Analys

US shale oil production growth to slow sharply in 2020

Baker Hughes US oil rig count has declined by 178 rigs since the recent peak of 888 rigs in mid-November 2018 with latest count now at 710. If anything the rig count decline has accelerated since July as investors have closed their pockets for debt based production growth with no profit to show for.

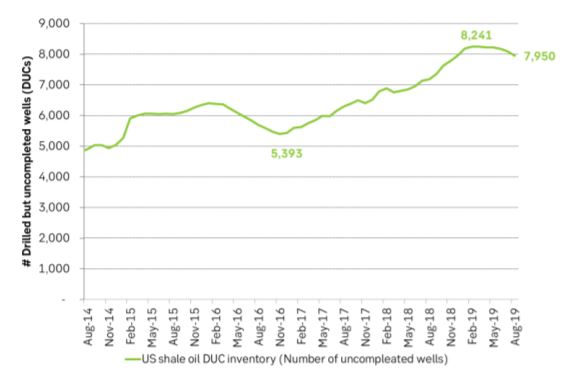

US oil rig count is now drawing down by about 3.5% per month. US shale oil producers are now completing more wells than they are drilling. As a consequence the DUC inventory of Drilled but uncompleted wells which ballooned from 5400 wells in late 2016 to a peak of 8246 in March 2019 has now been drawing down since April and is now drawing down at an accelerating pace.

The more the rig count falls the faster will be the DUC inventory draw-down be as producers work hard to maintain the monthly rate of well completions. In the end producers will have no other choice than to reduce the monthly rate of completed wells or to increase drilling activity and that is the point in time when US shale oil production growth will start to slow sharply. We think that in the end a higher oil price is needed to drive drilling activity higher.

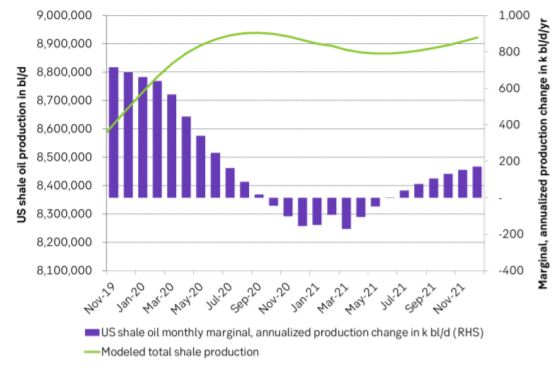

If we assume that the drilling rig count continues to fall by 20 rigs per month to the end of this year and then stabilizes then marginal US shale oil production growth is likely to slow sharply from March 2020 before contracting in September 2020.

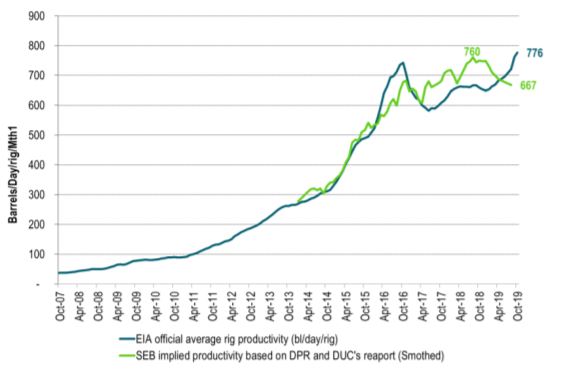

The US EIA has a very simplistic method of calculating shale oil drilling productivity. The consequence is that they underestimate productivity in periods when the DUC inventory is growing (Dec-2016 to Mar-2019) and overestimate it when the DUC inventory is declining as it has been doing now since April. As a consequence they also have too high production forecasts when the DUC inventory is drawing down like it is now.

The US EIA is now probably overestimating US oil production for 2020 by some 300 k bl/d with a projection that production will average 13.17 m bl/d in 2020 (US EIA STEO report released yesterday). They did reduce their 2020 US production forecast yesterday from 13.23 m bl/d in their September STEO forecast to 13.17 m bl/d yesterday but they are probably still some 300 k bl/d too high.

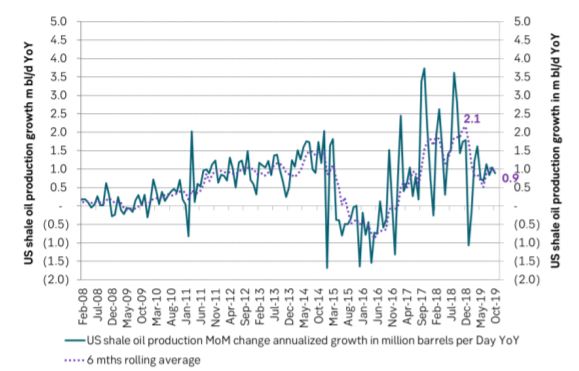

US shale oil production is still growing by a marginal, annualized pace of 0.9 m bl/d (75 k bl/d/mth) now in October according to the latest US EIA DPR report in September. Thus the current very strong marginal US production growth still gives a very strong bearish impulse to the global oil market. This bearish impulse is however going to slow sharply from March onwards next year and potentially go to neutral and turn to bullish in September next year.

Year on year production growth in the US is still going to be significant in 2020 due to base effects. The US EIA STEO report yesterday projects a US liquids production growth of 1.56 m bl/d y/y from 2019 to 2020. We think that this is probably in the ball-park some 0.3 m bl/d to high. That still leaves a very strong 1.2 m bl/d y/y average growth in 2020. The monthly production growth and thus marginal bearish impulse to the global oil market is however likely going to slow sharply from March next year. On a Jan-2020 to Jan-2021 basis the US crude oil production is probably not going to increase by more than 100 k bl/d unless drilling picks up.

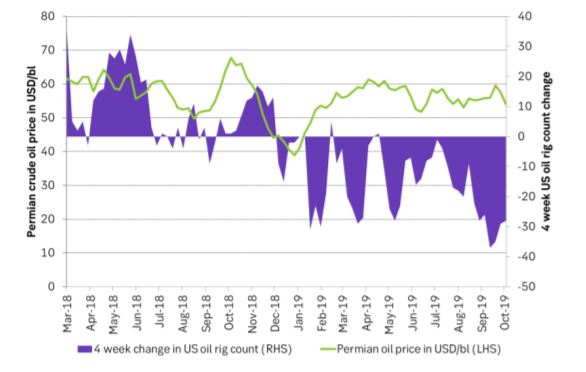

In order to instigate an expansion again in US drilling rig count the shale oil players will need a higher oil price than we have now. The Permian oil price has averaged $56/bl during the oil rig draw-down since January. The WTI price has averaged $57/bl and the 18 month forward WTI price has averaged $55/bl. These prices probably need to move up to $65-70/bl in order to instigate an expansion US shale oil drilling again. Right now we have Permian = $54/bl, WTI 1mth = $53/bl and WTI 18mth = $49.9/bl. I.e. all these prices are today lower than what they have been on average during the rig count draw down since January so further draw down in US oil rig count should be expected.

Ch1: Local Permian oil price in USD/bl versus 4 weeks change in US oil rig count. The Permian oil price has averaged $56/bl during the draw-down phase and probably needs to move up by some $10/bl in order to instigate drilling rig count expansion again. Latest Permian oil price is $54/bl

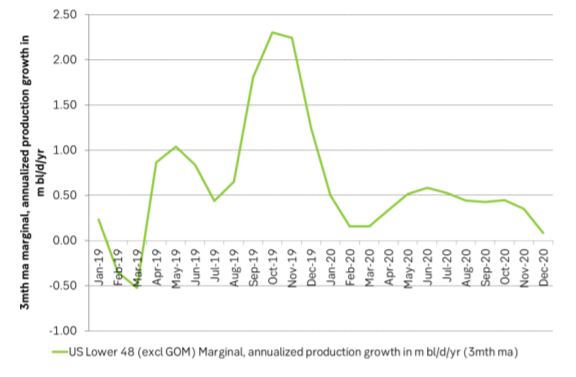

Ch2: The US EIA’s latest STEO report is also forecasting a sharply lower marginal, annualized production growth in US Lower 48 states (excl GOM) which is mostly shale oil production. They are forecasting a marginal, annualized production growth rate of 0.3 m bl/d/yr on average in 2020 versus an average growth rate of 0.84 m bl/d in 2019. Thus the US EIA is also forecasting a sharply slower production growth for US shale next year. However, we do think that their projections are probably too high and needs to be adjusted lower towards zero marginal production growth through 2020.

Ch3: US marginal, annualized production growth is still very strong with an annualized growth rate of 0.9 m bl/d according to the US EIA September DPR report. The estimate of 0.9 m bl/d/y for October is probably a bit on the high side. Nonetheless it is in decline. Shale oil players are probably going to start to reduce monthly well completion rates from January onwards as the DUC inventory starts to decline. That will rapidly drive the marginal production growth rate lower

Ch4: The US inventory of DUCs has now been drawing down since April and the draw down is accelerating. It will probably draw down to about 5,500 at around the end of 2020.

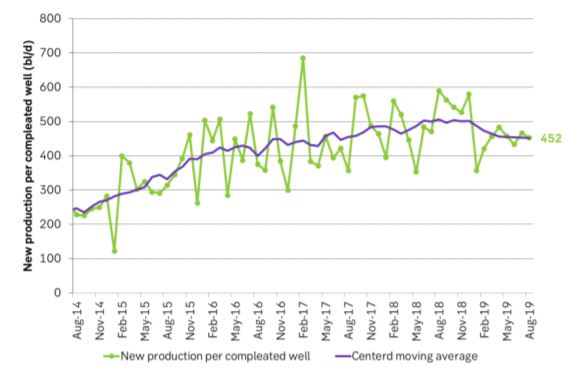

Ch5: US shale oil well productivity has halted its historical relentless productivity growth and has pulled back a little.

Ch6: Official US EIA drilling rig productivity measure has risen strongly since the end of 2018. In our view this is primarily due to the accelerating draw down in the US DUC inventory which technically is leading to an overestimation in drilling productivity according to the EIA’s methodology of calculating it as [New production at time T]/[Rig count in T-2]. If a significant amount of new production stems for the DUC draw down then production will be high while the rig count number will be low thus leading to an overestimation of the rig productivity

Ch7: US shale oil production is growing strongly but slowing and the slowing will accelerate in March 2020 onwards

Ch8: US production growth is likely to slow sharply in Q2-2020 onwards as well completions are likely to decline along with the declining DUC inventory

Ch9: US oil rig count is falling sharply and the decline seems to accelerate. Completions of shale oil wells per month has managed to hold up due to the DUC inventory but impact is likely to be significant in Q2-2020 leading in the end to lower well completion rates