Analys

Iran – Reactive Saudi means price will tick higher

Saudi Arabia pre-emptively and proactively lifted oil production last year in anticipation of US sanctions towards Iran. Sanctions were supposed to be more or less “cold turkey” starting November last year but Donald caved in and handed out a large portion of waivers. The result was that the pre-emptive production increase by OPEC+ last year instead managed to crash the oil price down to below $50/bl. Saudi Arabia is unlikely to make the same mistake again and is in our view likely to be reactive this time. First see how much oil supply is really lost and then increase production according to needs.

That means that the oil price is likely going to continue on its current bull-ride for a while before Saudi Arabia (++) decides to pitch in with substantially more production.

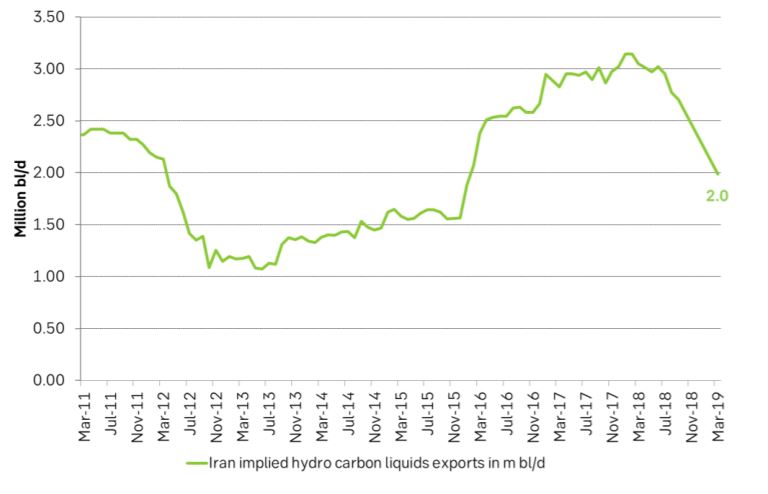

Iran probably exported about 2 m bl/d in March according to tanker tracker news. That is down 1 m bl/d from one year ago when they exported about 3.0 m bl/d liquids.

South Korea, India, Japan imported 0.75 m bl/d in March. They are likely going to comply fully so that their imports will likely fall to close to zero in May/June.

China imported 0.61 m bl/d in March versus waivers allowed by the US of 0.36 m bl/d. China has strongly opposed the US sanctions towards Iran: “The US is reaching beyond its jurisdiction” and “Our cooperation with Iran is open, transparent, lawful and legitimate”. We think that China can’t and won’t back down this time and that we could easily see an increase of Chinese oil imports from Iran up towards maybe 1.0 m bl/d

China Iran oil imports to increase and more Iran oil under the radar. There will also be an increasing amount of oil exports out of Iran which will go “under the sanctions radar”. This could probably amount to some 0.5 m bl/d and were probably already standing at around 0.3 m bl/d in March. So if China lifts imports from 0.6 m bl/d in March to instead 1.0 m bl/d and “under the radar” exports increase from 0.3 m bl/d in March to instead 0.5 m bl/d then Iran oil exports will continue at around 1.5 m bl/d versus around 2.0 m bl/d in March

Increasing collision course between the US and China. The “cold turkey” Iran sanctions from the US will force China to decide what to do, to hold its turf and claim its right to import oil from Iran. It will drive Iran closer to China and enable China to settle yet more oil in renminbi.

Russia is unlikely to hold back production in 2H-19. It reduced its production by some 0.2 m bl/d to 11.3 m bl/d in March in order to comply with the OPEC+ agreement from early December. It’ll probably lift production back up to 11.5 m bl/d in 2H-19 and then tick higher. It has been sensibly reluctant to pre-emptively promise to hold back production in 2H-19 and stated very clearly that it’ll manage production according to circumstances and that these circumstances will be evaluated when they meet with OPEC+ in Vienna in June 25/26.

Russian willingness to cut probably vanishes around $65/bl. Saudi Arabia would happily see the oil price back up at $85/bl. Russia’s willingness to cut in order to support the oil price probably vanishes around $65/bl. Russia is all-in joining Saudi Arabia on production cuts in times of surplus, rising stocks and Brent below $50/bl. It has however communicated very clearly that it is not all too eager to hold the oil price much above $65/bl as it will boost shale oil investments and production. That is alright as long as we are losing more and more supply from Iran and Venezuela. But what if those supplies come back into the market while US shale production growth is booming at the same time? Thus better to be safe than sorry and keep the oil price at around $65/bl and US shale oil activity at medium temperature.

The market will lose some 0.5 – 1.0 m bl/d. We cannot really know how much supply will now be lost from Iran. We don’t think it will go to zero but rather that exports will decline from 2.0 m bl/d in March to instead some 1.0 – 1.5 m bl/d along with increasing imports by China and “unknowns”. I.e. the market will lose some 0.5 – 1.0 m bl/d. OPEC+ can easily adjust for this. Saudi Arabia could actually do it alone.

Saudi Arabia (OPEC+) in very good control of the market. OPEC+ in general and Saudi Arabia specifically will have a very good handle of the supply situation of the oil market. I.e. Saudi will put current cuts partially back into the market and can then cut again at a later time instead.

John Bolton aiming for Iran regime shift. It has been stated that Donald Trump does not know what he want to achieve in the Middle East but that John Bolton does: a regime shift. The zero waivers is a victory for John Bolton’s politics. It increases the risk for turmoil in the Middle East.

A higher oil price is good for the US. Donald Trump has for a long time tried to aim for a low oil price in support of the US consumer and his core voters. His economic advisors have however this spring argued that a high oil price is now increasingly positive for the US economy as a whole as it is now increasingly becoming a net oil exporter. The negative for the consumers is increasingly outweighed by the positives for the oil producers. Thus Donald going for no waivers means that Donald is now increasingly siding with the producers rather than the consumers.

A more fragile oil market balance and yet more supply from the US. Less oil from Iran and a higher oil price means more US shale oil drilling and more supply growth from the US. But we are also getting a more fragile oil market. Supply from Venezuela continues to decline while supply from Libya and Nigeria is unstable as well.

Crude quality matters – IMO 2020 and diesel. Global oil supply is losing more and more medium to heavy sour crude oil which instead is largely replaced by ultralight US shale oil supply. The former is rich on medium to heavy molecule chains where the heavy chains can be converted to medium. The ultralight is rich on gasoline and light products which cannot be converted to medium elements. Medium elements mean Diesel, Gasoil and Jet fuel. Due to new fuel regulations in global shipping from 1 January 2020 the global shipping fleet will consume a lot more diesel/Gasoil like molecules. So less supply of diesel/Gasoil rich crudes but more demand means yet stronger mid-dist cracks.

Medium sour crude is typically the crude Saudi Arabia and OPEC and Russia. So if the world is craving for more Diesel, Gasoil and Jet fuel it is also craving for more of this crude. It means that Saudi Arabia and Russia (and OPEC) are in very good control of the oil market, even better than headline numbers indicate due to quality issues.

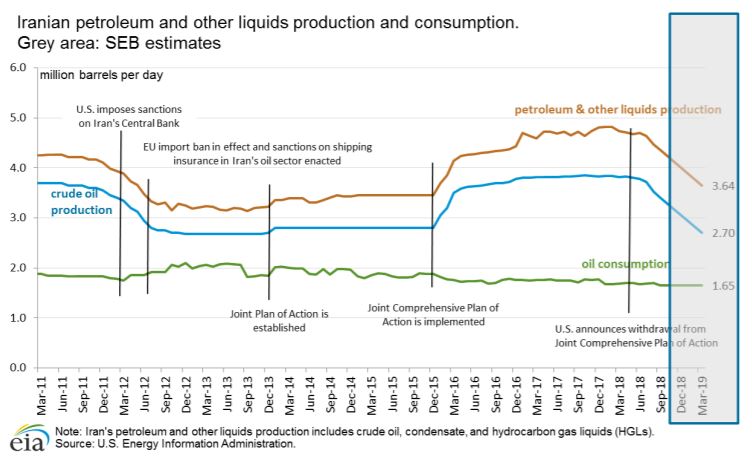

Ch1: Iran consumes some 1.7 m bl/d. In addition to 2.7 m bl/d of crude production in March 2019 it probably also produced some 0.95 m bl/d of condensates with total production of liquids of about 3.65 m bl/d. Exports thus probably stood at around 2.0 m bl/d in March which is also what tanker tracker data indicates. Exports are probably going to decline to about 1.0 to 1.5 m bl/d in May June

Ch2: Implied Iran hydro carbon liquids exports in m bl/d. US IEA data up to Sep 2018. Last data point estimated by SEB

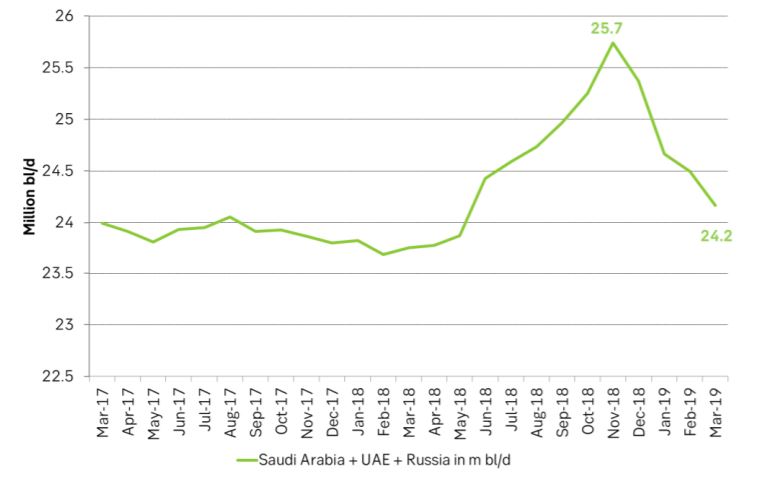

Ch3: Saudi Arabia, UAE and Russia can easily lift production by 1.5 m bl/d