Analys

Crude oil comment – Hard to be bullish for the coming 6 months

Crude oil price action – Down and then back towards the $48/b converging point – for now

Crude oil price action – Down and then back towards the $48/b converging point – for now- Crude oil comment – Hard to be bullish for the coming 6 months

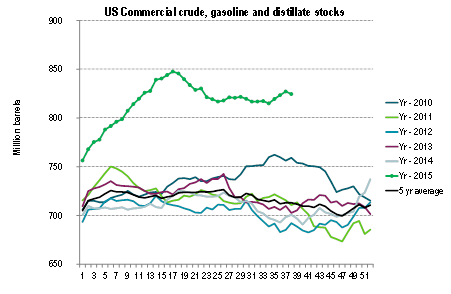

- Graph: US commercial crude and product stocks – on par with two years production from US frack log

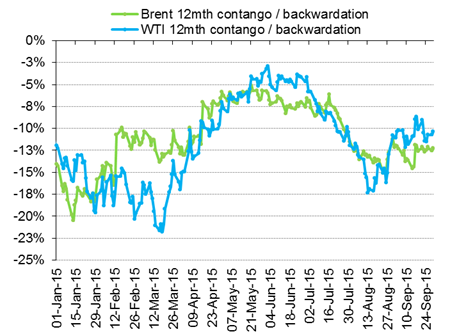

- Graph: Less Brent crude 12mth contango lately, but mostly since longer dated contracts are falling

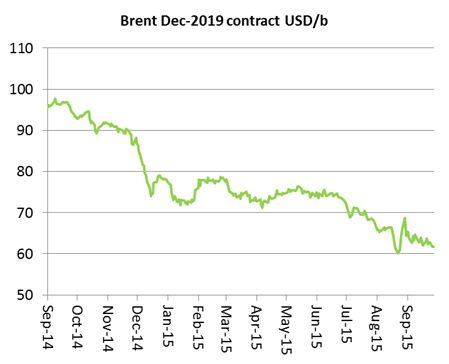

- Graph: The relentless decline of the Brent crude oil December 2019 contract

- Graph: China Leading Index inched yet lower to 98.23 and the lowest since 2009

Crude oil price action – Down and then back towards the $48/b converging point – for now

Brent crude oil traded down 2.6% yesterday to $47.34/b amid a broad based sell-off in European and US equities (-2.6%). Growth concerns for China (industrial profits down 8.8% y/y in August) and the close to 30% drop in Glencore shares helped to drive the bearish sentiment. Do note that Industrial metals only lost 1% so there was not really much of a shake-out in metals on the back of rising China concerns yesterday. Note that while Brent crude saw a percentage wise large drop yesterday, it did not stray too far from the $48/b line which has been a converging price point lately. Today Asia is in the red following the US from last night, but US equities are rebounding. Also Brent crude is rebounding today to $47.7/b and is closing in on the $48/b level again.

Crude oil comment – Hard to be bullish for the coming 6 months

It is difficult to be bullish for the coming 6 months. First out in October and November is the refining turnaround season where refineries now increasingly are taken off-line for maintenance and adjustments ahead of the Northern hemisphere winter season. As this happens more crude oil is left in the market as refineries are not consuming it. Chinese refineries are also projected to process some 250 kb/d to 400 kb/d less in Q4-15 than in Q3-15. At the same time crude oil production in the North Sea is increasing into October and may rise further in November and December, potentially to multi year high. While Q4 is normally a strong demand period of the year it also marks the entrance into demand weakness in Q1 and Q2. We are quite confident that OPEC will not trim its production at its December 4 meeting in Vienna. We are also quite confident that Iran will increase exports of crude oil in Q1 and Q2 as sanctions are lifted and that we overall will get yet another strong rise in global oil stocks in 1H-16. Global oil inventories are already very high with commercial OECD stocks up 272 mb y/y in July to 2972 mb. Of this the US account for 825 mb of crude, gasoline and distillates with a y/y rise of 124 mb (September). On top of this we have the so called US fracklog of drilled wells that have not yet been fracked and put into production. It is difficult to know the size of the fracklog exactly but one estimate places it at around 4500 wells. If we view the fracklog as a kind of oil storage, then 4500 wells amounts to around 800 mb of crude oil that can be put into the market over two years. In other words if all these 4500 wells were producing for two years they would yield some 800 mb of crude oil. After those two years comes the tail-production which will yield even more oil, but over quite a few years.

Counter to this however is the intensifying credit and liquidity situation for the many smaller US shale oil players which will lead to continued declining US crude oil production. Overall however there is limited risk to the upside with so much oil at hand in stocks around the world as well as the US fracklog. In a slightly longer perspective towards the end of 2016 deciding whether the market will be in surplus or deficit in Q4-16 is highly uncertain and will amongst other things depend highly on OPEC production. OPEC has increased production by between 1-2 mb/d this year with main contributors being Iraq and Saudi Arabia. While we expect increasing exports from Iran, it is highly uncertain whether we will see the same increase from Iraq and Saudi Arabia in 2016 as in 2015.

US commercial crude and product stocks – on par with two years production from US frack log

Two years of production from the US fracklog of yet unfracked, but drilled wells will yield crude oil in a magnitude of the current US commercial oil inventories.

Less Brent crude 12mth contango lately, but mostly since longer dated contracts are falling

A key factor here is however that this is not so much to do with strengthening in the front end of the curve, but more to do with a relentless decline in longer dated contracts.

The relentless decline of the Brent crude oil December 2019 contract

The front end of the Brent crude oil curve seems to be very well supported at the $48/b level for the time being. However as the longer dated contracts like the Dec-19 contract ticks lower and lower it forces the curve to be flatter with less contango. If stocks are to increase yet further, which is our base case into 1H-16, an increase in the contango will however be needed. If the longer dated contracts continue to push lower or just stay steady at current level, then the front end contract will need to move lower in order to create the necessary contango to hold increasing storage. At the moment we expect the longer dated contracts to continue lower as producers need to hedge out on the curve while consumer will preferred to purchase oil more towards the front end of the curve in order to utilize contango and low spot crude oil prices.

And then one last graph for the China bears. The China Leading Index inched yet lower to 98.23 and the lowest level since 2009.

Watch out for China PMI manufacturing and services index on Thursday this week.

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking

Brent M1 moving below the 200 dma of $78.7/b. Brent crude continued its move lower yesterday with a decline of 3.3% to $77.9/b. This morning it is adding another drop of 1.4% to $76.8/b. Israel bombing Lebanon during the weekend was a violence of the MoU and Iran was quick to declare the SoH closed again. But the willingness to move forward by both the US and Iran obviously trumped the bombing in Lebanon making the event more of a hiccup on the road of further negotiations.

The US has now waived sanctions against Iranian oil exports for two months allowing Iran to sell its oil all over the world, though sanctions instated in Europe will take more time to unwind. Oil from Iran, Russia as well as Venezuela can for the time being be sold across the world without any sharp discount due to sanctions. Chinese Tea-pot refineries will suffer as they previously could buy rebated crude while selling products at market prices.

Crude oil is no flowing out of the SoH with latest number close to 7 mb/d on a three day moving average. That is still well below the 14 mb/d of crude and 6 mb/d of products normally flowing out of the SoH. Latest estimate is that there is around 80 mb of crude on water inside the Persian Gulf and maybe another 80 mb of oil products on water as well. If crude is exiting the SoH at a rate of around 7 mb/d, then the 80 mb of crude would be depleted within 10-15 days and there after the flow would rely on new crude tankers entering, loading and then exiting the SoH to continue further flows. Given the uncertainties surrounding the status of the SoH with Iran stating that it was closed again as recent as this weekend, there is likely an asymmetry here where ships and oil stranded in the SoH for months are much more eager to exit than new ships are eager to enter.

For now Brent crude keeps falling like a rock with the front-end Brent contract now only trading at a premium of $7.6/b above the five year contract. Quickly heading towards parity. The Brent M1 contract has now broken below its 200 dma of $78.7/b and is closing in on the Fibo-level at $74.7/b. Below that there is not much more supporting levels to be found before $73/b which would close the gap from February 3.

Brent crude M1 technical levels

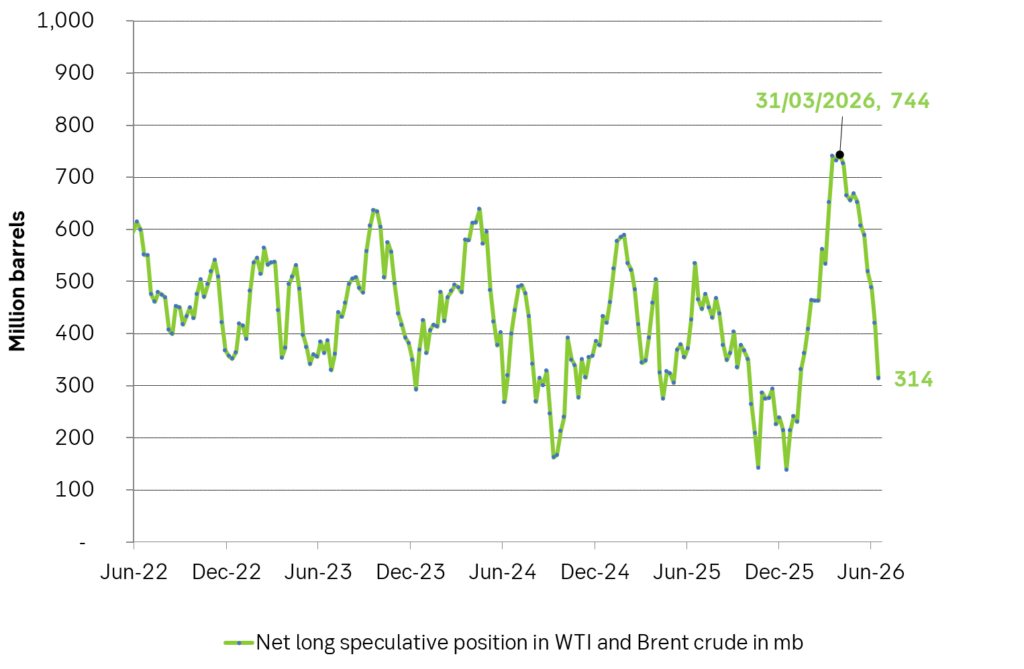

Net long speculative positions are also falling like a rock and as of Tuesday last week the net long positioning in Brent and WTI together summed to 314 million barrels and falling fast.

Will there be a rebound? A possible combination could be an exhaustion of the oil blob caught within the SoH within 1-2 weeks if exits continue at current rate while new ships entering are much more cautious, more Israeli bombardments in Lebanon as Netanyahu fights for re-election, a temporary closure of the SoH again while speculative short positions take cover buying back and covering their positions.

US and Israeli stands versus Iran could harden beyond elections so 2027 surplus is far from given. But Iran and the US are all in all moving towards a set of solutions with both clearly eager to reopen the SoH and keep it open. And that is what the market is pricing along with sharply falling prices. The ongoing discussions will likely take months and last beyond both the upcoming Israeli election (before 27 oct) and the US midterm elections on 3 Nov. Beyond those dates the stance by both Israel and the US may harden again versus Iran. But Iran knows that and is most likely preparing for such a hardening turn. Thus a surplus of oil and global oil stock rebuilding in 2027 (as now is mostly projected) is far from given.

Selling down on a ”deal”. Brent crude fell 6.2% last week with accelerated weakness towards the end of the week. Close of the week at $87.33/b and low of the week (and on Friday) of $85.8/b. Brent is falling another 4% this morning to $83.7/b on confirmation by Iran that a MoU text has been reached and that it will be signed on Friday this week.

So what is this ”deal” worth? Talk on the desk here this morning is that it is much like ”putting lipstick on a pig” where Trump has to sell this at home as a victory where ”the SoH has reopened”, the nuclear issue will be ironed out over the coming 60 days (or maybe 600 days?) and US consumers are getting a lower gasoline price and maybe US republicans survives the midterm elections.

The importance for Iran is that it emerges as the defacto winner of this war in the eyes of the non-US public world. That Iran now onwards is the ”ruler of the SoH” (combo of geography and new weapons systems like drones) or more softer: ”the guarantor of safe passage through the SoH”.

Iran doesn’t need nuclear weapons any more. Nuclear deterrence doesn’t work any more. Ukraine has made many attacks deep into Russia without being nuked in return. Plenty of Iranian ballistic rockets blasts over Israel but Iran wasn’t nuked in return.

There is no trust between the US and Iran. We don’t know all the details yet of the MoU. But what we do know is that there is no trust between the US and Iran what so ever. This is probably more like a descriptive text on how they can cooperate in a way where both sides keeps tactical leverage. Neither side makes irreversible concessions. Violations can be punished quickly. Cooperation produces immediate benefits.

This is a fragile structure. It can easily break down. There may be details which cannot be overcome. To be seen on Friday. The US has to show that it is willing put enough force behind managing and restraining Israel versus Hezbollah in Lebanon. We have seen that Netanyahu hasn’t listened all that much to Trump’s directives and wishes. This could be a major obstacle.

A gradual reopening is tactically preferable for Iran. A tactical leverage for Iran right now is that global oil stocks have been drawn down towards painful and increasingly dangerous levels with increasing risks for oil price spikes in mid-July to August. This together with US midterm elections on 3 November gives tactical leverage to Iran. Iran probably doesn’t want to fully give up on that leverage. A rapid, full reopening where global stocks are able to refill over the coming 60 days will significantly erode that leverage. If Iran reinstates a closure of the SoH after 60 days (if talks break down again), then the effect won’t be that impactful in terms of prices and the US midterm elections.

So a gradual and partial reopening where global markets gets the oil they need while they are unable to rebuild stocks could be a practical middle way for both parties. Trump can sell it as ”the SoH has reopened” and get affordable gasoline for US consumers. Iran can sell it as ”the SoH has fully reopened, but there is some friction” so flow is only 60-80% of normal.

Not much real demand destruction below $100/b. What we do know is that there is not much real price pain demand destruction for oil globally at an oil price below $100/b. A lot of demand-shock destruction. Fear. But demand should now come roaring back towards normal with fear for exceptionally high prices now is rapidly receding.

Sudden China demand destruction due to EVs? Bullocks. EV share of total Chinese carpool now around 13%. Share of new sales of EVs has reached 50%. This is a very gradual process. It doesn’t make oil demand fall like a rock over night. When EV new sales share reaches 100%, then the gasoline car pool will contract by some 5-10% per year. But that is only gasoline. Sudden reduction in Chinese oil demand is more about shock and risk.

Chinese crude oil imports will come roaring back. At what price? Today’s ”neutral” oil price is $70/b. That is the five year price which has steadily traded around the $70/b mark over the past 3-4 years. With still a risky picture one would think that China and the rest of the world will be big buyers of oil in the range of $70-85/b.

Global demand will likely snap back towards normal, forecasted demand and growth at such prices.

Physical reopening is a gradual process. The physical and practical reopening of the SoH will likely be gradual rather than sudden. And that probably suites Iran tactically as well.

Brent M1 price versus the Brent 5-yr (today’s ”normal” price)

Market is starting to take US/Iran headlines with a pinch of salt. Brent crude rose $2.8/b yesterday to an official close of $112.1/b. But after that it traded as low as $108.05/b before ending late night at around $109.7/b. Through the day it traded in a range of $106.87 – 112.72/b amid a flurry of news or rumors from Iran and the US. ”US temporary sanctions during negotiations” (falls alarm). ”We will bomb Iran” (not anyhow),… etc. While the market is still fluctuating to this kind of news flow, it is starting to take such headlines with a pinch of salt.

We’ll see. Maybe, maybe not. The Brent M1 contract is trading at $110.2/b this morning which very close to the average ticks through yesterday of $110.4/b.

Trump with bearish, verbal intervention whenever Brent trades above $110/b it seems. What seems to be a pattern is that Trump states something like ”very good negotiations going on with Iran”, ”New leaders in Iran are great,..”, ”Great progress in negotiations,…”, ”Deal in sight,..” etc whenever the Brent M1 contract trades above $110/b. An effort to cool the market. These hot air verbal interventions from Trump used to have a heavy bearish impact on prices, but they now seems to have less and less effect unless they are backed by reality.

As far as we can see there has been no real progress in the negotiations between the US and Iran with both sides still standing by their previous demands.

Iran is getting stronger while the cease fire lasts making a return to war for Trump yet harder. Iran is naturally in constant preparation for a return to war given Trump’s steady threats of bombing Iran again. Iran is naturally doing what ever is possible to prepare for a return to war. And every day the cease fire lasts it is better prepared. This naturally makes it more and more difficult and dangerous for the US to return to warring activity versus Iran as the consequences for energy infrastructure in the Persian Gulf will be more and more severe the longer the cease fire lasts. Israel seems to see it this way as well. That the war is not won and that current frozen state of a cease fire gives Iran opportunity to rebuild military and politically.

Global inventories are drawing down day by day. How much? In the meantime the Strait of Hormuz stays closed. There is varying measures and estimates of how much global inventories are drawing down. Our rough estimate, back of the envelope, is that global inventories are drawing down by at least some 10 mb/d or about 300 mb/d in a balance between loss of supply versus demand destruction. Other estimates we see are a monthly draw of 250-270 mb/d. The IEA only ’measured’ a draw in global observable stocks of 117 mb in April with oil on water rising 53 mb while on shore stocks fell 170 mb. But global stocks are hard to measure with large invisible, unmeasured stocks. As such a back of the envelope approach may be better.

Oil products is what the world is consuming. Oil product prices likely to rise while product stocks fall. Strategic Petroleum Reserves (SPR) are predominantly crude oil. Discharging oil from OECD SPR stocks, a sharp reduction in Chinese crude imports and a reduction in global refinery throughput of 6-7 mb/d has helped to keep crude oil markets satisfactorily supplied. But global inventories are drawing down none the less. And oil products is really what the world is consuming. So if global refinery throughput stays subdued, then demand will eventually have to match the supply of oil products. The likely path forward this summer is a steady draw down in jet fuel, diesel and gasoline. Higher prices for these. Then, if possible, higher refinery throughput and higher usage of crude in response to very profitable refinery margins. And lastly sharper draw in crude stocks and higher prices for these. But some 6 mb/d of oil products used to be exported through the Strait of Hormuz. And it may not be so easy to ramp up refinery activity across the world to compensate. Especially as Ukraine continues to damage Russian refineries as well as Russian crude production and export facilities.

Watch oil product stocks and prices as well as Brent calendar 2027. What to watch for this summer is thus oil product inventories falling and oil product premiums to crude rising. Another measure to watch is the Brent crude 2027 contract as it rises steadily day by day as the Strait of Hormuz stays closed and global oil inventories decline. The latter is close to the highest level since the start of the war and keeps rising.

The Brent M1 contract and the Brent 2027 prices and current price of jet fuel in Europe (ARA). All in USD/b

Our back of the envelope calculation of the global shortage created by the closure of the Strait of Hormuz. Note that 3.5 mb/d of discharge from SPR is also a draw. Note also that ’Forced demand loss’ of 2.5 mb/d is probably temporary and will fall back towards zero as logistics are sorted out leaving ’Price demand loss’ to do the job of balancing the market. Thus a shortfall of at least 9 mb/d created by the closure. More if SPR discharge is included and more if Forced demand loss recedes.

Brent falling like a rock with oil likely to flow from SoH until at least 3 November

Vattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

Selling down on a ”deal”

Sommarväder skapar prisrally på elbörsen

Oil product price pain is set to rise as the Strait of Hormuz stays closed into summer

Sommarväder skapar prisrally på elbörsen

Vattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

Selling down on a ”deal”

Brent falling like a rock with oil likely to flow from SoH until at least 3 November

-

Nyheter3 veckor sedan

Sommarväder skapar prisrally på elbörsen

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanVattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

-

Analys1 vecka sedan

Selling down on a ”deal”

-

Analys9 timmar sedan

Brent falling like a rock with oil likely to flow from SoH until at least 3 November