Nyheter

David Hargreaves on Precious Metals, week 26 2014

Gold continues to nudge ahead as the Iraq conflict intensifies; we can expect little else. America has its finger on the trigger even as it and the UK dither over increases in interest rates. So lots of incentives to stay with the metal right now. Platinum saw the end of the RSA miners’ strike, after 24 weeks, so an inevitable price drift follows.

Silver, as ever, is hostage to the two whilst the short-lived palladium bubble will surely pop. We are into politico-economic land.

Gold goes down when interest rates rise, normally. Gold goes up when people start throwing things at each other, usually. That is how we see it now. Both features are behind the metal but this can quickly change.

The stock market has not bought into it fully yet:

We are not alone in believing this rally cannot last. Bloomberg thinks so too. Begging the question as to whether Fed. Chair Janet Yellen and Bank of England governor Mark Carney are having an affair, we witness that they are certainly holding hands on interest rates at least. They will stay low. So Bloomberg says its consensus pull goes for a gold price of $1240 in Q4 and $1300 in Q1 2015. Then it opts for a shilly-shally of $1225-1270. It also notes that daily London trading volumes were down, 16% in the 4 months through to April to c. 18.3Moz per day and the least since 2010. US domestic gold buying is also down. The sale of one-ounce Eagle coins was 252.500 in the 6 months to June, 60% on like 2013. Holdings in global ETFs are at their lowest since 2009. Clearly America believes in economic growth, not gold.

ETFs and all that (Exchange Traded Funds) were a good idea. Have a stake in a physical metal without having to pay VAT, store and insure the stuff, but not take a risk on share prices. So they became popular. Dangerous, too. These funds hold thousands of tonnes and the managers can decide on when to sell. Not like an individual rattling a few Krugerrand. They became popular in China and India where locals pay a premium on the gold price. The migration of gold and silver from West to East has been notable. But now, in China at least, the music may have stopped awhile so decreasing premiums attach. What it all points to is an increase in volatility on a short term basis.

Peru and gold. In fact, Peru and what else? That large South American country is major to copper (8% of world output), silver (16%), zinc (12%) and lead (6%). Its importance rests in the fact that most of its output is exported, much to China. But it is troubled politically. A largely peasant population is easily swayed to the communist persuasion and this has been behind Newmont Mining (NYSE) the world’s No 2 producer, halting the major Conga project there. It sits in the mineral-rich Cajamarca region where political tensions run high. Now the regional president, one G Santos, has just been jailed for 14 months whilst a corruption enquiry takes place. G.S. did not think the Conga miner would do the peasants any good.

WIM says: We presently pre-occupy with Africa, but South America simmers, too. Little wonder the safety of North America, Europe and Australia looks attractive.

Silver is on a charm offensive. It has breached $21/oz on the upside but to remind, in late 2012, it bettered $30. The ratio to gold rests at c.62:1, where as it has seen 55:1. The metal’s rampers are coming out of the woodwork but we ask, why? We conservatively believe there to be about 9,000,000 tonnes of silver on surface, being added to at 20,000 tonnes annually. It has industrial uses, all capable of substitution if the price is right. The only silver corner of recent years, the Bunker-Hunt endeavour of 1980-81, was carefully orchestrated but short-lived. Little chance of a replay now.

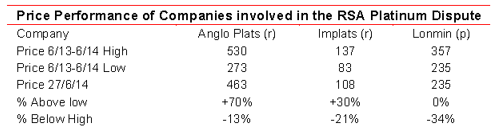

Platinum celebrated the end of the longest and costliest strike in South Africa’s history with militant union AMCU declaring “a victory”. Well, they would, wouldn’t they? Over the week, the price edged up a notch, $23 or 1.6% to $1479/oz. What now? To the immediate we have the share prices of the three involved companies:

Not bad when you have suffered a six-months outage of production. There were threats of cash calls, but none materialised. Surface stocks, including recycled material, held out. Now for the aftermath. We discuss it more broadly in this week’s leader and warn it will be a telling one (the aftermath, not the leader). This strike has done the country lasting damage and we suspect that both Angloplats and Lonmin are looking for a new home. What will need close examination is the true supply-demand position on the metal’s availability. Mine production will flow again so we can only see the price being under pressure.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.

Nyheter

Hur säkrar vi Sveriges tillgång till kritiska metaller och mineral i en ny geopolitisk verklighet?

När världsläget förändras ställs Europas beroende av metaller och mineral på sin spets. Geopolitiska spänningar, handelskonflikter och ett mer oförutsägbart USA gör att vi inte längre kan ta gamla allianser för givna. Samtidigt kontrolleras en stor del av de kritiska råvarorna vi är beroende av av andra makter – inte minst Kina. Vad händer med Sveriges industriella förmåga i ett läge där importen stryps? Hur påverkas försvarsindustrin av Kinas exportrestriktioner? Är EU:s nya råvarupolitik tillräcklig för att minska sårbarheten – eller krävs ytterligare statliga insatser och beredskapslagring? Svemin anordnade den 25 juni ett seminarium som bestod av bestod av deltagare från myndigheter, politik och industri. Man diskuterar Sveriges och EU:s strategiska vägval i en ny global verklighet – och vad som krävs för att säkra tillgången till metaller när vi behöver dem som mest.

Lundin Mining är bolaget i Lundin-sfären som satsar stort på Vicuña-projektet i Argentina. Det ska lyfta Lundin Mining till att bli en av de tio största kopparproducenterna i världen skriver Affärsvärlden och upprepar sin köprekommendation för aktien.

”Även om en framgång inte är på förhand given tror vi att Vicuña har goda chanser att bli bra. Vi förnyar vårt köpråd för Lundin Mining”

Enligt Lundin Minings ledning kommer man att klara att finansiera sin del av investeringarna i Vicuña genom det löpande kassaflödet som man förväntar sig ska bli omkring 5 miljarder dollar kommande fem år i kombination med lån.

Många verksamheter tar nu ett sommaruppehåll och ute värmer solen, det är gott om vatten och vinden blåser. Lägre efterfrågan på el och goda förutsättningar för kraftproduktionen höll ner elpriserna under juni.

Elpriset på den nordiska elbörsen Nord Pool (utan påslag och exklusive moms) i elområde 1 och 2 (Norra Sverige) blev för juni 3,05 respektive 4,99 öre/kWh, vilket är rekordlågt och de lägsta på minst 25 år.

– Elpriset påverkas av en rad faktorer men vädret väger tyngst. På sommaren minskar efterfrågan på el och många verksamheter har ett uppehåll. Detta tillsammans med goda förutsättningar inom kraftproduktionen påverkar elpriset nedåt, säger Jonas Stenbeck, privatkundschef Vattenfall Försäljning Norden.

Den hydrologiska balansen, måttet för att uppskatta hur mycket vatten som finns lagrat ovanför kraftstationerna, ligger över normal nivå, särskilt i norra Skandinavien. Tillgängligheten för kärnkraften i Norden är just nu 82 procent av installerad effekt.

– De goda nordiska produktionsförutsättningarna gör elpriserna mindre känsliga för förändringar i omvärlden, säger Jonas Stenbeck.

Priserna på olja och gas kan dock ändras snabbt med anledning av en turbulent omvärld. På kontinenten har efterfrågan på gas sjunkit och nytt solkraftsrekord för Tyskland sattes på midsommarafton med en produktion på 52,5 GW.

– Många av de goda elvanor vi skaffade oss under elpriskrisen verkar leva kvar och gör nytta även på sommaren. De svenska hushållens elförbrukning under 2024 var faktiskt den lägsta detta millenium, säger Jonas Stenbeck.

| Medelspotpris | Juni 2024 | Juni 2025 |

| Elområde 1, Norra Sverige | 24,04 öre/kWh | 3,05 öre/kWh |

| Elområde 2, Norra Mellansverige | 24,04 öre/kWh | 4,99 öre/kWh |

| Elområde 3, Södra Mellansverige | 27,27 öre/kWh | 22,79 öre/kWh |

| Elområde 4, Södra Sverige | 62,70 öre/kWh | 40,70 öre/kWh |

Hur säkrar vi Sveriges tillgång till kritiska metaller och mineral i en ny geopolitisk verklighet?

Lundin Mining ska bli en av de tio största kopparproducenterna i världen

Sommarvädret styr elpriset i Sverige

Samtal om flera delar av råvarumarknaden

Tightening fundamentals – bullish inventories from DOE

Stor uppsida i Lappland Guldprospekterings aktie enligt analys

Silverpriset släpar efter guldets utveckling, har mer uppsida

Uppgången i oljepriset planade ut under helgen

Låga elpriser i sommar – men mellersta Sverige får en ökning

Mahvie Minerals växlar spår – satsar fullt ut på guld

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanStor uppsida i Lappland Guldprospekterings aktie enligt analys

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanSilverpriset släpar efter guldets utveckling, har mer uppsida

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUppgången i oljepriset planade ut under helgen

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanLåga elpriser i sommar – men mellersta Sverige får en ökning

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMahvie Minerals växlar spår – satsar fullt ut på guld

-

Analys3 veckor sedan

Analys3 veckor sedanVery relaxed at USD 75/b. Risk barometer will likely fluctuate to higher levels with Brent into the 80ies or higher coming 2-3 weeks

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanOljan, guldet och marknadens oroande tystnad

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanJonas Lindvall är tillbaka med ett nytt oljebolag, Perthro, som ska börsnoteras