Analys

SEB – Jordbruksprodukter, vecka 26 2012

Inledning

Inledning

Utsikterna för årets skörd har drastiskt försämrats den senaste tiden och därför ändrar vi vår marknadstro till positiv för priserna på en rad grödor. Teknisk analys stödjer detta då vi noterar köpsignaler i flera marknader för grödor som skördas nu under sommaren på norra halvklotet.

Odlingsväder

Southern Oscillation Index, ett mått på intensiteten i graden av La Niña eller El Niño, sjunkit lägre. Aktuell notering är -9.5. Ett värde lägre än -8 innebär El Niño. El Niño är bra för globalt odlingsväder.

Det är däremot torrt i USA och i Ryssland just nu och det är det som påverkar priserna uppåt. Nedan ser vi nederbörden i Nordamerika den senaste veckan. Över stora områden har det inte kommit något regn alls.

Nedan ser vi avvikelsen från normal nederbörd för områden i Europa som är relevanta för höstvete.

Källa: Martell Crop projections

Källa: Martell Crop projections

Vete

Matifvetet med novemberleverans gjorde ett nytt kliv uppåt från det tekniska stödet på ca 204 – 205 euros nivå. Vid 230 euro, där priset vände ner för ett år sedan, finns ett motstånd.

Nedan ser vi Chicagovetet med leverans i december. Priset har skjutit iväg upp över motståndslinjen och vi har nu en köpsignal. Möjligen kommer en rekyl nedåt och då ska man nog tolka det som ett köptillfälle.

Nedan ser vi hur terminspriserna på Matif och Chicago förändrats den senaste veckan. Det har varit mycket stora förändringar, uppåt. Matif är nu den blå kurvan. Den har gått ännu mer in i backwardation. Chicago är nu den oranga kurvan. Dess contango har minskat och för september 1014 är det till och med lite backwardation. Alla priser är så klart angivna i euro per ton. Vi ser också för övrigt att priserna för leverans i närtid har gått ihop mellan Chicago och Matif.

Som vi skrev om i förra veckans marknadsbrev så uppgår FAO’s senaste prognos för den globala vete produktionen 2012 till 680 mt, vilket är ca 5 mt högre än för en månad sedan, till följd av ökade estimat för Kina och Indien. Den första officiella prognosen i maj för den totala vete produktionen i USA, som baseras på tillståndet för höstvete och estimat för vårgrödorna, pekar på en högre produktion än vad som tidigare har uppskattats. Dessa uppjusteringar uppvägde mer än väl för nedjusteringar i Europa, däribland några EU-länder men i synnerhet för Ryssland.

Kommentarerna i bilden nedan hänvisar till situationen i juni:

Enligt den nya prognosen, skulle den globala vete produktionen minska med ca 3 procent jämfört med förra året, men fortfarande ligga långt över genomsnittet för de senaste fem åren. Produktionen av vete kvarstår som ett förhållandevis attraktivt alternativ för producenter i världen under 2012, som en följd av höga priser. Ogynnsamma väderförhållanden har dock skadat höstgrödorna i vissa större vete producerande områden och den genomsnittliga avkastningen beräknas bli lägre än förra årets rekord nivåer.

Enligt den nya prognosen, skulle den globala vete produktionen minska med ca 3 procent jämfört med förra året, men fortfarande ligga långt över genomsnittet för de senaste fem åren. Produktionen av vete kvarstår som ett förhållandevis attraktivt alternativ för producenter i världen under 2012, som en följd av höga priser. Ogynnsamma väderförhållanden har dock skadat höstgrödorna i vissa större vete producerande områden och den genomsnittliga avkastningen beräknas bli lägre än förra årets rekord nivåer.

I Nordamerika visar de senaste indikationerna på en stark återhämtning från 2011 och reflekterar ökad sådd och generellt bättre väderförhållanden, som bör leda till högre avkastning, särskilt i de områden som drabbades av torka förra året. I Kanada visar de senaste prognoserna på en ökad produktion genom en ökning av sådd areal under våren i kombination med goda väderförhållanden.

Årets produktion av vete inom EU har äventyrats av en sträng vinter i många delar och prognosen för en genomsnittlig avkastning kan komma att försämras ytterligare om inte tillräckligt med regn kommer snart och lindrar torkan i de centrala EU-länderna, framförallt Ungern och Slovakien. I slutet av maj beräknades EU:s totala vete produktion 2012 att uppgå till 133 mt, en minskning med 3.6 procent jämfört med förra året.

I Ryssland pekar de senaste indikationerna på en 4 procentig minskning av vete produktionen till 54 mt. Mer regn behövs i de södra delarna, i annat fall riskerar avkastningen att sjunka under nuvarande estimerade nivåer.

En kraftig nedgång i produktionen av vete förväntas i Ukraina, framförallt som en följd av ogynnsamma väderförhållanden denna säsong. Genom kraftigt minskad skördad areal och lägre avkastning beräknas produktionen uppgå till 14 mt, vilket är 40 procent lägre än förra årets rekordskörd och långt under genomsnittet för de senaste fem åren.

I Asien är man i slutskedet av 2012 års skörd och de senaste estimaten pekar på en rekordproduktion på 239 mt för Fjärran Östern, en ökning med 2.5 procent från förra årets höga nivåer. Rekordskördar av vete i Kina och Indien återspeglar höga priser för producenterna i kombination med gynnsamma förhållanden och tillräcklig tillförsel av vatten, gödning mm. I den asiatiska delen av OSS så förväntas vete produktionen i Kazakstan att minska kraftigt med ungefär en tredjedel från förra året till 14.7 mt på grund av lägre odlad areal tillsammans med torrt väder och höga temperaturer.

I Mellanöstern, bedöms den sammanlagda veteskörden att uppgå till 44 mt, en minskning med ca 5 procent från förra året. I Nordafrika kvarstår utsikterna som blandade, med sämre prognoser för Marocko där torka har minskat avkastningspotentialen kraftigt, medan det ser bättre ut i Algeriet och Tunisien.

På det södra halvklotet, pågår sådden av höstgrödor i vissa delar av Australien men regn behövs i de nordöstra och östra områdena innan man kan börja. Tidiga indikationer pekar på en minskad vete areal efter förra årets höga nivå, och avkastningen förväntas återgå till genomsnittliga nivåer. I och med det beräknas produktionen preliminärt att sjunka med nästan 12 procent till 26 mt.

I Sydamerika pågår sådden av vete i de flesta länderna och tidiga prognoser pekar på en minskning med 7 procent från förra årets nivå till följd av lägre odlad areal hos de största producenterna, Argentina, Brasilien och Uruguay, där lantbrukare föredrar mer lönsamma grödor.

Strategie Grains, har justerat upp sin prognos för Europas grödor, och höjer sitt estimat för produktionen av vete med 1.5 mt till 124.2 mt som en följd av gynnsamt väder. Revideringen inkluderar högre estimat för Frankrike (+900 000 ton), Tyskland (+500 000 ton), Litauen, (+300 000 ton) och Bulgarien (+300 000 ton), något som uppväger för nedjusteringar i Polen och Rumänien med 300 000 ton för respektive. Beroende på framtida väderförhållanden kan avkastningsprognosen fortfarande öka för länder i de västra och norra delarna av EU, och ytterligare regn kan också generera högra avkastningsprognoser för länder som Tjeckien, Slovakien och Ungern. Prognosen för durumvete höjdes också med 300 000 ton till 7.9 mt, efter rapporter om god kvalitet på i Spanien och södra Italien där skörden har börjat. Export av vete 2012/13 beräknas uppgå till 13.5 mt, en ökning med 2 mt, som en följd av förbättrad produktion samt högre konkurrenskraft gentemot export av amerikanskt vete.

Utsikterna för Rysslands spannmålsskörd justeras ned till följd av ogynnsamma väderförhållanden. Vädret, som fortfarande är varmt och torrt i många regioner, får analysfirman SovEcon att justera ned sin prognos, för andra gången på en månad, från 88.5 mt till 85 mt. Landets produktion av vete justeras ned med 3 mt till 50 mt. Rysslands jordbruksminister justerar också ner sin uppskattning av landets spannmålsproduktion med nästan 10% från 94 mt till 85 mt. Produktionen av vete justeras ned till 46-49 mt, mot tidigare 57 mt och jämfört med USDA’s prognos på 53 mt. Jordbruksministern gjorde ett uttalande häromdagen att det inte finns någon anledning för marknaden att oroa sig för ett ryskt exportstopp. Det är klart han säger det, eftersom det ser ut som det borde komma ett. Efter justeringen av skörden återstår bara 30 mt för inhemsk konsumtion och det brukar alltid konsumeras 38 mt. CNGOIC uppskattar Kinas vete produktion 2012 till 118 mt, en marginell ökning med 0.07% från 2011, men 2.3 mt lägre än deras tidigare prognos från maj och även 2 mt under USDA’s estimat. Produktionen av höstvete beräknas till 111.7 mt mot tidigare 114 mt.

ABARES har justerat ned sin prognos för landets vete produktion 2012/13 med 1.6 mt från tidigare estimat till 24.1 mt, vilket innebär en minskning med 18.3% från förra årets rekordskörd och den lägsta skörden på tre år. Minskningen beror på lägre spannmålspriser som får lantbrukare att avstå från sådd och istället ägna sig åt boskap (får), i kombination med torrt väder under april och maj som försenade sådden.

Den senaste tidens regn har varit gynnsamma men ytterligare nederbörd behövs för att underlätta sådden och grödornas tillväxt för att uppnå genomsnittlig avkastning.

USDA’s estimat från förra tisdagens WASDE-rapport låg kvar på 26 mt för Australien. Arealen för vete har justerats ned med 347 000 hektar till 13.4 miljoner hektar, medan prognosen för landets export av vete har reviderats ned med 500 000 ton till 20.5 mt jämfört med förra årets 22.3 mt.

Buenos Aires Grain Exchange estimerar Argentinas vete areal 2012/13 till 3.8 miljoner hektar, en minskning med 17% från 2011/12, och en fjärdedel av sådden är klar vid det här laget. Argentinas regering har godkänt export av 6 miljoner ton vete under 2012/13. Landet, är världens sjätte största vete exportör och en viktig leverantör till grannlandet Brasilien, men under de senaste åren har lantbrukarna producerat mindre vete som en protest mot regerings export kvotsystem. Det inhemska behovet av vete uppskattas till 6.5 miljoner ton, vilket tyder på att regeringen förväntar sig en skörd på minst 12.5 miljoner ton i år.

USDA sänkte global skörd med 5 mt i junis WASDE och med det väder som varit nu och de rapporter som kommit från olika producentländer, borde julis WASDE innehålla ytterligare en sänkning med 5 mt. Det innebär att skörden ligger 30 mt under förra årets och torkan El Niño, som är positivt för Sydamerika, lär påverka Australien med torka, där det redan är torrt, under hösten.

Maltkorn

Novemberkontraktet på maltkorn har vaknat ur sin slummer och stigit över det prisintervall novemberkontraktet etablerat under våren. Det finns möjligheter för priset att söka sig högre, eventuellt efter en kortare rekyl efter den snabba prisuppgången.

Strategie Grains höjer sin prognos för Europas produktion av korn med 500 000 ton till 53.2 mt, vilket är en ökning med 3% från förra årets 51.6 mt. ABARES justerar ned sitt estimat för Australiens produktion av korn med 1.7 mt från tidigare prognos till 7.3 mt som en följd av lägre förväntad sådd och avkastning.

Potatis

Potatispriset för leverans nästa år, som i slutet av maj var uppe på 17 euro per deciton och sedan såldes ner till 14, tycks vara på väg uppåt igen. Trenden är alltjämt uppåtriktad och vi tror att priset kommer att gå upp.

Majs

Priset på decembermajs bröt den sjunkande trenden, passerade genom 550 cent och stängde ”limit up” ett par dagar i rad. Bakom prisrörelsen ligger den torka och värme som slagit till i USA just när majsen är i pollineringsfas. USDA skar ner crop ratings så att de ligger 10 enheter (good/excellent) under förra årets nivå. Samtidigt har USDA prognosticerat skörden med en avkastning som ligger 19 bushels per acre över förra årets. Nu har USDA väntat sig utgående lager nästa år om 1.88 miljoner bushels, men justerar vi avkastning per acre så att den bättre stämmer med crop ratings hamnar vi på en skörd som är 1.7 miljoner bushels lägre, vilket betyder att det är nära nollan i utgående lager. Vi tar naturligtvis både den ändrade fundamentala situationen och den tekniska styrkan till oss och ändrar vår vy till positiv för priset. På fredag kommer Stocks report från USDA.

Produktionen av majs i Europa beräknas uppgå till 66 mt, upp 400 000 ton sedan förra månaden, och är nästan i linje med förra årets produktion på 66.2 mt enligt Strategie Grains.

Regn under andra hälften av maj har gynnat Brasiliens majsgrödor och 2011/12 års skörd av majs som vintergröda (safrinha) ser mycket bra ut enligt Agroconsult, och beräknas uppgå till 38.8 mt (en ökning med 84% från förra året). Med den siffran beräknas den totala skörden av majs till rekordhöga 73.7 mt , 15 mt mer än det tidigare rekordet som sattes 2007/08 och en bra bit över USDA’s nuvarande prognos på 69 mt.

Buenos Aires Grain Exchange estimerar landets produktion av majs 2012 till 19.3 mt, och 67% procent av skörden är avklarad jämfört med 64.4% för en vecka sedan.

Rosario Grain Exchanges prognos på en produktion om 19 mt är oförändrad från förra månaden.

CNGOIC uppskattar Kinas produktion av majs 2012 till 197.5 mt, oförändrad från tidigare estimat och en uppjustering med 3% från 2011. Prognosen ligger 2.5 mt över USDA’s senaste uppskattning.

Sojabönor

Sojabönorna med novemberleverans bröt oväntat 14 dollar. Det är en stark köpsignal och vi har nu också ett starkt stöd i just 14 dollar.

Buenos Aires Grain Exchange estimerar landets produktion av sojabönor 2011/12 till 39.9 mt, och 96.8% av skörden ör avklarad jämfört med 95% för en vecka sedan.

Rosario Grain Exchange justerar ned sin prognos för Argentinas produktion 2011/12 med 400 000 ton till 40.5 mt. CNGOIC’s senaste prognos för Kinas produktion av sojabönor 2012 är oförändrad och uppgår till 13.0 mt, en minskning med 7.14% från 2011.

ABIOVE uppskattar Brasiliens produktion av sojabönor 2011/12 till 66.2 mt, en ökning från 65.9 mt i april och högre än USDA’s senaste prognos på 65.5 mt. På grund av att den brasilianska valutan, realen, faller, noterar nu det kontantavräknade kontraktet på BM&F i Sao Paulo all-time-high. Nedan ser vi priserna på BM&F angivna i dollar per säck. Pga de höga priserna har bönderna redan säkrat 31% av vinterns kommande skörd. Vanligtvis är det ingen som ens börjat säkra så här års. Liksom med Matif-vetet hösten 2010, där lantbrukarna var snabba med att prissäkra i början på prisuppgången, redan i september, kan det bli brist på osåld vara längre fram på säsongen, som kan få priset att fortsätta stiga.

Raps

Priset på novemberterminen befinner har stigit upp till motståndet på 480 euro per ton. Om 480 euro per ton bryts är det möjligt att vi får se nya kontraktshögsta därefter. Helst skulle vi vilja se att 485.50 bryts som är tidigare kontraktshögsta från den 10 april.

Torka i Australiens östra delar påverkar prognoserna för landet canola produktion, men en ökad canola areal gör att ABARES justerat upp sin prognos för produktionen av canola till 2.94 mt från tidigare 2.93 mt.

AOF (Australian Oilseeds Federation) höjer samtidgt sin prognos för landets canola skörd i år med 231 000 ton till 3.20 mt. Revideringen görs efter en omvärdering av odlingsarealen för canola i New South Wales (NSW), i kombination med att välbehövligt regn i många distrikt har höjt prognosen för areal och avkastning betydligt jämfört med förra månaden.

CNGOIC’s uppskattar Kinas rapsproduktion 2012 till 12.8 mt, ner 4.66% från 2011.

Gris

Decemberkontraktet fortsätter att rekylera nedåt, men ligger nu på låga nivåer, där det bör finnas intresserade köpare.

Mjölk

Mjölkpriset fortsätter sin uppgång från början på maj. Nu ligger priset återigen på toppnivåer. Och gissningsvis finns det en del säljare kvar på den här nivån sedan förra gången priset var uppe här.

[box]SEB Veckobrev Jordbruksprodukter är producerat av SEB Merchant Banking och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Disclaimer

The information in this document has been compiled by SEB Merchant Banking, a division within Skandinaviska Enskilda Banken AB (publ) (“SEB”).

Opinions contained in this report represent the bank’s present opinion only and are subject to change without notice. All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, expressed or implied, is made with respect to the completeness or accuracy of its contents and the information is not to be relied upon as authoritative. Anyone considering taking actions based upon the content of this document is urged to base his or her investment decisions upon such investigations as he or she deems necessary. This document is being provided as information only, and no specific actions are being solicited as a result of it; to the extent permitted by law, no liability whatsoever is accepted for any direct or consequential loss arising from use of this document or its contents.

About SEB

SEB is a public company incorporated in Stockholm, Sweden, with limited liability. It is a participant at major Nordic and other European Regulated Markets and Multilateral Trading Facilities (as well as some non-European equivalent markets) for trading in financial instruments, such as markets operated by NASDAQ OMX, NYSE Euronext, London Stock Exchange, Deutsche Börse, Swiss Exchanges, Turquoise and Chi-X. SEB is authorized and regulated by Finansinspektionen in Sweden; it is authorized and subject to limited regulation by the Financial Services Authority for the conduct of designated investment business in the UK, and is subject to the provisions of relevant regulators in all other jurisdictions where SEB conducts operations. SEB Merchant Banking. All rights reserved.

Down on Friday. Up on Monday. The Brent June crude oil contract traded down 5.1% last week to a close of $90.38/b. It reached a high of $103.87/b last Monday and a low of $86.09/b on Friday as Iran announced that the Strait of Hormuz was fully open for transit. That quickly changed over the weekend as the US upheld its blockade of Iranian oil exports while Iran naturally responded by closing the SoH again. The US blew a hole in the engine room of the Iranian ship TOUSKA and took custody of the ship on Sunday. Brent crude is up 5.6% this morning to $95.4/b.

The cease-fire is expiring tomorrow. The US has said it will send a delegation for a second round of negotiations in Islamabad in Pakistan. But Iran has for now rejected a second round of talks as it views US demands as unrealistic and excessive while the US is also blocking the Strait of Hormuz.

While Brent is up 5% this morning, the financial market is still very optimistic that progress will be made. That talks will continue and that the SoH will fully open by the start of May which is consistent with a rest-of-year average Brent crude oil price of around $90/b with the market now trading that balance at around $88/b.

Financial optimism vs. physical deterioration. We have a divergence where the financial market is trading negotiations, improvements and resolution while at the same time the physical market is deteriorating day by day. Physical oil flows remain constrained by disrupted flows, longer voyage times and elevated freight and insurance costs.

Financial markets are betting that a US/Iranian resolution will save us in time from violent shortages down the road. But every day that the SoH remains closed is bringing us closer to a potentially very painful point of shortages and much higher prices.

The US blockade is also a weapon of leverage against its European and Asian allies. When Iran closed the SoH it held the world economy as a hostage against the US. The US blockade of the SoH is of course blocking Iranian oil exports. But it is also an action of disruption directed towards Europe and Asia. The US has called for the rest of the world to engaged in the war with Iran: ”If you want oil from the Persian Gulf, then go and get it”. A risk is that the US plays brinkmanship with the global oil market directed towards its European and Asian allies and maybe even towards China to force them to engage and take part. Maybe unthinkable. But unthinkable has become the norm with Trump in the White House.

Wild moves yesterday. Brent crude traded to a high of $114.43/b and a low of $96.0/b and closed at $99.94/b yesterday.

US – Iran negotiations ongoing or not? What a day. Donald Trump announced that good talks were ongoing between Iran and the US and that the 48 hour deadline before bombing Iranian power plants and energy infrastructure was postponed by five days subject to success of ongoing meetings. Iranian media meanwhile stated that no meetings were ongoing at all.

Today we are scratching our heads trying to figure out what yesterday was all about.

Friends and family playing the market? Was it just Trump and his friends and family who were playing with oil and equity markets with $580m and $1.46bn in bets being placed by someone in oil and equity markets just 15 minutes before Trump’s announcement?

Was Trump pulling a TACO as he reached his political and economic pain point: Brent at $112/b, US Gas at $4/gal, SPX below 200dma and US 10yr above 4.4%?

Different Iranian factions with Trump talking with one of them? Are there real negotiations going on but with the US talking to one faction in Iran while another, the hardliners, are not involved and are denying any such negotiations going on?

Extending the ultimatum to attack and invade Kharg island next weekend? Or, is the five day delay of the deadline a tactical decision to allow US amphibious assault ships and marines to arrive in the Gulf in the upcoming weekend while US and Israeli continues to degrade Iranian military targets till then. And then next weekend a move by the US/Israel to attack and conquer for example the Kharg island?

We do not really know which it is or maybe a combination of these.

We did get some kind of TACO ydy. But markets have been waiting for some kind of TACO to happen and yesterday we got some kind of TACO. And Brent crude is now trading at $101.5/b as a result rather than at $112-114/b as it did no the high yesterday.

But what really matters in our view is the political situation on the ground in Iran. Will hardliners continue to hold power or will a more pragmatic faction gain power?

If the hardliners remain in power then oil pain should extend all the way to US midterm elections. The hardliners were apparently still in charge as of last week. Iran immediately retaliated and damaged LNG infrastructure in Qatar after Israel hit Iranian South Pars. The SoH was still closed and all messages coming out of Iran indicated defiance. Hardliners continues in power has a huge consequence for oil prices going forward. The regime has played its ’oil-weapon’ (closing or chocking the Strait of Hormuz). It is using it to achieve political goals. Deterrence: it needs to be so politically and economically expensive to attack Iran that it won’t happen again in the future. Or at least that the US/Israel thinks 10-times over before they attack again. The highest Brent crude oil closing price since the start of the war is $112.19/b last Friday. In comparison the 20-year inflation adjusted Brent price is $103/b. So Brent crude last Friday at $112.19/b isn’t a shockingly high price. And it is still far below the nominal high of $148/b from 2008 which is $220/b if inflation adjusted. So once in a lifetime Iran activates its most powerful weapon. The oil weapon. It needs to show the power of this weapon and it needs to reap political gains. Getting Brent to $112/b and intraday high of $119.5/b (9 March) isn’t a display of the power of that weapon. And it is not a deterrence against future attacks.

So if the hardliners remain in power in Iran, then the SoH will likely remain chocked all the way to US midterm elections and Brent crude will at a minimum go above the historical nominal high of $148/b from 2008.

Thus the outlook for the oil price for the rest of the year doesn’t depend all that much of whether Trump pulls a TACO or not. Stops bombing or not. It depends more on who is in charge in Iran. If it is the hardliners, then deterrence against future attacks via chocking of the SoH and high oil prices is the likely line of action. It is impacting the world but the Iranian ’oil-weapon’ is directed towards the US president and the the US midterm elections.

If a pragmatic faction gets to power in Iran, then a very prosperous future is possible. However, if power is shifting towards a more pragmatic faction in Iran then a completely different direction could evolve. Such a faction could possibly be open for cooperation with the US and the GCC and possibly put its issues versus Israel aside. Then the prosperity we have seen evolving in Dubai could be a possible future also for Iran.

So far it looks like the hardliners are fully in charge. As far as we can see, the hardliners are still fully in control in Iran. That points towards continued chocking of the SoH and oil prices ticking higher as global inventories (the oil market buffers) are drawn lower. And not just for a few more weeks, but possibly all the way to the US midterm elections.

A brief sigh of relief yesterday as oil infra at Kharg wasn’t damaged. But higher today. Brent crude dabbled around a bit yesterday in relief that oil infrastructure at Iran’s Kharg island wasn’t damaged. It traded briefly below the 100-line and in a range of $99.54 – 106.5/b. Its close was near the low at $100.21/b.

No easy victorious way out for Trump. So no end in sight yet. Brent is up 3.2% today to $103.4/b with no signs that the war will end anytime soon. Trump has no easy way to declare victory and mission accomplished as long as Iran is in full control of the Strait of Hormuz while also holding some 440 kg of uranium enriched to 60% and not far from weapons grade at 90%. As long as these two factors are unresolved it is difficult for Trump to pull out of the Middle East. Naturally he gets increasingly frustrated over the situation as the oil price and US retail gas prices keeps ticking higher while the US is tied into the mess in the Middle East. Trying to drag NATO members into his mess but not much luck there.

When commodity prices spike they spike 2x, 3x, 4x or 5x. Supply and demand for commodities are notoriously inflexible. When either of them shifts sharply, the the price can easily go to zero (April 2022) or multiply 2x, 3x, or even 5x of normal. Examples in case cobalt in 2025 where Kongo restricted supply and the price doubled. Global LNG in 2022 where the price went 5x normal for the full year average. Demand for tungsten in ammunition is up strongly along with full war in the middle east. And its price? Up 537%.

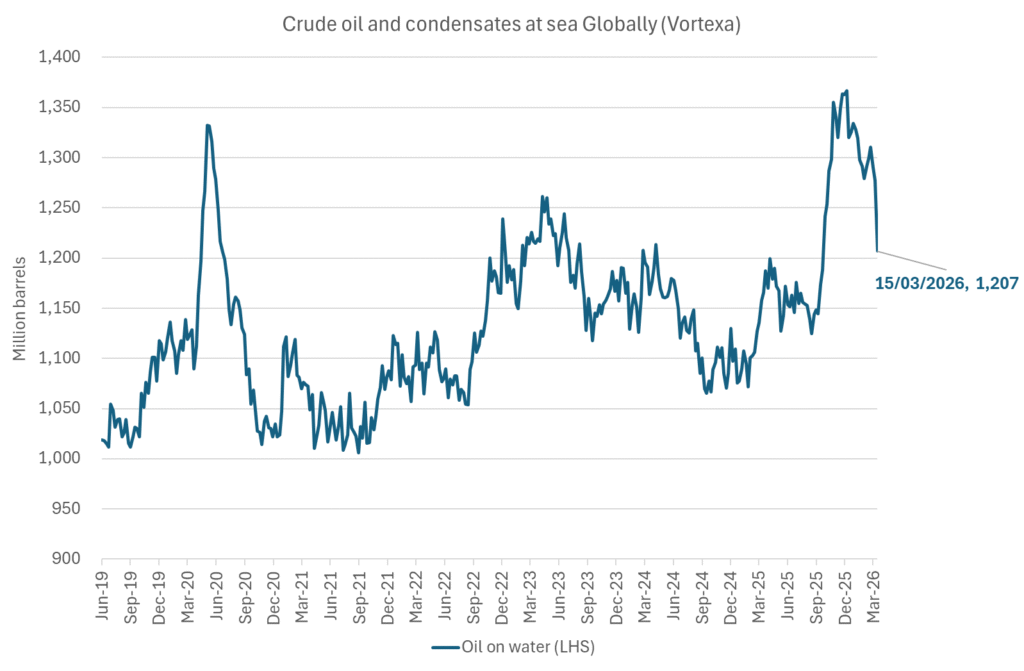

Why hasn’t the Brent crude oil price gone 2x, 3x, 4x or 5x versus its normal of $68/b given close to full stop in the flow of oil of the Strait of Hormuz? We are after all talking about close to 20% of global supply being disrupted. The reason is the buffers. It is fairly easy to store oil. Commercial operators only hold stocks for logistical variations. It is a lot of oil in commercial stocks, but that is predominantly because the whole oil system is so huge. In addition we have Strategic Petroleum Reserves (SPRs) of close to 2500 mb of crude and 1000 mb of oil products. The IEA last week decided to release 400 mb from global SPR. Equal to 20 days of full closure of the Strait of Hormuz. Thus oil in commercial stocks on land, commercial oil in transit at sea and release of oil from SPRs is currently buffering the situation.

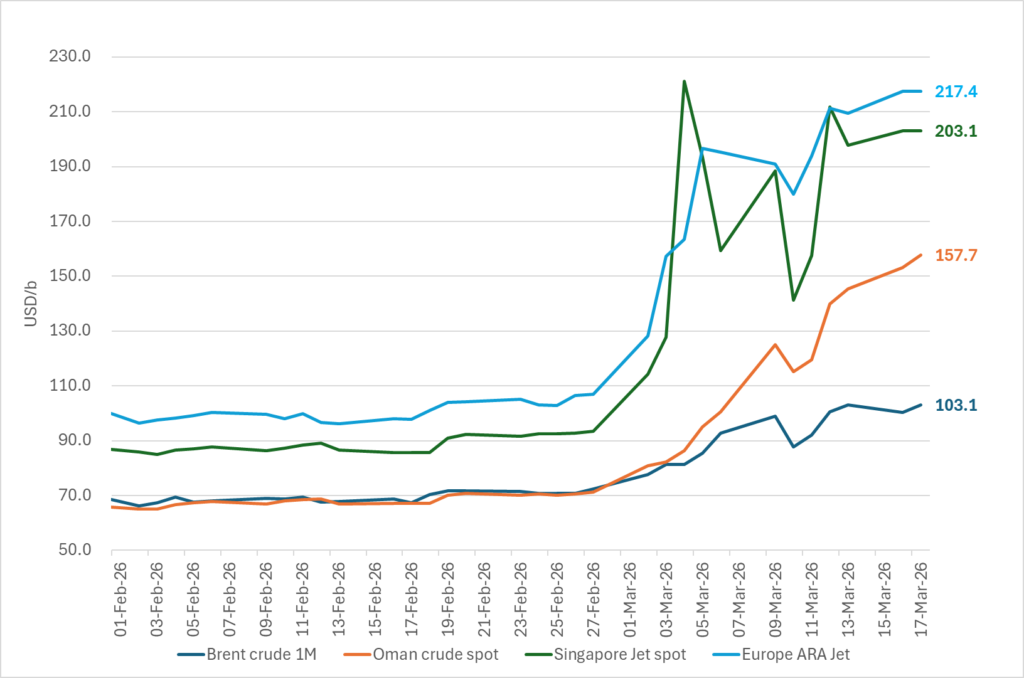

But we are running the buffers down day by day. As a result we see gradually increasing stress here and there in the global oil market. Asia is feeling the pinch the most. It has very low self sufficiency of oil and most of the exports from the Gulf normally head to Asia. Availability of propane and butane many places in India (LPG) has dried up very quickly. Local prices have tripled as a result. Local availability of crude, bunker oil, fuel oil, jet fuel, naphtha and other oil products is quickly running down to critical levels many places in Asia with prices shooting up. Oman crude oil is marked at $153/b. Jet fuel in Singapore is marked at $191/b.

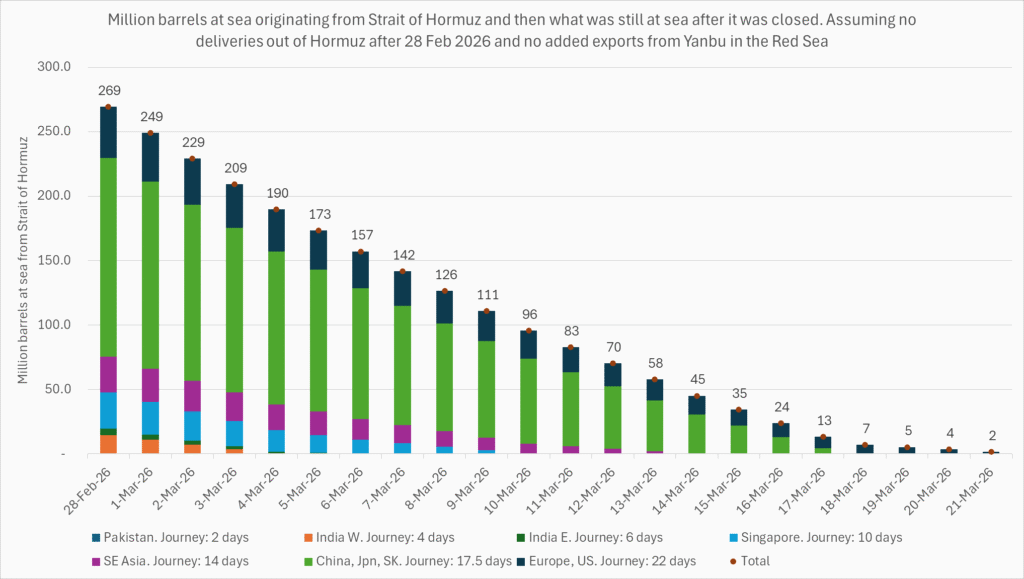

Oil at sea originating from Strait of Hormuz from before 28 Feb is rapidly emptied. Oil at sea is a large pool of commercial oil. An inventory of oil in constant move. If we assume that the average journey from the Persian Gulf to its destinations has a volume weighted average of 13.5 days then the amount of oil at sea originating from the Persian Gulf when the the US/Israel attacked on 28 Feb was 13.5 days * 20 mb/d = 269 mb. Since the strait closed, this oil has increasingly been delivered at its destinations. Those closest to the Strait, like Pakistan, felt the emptying of this supply chain the fastest. Propane prices shooting to 3x normal there already last week and restaurants serving cold food this week is a result of that. Some 50-60% of Asia’s imports of Naphtha normally originates from the Persian Gulf. So naphtha is a natural pain point for Asia. The Gulf also a large and important exporter of Jet fuel. That shut in has lifted jet prices above $200/b.

To simplify our calculations we assume that no oil has left the Strait since that date and that there is no increase in Saudi exports from Yanbu. Then the draining of this inventory at sea originated from the Persian Gulf will essentially look like this:

The supply chain of oil at sea originating from the Strait of Hormuz is soon empty. Except for oil allowed through the Strait of Hormuz by Iran and increased exports from Yanbu in the Red Sea. Not included here.

Oil at sea is falling fast as oil is delivered without any new refill in the Persian Gulf. Waivers for Russian crude is also shifting Russian crude to consumers. Brent crude will likely start to feel the pinch much more forcefully when oil at sea is drawn down another 200 mb to around 1000 mb. That is not much more than 10 days from here.

Oil and oil products are starting to become very pricy many places. Brent crude has still been shielded from spiking like the others.

Market Still Betting on Timely Resolution, But Each Day Raises Shortage Risk

Christian Kopfer om läget för oljan

Marknaden måste börja betrakta de höga kopparpriserna som det nya normala

Det fysiska spotpriset på brentolja har slagit nytt rekord

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

Elpriserna fördubblas, stor osäkerhet inför sommaren

MP Materials, USA:s svar på Kinas dominans över sällsynta jordartsmetaller

Det fysiska spotpriset på brentolja har slagit nytt rekord

Studsvik har idag ansökt om att få bygga 1200-1600 MW kärnkraft i Valdemarsvik

-

Nyheter3 veckor sedan

Nyheter3 veckor sedan40 minuter med Javier Blas om hur världen verkligen påverkas av energikrisen

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanElpriserna fördubblas, stor osäkerhet inför sommaren

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMP Materials, USA:s svar på Kinas dominans över sällsynta jordartsmetaller

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanDet fysiska spotpriset på brentolja har slagit nytt rekord

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanStudsvik har idag ansökt om att få bygga 1200-1600 MW kärnkraft i Valdemarsvik

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMarknaden måste börja betrakta de höga kopparpriserna som det nya normala

-

Analys4 veckor sedan

TACO (or Whatever It Was) Sends Oil Lower — Iran Keeps Choking Hormuz

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMatproduktion är beroende av gödsel, Gulfkriget skapar brist