Analys

SEB Jordbruksprodukter, 6 maj 2013

USA var kallt och vått förra veckan, med frost och snö på många håll, ända nere i Texas. I torsdags fick norra Mellanvästern 35 cm snö. Höstvetets kondition försämrades i måndagens rapport från 35% ”good” och ”excellent condition” till 33% (redan innan förra veckans snö och frost). Sådden av majs ökade med bara 1% till veckan innan förra veckan, till rekordlåga 5%. Antagligen har väldigt lite blivit sått i veckan som gick. Det får vi facit på i kväll. Sojabönor har ännu inte kommit igång med sådden. Allt annat lika bör en allt för stor försening av majssådden leda till att sojabönor vinner areal.

USA var kallt och vått förra veckan, med frost och snö på många håll, ända nere i Texas. I torsdags fick norra Mellanvästern 35 cm snö. Höstvetets kondition försämrades i måndagens rapport från 35% ”good” och ”excellent condition” till 33% (redan innan förra veckans snö och frost). Sådden av majs ökade med bara 1% till veckan innan förra veckan, till rekordlåga 5%. Antagligen har väldigt lite blivit sått i veckan som gick. Det får vi facit på i kväll. Sojabönor har ännu inte kommit igång med sådden. Allt annat lika bör en allt för stor försening av majssådden leda till att sojabönor vinner areal.

WASDE-rapporten kommer på fredag och nästa veckas brev kommer därför att innehålla en genomgång av den.

WASDE-rapporten kommer på fredag och nästa veckas brev kommer därför att innehålla en genomgång av den.

Den som vill lyssna på en tvåtimmars genomgång av WASDE-rapporten, och hur man analyserar marknaden samt placerar framgångsrikt i marknaden genom certifikat, är välkommen till ett seminarium hos SEB i Malmö.

Odlingsväder

USA var kallt och vått med frost och snö ända nere i Texas. 35 cm snö föll i torsdags över norra Mellanvästern. Kanada var varmare och torrare. I Europa var det lite nederbörd i norr, men desto mer på den södra halvan av kontinenten. Australien var huvudsakligen fortsatt torrt.

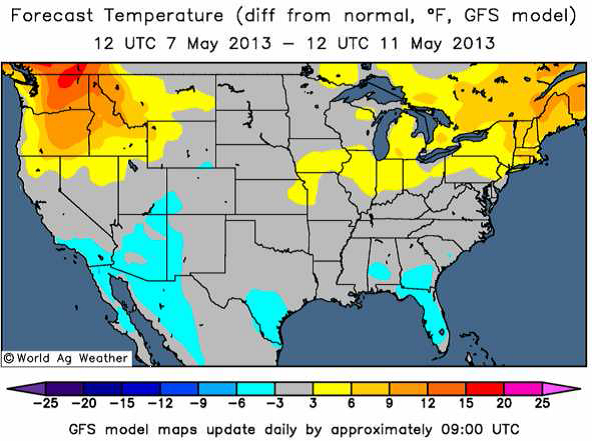

Nedan ser vi prognostiserad avvikelse från normal temperatur i USA.

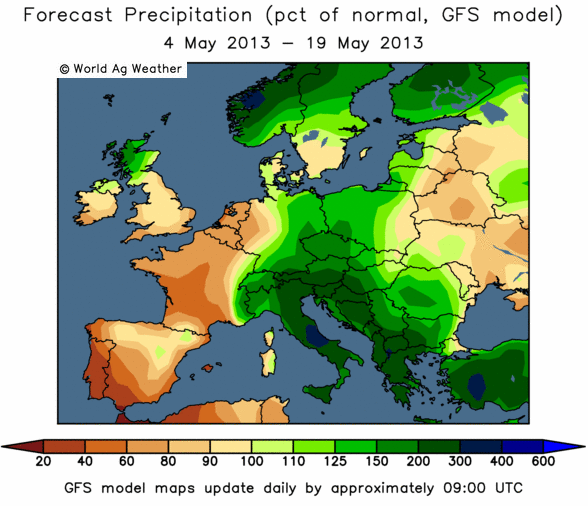

Nedan ser vi prognostiserad avvikelse från normal nederbörd i Europa.

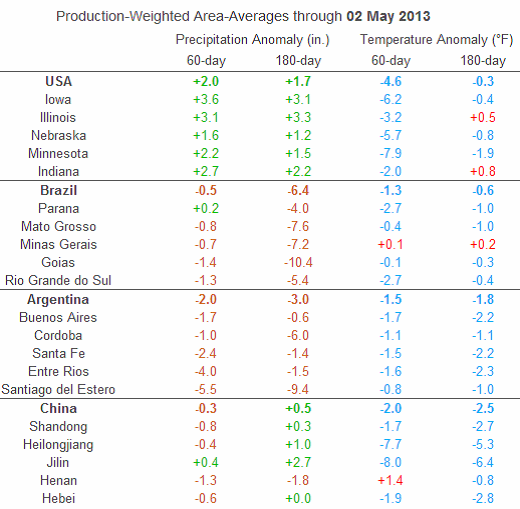

World Ag Weather publicerar även avvikelser från det normala för regn och temperatur för viktiga jordbruksområden. De har till och med bemödat sig om att vikta avvikelsen efter jordbruksareal. Vi ser att större delen av jorden är kallare än normalt. Vissa delar av Argentina har fått väsentligt mycket mindre nederbörd än normalt och USA tvärtom mycket mer än normalt.

Vi noterar också att Kina är väsentligt mycket kallare än normalt. Eventuella negativa effekter av det på väntad skörd har än så länge inte blivit kända.

Vete

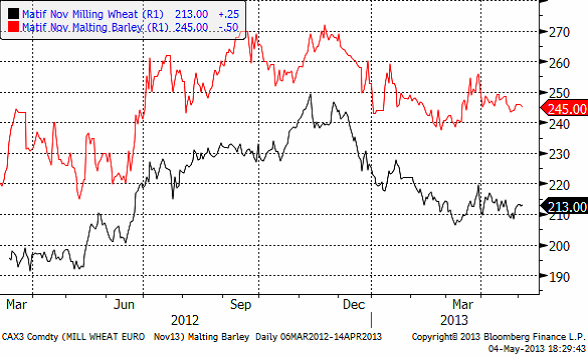

Priset på november (2013) har stabiliserat sig över 210 euro per ton. Trenden är alltjämt nedåtriktad, men den här sidledes rörelsen är ändå ett observandum. Det är möjligt att pristrenden nedåt håller på att förlora momentum och att en prisuppgång kan ta vid. Det beror helt på vädret. Möjligen kan WASDE-rapporten på fredag bli utslagsgivande.

Decemberkontraktet på CBOT har stigit upp till motståndet på 758 cent per ton. Vi ser att det finns ytterligare ett motstånd på ca 780 cent, om 758 skulle brytas.

Ser vi på den senaste veckan förändring av terminskurvorna, ser vi att priserna gått upp både i Europa och i USA och ungefär lika mycket på alla löptider.

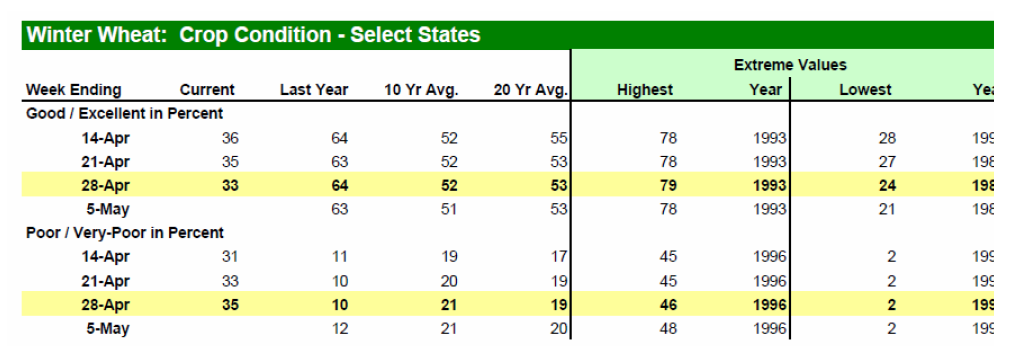

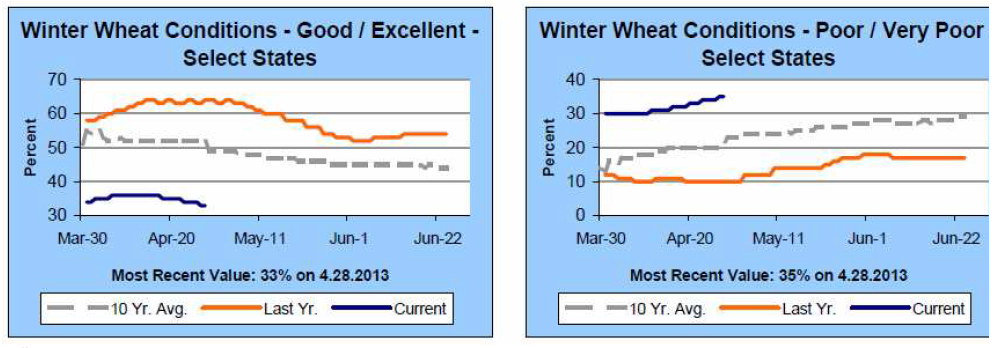

Nedan ser vi Crop condition från förra måndagens rapport.

Måndagens Crop Progress rapport från USDA visar att tillståndet för det amerikanska höstvetet är fortsatt dystert. 35% klassas nu som ”poor/very poor”, en ökning med 2% från veckan innan och att jämföra med 10% vid samma tid förra året. Höstvete klassat som ”good/excellent” har minskat med samma mängd och uppgår nu till 33%, vilket är den lägsta nivån sedan 1996, medan förra årets siffra vid samma tid låg på 64%. Dessutom har endast 14% av höstvetet gått i ax, vilket är långt efter förra årets 55% vid samma tid. I Kansas, den största producenten av HRW vete, backade höstvete i kategorin ”good/excellent” med 3% till 27%.

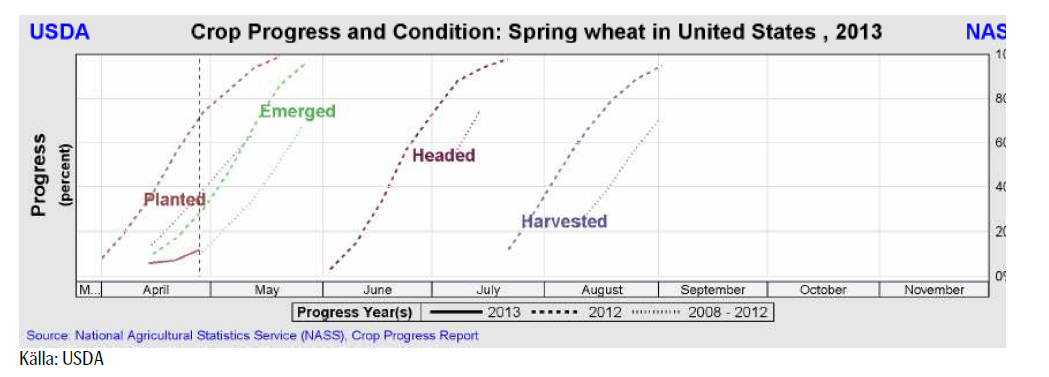

Det blöta och kalla vädret fortsätter också att försena de amerikanska lantbrukarnas sådd av vårvete. Endast 12% av sådden var avklarad per den 29 april, vilket är långt under det femåriga genomsnittet på 37%.

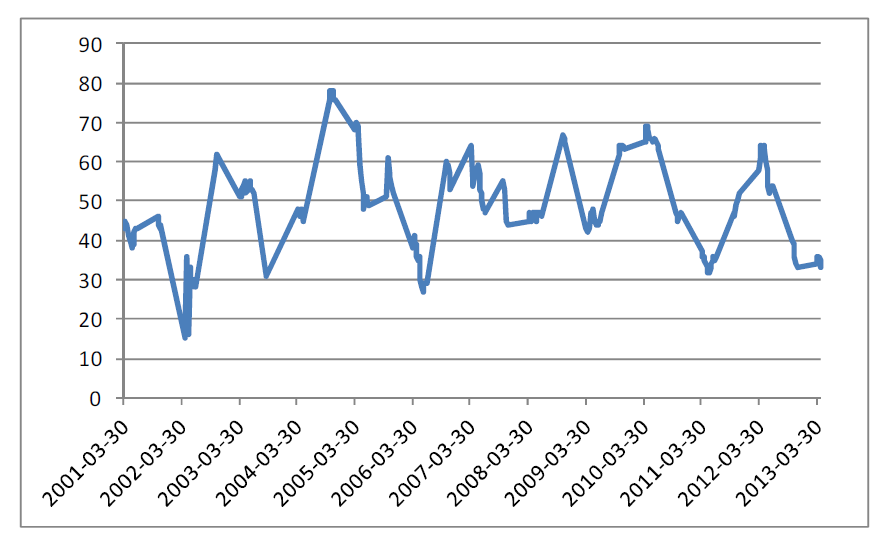

Crop condition för vintervetet i USA ligger kvar på den historiskt låga nivån, som vi ser i diagrammet nedan. Y-axeln visar hur många procent av arealen som har vete i ”good” eller ”excellent condition”.

The Kansas Crop Tour publicerade sin gissning på skörden; endast 313 mbu mot 383 mbu förra året.

Oklahoma Wheat Commission publicerade sitt estimat till 85 mbu mot 155 mbu förra året.

Vi fortsätter, med det observandum vi nämnt ovan, att tro på sidledes eller lägre priser. Uppgångar bör ses som tillfällen att sälja.

Maltkorn

Priset på maltkorn med leverans i november har ännu en vecka fortsatt att visa mer styrka än höstvetet / kvarnvetet på Matif.

Majs

Majspriset (december 2013) steg kraftigt när vädret slog och om det visade sig att sådden blivit ytterligare försenad. Priset har åtminstone kortsiktigt etablerat sig över 550 cent. Det KAN bli en trendvändning uppåt. Det återstår att se.

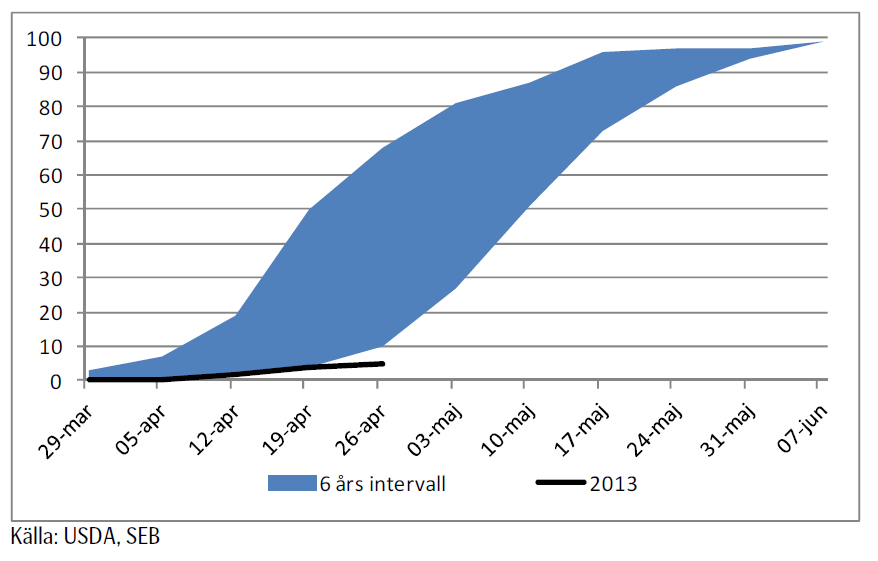

Sådden ligger kraftigt efter i USA. Nedan ser vi såddens framåtskridande i USA. 6-årsintervallet sträcker sig från 2007 till 2012.

Medelvärdet för de sex åren 2006 – 2012 är 33% klart. Den långsammaste starten var 2008, när 10% var sått. Nu är det alltså bara 5%, en marginell ökning från 4% en vecka tidigare men fortfarande långt under förra årets 49% vid den här tiden och även under det genomsnittet. Iowa, den största producenten, har nu påbörjat sådden men endast 2% är avklarad så här långt – att jämföra med det femåriga genomsnittet på 36%. Sådden av majs i de två andra stora producentstaterna, Illinois och Indiana, står fortfarande och stampar på 1% då kraftiga regnskurar i kombination med kallare väder än normalt har gjort att många fält fortfarande är alltför blöta.

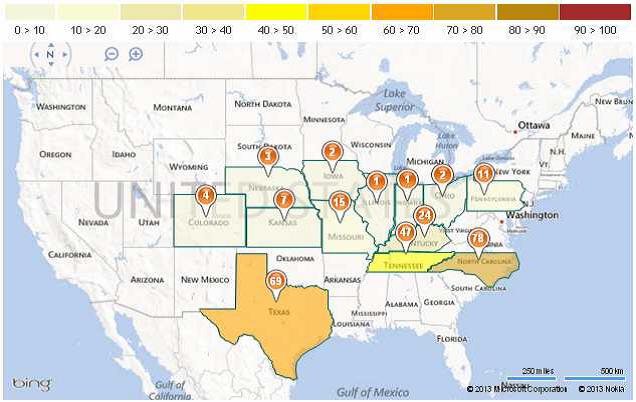

Nedan ser vi en karta över staterna i ”Corn belt”, färgkodade efter hur många procent som är sått och med procentsiffran på kartan.

Det sägs att den 10 maj är en slags deadline för sådden. Den majs som sås efter det datumet ger lägre avkastning. Farmdoc har emellertid skrivit att även om skörden blir 14% mindre än den skulle blivit enligt den hektarskörd som man räknat med, kommer majsen att räcka till efterfrågan. En av de efterfrågeposter som ökat de senaste åren är efterfrågan till etanol. Den kommer inte att öka i år, eftersom USA redan nått maximal inblandning i bensinen av etanol. Foderefterfrågan kommer också att vara tämligen konstant. Med 14% lägre skörd räcker majsen till efterfrågan och ger en viss ökning av utgående lager, enligt Farmdoc. Det finns alltså en hel del marginal i den väntade skördens storlek.

Sojabönor

Sojabönorna (november 2013) anser jag befinner sig i negativ trend och vi ser en rekyl upp från 1200 cent. En rekyl är en naturlig och temporär fluktuation mot trenden.

Exporten från Brasilien börjar ta mer fart nu, efter de initiala problemen att få ut nästan 20 miljoner ton mer än förra året. Kinas tillväxt håller på att bromsa in. Nya svaga siffror kom i veckan. Den senaste köttskandalen där fårkött i egentligen kommit från flera andra djur. Det enda som stack ut med sin frånvaro av förklarliga skäl var hund. De här skandalerna och den allt jämt pågående nya fågelinfluensan gör att efterfrågan på soja borde vara dämpad framöver i Kina.

Man kan spekulera i att sojaarealen i USA borde bli större när den inte kan sås med majs. Arealen är antagligen inte utbytbar 1:1, inte minst pga behovet av utsäde. Marken är visserligen kvävegödslad sedan länge, men detta är en ”sunk cost” och även om det inte är till stor nytta för sojabönorna, så är det i vart fall inte till nackdel. Blir det fortsatt kallt drabbar vädret dock även sojaarealen.

Jag skulle passa på och sälja sojabönor på högre priser, eftersom trenden och fundamenta så väl pekar på lägre priser. Jag har svårt att se hur WASDE-rapporten kan bli positiv för marknaden

Raps

I flera veckor har vi noterat att rapspriset byggt upp fallhöjd i förhållande till det allt lägre sojabönspriset. I veckan som gick orkade inte rapsmarknaden hålla emot den kraften med fallande pris som följd. Den lilla nedgång som hittills ägt rum tror vi bara är början på en nedgång, som gör att priset på raps hamnar i paritet med sojapriset igen. Nedan ser vi november-terminens kursutveckling.

Skulle det tekniska stödet på 415 euro brytas, är detta en rejäl säljsignal. Om WASDE-rapporten är riktigt negativ för sojabönor skulle detta kunna inträffa. I mellantiden vill jag vara fortsatt såld raps.

[box]SEB Veckobrev Jordbruksprodukter är producerat av SEB Merchant Banking och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Disclaimer

The information in this document has been compiled by SEB Merchant Banking, a division within Skandinaviska Enskilda Banken AB (publ) (“SEB”).

Opinions contained in this report represent the bank’s present opinion only and are subject to change without notice. All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, expressed or implied, is made with respect to the completeness or accuracy of its contents and the information is not to be relied upon as authoritative. Anyone considering taking actions based upon the content of this document is urged to base his or her investment decisions upon such investigations as he or she deems necessary. This document is being provided as information only, and no specific actions are being solicited as a result of it; to the extent permitted by law, no liability whatsoever is accepted for any direct or consequential loss arising from use of this document or its contents.

About SEB

SEB is a public company incorporated in Stockholm, Sweden, with limited liability. It is a participant at major Nordic and other European Regulated Markets and Multilateral Trading Facilities (as well as some non-European equivalent markets) for trading in financial instruments, such as markets operated by NASDAQ OMX, NYSE Euronext, London Stock Exchange, Deutsche Börse, Swiss Exchanges, Turquoise and Chi-X. SEB is authorized and regulated by Finansinspektionen in Sweden; it is authorized and subject to limited regulation by the Financial Services Authority for the conduct of designated investment business in the UK, and is subject to the provisions of relevant regulators in all other jurisdictions where SEB conducts operations. SEB Merchant Banking. All rights reserved.

Lower as OPEC+ keeps fast-tracking redeployment of previous cuts. Brent closed down 1.3% yesterday to USD 68.76/b on the back of the news over the weekend that OPEC+ (V8) lifted its quota by 547 kb/d for September. Intraday it traded to a low of USD 68.0/b but then pushed higher as Trump threatened to slap sanctions on India if it continues to buy loads of Russian oil. An effort by Donald Trump to force Putin to a truce in Ukraine. This morning it is trading down 0.6% at USD 68.3/b which is just USD 1.3/b below its July average.

Only US shale can hand back the market share which OPEC+ is after. The overall picture in the oil market today and the coming 18 months is that OPEC+ is in the process of taking back market share which it lost over the past years in exchange for higher prices. There is only one source of oil supply which has sufficient reactivity and that is US shale. Average liquids production in the US is set to average 23.1 mb/d in 2025 which is up a whooping 3.4 mb/d since 2021 while it is only up 280 kb/d versus 2024.

Taking back market share is usually a messy business involving a deep trough in prices and significant economic pain for the involved parties. The original plan of OPEC+ (V8) was to tip-toe the 2.2 mb/d cuts gradually back into the market over the course to December 2026. Hoping that robust demand growth and slower non-OPEC+ supply growth would make room for the re-deployment without pushing oil prices down too much.

From tip-toing to fast-tracking. Though still not full aggression. US trade war, weaker global growth outlook and Trump insisting on a lower oil price, and persistent robust non-OPEC+ supply growth changed their minds. Now it is much more fast-track with the re-deployment of the 2.2 mb/d done already by September this year. Though with some adjustments. Lifting quotas is not immediately the same as lifting production as Russia and Iraq first have to pay down their production debt. The OPEC+ organization is also holding the door open for production cuts if need be. And the group is not blasting the market with oil. So far it has all been very orderly with limited impact on prices. Despite the fast-tracking.

The overall process is nonetheless still to take back market share. And that won’t be without pain. The good news for OPEC+ is of course that US shale now is cooling down when WTI is south of USD 65/b rather than heating up when WTI is north of USD 45/b as was the case before.

OPEC+ will have to break some eggs in the US shale oil patches to take back lost market share. The process is already in play. Global oil inventories have been building and they will build more and the oil price will be pushed lower.

A Brent average of USD 60/b in 2026 implies a low of the year of USD 45-47.5/b. Assume that an average Brent crude oil price of USD 60/b and an average WTI price of USD 57.5/b in 2026 is sufficient to drive US oil rig count down by another 100 rigs and US crude production down by 1.5 mb/d from Dec-25 to Dec-26. A Brent crude average of USD 60/b sounds like a nice price. Do remember though that over the course of a year Brent crude fluctuates +/- USD 10-15/b around the average. So if USD 60/b is the average price, then the low of the year is in the mid to the high USD 40ies/b.

US shale oil producers are likely bracing themselves for what’s in store. US shale oil producers are aware of what is in store. They can see that inventories are rising and they have been cutting rigs and drilling activity since mid-April. But significantly more is needed over the coming 18 months or so. The faster they cut the better off they will be. Cutting 5 drilling rigs per week to the end of the year, an additional total of 100 rigs, will likely drive US crude oil production down by 1.5 mb/d from Dec-25 to Dec-26 and come a long way of handing back the market share OPEC+ is after.

The OPEC+ subgroup V8 this weekend decided to fully unwind their voluntary cut of 2.2 mb/d. The September quota hike was set at 547 kb/d thereby unwinding the full 2.2 mb/d. This still leaves another layer of voluntary cuts of 1.6 mb/d which is likely to be unwind at some point.

Higher quotas however do not immediately translate to equally higher production. This because Russia and Iraq have ”production debts” of cumulative over-production which they need to pay back by holding production below the agreed quotas. I.e. they cannot (should not) lift production before Jan (Russia) and March (Iraq) next year.

Argus estimates that global oil stocks have increased by 180 mb so far this year but with large skews. Strong build in Asia while Europe and the US still have low inventories. US Gulf stocks are at the lowest level in 35 years. This strong skew is likely due to political sanctions towards Russian and Iranian oil exports and the shadow fleet used to export their oil. These sanctions naturally drive their oil exports to Asia and non-OECD countries. That is where the surplus over the past half year has been going and where inventories have been building. An area which has a much more opaque oil market. Relatively low visibility with respect to oil inventories and thus weaker price signals from inventory dynamics there.

This has helped shield Brent and WTI crude oil price benchmarks to some degree from the running, global surplus over the past half year. Brent crude averaged USD 73/b in December 2024 and at current USD 69.7/b it is not all that much lower today despite an estimated global stock build of 180 mb since the end of last year and a highly anticipated equally large stock build for the rest of the year.

What helps to blur the message from OPEC+ in its current process of unwinding cuts and taking back market share, is that, while lifting quotas, it is at the same time also quite explicit that this is not a one way street. That it may turn around make new cuts if need be.

This is very different from its previous efforts to take back market share from US shale oil producers. In its previous efforts it typically tried to shock US shale oil producers out of the market. But they came back very, very quickly.

When OPEC+ now is taking back market share from US shale oil it is more like it is exerting a continuous, gradually increasing pressure towards US shale oil rather than trying to shock it out of the market which it tried before. OPEC+ is now forcing US shale oil producers to gradually back off. US oil drilling rig count is down from 480 in Q1-25 to now 410 last week and it is typically falling by some 4-5 rigs per week currently. This has happened at an average WTI price of about USD 65/b. This is very different from earlier when US shale oil activity exploded when WTI went north of USD 45/b. This helps to give OPEC+ a lot of confidence.

Global oil inventories are set to rise further in H2-25 and crude oil prices will likely be forced lower though the global skew in terms of where inventories are building is muddying the picture. US shale oil activity will likely decline further in H2-25 as well with rig count down maybe another 100 rigs. Thus making room for more oil from OPEC+.

The latest weekly report from the US DOE showed a substantial drawdown across key petroleum categories, adding more upside potential to the fundamental picture.

Commercial crude inventories (excl. SPR) fell by 5.8 million barrels, bringing total inventories down to 415.1 million barrels. Now sitting 11% below the five-year seasonal norm and placed in the lowest 2015-2022 range (see picture below).

Product inventories also tightened further last week. Gasoline inventories declined by 2.1 million barrels, with reductions seen in both finished gasoline and blending components. Current gasoline levels are about 3% below the five-year average for this time of year.

Among products, the most notable move came in diesel, where inventories dropped by almost 4.1 million barrels, deepening the deficit to around 20% below seasonal norms – continuing to underscore the persistent supply tightness in diesel markets.

The only area of inventory growth was in propane/propylene, which posted a significant 5.1-million-barrel build and now stands 9% above the five-year average.

Total commercial petroleum inventories (crude plus refined products) declined by 4.2 million barrels on the week, reinforcing the overall tightening of US crude and products.

Guld stiger till över 3500 USD på osäkerhet i världen

Lyten, tillverkare av litium-svavelbatterier, tar över Northvolts tillgångar i Sverige och Tyskland

Lundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

Alkane Resources och Mandalay Resources har gått samman, aktör inom guld och antimon

Breaking some eggs in US shale

USA inför 93,5 % tull på kinesisk grafit

Fusionsföretag visar hur guld kan produceras av kvicksilver i stor skala – alkemidrömmen ska bli verklighet

Westinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

Ryska militären har skjutit ihjäl minst 11 guldletare vid sin gruva i Centralafrikanska republiken

Eurobattery Minerals förvärvar majoritet i spansk volframgruva

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUSA inför 93,5 % tull på kinesisk grafit

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFusionsföretag visar hur guld kan produceras av kvicksilver i stor skala – alkemidrömmen ska bli verklighet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanWestinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanRyska militären har skjutit ihjäl minst 11 guldletare vid sin gruva i Centralafrikanska republiken

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanEurobattery Minerals förvärvar majoritet i spansk volframgruva

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanKopparpriset i fritt fall i USA efter att tullregler presenterats

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanLundin Gold rapporterar enastående borrresultat vid Fruta del Norte

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKina skärper kontrollen av sällsynta jordartsmetaller, vill stoppa olaglig export