 0.84 m bl/d in 2019. Thus the US EIA is also forecasting a sharply slower production growth for US shale next year. However, we do think that their projections are probably too high and needs to be adjusted lower towards zero marginal production growth through 2020.

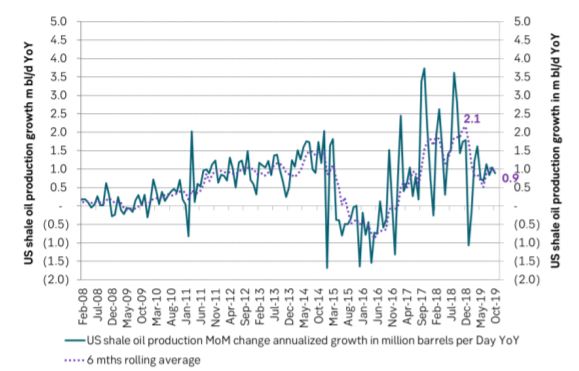

Ch3: US marginal, annualized production growth is still very strong with an annualized growth rate of 0.9 m bl/d according to the US EIA September DPR report. The estimate of 0.9 m bl/d/y for October is probably a bit on the high side. Nonetheless it is in decline. Shale oil players are probably going to start to reduce monthly well completion rates from January onwards as the DUC inventory starts to decline. That will rapidly drive the marginal production growth rate lower

Ch4: The US inventory of DUCs has now been drawing down since April and the draw down is accelerating. It will probably draw down to about 5,500 at around the end of 2020.

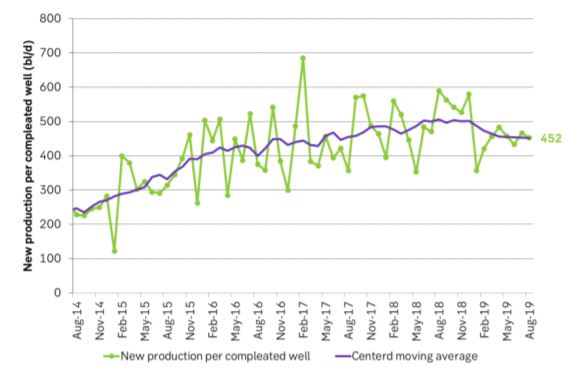

Ch5: US shale oil well productivity has halted its historical relentless productivity growth and has pulled back a little.

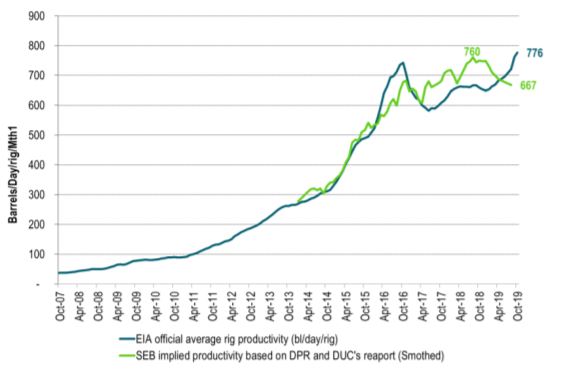

Ch6: Official US EIA drilling rig productivity measure has risen strongly since the end of 2018. In our view this is primarily due to the accelerating draw down in the US DUC inventory which technically is leading to an overestimation in drilling productivity according to the EIA’s methodology of calculating it as [New production at time T]/[Rig count in T-2]. If a significant amount of new production stems for the DUC draw down then production will be high while the rig count number will be low thus leading to an overestimation of the rig productivity

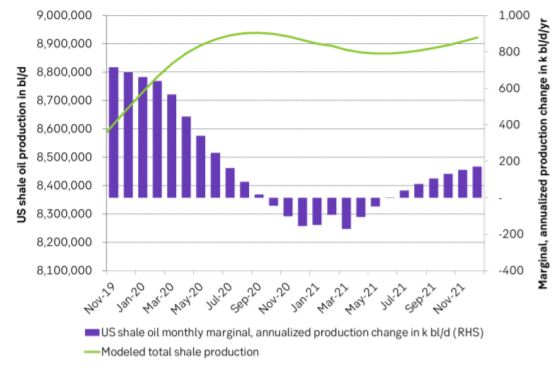

Ch7: US shale oil production is growing strongly but slowing and the slowing will accelerate in March 2020 onwards

Ch8: US production growth is likely to slow sharply in Q2-2020 onwards as well completions are likely to decline along with the declining DUC inventory

Ch9: US oil rig count is falling sharply and the decline seems to accelerate. Completions of shale oil wells per month has managed to hold up due to the DUC inventory but impact is likely to be significant in Q2-2020 leading in the end to lower well completion rates

Oil prices are likely to fall for a fourth straight year as OPEC+ unwinds cuts and retakes market share. We expect Brent crude to average USD 55/b in Q4/25 before OPEC+ steps in to stabilise the market into 2026. Surplus, stock building, oil prices are under pressure with OPEC+ calling the shots as to how rough it wants to play it. We see natural gas prices following parity with oil (except for seasonality) until LNG surplus arrives in late 2026/early 2027.

Oil market: Q4/25 and 2026 will be all about how OPEC+ chooses to play it

OPEC+ is in a process of unwinding voluntary cuts by a sub-group of the members and taking back market share. But the process looks set to be different from 2014-16, as the group doesn’t look likely to blindly lift production to take back market share. The group has stated very explicitly that it can just as well cut production as increase it ahead. While the oil price is unlikely to drop as violently and lasting as in 2014-16, it will likely fall further before the group steps in with fresh cuts to stabilise the price. We expect Brent to fall to USD 55/b in Q4/25 before the group steps in with fresh cuts at the end of the year.

Natural gas market: Winter risk ahead, yet LNG balance to loosen from 2026

The global gas market entered 2025 in a fragile state of balance. European reliance on LNG remains high, with Russian pipeline flows limited to Turkey and Russian LNG constrained by sanctions. Planned NCS maintenance in late summer could trim exports by up to 1.3 TWh/day, pressuring EU storage ahead of winter. Meanwhile, NE Asia accounts for more than 50% of global LNG demand, with China alone nearing a 20% share (~80 mt in 2024). US shale gas production has likely peaked after reaching 104.8 bcf/d, even as LNG export capacity expands rapidly, tightening the US balance. Global supply additions are limited until late 2026, when major US, Qatari and Canadian projects are due to start up. Until then, we expect TTF to average EUR 38/MWh through 2025, before easing as the new supply wave likely arrives in late 2026 and then in 2027.

Price action contained withing USD 2/b last week. Likely muted today as well with US closed. The Brent November contract is the new front-month contract as of today. It traded in a range of USD 66.37-68.49/b and closed the week up a mere 0.4% at USD 67.48/b. US oil inventory data didn’t make much of an impact on the Brent price last week as it is totally normal for US crude stocks to decline 2.4 mb/d this time of year as data showed. This morning Brent is up a meager 0.5% to USD 67.8/b. It is US Labor day today with US markets closed. Today’s price action is likely going to be muted due to that.

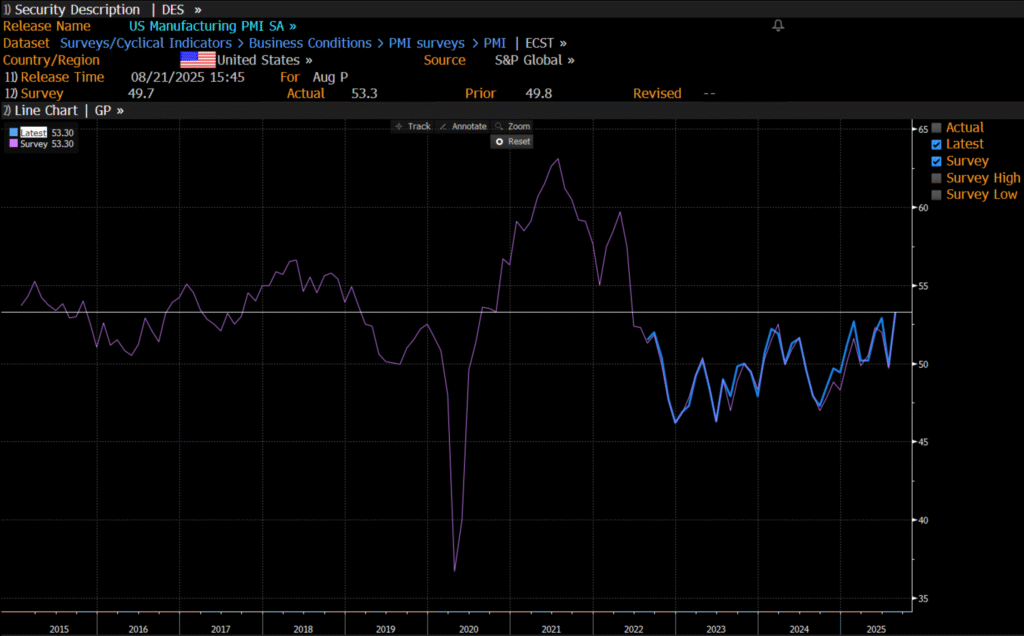

Improving manufacturing readings. China’s manufacturing PMI for August came in at 49.4 versus 49.3 for July. A marginal improvement. The total PMI index ticked up to 50.5 from 50.2 with non-manufacturing also helping it higher. The HCOB Eurozone manufacturing PMI was a disastrous 45.1 last December, but has since then been on a one-way street upwards to its current 50.5 for August. The S&P US manufacturing index jumped to 53.3 in August which was the highest since 2022 (US ISM manufacturing tomorrow). India manufacturing PMI rose further and to 59.3 for August which is the highest since at least 2022.

Are we in for global manufacturing expansion? Would help to explain copper at 10k and resilient oil. JPMorgan global manufacturing index for August is due tomorrow. It was 49.7 in July and has been below the 50-line since February. Looking at the above it looks like a good chance for moving into positive territory for global manufacturing. A copper price of USD 9935/ton, sniffing at the 10k line could be a reflection of that. An oil price holding up fairly well at close to USD 68/b despite the fact that oil balances for Q4-25 and 2026 looks bloated could be another reflection that global manufacturing may be accelerating.

US manufacturing PMI by S&P rose to 53.3 in August. It was published on 21 August, so not at all newly released. But the US ISM manufacturing PMI is due tomorrow and has the potential to follow suite with a strong manufacturing reading.

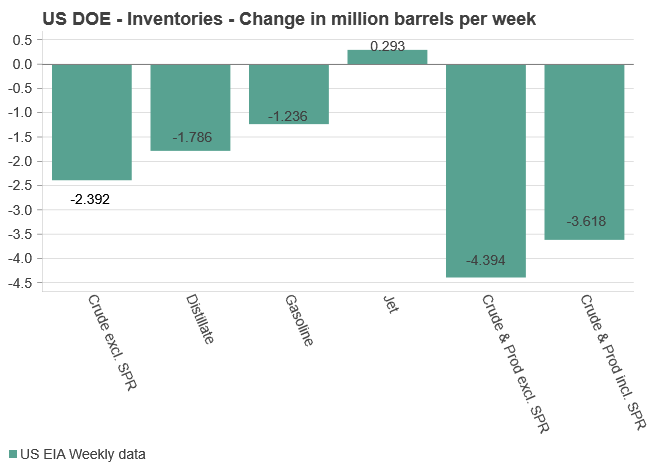

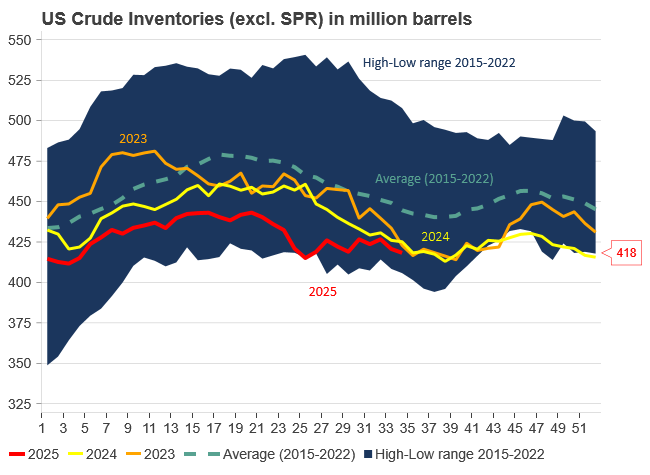

U.S. commercial crude inventories posted another draw last week, falling by 2.4 million barrels to 418.3 million barrels, according to the latest DOE report. Inventories are now 6% below the five-year seasonal average, underlining a persistently tight supply picture as we move into the post-peak demand season.

While the draw was smaller than last week’s 6 million barrel decline, the trend remains consistent with seasonal patterns. Current inventories are still well below the 2015–2022 average of around 449 million barrels.

Gasoline inventories dropped by 1.2 million barrels and are now close to the five-year average. The breakdown showed a modest increase in finished gasoline offset by a decline in blending components – hinting at steady end-user demand.

Diesel inventories saw yet another sharp move, falling by 1.8 million barrels. Stocks are now 15% below the five-year average, pointing to sustained tightness in middle distillates. In fact, diesel remains the most undersupplied segment, with current inventory levels at the very low end of the historical range (see page 3 attached).

Total commercial petroleum inventories – including crude and products but excluding the SPR – fell by 4.4 million barrels on the week, bringing total inventories to approximately 1,259 million barrels. Despite rising refinery utilization at 94.6%, the broader inventory complex remains structurally tight.

On the demand side, the DOE’s ‘products supplied’ metric – a proxy for implied consumption – stayed strong. Total product demand averaged 21.2 million barrels per day over the last four weeks, up 2.5% YoY. Diesel and jet fuel were the standouts, up 7.7% and 1.7%, respectively, while gasoline demand softened slightly, down 1.1% YoY. The figures reflect a still-solid late-summer demand environment, particularly in industrial and freight-related sectors.

Ett samtal om guld, silver, uran, koppar och olja

Guld kostar för första gången någonsin 3600 USD per uns

OPEC+ in a process of retaking market share

Manufacturing PMIs ticking higher lends support to both copper and oil

Ombytliga elpriser på elmarknaden

Omgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

Lundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

Meta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

Guld stiger till över 3500 USD på osäkerhet i världen

What OPEC+ is doing, what it is saying and what we are hearing

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOmgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanLundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMeta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuld stiger till över 3500 USD på osäkerhet i världen

-

Analys3 veckor sedan

What OPEC+ is doing, what it is saying and what we are hearing

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAlkane Resources och Mandalay Resources har gått samman, aktör inom guld och antimon

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanLyten, tillverkare av litium-svavelbatterier, tar över Northvolts tillgångar i Sverige och Tyskland