Analys

SEB Jordbruksprodukter, 6 september 2012

Det har varit en händelsefattig vecka. Priserna har rört sig ”sidledes” till stor del. Nästa vecka släpper USDA WASDE-rapporten för september och det lär vara en flau marknad till dess. Den 4 september meddelade den tyska terminsbörsen EUREX att man startar handel i vasslepulver. Handeln startar den 28 september. Terminskontrakten avser 5 ton, dvs samma storlek som de tidigare terminskontrakten på smör och skummjölkspulver. Underliggande index, som terminerna avräknas kontant mot, är

Det har varit en händelsefattig vecka. Priserna har rört sig ”sidledes” till stor del. Nästa vecka släpper USDA WASDE-rapporten för september och det lär vara en flau marknad till dess. Den 4 september meddelade den tyska terminsbörsen EUREX att man startar handel i vasslepulver. Handeln startar den 28 september. Terminskontrakten avser 5 ton, dvs samma storlek som de tidigare terminskontrakten på smör och skummjölkspulver. Underliggande index, som terminerna avräknas kontant mot, är  ”European Whey Powder Index”, som publiceras av Agrarmarkt Informations- Gesellschaft GmbH, i Bonn. De befintliga terminskontrakten på smör och skummjölkspulver noterades i maj 2010. Samtidigt ökar nu EUREX antal terminskontrakt som går att handla. Det kommer att finnas terminskontrakt för varje månad de närmaste sex månaderna. Därutöver kommer det att finnas terminskontrakt för varje kvartal med cykeln januari, april, juli och oktober.

”European Whey Powder Index”, som publiceras av Agrarmarkt Informations- Gesellschaft GmbH, i Bonn. De befintliga terminskontrakten på smör och skummjölkspulver noterades i maj 2010. Samtidigt ökar nu EUREX antal terminskontrakt som går att handla. Det kommer att finnas terminskontrakt för varje månad de närmaste sex månaderna. Därutöver kommer det att finnas terminskontrakt för varje kvartal med cykeln januari, april, juli och oktober.

Odlingsväder

ENSO fortsätter att surfa på gränsen till ett riktigt El Niño. SOI ligger nu på -4.7, men låg förra veckan på – 9.1. Gränsen för El Niño ligger på -8. Klimatmodeller prognostiserar att ENSO kommer att fortsätta ligga på gränsen fram till slutet av året eller in i början på 2013, för att sedan återgå till normala ENSO-förhållanden.

Kanada är helt utan nederbörd den här veckan och skörden fortskrider snabbt. Europa har också varmare och torrare väder än normalt – utom här i norra Europa. Kina har just fått en tyfon, förra veckan och har fått mer regn än normalt. Monsunen i Indien fortsätter att förbättras. Indien har nu skörd nummer två på gång och den gynnas. Vi skrev förra veckan att den förbättrade monsunen har fått läget att ljusna för grödor som majs, ris och sojabönor. Arealen sådd med ris har ökat till 32.9 miljoner hektar från 30.8 förra året. Förra årets skörd var rekordhöga 91.5 mt, enligt det indiska jordbruksministeriet.

Argentina har god nederbörd över alla väsentliga odlingsområden. Parana i södra Brasilien, där vete odlas, har också fått del av den här nederbörden. Däremot är det torrt i typiska sojaområden i centrala och norra Brasilien. Region Centro-Oeste har fått 50% av normal nederbörd. Nedanför ser vi en ögonblicksbild av vädret där.

Med utsikter om att El Niño blir ganska mild, alltså med ett ENSO som ligger på ”nästan” El Niño, kan nederbörden i Brasilien och Argentina bli mindre än vad vi trodde under våren, när det såg ut att bli en starkare El Niño. Australien har ytterst lite nederbörd – vilket är i enlighet med vad som vanligtvis sker vid ett El Niño.

Vete

Tekniskt har Matif:s novemberkontrakt fortsatt att röra sig ”sidledes” och vi tror fortfarande att nästa större rörelse blir uppåt. Den som vill ta en position redan nu, köper terminen och lägger en stop-lossorder på 258 euro. Den som placerar på lite längre sikt kan lägga stoppen på 253.90. Kursen ligger i skrivande stund på 261.50.

Det börjar ju dra ihop sig till att byta år, och då kan det vara bra att se kursutvecklingen för Matifs november 2013-kontrakt. (Kan kanske också vara ett lämpligt tillfälle att börja handla hos SEB?) Priset för nästa års skörd har som vi ser inte rört sig sidledes som november 2012, utan segat sig uppåt.

den 5 september 2012")

Nedan ser vi Chicagovetet med leverans i december. Den tekniska bilden indikerar samma sak här – förestående brott uppåt (förmodligen).

I diagrammet nedan ser vi terminspriserna framåt i tiden för Chicago och Matif och förändringen från 7 dagar sedan. Vi ser att backwardation har minskat i USA. Priset för leverans nästa november (2013) är nästan 20 euro per ton högre i Chicago än i Paris. Förra veckan var det 20 euro. Nu har skillnaden minskat ett par euro.

Nedan ser vi medias intresse för nyckelorden Wheat+Export+Ban. Som vi ser lite mindre intresse och också lite lägre priser. Frågan om exportstopp i Ryssland har mycket stor effekt på priset i den oroliga situation som nu råder.

Det ryska jordbruksministeriet har uppdaterat hektarskördeestimaten och de visar att hektarskörden för vete är 32% lägre än förra året. Det innebär en skörd av vete på ca 38 mt. Hektarskörden för spannmål inklusive majs är, enligt det ryska jordbruksministeriet, 27% lägre än förra året. Minns att vi i det här brevet för ca en månad sedan gjorde kalkylen 94 x 0.7 = 66 mt. 94 mt var förra årets skörd. 27% lägre skörd blir 68.6 mt. Detta är lägre än vad ministermötet i fredags resulterade i, en sänkning från 75 mt till 70. Vi har skrivit att vi tror att 70 mt är en allt för optimistisk siffra och att den kommer att följas av ytterligare nedjusteringar vid följande ministermöten. Samtidigt sänks exportpotentialen, tror vi. Det kommer en GASC-tender för novemberleverans. Om de accepterar några erbjudanden på ryskt vete eller inte, kommer att säga en hel del om hur det egentligen står till med rysk export. Sådden av höstvete i Ryssland rapporterades vara avklarad till 15%.

Vi nämnde under ”odlingsväder” att El Niño gör det torrt i Australien. Västra Australien har fått ungefär hälften av normal nederbörd. Vetet sätter ax just nu och börjar skördas i oktober. Så lite regn är naturligtvis inte bra för skördens storlek. Vi har även vad gäller Australien gjort egna El Niño-baserade beräkningar och kommit fram till att skörden ”borde” bli lägre än de 26 mt som USDA förutspådde i senaste WASDE-rapporten. Det ”borde” komma en nedjustering i WASDE-rapporten nästa vecka.

Maltkorn

Novemberkontraktet på maltkorn har funnit stöd och ser ur teknisk synvinkel ut att kunna stiga den närmaste tiden. Det är samma vy som förra veckan. Ingen förändring.

Potatis

Potatispriset tycks stabilisera sig mellan 20 och 24 euro per deciton. Det återstår att se om det är en konsolidering inför ytterligare prisuppgång över 24 euro, eller en toppformation i väntan på att se vad som händer med konsumtionen.

Majs

Vi skrev förra veckan, att ett brott nedåt inte skulle vara bra och skulle innebära att vi skulle gå ur alla positioner och rentav kanske gå kort. Nu har priset faktiskt i skrivande stund gått under stödlinjen i triangelformationen och det är en klart negativ signal.

Nedan ser vi terminskurvan framåt i tiden för majs. Vi ser att de korta kontrakten har fallit. De längre har stigit.

Måndagens crop ratings för majs var kom in med 22% i good/excellent condition, vilket är på samma nivå som förra veckan. 41% är moget. Förra året så här års var det bara 15% som var moget. 10% är skördat. Förra året var det 3%.

Sojabönor

Priset steg som väntat upp från den lilla konsolideringen i veckan som gått sedan förra veckobrevet. Den teoretiska målkursen enligt skolboken i teknisk analys ligger på 1879 cent / bu. Uppgången verkar förlora kraft och övertygelse, vilket är naturligt när det börjar närma sig målkursen. Trenden uppåt är bruten, men det är möjligt att det kommer in mer säljare vid de här nivåerna på 1800 cent.

Crop conditions var oförändrade från förra veckan. 30% är i good eller very good condition, med 38% är i poor eller very poor condition. 9% har tappat löven; det är långt över genomsnittet för de senaste fem åren, som ligger på 5%.

Brasiliens skörd ligger åtskilliga månader framåt i tiden och när det nu är torrare än normalt i sojadistrikten, framförallt i region Centro-Oeste, kan vädret där få en stor effekt. Det är viktigt att det regnar i september och framförallt i oktober för att det ska bli en god skörd. Världen behöver en rekordskörd från Brasilien efter årets missväxt i USA.

Raps

Ett brott uppåt rycker allt närmare, när trycket ökar i marknaden. Att det finns övertygade säljare på 520- nivån är dock helt klart och det kan också komma ett brott nedåt. Nästa stöd finns då på 490 euro. Man kan fortsätta ligga lång (osäkrad) och behålla en stop-loss-order på en nivå under 55-dagars glidande medelvärde. Det är det medelvärde som är inritat i nedanstående diagram.

Gris

Grispriset befinner sig i en tydlig bear market. Men tycks ha kommit till en konsolideringsfas. 70 cent per pund ser ut att vara golvet på konsolideringsområdet.

Mjölk

Priset på mjölkpulver i Nordeuropa ligger på samma prisnivå som förra veckan. Det är den första veckan sedan juli när priset inte har stigit. Priset på smör har däremot gått upp från 3150 euro per ton till 3300 euro per ton.

Nedan ser vi priset på smör, också oktoberkontraktet såsom handlat på EUREX. Priset är angivet i euro per ton.

På den amerikanska börsen CME i Chicago har priset faktiskt gått ner något för decemberleverans, som vi ser i diagrammet nedan. Priset har ändå gått upp med nästan 30% sedan bottenoteringen i maj månad.

Vad säger då marknaden just nu om priserna för leverans av mjölk i USA i framtiden? Nedan ser vi terminspriserna som kurva som de ser ut idag och hur de såg ut för 7 dagar sedan.

Vi rapporterade även i inledningen av brevet att EUREX noterar terminskontrakt på vasslepulver nu i september. Det händer onekligen mycket på mjölkmarknaden just nu.

Socker

Priset på socker, som handlades ett tag kring 20 cent, började i måndags falla igen. Det ser ut som om bottennoteringen på 18.86 cent som noterades den 4 juni ska testas igen.

EURSEK

EURSEK fortsatte som vi trodde förra veckan upp mot 8.50. Prisuppgången har fått mer och mer kraft. Kanske kommer den här uppgången att gå ända till 8.55 kr per euro.

USDSEK

Dollarn har svarat på supportområdet och hoppat upp från det. Stödet ligger vid 6.60 kr. Priset kan i första hand gå upp till 6.80. Kraften i uppgången tyder på att det kan komma en lite kraftigare uppgångsfas.

[box]SEB Veckobrev Jordbruksprodukter är producerat av SEB Merchant Banking och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Disclaimer

The information in this document has been compiled by SEB Merchant Banking, a division within Skandinaviska Enskilda Banken AB (publ) (“SEB”).

Opinions contained in this report represent the bank’s present opinion only and are subject to change without notice. All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, expressed or implied, is made with respect to the completeness or accuracy of its contents and the information is not to be relied upon as authoritative. Anyone considering taking actions based upon the content of this document is urged to base his or her investment decisions upon such investigations as he or she deems necessary. This document is being provided as information only, and no specific actions are being solicited as a result of it; to the extent permitted by law, no liability whatsoever is accepted for any direct or consequential loss arising from use of this document or its contents.

About SEB

SEB is a public company incorporated in Stockholm, Sweden, with limited liability. It is a participant at major Nordic and other European Regulated Markets and Multilateral Trading Facilities (as well as some non-European equivalent markets) for trading in financial instruments, such as markets operated by NASDAQ OMX, NYSE Euronext, London Stock Exchange, Deutsche Börse, Swiss Exchanges, Turquoise and Chi-X. SEB is authorized and regulated by Finansinspektionen in Sweden; it is authorized and subject to limited regulation by the Financial Services Authority for the conduct of designated investment business in the UK, and is subject to the provisions of relevant regulators in all other jurisdictions where SEB conducts operations. SEB Merchant Banking. All rights reserved.

Brent M1 moving below the 200 dma of $78.7/b. Brent crude continued its move lower yesterday with a decline of 3.3% to $77.9/b. This morning it is adding another drop of 1.4% to $76.8/b. Israel bombing Lebanon during the weekend was a violence of the MoU and Iran was quick to declare the SoH closed again. But the willingness to move forward by both the US and Iran obviously trumped the bombing in Lebanon making the event more of a hiccup on the road of further negotiations.

The US has now waived sanctions against Iranian oil exports for two months allowing Iran to sell its oil all over the world, though sanctions instated in Europe will take more time to unwind. Oil from Iran, Russia as well as Venezuela can for the time being be sold across the world without any sharp discount due to sanctions. Chinese Tea-pot refineries will suffer as they previously could buy rebated crude while selling products at market prices.

Crude oil is no flowing out of the SoH with latest number close to 7 mb/d on a three day moving average. That is still well below the 14 mb/d of crude and 6 mb/d of products normally flowing out of the SoH. Latest estimate is that there is around 80 mb of crude on water inside the Persian Gulf and maybe another 80 mb of oil products on water as well. If crude is exiting the SoH at a rate of around 7 mb/d, then the 80 mb of crude would be depleted within 10-15 days and there after the flow would rely on new crude tankers entering, loading and then exiting the SoH to continue further flows. Given the uncertainties surrounding the status of the SoH with Iran stating that it was closed again as recent as this weekend, there is likely an asymmetry here where ships and oil stranded in the SoH for months are much more eager to exit than new ships are eager to enter.

For now Brent crude keeps falling like a rock with the front-end Brent contract now only trading at a premium of $7.6/b above the five year contract. Quickly heading towards parity. The Brent M1 contract has now broken below its 200 dma of $78.7/b and is closing in on the Fibo-level at $74.7/b. Below that there is not much more supporting levels to be found before $73/b which would close the gap from February 3.

Brent crude M1 technical levels

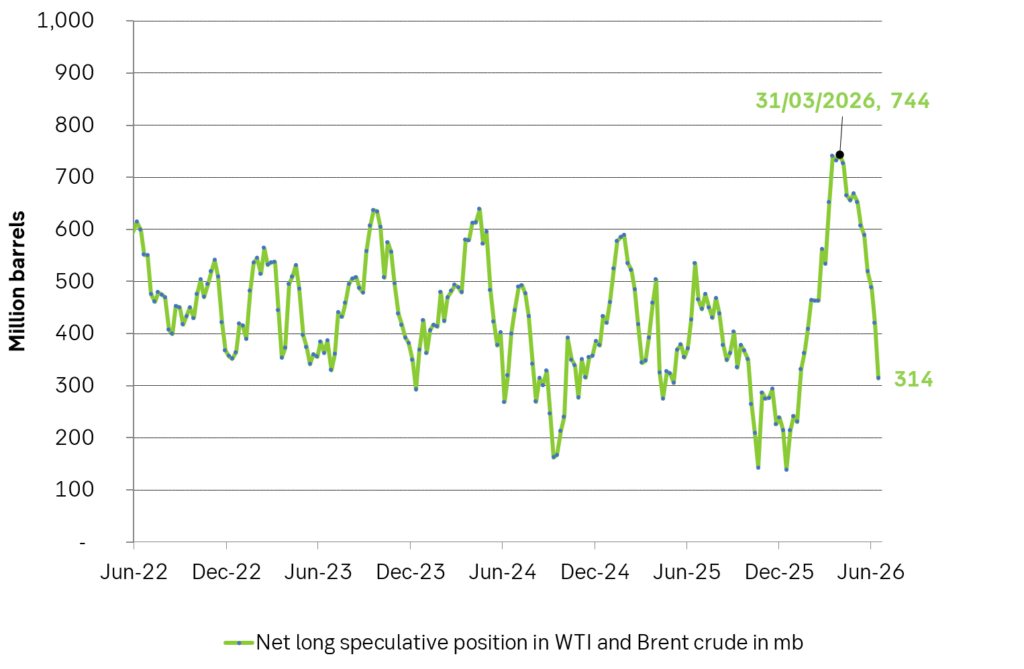

Net long speculative positions are also falling like a rock and as of Tuesday last week the net long positioning in Brent and WTI together summed to 314 million barrels and falling fast.

Will there be a rebound? A possible combination could be an exhaustion of the oil blob caught within the SoH within 1-2 weeks if exits continue at current rate while new ships entering are much more cautious, more Israeli bombardments in Lebanon as Netanyahu fights for re-election, a temporary closure of the SoH again while speculative short positions take cover buying back and covering their positions.

US and Israeli stands versus Iran could harden beyond elections so 2027 surplus is far from given. But Iran and the US are all in all moving towards a set of solutions with both clearly eager to reopen the SoH and keep it open. And that is what the market is pricing along with sharply falling prices. The ongoing discussions will likely take months and last beyond both the upcoming Israeli election (before 27 oct) and the US midterm elections on 3 Nov. Beyond those dates the stance by both Israel and the US may harden again versus Iran. But Iran knows that and is most likely preparing for such a hardening turn. Thus a surplus of oil and global oil stock rebuilding in 2027 (as now is mostly projected) is far from given.

Selling down on a ”deal”. Brent crude fell 6.2% last week with accelerated weakness towards the end of the week. Close of the week at $87.33/b and low of the week (and on Friday) of $85.8/b. Brent is falling another 4% this morning to $83.7/b on confirmation by Iran that a MoU text has been reached and that it will be signed on Friday this week.

So what is this ”deal” worth? Talk on the desk here this morning is that it is much like ”putting lipstick on a pig” where Trump has to sell this at home as a victory where ”the SoH has reopened”, the nuclear issue will be ironed out over the coming 60 days (or maybe 600 days?) and US consumers are getting a lower gasoline price and maybe US republicans survives the midterm elections.

The importance for Iran is that it emerges as the defacto winner of this war in the eyes of the non-US public world. That Iran now onwards is the ”ruler of the SoH” (combo of geography and new weapons systems like drones) or more softer: ”the guarantor of safe passage through the SoH”.

Iran doesn’t need nuclear weapons any more. Nuclear deterrence doesn’t work any more. Ukraine has made many attacks deep into Russia without being nuked in return. Plenty of Iranian ballistic rockets blasts over Israel but Iran wasn’t nuked in return.

There is no trust between the US and Iran. We don’t know all the details yet of the MoU. But what we do know is that there is no trust between the US and Iran what so ever. This is probably more like a descriptive text on how they can cooperate in a way where both sides keeps tactical leverage. Neither side makes irreversible concessions. Violations can be punished quickly. Cooperation produces immediate benefits.

This is a fragile structure. It can easily break down. There may be details which cannot be overcome. To be seen on Friday. The US has to show that it is willing put enough force behind managing and restraining Israel versus Hezbollah in Lebanon. We have seen that Netanyahu hasn’t listened all that much to Trump’s directives and wishes. This could be a major obstacle.

A gradual reopening is tactically preferable for Iran. A tactical leverage for Iran right now is that global oil stocks have been drawn down towards painful and increasingly dangerous levels with increasing risks for oil price spikes in mid-July to August. This together with US midterm elections on 3 November gives tactical leverage to Iran. Iran probably doesn’t want to fully give up on that leverage. A rapid, full reopening where global stocks are able to refill over the coming 60 days will significantly erode that leverage. If Iran reinstates a closure of the SoH after 60 days (if talks break down again), then the effect won’t be that impactful in terms of prices and the US midterm elections.

So a gradual and partial reopening where global markets gets the oil they need while they are unable to rebuild stocks could be a practical middle way for both parties. Trump can sell it as ”the SoH has reopened” and get affordable gasoline for US consumers. Iran can sell it as ”the SoH has fully reopened, but there is some friction” so flow is only 60-80% of normal.

Not much real demand destruction below $100/b. What we do know is that there is not much real price pain demand destruction for oil globally at an oil price below $100/b. A lot of demand-shock destruction. Fear. But demand should now come roaring back towards normal with fear for exceptionally high prices now is rapidly receding.

Sudden China demand destruction due to EVs? Bullocks. EV share of total Chinese carpool now around 13%. Share of new sales of EVs has reached 50%. This is a very gradual process. It doesn’t make oil demand fall like a rock over night. When EV new sales share reaches 100%, then the gasoline car pool will contract by some 5-10% per year. But that is only gasoline. Sudden reduction in Chinese oil demand is more about shock and risk.

Chinese crude oil imports will come roaring back. At what price? Today’s ”neutral” oil price is $70/b. That is the five year price which has steadily traded around the $70/b mark over the past 3-4 years. With still a risky picture one would think that China and the rest of the world will be big buyers of oil in the range of $70-85/b.

Global demand will likely snap back towards normal, forecasted demand and growth at such prices.

Physical reopening is a gradual process. The physical and practical reopening of the SoH will likely be gradual rather than sudden. And that probably suites Iran tactically as well.

Brent M1 price versus the Brent 5-yr (today’s ”normal” price)

Market is starting to take US/Iran headlines with a pinch of salt. Brent crude rose $2.8/b yesterday to an official close of $112.1/b. But after that it traded as low as $108.05/b before ending late night at around $109.7/b. Through the day it traded in a range of $106.87 – 112.72/b amid a flurry of news or rumors from Iran and the US. ”US temporary sanctions during negotiations” (falls alarm). ”We will bomb Iran” (not anyhow),… etc. While the market is still fluctuating to this kind of news flow, it is starting to take such headlines with a pinch of salt.

We’ll see. Maybe, maybe not. The Brent M1 contract is trading at $110.2/b this morning which very close to the average ticks through yesterday of $110.4/b.

Trump with bearish, verbal intervention whenever Brent trades above $110/b it seems. What seems to be a pattern is that Trump states something like ”very good negotiations going on with Iran”, ”New leaders in Iran are great,..”, ”Great progress in negotiations,…”, ”Deal in sight,..” etc whenever the Brent M1 contract trades above $110/b. An effort to cool the market. These hot air verbal interventions from Trump used to have a heavy bearish impact on prices, but they now seems to have less and less effect unless they are backed by reality.

As far as we can see there has been no real progress in the negotiations between the US and Iran with both sides still standing by their previous demands.

Iran is getting stronger while the cease fire lasts making a return to war for Trump yet harder. Iran is naturally in constant preparation for a return to war given Trump’s steady threats of bombing Iran again. Iran is naturally doing what ever is possible to prepare for a return to war. And every day the cease fire lasts it is better prepared. This naturally makes it more and more difficult and dangerous for the US to return to warring activity versus Iran as the consequences for energy infrastructure in the Persian Gulf will be more and more severe the longer the cease fire lasts. Israel seems to see it this way as well. That the war is not won and that current frozen state of a cease fire gives Iran opportunity to rebuild military and politically.

Global inventories are drawing down day by day. How much? In the meantime the Strait of Hormuz stays closed. There is varying measures and estimates of how much global inventories are drawing down. Our rough estimate, back of the envelope, is that global inventories are drawing down by at least some 10 mb/d or about 300 mb/d in a balance between loss of supply versus demand destruction. Other estimates we see are a monthly draw of 250-270 mb/d. The IEA only ’measured’ a draw in global observable stocks of 117 mb in April with oil on water rising 53 mb while on shore stocks fell 170 mb. But global stocks are hard to measure with large invisible, unmeasured stocks. As such a back of the envelope approach may be better.

Oil products is what the world is consuming. Oil product prices likely to rise while product stocks fall. Strategic Petroleum Reserves (SPR) are predominantly crude oil. Discharging oil from OECD SPR stocks, a sharp reduction in Chinese crude imports and a reduction in global refinery throughput of 6-7 mb/d has helped to keep crude oil markets satisfactorily supplied. But global inventories are drawing down none the less. And oil products is really what the world is consuming. So if global refinery throughput stays subdued, then demand will eventually have to match the supply of oil products. The likely path forward this summer is a steady draw down in jet fuel, diesel and gasoline. Higher prices for these. Then, if possible, higher refinery throughput and higher usage of crude in response to very profitable refinery margins. And lastly sharper draw in crude stocks and higher prices for these. But some 6 mb/d of oil products used to be exported through the Strait of Hormuz. And it may not be so easy to ramp up refinery activity across the world to compensate. Especially as Ukraine continues to damage Russian refineries as well as Russian crude production and export facilities.

Watch oil product stocks and prices as well as Brent calendar 2027. What to watch for this summer is thus oil product inventories falling and oil product premiums to crude rising. Another measure to watch is the Brent crude 2027 contract as it rises steadily day by day as the Strait of Hormuz stays closed and global oil inventories decline. The latter is close to the highest level since the start of the war and keeps rising.

The Brent M1 contract and the Brent 2027 prices and current price of jet fuel in Europe (ARA). All in USD/b

Our back of the envelope calculation of the global shortage created by the closure of the Strait of Hormuz. Note that 3.5 mb/d of discharge from SPR is also a draw. Note also that ’Forced demand loss’ of 2.5 mb/d is probably temporary and will fall back towards zero as logistics are sorted out leaving ’Price demand loss’ to do the job of balancing the market. Thus a shortfall of at least 9 mb/d created by the closure. More if SPR discharge is included and more if Forced demand loss recedes.

Brent falling like a rock with oil likely to flow from SoH until at least 3 November

Vattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

Selling down on a ”deal”

Sommarväder skapar prisrally på elbörsen

Oil product price pain is set to rise as the Strait of Hormuz stays closed into summer

Sommarväder skapar prisrally på elbörsen

Vattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

Selling down on a ”deal”

Brent falling like a rock with oil likely to flow from SoH until at least 3 November

-

Nyheter3 veckor sedan

Sommarväder skapar prisrally på elbörsen

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanVattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

-

Analys1 vecka sedan

Selling down on a ”deal”

-

Analys8 timmar sedan

Brent falling like a rock with oil likely to flow from SoH until at least 3 November