Analys

SEB – Råvarukommentarer, 16 september 2013

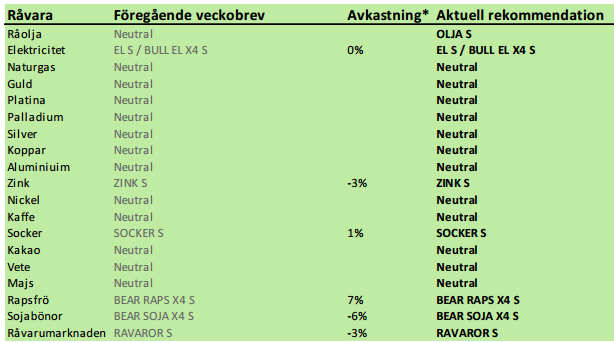

Rekommendationer

*) Avkastningen anges för 1:1 certifikaten där både BULL och 1:1 certifikat är angivna.

Inledning

Elmarknaden går kanske ner i veckan eftersom det ostadiga vädret har anlänt. Eftersom trenden är så tydligt positiv på marknaderna för kol och utsläppsrätter bör man ta ett sådant tillfälle i akt och köpa certifikat på el. Det kan bli en mycket bra affär.

De höga priserna på olja har fått oljeproducenter att sälja sin produkt på termin. Detta gör att avkastningen för dem som investerar i oljemarknaden via terminer erbjuds bra avkastning. Den rekyl nedåt som USA:s inställda angrepp på Syrien föranlett, är ett bra tillfälle att placera i oljemarknaden via certifikatet OLJA S.

USA:s jordbruksdepartement USDA publicerade sin månadsvisa uppdatering av utbud och efterfrågan på världsmarknaden. Den var negativ för priset på vete och majs, men neutral på soja. Sojapriset steg och det tror vi beror på att vissa aktörer lider av en psykologisk anspänning, snarare än något med grund i fakta. Vi upprepar vår säljrekommendation på soja och raps.

Två rapporter kom, i polemik med Czarnikows prognos om ett mindre överskott än väntat i sockermarknaden. Men kontentan var ändå att överskottet blir mindre än tidigare prognostiserats.

Råolja – Brent

Oljepriset föll tillbaka när det gick upp för alla – även de som inte läst det här veckobrevet – att USA inte skulle eskalera konflikten med Syrien. Som vi skrev för redan två veckor sedan var det uppenbart att USA:s president inte skulle fullfölja sitt hot. Syrienkonflikten skulle kunna ha påverkat producerande länder, så att oljepriset påverkats, men det finns även andra faktorer som faktiskt har en påverkan på oljepriset och som fått verka i det tysta. Libyens produktion har haft problem och efterfrågan har fått skjuts av den ekonomiska återhämtningen som sker i hela världen. Oljepriset befinner sig i en positiv trend rent tekniskt. Priset har gott stöd vid 110 dollar per fat, men motstånd vid 118 dollar ungefär. Fortfarande handlas oljepriset inom det prisintervall som varit rådande sedan tre år tillbaka.

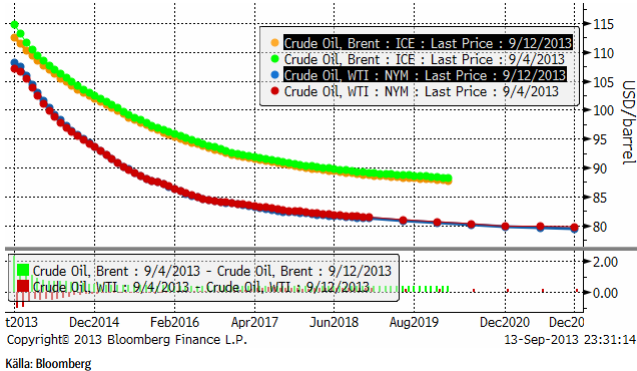

Terminskurvorna för Brent (den översta) och den av lager- och transportkapacitet strypta marknaden för West Texas Intermediate ligger lite lägre.

Tidningen Energy Risk skrev i fredags en artikel om att de höga priserna lockat fram en våg av prissäkring från amerikanska oljebolag. Dessa säljer framtida produktion på termin och lyckas på så sätt minska risken i sin verksamhet. De gör detta trots att terminspriserna är lägre än spotpriserna därför att de vinner i minskad osäkerhet. De är med andra ord villiga att betala försäkringspremien till dem som köper terminerna – och bär risken i deras ställe.

För råvaruinvesterare är den här rabatten nu väldigt attraktiv. Man kan tjäna ca 7 – 10% extra på att äga råoljeterminer.

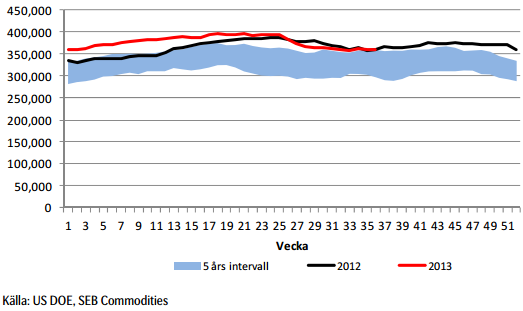

Råoljelagren fortsätter att minska i USA.

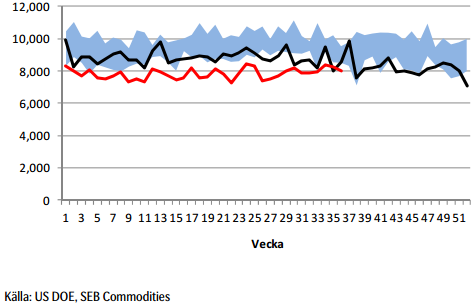

Importen år 2013 (röd) minskade i den senaste rapporten från DOE.

När nu priset fallit tillbaka och rabatten på terminer är så attraktiv, tycker vi att det är ett bra tillfälle att komma in i den lönsamma oljemarknaden och rekommenderar köp av OLJA S. Det är framförallt rabatten på terminerna vi vill komma åt och därför föredrar vi OLJA S framför t ex BULL OLJA X4 S.

Elektricitet

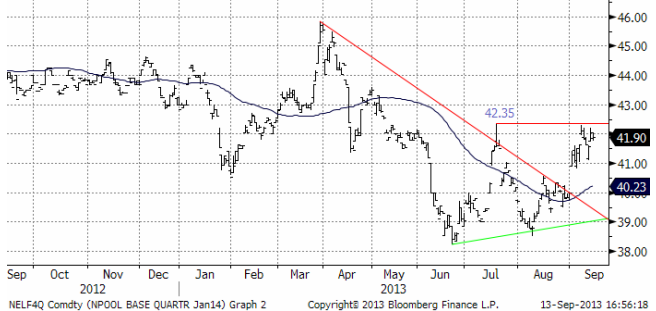

Nedan ser vi prisdiagrammet på det första kvartalets 2014 kontrakt. Det är det kontrakt som är underliggande för certifikaten sedan början på månaden.

Man har gjort försök att få igång O3:an i veckan, utan att lyckas. Finnarna har inte heller fått igång sin. Kärnkraften går just nu på halva sin installerade kapacitet.

Väderleksprognoserna visar fortsatt blött. Det ostadiga vädret väntas komma nu.

Tekniskt har motståndet vid 41.35 hållit stånd. Det är inte otänkbart att blötare väder och kärnkraftverk som kommer igång, kan få priset att rekylera ner från fredagens stängningspris på 41.90 euro per MWh. En sådan rekyl betraktar vi som ett utmärkt köptillfälle.

Som nämnt ovan, har den nordiska kärnkraften fortsätta problem. I fredags producerades endast 51% av den installerade kapaciteten. OKG kommer att starta om Oskarshamn 3 klockan 15:00 på tisdag. Reaktorn har varit avstängd sedan den 1 september och tre försök att återstarta den har misslyckats. OKG har skjutit upp starten av Orskarshamn 1 från i torsdags till måndagen. Reaktorn har varit avstängd sedan den 9 juli pga ventilproblem. PVO kommer att återstarta Olkiluoto 2 på tisdag. Reaktorn stängdes i måndags förra veckan pga en överhettad generator. Ringhals 2, Ringhals 3, Orskarshamn 2 och Loviisa 2 var avstängda för det årliga underhållet.

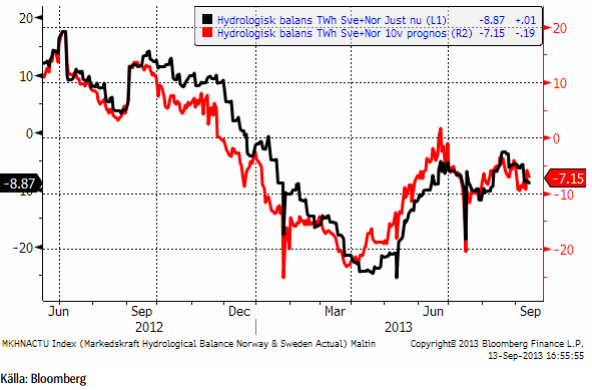

Hydrologisk balans har fortsatt att försämras, särskilt prognosen.

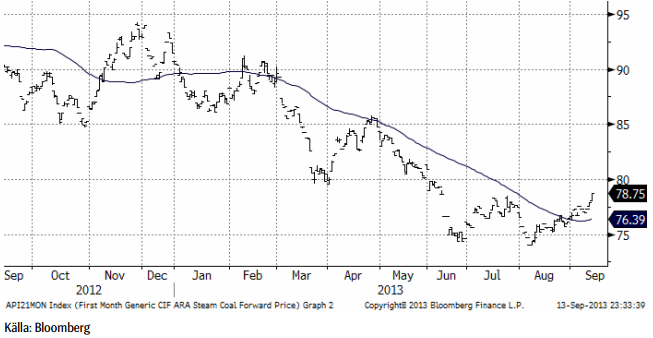

Marginalkostnaden för att producera el bestäms av priset på kol och priset på utsläppsrätter. Nedan ser vi priset på utsläppsrätter i euro / ton. Notera den fortsatta prisuppgången.

Nedan ser vi terminspriset för månaden, på energikol i Rotterdam. Vi ser att marknaden har vänt uppåt. Trenden är bruten. Detta har indirekt, men helt säkert, en påverkan på prisnivån på nordisk elektricitet. Vi väntar oss en fortsatt återhämtning i kolpriset åtminstone upp till 95 dollar per ton. Och därmed motsvarande prisuppgång på nordisk elektricitet. Dessutom tror vi på en procentuellt sett väsentligt högre prisuppgång på utsläppsrätter.

Vi rekommenderar alltså köp av el, t ex EL S eller BULL EL X4 S.

Naturgas

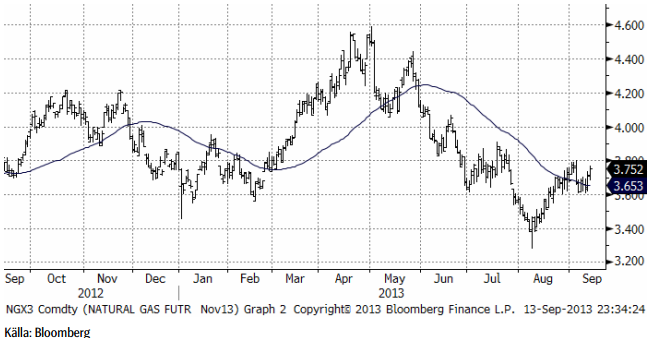

Naturgaspriset studsade på 3.60 i veckan och stängde i fredags på 3.75. Tekniskt motstånd ligger på 3.80.

Vi har neutral rekommendation.

Guld & Silver

Guldpriset föll ned till stödet på 1300 dollar per troy uns, efter att ha brutit stödet för uppgången från juni / juli. Vi har tidigare sagt att vi betraktar hela uppgången från juni / juli som en rekyl mot den fallande trenden. Goldman Sachs publicerade en rapport i fredags, där de säger att priset på guld kan falla så långt som till 1000 dollar per troy uns. Goldman Sachs har emellertid en tendens att göra prognoser som påminner om rena extrapoleringar av trender. Det går sällan så långt som Goldman Sachs analytiker har förutspått. Vi delar dock vyn att priset på guld förmodligen kommer att falla vidare. I det riktigt korta perspektivet noterar vi dock att 1300 dollar är ett starkt tekniskt stöd, varifrån marknaden kan samla kraft och göra ett nytt försök uppåt.

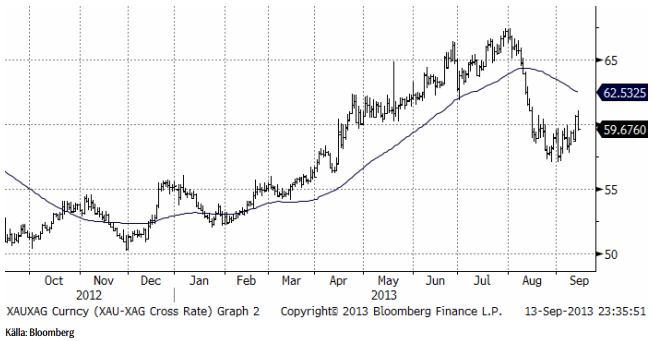

Nedan ser vi kursdiagrammet för silver i dollar per troy ounce. Då och då ser man att handlare hänger upp sig på 55-dagars glidande medelvärde och priset studsade i fredags precis på den nivå som det ligger på, som vi ser i diagrammet nedan. Går priset under den nivån, kan priset gå till 20 dollar, annars kan det gå pp mot 24 dollar. Notera att toppen i slutat av augusti inte lyckades bryta motståndet för den fallande pristrenden. Vi är alltså fortfarande i en bear market för silver.

Nedan ser vi kvoten mellan guldpriset och silverpriset.

Silverpriset har i den allmänna prisnedgången, i vanlig ordning, fallit mer än guld.

Vi fortsätter att vara neutrala guld och silver och skulle inte vilja köpa någon av dem idag.

Platina & Palladium

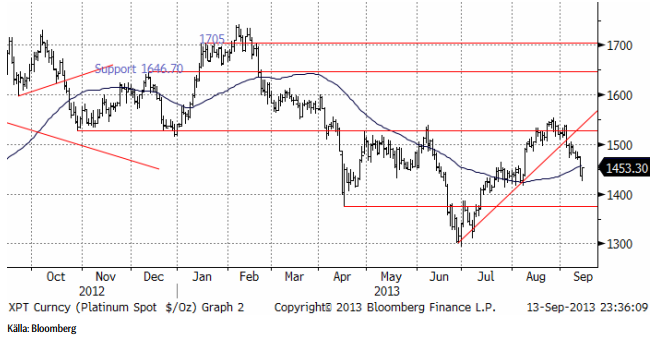

Förra veckan skrev vi att platina då brutit stödet för uppgången. Resultatet ser vi nu, där priset fallit ordentligt, ned till nivåer som utgjorde stöd under juli – augusti. Det vore inte otänktbart med en rekyl uppåt i det riktigt korta perspektivet, men vi ser inte detta som en trendvändning, utan som en rekyl i en fallande pristrend.

Nedan ser i kvoten mellan platina och guld. I slutet av förra veckan steg platina i förhållande till guld, men vi ser detta som en kortsiktig ”blip” och tror att platina kan falla tillbaka.

Palladiumpriset är håller på att bryta ner från den triangel vi skrivit om tidigare. Kursfallet kan bli stort.

Vi är för närvarande neutrala platina och palladium, men om palladium skulle falla bara något lite ytterligare, skulle vi vilja haka på och ta en kort position via BEAR PALLAD X4 S. Vi skulle absolut inte vilja köpa någon av dem.

Koppar

Priset på koppar var i princip oförändrat i veckan som gick. Trenden är nedåtriktad, men priset är förhållandevis lågt. Vi fortsätter med neutral vy.

Det är en svårtolkad bild och vi rekommenderar neutral position.

Aluminium

Förra veckan noterade en marginell prisnedgång som stannade på 1812 dollar per ton. Stöd finns vid 1800 dollar. Går priset under den nivån skulle vi vilja vara korta, dvs köpta BEAR ALU X4 S.

Vi har neutral rekommendation, tidigare köp.

Zink

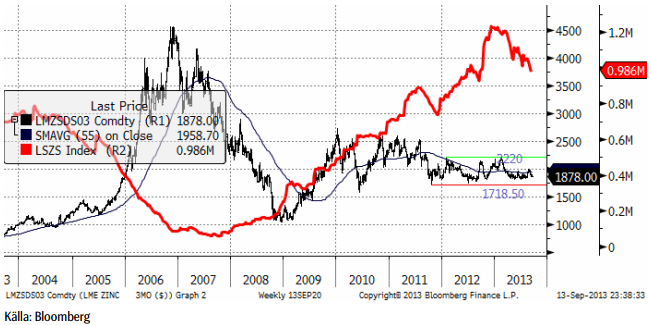

Priset på zink har i nästan två års tid legat inom ett intervall mellan 1718.50 dollar per ton och 2200 dollar per ton, som vi ser nedan. Den röda linjen visar lagren av zink vid LME. Vi ser att marknaden börjat komma mer i balans. Detta fortsatte i veckan som gick. De rekordstora lagren har börjat minska. Det finns en förväntan om en stor inleverans till tredje onsdagen i september, den 18 september, eftersom detta skett både i maj och i juli. Analytiker har noterat att detta kan hänga ihop med lagerfinansieringsaffärer utanför LME-systemet.

Den senaste ILZG-rapporten indikerar dock att det finns en starkare efterfrågan och att balansen förbättras, vilket gör ett aluminium-scenario mindre sannolikt. Stöd finns vid 1850 dollar per ton, som vi tror att marknaden håller sig över.

Vi fortsätter med en försiktig köprekommendation, av ZINK S.

Nickel

Nickelpriset följde den generella tendensen under veckan och stängde på veckans lägsta nivå, där priset balanserar på det tekniska stödet 13675 dollar per ton. Marknaden förväntar sig en återhämtning av fysisk efterfrågan under årets sista kvartal, huvudsakligen drivet av Kina. Produktionen av rostfritt stål steg med 11% i Kina under det första halvåret i år, huvudsakligen från 300-serien, som innehåller 8 – 10% nickel, enligt CRU. Efter en långsammare takt under det tredje kvartalet, tror CRU på en återhämtning under det fjärde. Det skulle innebära en ökning av efterfrågan på 13% i årstakt. Med det stora lager som finns skulle detta verkligen behövas för att få marknaden i balans. En faktor som skulle kunna leda till ökad efterfrågan är den premie för nickel i nickel pig iron vi nämnde i förra veckans brev. Att vi ser att cancellerade warrants (lagerbevis) vid LME nu uppgår till 20% av LME:s lager, kan vara ett tecken på ökad efterfrågan på primärnickel. Nya ”cancellations” rapporteras från Malaysia, där allt nickel i lager har levererats in från Kina. Det är nu möjligt att det här lagret går tillbaka till Kina. Det finns alltså några tecken på förbättringar i marknadsläget, men nickel har förmodligen en lång väg att gå innan vi ser en rejäl återhämtning.

[box]SEB Veckobrev Veckans råvarukommentar är producerat av SEB Merchant Banking och publiceras i samarbete och med tillstånd på Råvarumarknaden.se[/box]

Disclaimer

The information in this document has been compiled by SEB Merchant Banking, a division within Skandinaviska Enskilda Banken AB (publ) (“SEB”).

Opinions contained in this report represent the bank’s present opinion only and are subject to change without notice. All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, expressed or implied, is made with respect to the completeness or accuracy of its contents and the information is not to be relied upon as authoritative. Anyone considering taking actions based upon the content of this document is urged to base his or her investment decisions upon such investigations as he or she deems necessary. This document is being provided as information only, and no specific actions are being solicited as a result of it; to the extent permitted by law, no liability whatsoever is accepted for any direct or consequential loss arising from use of this document or its contents.

About SEB

SEB is a public company incorporated in Stockholm, Sweden, with limited liability. It is a participant at major Nordic and other European Regulated Markets and Multilateral Trading Facilities (as well as some non-European equivalent markets) for trading in financial instruments, such as markets operated by NASDAQ OMX, NYSE Euronext, London Stock Exchange, Deutsche Börse, Swiss Exchanges, Turquoise and Chi-X. SEB is authorized and regulated by Finansinspektionen in Sweden; it is authorized and subject to limited regulation by the Financial Services Authority for the conduct of designated investment business in the UK, and is subject to the provisions of relevant regulators in all other jurisdictions where SEB conducts operations. SEB Merchant Banking. All rights reserved.

The latest weekly report from the US DOE showed a substantial drawdown across key petroleum categories, adding more upside potential to the fundamental picture.

Commercial crude inventories (excl. SPR) fell by 5.8 million barrels, bringing total inventories down to 415.1 million barrels. Now sitting 11% below the five-year seasonal norm and placed in the lowest 2015-2022 range (see picture below).

Product inventories also tightened further last week. Gasoline inventories declined by 2.1 million barrels, with reductions seen in both finished gasoline and blending components. Current gasoline levels are about 3% below the five-year average for this time of year.

Among products, the most notable move came in diesel, where inventories dropped by almost 4.1 million barrels, deepening the deficit to around 20% below seasonal norms – continuing to underscore the persistent supply tightness in diesel markets.

The only area of inventory growth was in propane/propylene, which posted a significant 5.1-million-barrel build and now stands 9% above the five-year average.

Total commercial petroleum inventories (crude plus refined products) declined by 4.2 million barrels on the week, reinforcing the overall tightening of US crude and products.

A classic case of “buy the rumor, sell the news” played out in oil markets, as Brent crude has dropped sharply – down nearly USD 10 per barrel since yesterday evening – following Iran’s retaliatory strike on a U.S. air base in Qatar. The immediate reaction was: “That was it?” The strike followed a carefully calibrated, non-escalatory playbook, avoiding direct threats to energy infrastructure or disruption of shipping through the Strait of Hormuz – thus calming worst-case fears.

After Monday morning’s sharp spike to USD 81.4 per barrel, triggered by the U.S. bombing of Iranian nuclear facilities, oil prices drifted sideways in anticipation of a potential Iranian response. That response came with advance warning and caused limited physical damage. Early this morning, both the U.S. President and Iranian state media announced a ceasefire, effectively placing a lid on the immediate conflict risk – at least for now.

As a result, Brent crude has now fallen by a total of USD 12 from Monday’s peak, currently trading around USD 69 per barrel.

Looking beyond geopolitics, the market will now shift its focus to the upcoming OPEC+ meeting in early July. Saudi Arabia’s decision to increase output earlier this year – despite falling prices – has drawn renewed attention considering recent developments. Some suggest this was a response to U.S. pressure to offset potential Iranian supply losses.

However, consensus is that the move was driven more by internal OPEC+ dynamics. After years of curbing production to support prices, Riyadh had grown frustrated with quota-busting by several members (notably Kazakhstan). With Saudi Arabia cutting up to 2 million barrels per day – roughly 2% of global supply – returns were diminishing, and the risk of losing market share was rising. The production increase is widely seen as an effort to reassert leadership and restore discipline within the group.

That said, the FT recently stated that, the Saudis remain wary of past missteps. In 2018, Riyadh ramped up output at Trump’s request ahead of Iran sanctions, only to see prices collapse when the U.S. granted broad waivers – triggering oversupply. Officials have reportedly made it clear they don’t intend to repeat that mistake.

The recent visit by President Trump to Saudi Arabia, which included agreements on AI, defense, and nuclear cooperation, suggests a broader strategic alignment. This has fueled speculation about a quiet “pump-for-politics” deal behind recent production moves.

Looking ahead, oil prices have now retraced the entire rally sparked by the June 13 Israel–Iran escalation. This retreat provides more political and policy space for both the U.S. and Saudi Arabia. Specifically, it makes it easier for Riyadh to scale back its three recent production hikes of 411,000 barrels each, potentially returning to more moderate increases of 137,000 barrels for August and September.

In short: with no major loss of Iranian supply to the market, OPEC+ – led by Saudi Arabia – no longer needs to compensate for a disruption that hasn’t materialized, especially not to please the U.S. at the cost of its own market strategy. As the Saudis themselves have signaled, they are unlikely to repeat previous mistakes.

Conclusion: With Brent now in the high USD 60s, buying oil looks fundamentally justified. The geopolitical premium has deflated, but tensions between Israel and Iran remain unresolved – and the risk of missteps and renewed escalation still lingers. In fact, even this morning, reports have emerged of renewed missile fire despite the declared “truce.” The path forward may be calmer – but it is far from stable.

Analys

A muted price reaction. Market looks relaxed, but it is still on edge waiting for what Iran will do

Brent crossed the 80-line this morning but quickly fell back assigning limited probability for Iran choosing to close the Strait of Hormuz. Brent traded in a range of USD 70.56 – 79.04/b last week as the market fluctuated between ”Iran wants a deal” and ”US is about to attack Iran”. At the end of the week though, Donald Trump managed to convince markets (and probably also Iran) that he would make a decision within two weeks. I.e. no imminent attack. Previously when when he has talked about ”making a decision within two weeks” he has often ended up doing nothing in the end. The oil market relaxed as a result and the week ended at USD 77.01/b which is just USD 6/b above the year to date average of USD 71/b.

Brent jumped to USD 81.4/b this morning, the highest since mid-January, but then quickly fell back to a current price of USD 78.2/b which is only up 1.5% versus the close on Friday. As such the market is pricing a fairly low probability that Iran will actually close the Strait of Hormuz. Probably because it will hurt Iranian oil exports as well as the global oil market.

It was however all smoke and mirrors. Deception. The US attacked Iran on Saturday. The attack involved 125 warplanes, submarines and surface warships and 14 bunker buster bombs were dropped on Iranian nuclear sites including Fordow, Natanz and Isfahan. In response the Iranian Parliament voted in support of closing the Strait of Hormuz where some 17 mb of crude and products is transported to the global market every day plus significant volumes of LNG. This is however merely an advise to the Supreme leader Ayatollah Ali Khamenei and the Supreme National Security Council which sits with the final and actual decision.

No supply of oil is lost yet. It is about the risk of Iran closing the Strait of Hormuz or not. So far not a single drop of oil supply has been lost to the global market. The price at the moment is all about the assessed risk of loss of supply. Will Iran choose to choke of the Strait of Hormuz or not? That is the big question. It would be painful for US consumers, for Donald Trump’s voter base, for the global economy but also for Iran and its population which relies on oil exports and income from selling oil out of that Strait as well. As such it is not a no-brainer choice for Iran to close the Strait for oil exports. And looking at the il price this morning it is clear that the oil market doesn’t assign a very high probability of it happening. It is however probably well within the capability of Iran to close the Strait off with rockets, mines, air-drones and possibly sea-drones. Just look at how Ukraine has been able to control and damage the Russian Black Sea fleet.

What to do about the highly enriched uranium which has gone missing? While the US and Israel can celebrate their destruction of Iranian nuclear facilities they are also scratching their heads over what to do with the lost Iranian nuclear material. Iran had 408 kg of highly enriched uranium (IAEA). Almost weapons grade. Enough for some 10 nuclear warheads. It seems to have been transported out of Fordow before the attack this weekend.

The market is still on edge. USD 80-something/b seems sensible while we wait. The oil market reaction to this weekend’s events is very muted so far. The market is still on edge awaiting what Iran will do. Because Iran will do something. But what and when? An oil price of 80-something seems like a sensible level until something do happen.

Nickelmarknaden under fortsatt press – överskott väntas bestå till 2026

Westinghouse planerar tio nya stora kärnreaktorer i USA – byggstart senast 2030

Eurobattery Minerals förvärvar majoritet i spansk volframgruva

USA ska införa 50 procent tull på koppar

Ryska staten siktar på att konfiskera en av landets största guldproducenter

Mahvie Minerals växlar spår – satsar fullt ut på guld

A muted price reaction. Market looks relaxed, but it is still on edge waiting for what Iran will do

Jonas Lindvall är tillbaka med ett nytt oljebolag, Perthro, som ska börsnoteras

Oljan, guldet och marknadens oroande tystnad

Domstolen ger klartecken till Lappland Guldprospektering

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanMahvie Minerals växlar spår – satsar fullt ut på guld

-

Analys4 veckor sedan

A muted price reaction. Market looks relaxed, but it is still on edge waiting for what Iran will do

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanJonas Lindvall är tillbaka med ett nytt oljebolag, Perthro, som ska börsnoteras

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOljan, guldet och marknadens oroande tystnad

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanDomstolen ger klartecken till Lappland Guldprospektering

-

Analys3 veckor sedan

Tightening fundamentals – bullish inventories from DOE

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanRyska staten siktar på att konfiskera en av landets största guldproducenter

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSommarvädret styr elpriset i Sverige