Analys

Iran – Reactive Saudi means price will tick higher

Saudi Arabia pre-emptively and proactively lifted oil production last year in anticipation of US sanctions towards Iran. Sanctions were supposed to be more or less “cold turkey” starting November last year but Donald caved in and handed out a large portion of waivers. The result was that the pre-emptive production increase by OPEC+ last year instead managed to crash the oil price down to below $50/bl. Saudi Arabia is unlikely to make the same mistake again and is in our view likely to be reactive this time. First see how much oil supply is really lost and then increase production according to needs.

That means that the oil price is likely going to continue on its current bull-ride for a while before Saudi Arabia (++) decides to pitch in with substantially more production.

Iran probably exported about 2 m bl/d in March according to tanker tracker news. That is down 1 m bl/d from one year ago when they exported about 3.0 m bl/d liquids.

South Korea, India, Japan imported 0.75 m bl/d in March. They are likely going to comply fully so that their imports will likely fall to close to zero in May/June.

China imported 0.61 m bl/d in March versus waivers allowed by the US of 0.36 m bl/d. China has strongly opposed the US sanctions towards Iran: “The US is reaching beyond its jurisdiction” and “Our cooperation with Iran is open, transparent, lawful and legitimate”. We think that China can’t and won’t back down this time and that we could easily see an increase of Chinese oil imports from Iran up towards maybe 1.0 m bl/d

China Iran oil imports to increase and more Iran oil under the radar. There will also be an increasing amount of oil exports out of Iran which will go “under the sanctions radar”. This could probably amount to some 0.5 m bl/d and were probably already standing at around 0.3 m bl/d in March. So if China lifts imports from 0.6 m bl/d in March to instead 1.0 m bl/d and “under the radar” exports increase from 0.3 m bl/d in March to instead 0.5 m bl/d then Iran oil exports will continue at around 1.5 m bl/d versus around 2.0 m bl/d in March

Increasing collision course between the US and China. The “cold turkey” Iran sanctions from the US will force China to decide what to do, to hold its turf and claim its right to import oil from Iran. It will drive Iran closer to China and enable China to settle yet more oil in renminbi.

Russia is unlikely to hold back production in 2H-19. It reduced its production by some 0.2 m bl/d to 11.3 m bl/d in March in order to comply with the OPEC+ agreement from early December. It’ll probably lift production back up to 11.5 m bl/d in 2H-19 and then tick higher. It has been sensibly reluctant to pre-emptively promise to hold back production in 2H-19 and stated very clearly that it’ll manage production according to circumstances and that these circumstances will be evaluated when they meet with OPEC+ in Vienna in June 25/26.

Russian willingness to cut probably vanishes around $65/bl. Saudi Arabia would happily see the oil price back up at $85/bl. Russia’s willingness to cut in order to support the oil price probably vanishes around $65/bl. Russia is all-in joining Saudi Arabia on production cuts in times of surplus, rising stocks and Brent below $50/bl. It has however communicated very clearly that it is not all too eager to hold the oil price much above $65/bl as it will boost shale oil investments and production. That is alright as long as we are losing more and more supply from Iran and Venezuela. But what if those supplies come back into the market while US shale production growth is booming at the same time? Thus better to be safe than sorry and keep the oil price at around $65/bl and US shale oil activity at medium temperature.

The market will lose some 0.5 – 1.0 m bl/d. We cannot really know how much supply will now be lost from Iran. We don’t think it will go to zero but rather that exports will decline from 2.0 m bl/d in March to instead some 1.0 – 1.5 m bl/d along with increasing imports by China and “unknowns”. I.e. the market will lose some 0.5 – 1.0 m bl/d. OPEC+ can easily adjust for this. Saudi Arabia could actually do it alone.

Saudi Arabia (OPEC+) in very good control of the market. OPEC+ in general and Saudi Arabia specifically will have a very good handle of the supply situation of the oil market. I.e. Saudi will put current cuts partially back into the market and can then cut again at a later time instead.

John Bolton aiming for Iran regime shift. It has been stated that Donald Trump does not know what he want to achieve in the Middle East but that John Bolton does: a regime shift. The zero waivers is a victory for John Bolton’s politics. It increases the risk for turmoil in the Middle East.

A higher oil price is good for the US. Donald Trump has for a long time tried to aim for a low oil price in support of the US consumer and his core voters. His economic advisors have however this spring argued that a high oil price is now increasingly positive for the US economy as a whole as it is now increasingly becoming a net oil exporter. The negative for the consumers is increasingly outweighed by the positives for the oil producers. Thus Donald going for no waivers means that Donald is now increasingly siding with the producers rather than the consumers.

A more fragile oil market balance and yet more supply from the US. Less oil from Iran and a higher oil price means more US shale oil drilling and more supply growth from the US. But we are also getting a more fragile oil market. Supply from Venezuela continues to decline while supply from Libya and Nigeria is unstable as well.

Crude quality matters – IMO 2020 and diesel. Global oil supply is losing more and more medium to heavy sour crude oil which instead is largely replaced by ultralight US shale oil supply. The former is rich on medium to heavy molecule chains where the heavy chains can be converted to medium. The ultralight is rich on gasoline and light products which cannot be converted to medium elements. Medium elements mean Diesel, Gasoil and Jet fuel. Due to new fuel regulations in global shipping from 1 January 2020 the global shipping fleet will consume a lot more diesel/Gasoil like molecules. So less supply of diesel/Gasoil rich crudes but more demand means yet stronger mid-dist cracks.

Medium sour crude is typically the crude Saudi Arabia and OPEC and Russia. So if the world is craving for more Diesel, Gasoil and Jet fuel it is also craving for more of this crude. It means that Saudi Arabia and Russia (and OPEC) are in very good control of the oil market, even better than headline numbers indicate due to quality issues.

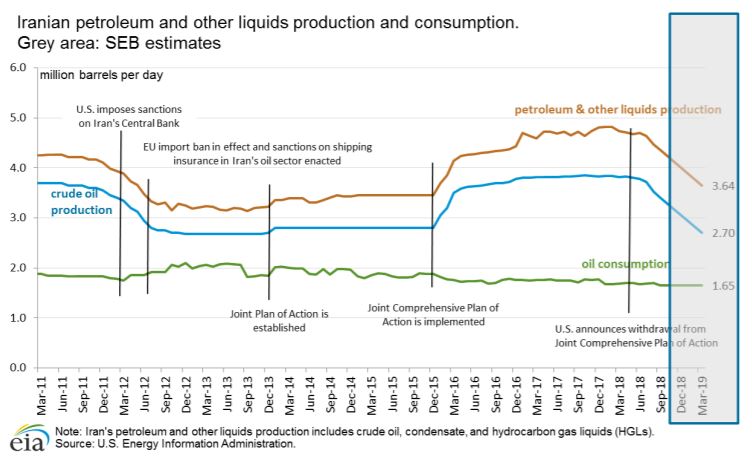

Ch1: Iran consumes some 1.7 m bl/d. In addition to 2.7 m bl/d of crude production in March 2019 it probably also produced some 0.95 m bl/d of condensates with total production of liquids of about 3.65 m bl/d. Exports thus probably stood at around 2.0 m bl/d in March which is also what tanker tracker data indicates. Exports are probably going to decline to about 1.0 to 1.5 m bl/d in May June

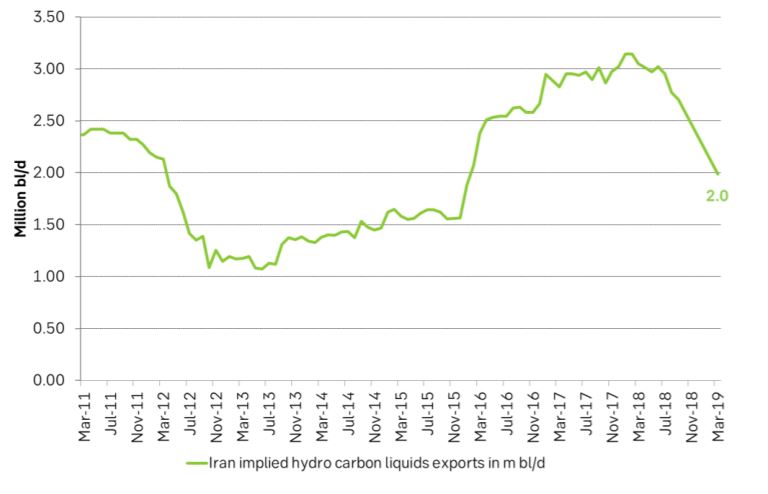

Ch2: Implied Iran hydro carbon liquids exports in m bl/d. US IEA data up to Sep 2018. Last data point estimated by SEB

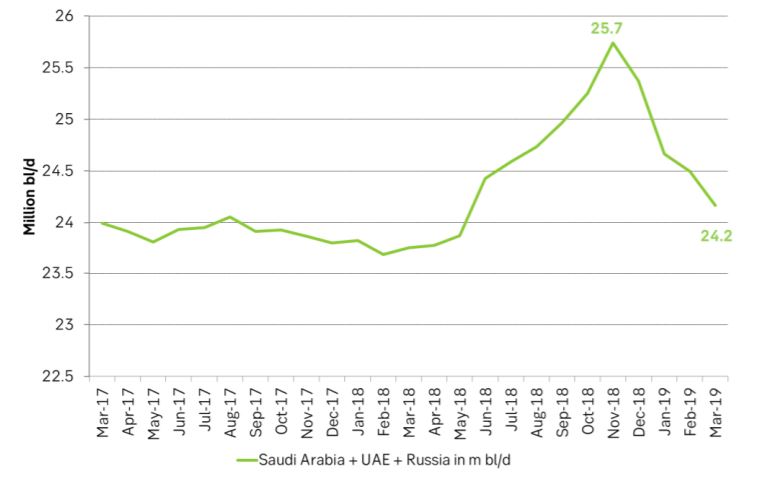

Ch3: Saudi Arabia, UAE and Russia can easily lift production by 1.5 m bl/d

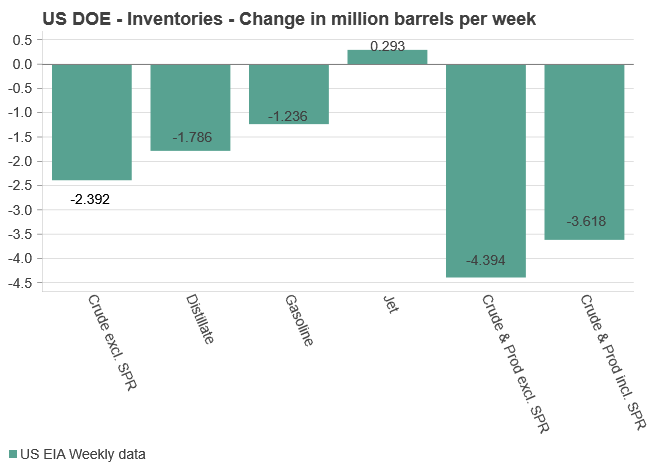

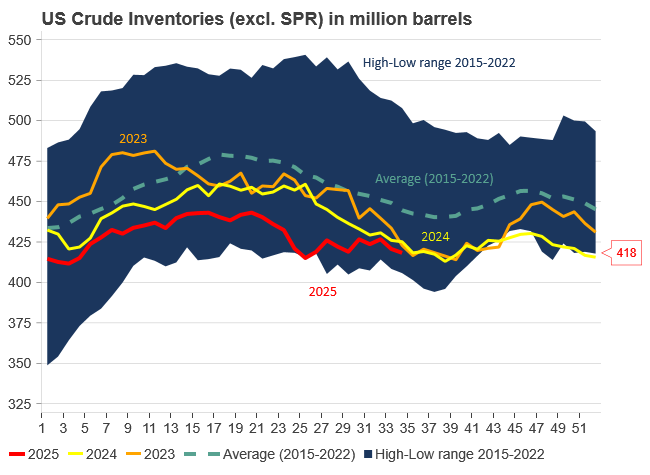

U.S. commercial crude inventories posted another draw last week, falling by 2.4 million barrels to 418.3 million barrels, according to the latest DOE report. Inventories are now 6% below the five-year seasonal average, underlining a persistently tight supply picture as we move into the post-peak demand season.

While the draw was smaller than last week’s 6 million barrel decline, the trend remains consistent with seasonal patterns. Current inventories are still well below the 2015–2022 average of around 449 million barrels.

Gasoline inventories dropped by 1.2 million barrels and are now close to the five-year average. The breakdown showed a modest increase in finished gasoline offset by a decline in blending components – hinting at steady end-user demand.

Diesel inventories saw yet another sharp move, falling by 1.8 million barrels. Stocks are now 15% below the five-year average, pointing to sustained tightness in middle distillates. In fact, diesel remains the most undersupplied segment, with current inventory levels at the very low end of the historical range (see page 3 attached).

Total commercial petroleum inventories – including crude and products but excluding the SPR – fell by 4.4 million barrels on the week, bringing total inventories to approximately 1,259 million barrels. Despite rising refinery utilization at 94.6%, the broader inventory complex remains structurally tight.

On the demand side, the DOE’s ‘products supplied’ metric – a proxy for implied consumption – stayed strong. Total product demand averaged 21.2 million barrels per day over the last four weeks, up 2.5% YoY. Diesel and jet fuel were the standouts, up 7.7% and 1.7%, respectively, while gasoline demand softened slightly, down 1.1% YoY. The figures reflect a still-solid late-summer demand environment, particularly in industrial and freight-related sectors.

Analys

Increasing risk that OPEC+ will unwind the last 1.65 mb/d of cuts when they meet on 7 September

Pushed higher by falling US inventories and positive Jackson Hall signals. Brent crude traded up 2.9% last week to a close of $67.73/b. It traded between $65.3/b and $68.0/b with the low early in the week and the high on Friday. US oil inventory draws together with positive signals from Powel at Jackson Hall signaling that rate cuts are highly likely helped to drive both oil and equities higher.

Ticking higher for a fourth day in a row. Bank holiday in the UK calls for muted European session. Brent crude is inching 0.2% higher this morning to $67.9/b which if it holds will be the fourth trading day in a row with gains. Price action in the European session will likely be quite muted due to bank holiday in the UK today.

OPEC+ is lifting production but we keep waiting for the surplus to show up. The rapid unwinding of voluntary cuts by OPEC+ has placed the market in a waiting position. Waiting for the surplus to emerge and materialize. Waiting for OECD stocks to rise rapidly and visibly. Waiting for US crude and product stocks to rise. Waiting for crude oil forward curves to bend into proper contango. Waiting for increasing supply of medium sour crude from OPEC+ to push sour cracks lower and to push Mid-East sour crudes to increasing discounts to light sweet Brent crude. In anticipation of this the market has traded Brent and WTI crude benchmarks up to $10/b lower than what solely looking at present OECD inventories, US inventories and front-end backwardation would have warranted.

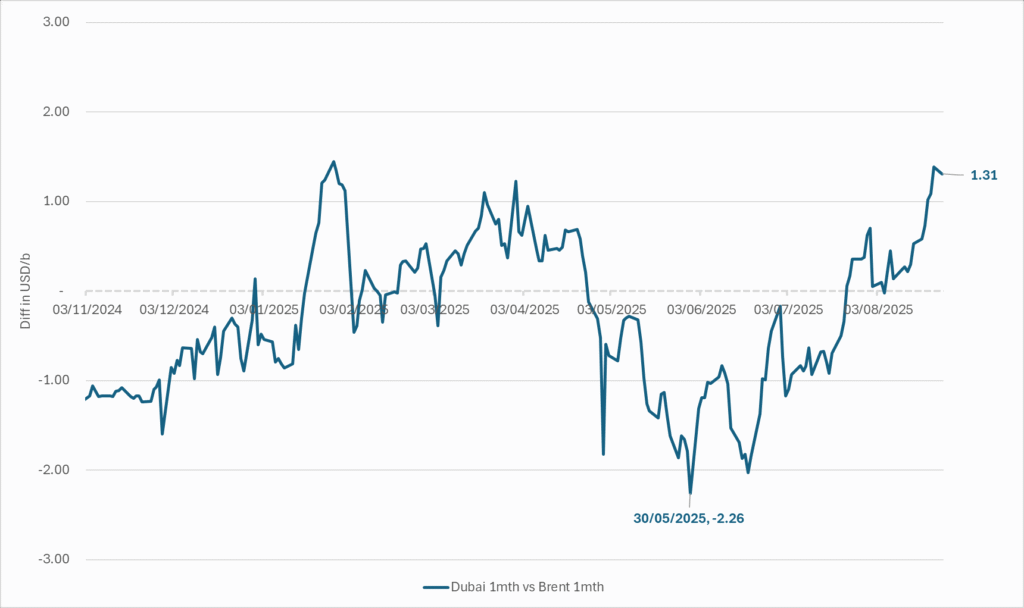

Quite a few pockets of strength. Dubai sour crude is trading at a premium to Brent crude! The front-end of the crude oil curves are still in backwardation. High sulfur fuel oil in ARA has weakened from parity with Brent crude in May, but is still only trading at a discount of $5.6/b to Brent versus a more normal discount of $10/b. ARA middle distillates are trading at a premium of $25/b versus Brent crude versus a more normal $15-20/b. US crude stocks are at the lowest seasonal level since 2018. And lastly, the Dubai sour crude marker is trading a premium to Brent crude (light sweet crude in Europe) as highlighted by Bloomberg this morning. Dubai is normally at a discount to Brent. With more medium sour crude from OPEC+ in general and the Middle East specifically, the widespread and natural expectation has been that Dubai should trade at an increasing discount to Brent. the opposite has happened. Dubai traded at a discount of $2.3/b to Brent in early June. Dubai has since then been on a steady strengthening path versus Brent crude and Dubai is today trading at a premium of $1.3/b. Quite unusual in general but especially so now that OPEC+ is supposed to produce more.

This makes the upcoming OPEC+ meeting on 7 September even more of a thrill. At stake is the next and last layer of 1.65 mb/d of voluntary cuts to unwind. The market described above shows pockets of strength blinking here and there. This clearly increases the chance that OPEC+ decides to unwind the remaining 1.65 mb/d of voluntary cuts when they meet on 7 September to discuss production in October. Though maybe they split it over two or three months of unwind. After that the group can start again with a clean slate and discuss OPEC+ wide cuts rather than voluntary cuts by a sub-group. That paves the way for OPEC+ wide cuts into Q1-26 where a large surplus is projected unless the group kicks in with cuts.

The Dubai medium sour crude oil marker usually trades at a discount to Brent crude. More oil from the Middle East as they unwind cuts should make that discount to Brent crude even more pronounced. Dubai has instead traded steadily stronger versus Brent since late May.

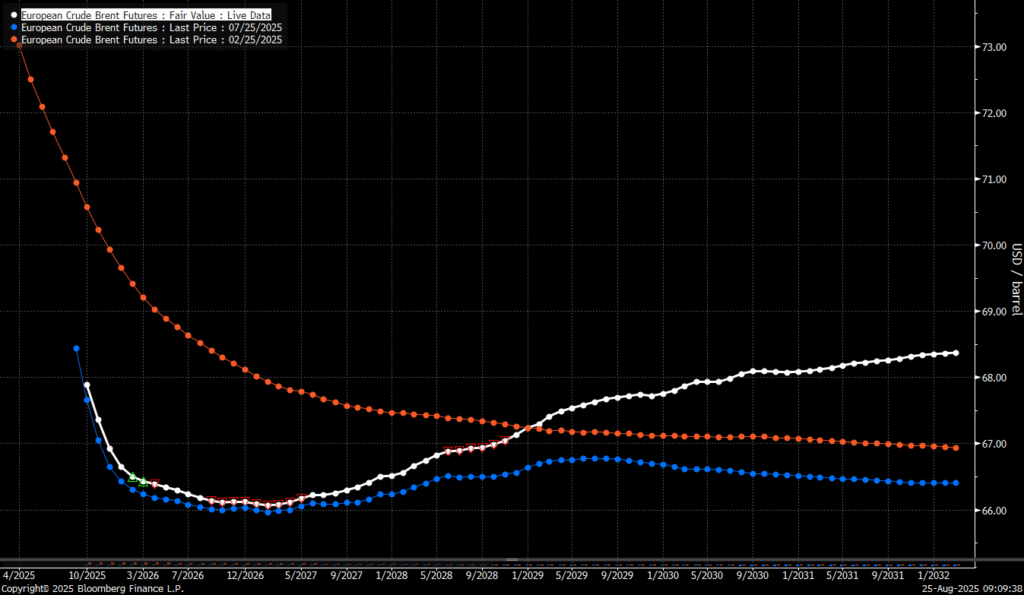

The Brent crude oil forward curve (latest in white) keeps stuck in backwardation at the front end of the curve. I.e. it is still a tight crude oil market at present. The smile-effect is the market anticipation of surplus down the road.

Analys

Brent edges higher as India–Russia oil trade draws U.S. ire and Powell takes the stage at Jackson Hole

Best price since early August. Brent crude gained 1.2% yesterday to settle at USD 67.67/b, the highest close since early August and the second day of gains. Prices traded to an intraday low of USD 66.74/b before closing up on the day. This morning Brent is ticking slightly higher at USD 67.76/b as the market steadies ahead of Fed Chair Jerome Powell’s Jackson Hole speech later today.

No Russia/Ukraine peace in sight and India getting heat from US over imports of Russian oil. Yesterday’s price action was driven by renewed geopolitical tension and steady underlying demand. Stalled ceasefire talks between Russia and Ukraine helped maintain a modest risk premium, while the spotlight turned to India’s continued imports of Russian crude. Trump sharply criticized New Delhi’s purchases, threatening higher tariffs and possible sanctions. His administration has already announced tariff hikes on Indian goods from 25% to 50% later this month. India has pushed back, defending its right to diversify crude sourcing and highlighting that it also buys oil from the U.S. Moscow meanwhile reaffirmed its commitment to supply India, deepening the impression that global energy flows are becoming increasingly politicized.

Holding steady this morning awaiting Powell’s address at Jackson Hall. This morning the main market focus is Powell’s address at Jackson Hole. It is set to be the key event for markets today, with traders parsing every word for signals on the Fed’s policy path. A September rate cut is still the base case but the odds have slipped from almost certainty earlier this month to around three-quarters. Sticky inflation data have tempered expectations, raising the stakes for Powell to strike the right balance between growth concerns and inflation risks. His tone will shape global risk sentiment into the weekend and will be closely watched for implications on the oil demand outlook.

For now, oil is holding steady with geopolitical frictions lending support and macro uncertainty keeping gains in check.

Oil market is starting to think and worry about next OPEC+ meeting on 7 September. While still a good two weeks to go, the next OPEC+ meeting on 7 September will be crucial for the oil market. After approving hefty production hikes in August and September, the question is now whether the group will also unwind the remaining 1.65 million bpd of voluntary cuts. Thereby completing the full phase-out of voluntary reductions well ahead of schedule. The decision will test OPEC+’s balancing act between volume-driven influence and price stability. The gathering on 7 September may give the clearest signal yet of whether the group will pause, pivot, or press ahead.

Silverpriset når 40 USD, högsta sedan 2011

Nytt produktionsrekord av olja i USA, högsta efterfrågan på 20 år

Crude stocks fall again – diesel tightness persists

Mahvie Minerals är verksamt i guldrikt område i Finland

Neil Atkinson spår att priset på olja kommer att stiga till 70 USD

Omgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

Lundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

Meta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

Guld stiger till över 3500 USD på osäkerhet i världen

What OPEC+ is doing, what it is saying and what we are hearing

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOmgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanLundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanMeta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGuld stiger till över 3500 USD på osäkerhet i världen

-

Analys3 veckor sedan

What OPEC+ is doing, what it is saying and what we are hearing

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanAlkane Resources och Mandalay Resources har gått samman, aktör inom guld och antimon

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanAker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanLyten, tillverkare av litium-svavelbatterier, tar över Northvolts tillgångar i Sverige och Tyskland