Analys

Crude oil comment: Balancing act

Brent crude prices have experienced a decline this week, falling by approximately USD 1.80 per barrel from Monday’s opening, settling at USD 74.80 this morning. This marks one of the lowest price levels of 2025 to date, with an intraday dip reaching USD 74.15 per barrel on February 4th.

As highlighted in our previous report, crude oil prices are currently caught in a delicate balance between rising concerns over global demand growth and the potential for supply disruptions. On one side, fears surrounding an escalating trade war, with its negative impact on global growth, are putting downward pressure on the market. The persistent uncertainty surrounding tariffs and trade tensions – particularly between major economies – has raised expectations of a slowdown in business investment and consumer spending, which could dampen oil demand. Consequently, bearish sentiment is gaining traction.

On the other hand, the threat of supply disruptions, particularly from Iran, introduces an element of volatility that could quickly reverse market sentiment. This week, President Trump’s new actions aimed at intensifying pressure on Iran have raised expectations of a significant drop in the country’s oil exports. While such a move was anticipated, it still brings a fresh layer of uncertainty, further complicating the market’s outlook.

In essence, the market is now navigating between concerns about weakening global oil demand due to trade tensions and the possibility of sudden disruptions to Iranian oil supplies.

US Data (see attached data package):

U.S. oil production growth significantly slowed in the first eleven months of 2024, with crude and condensate output averaging 13.2 million barrels per day (b/d) – a modest increase from 12.9 million b/d in the same period in 2023 (+0.3 million b/d). However, this marks a sharp deceleration compared to previous years, where growth in 2023 and 2022 stood at 0.9 million b/d and 0.7 million b/d, respectively.

As global oil prices returned to pre-Ukraine war levels, U.S. producers shifted their focus from expanding output to managing costs. Inflation-adjusted front-month U.S. crude futures averaged USD 76 per barrel in 2024, down from USD 80 in 2023, reducing the incentive for further production increases. In line with this, the number of active oil rigs has also decreased, falling to 491 per week in 2024, down from 549 in 2023.

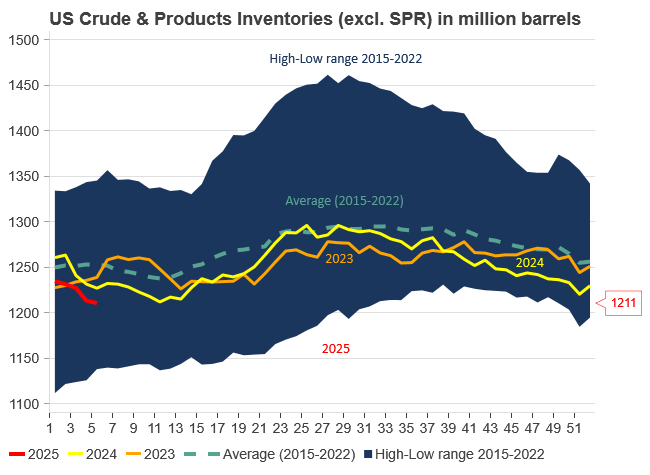

With OPEC+ partners, including Saudi Arabia, postponing planned production increases, U.S. commercial crude inventories dropped below the ten-year seasonal average by mid-2024. By January 2025, the inventory deficit had widened to 24 million barrels, or -5% below the average.

We anticipate that a further inventory depletion, which, coupled with expected sanctions on rival producers in Russia, Iran, and Venezuela, has driven a modest rise in futures prices so far in 2025.

The latest data from the EIA for the week ending January 31, 2025, presents a mixed picture. U.S. crude oil refinery inputs averaged 15.3 million b/d, a slight increase of 159 thousand b/d from the previous week.

Refinery runs also increased, with utilization partially recovering from the significant decline the prior week, rising back to 84.5% following the winter storm disruption. However, gasoline and distillate production both decreased, with gasoline output averaging 9.2 million b/d and distillates 4.6 million b/d. On the import side, crude oil imports rose by 467 thousand b/d to 6.9 million b/d, while gasoline and distillate imports remained modest.

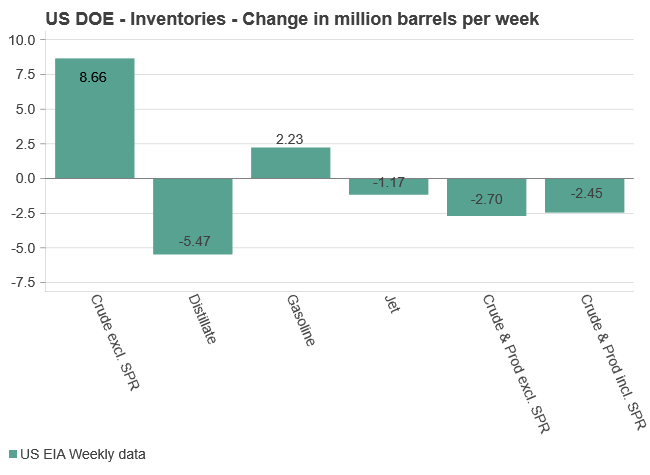

Of greater significance, commercial crude oil inventories increased more than expected by 8.7 million barrels (API = 5 mb), bringing total crude stockpiles to 423.8 million barrels. Despite this, inventories remain 5% below the five-year average for this time of year. In contrast, distillate (diesel) inventories fell sharply by 5.5 million barrels (API = -7 mb), now standing 12% below the five-year average. Gasoline inventories saw a modest increase of 2.2 million barrels (API = 5.4 mb), slightly above the five-year average. Overall, total commercial petroleum inventories decreased by 2.7 million barrels during the week.

Given this backdrop, we continue to see Brent crude prices balancing between concerns over weaker global oil demand due to trade tensions and the potential for sudden disruptions in Iranian oil supplies. Our forecast for Brent crude at USD 75 per barrel for 2025 remains intact, reflecting this ongoing volatility.

Analys

Oversold. Rising 1-3mth time-spreads. Possibly rebounding to USD 73.5/b before downside ensues

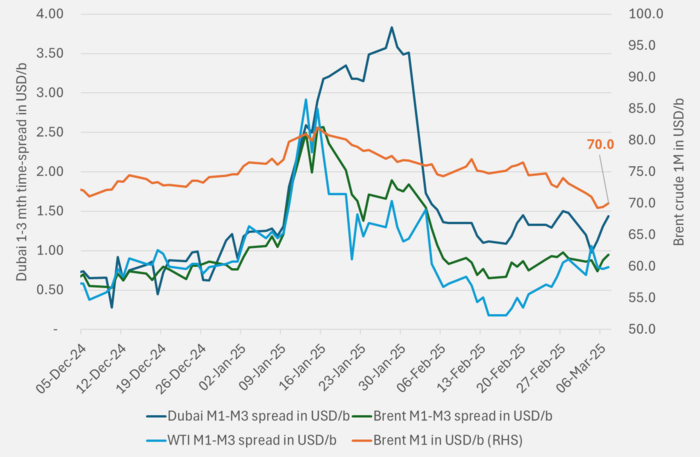

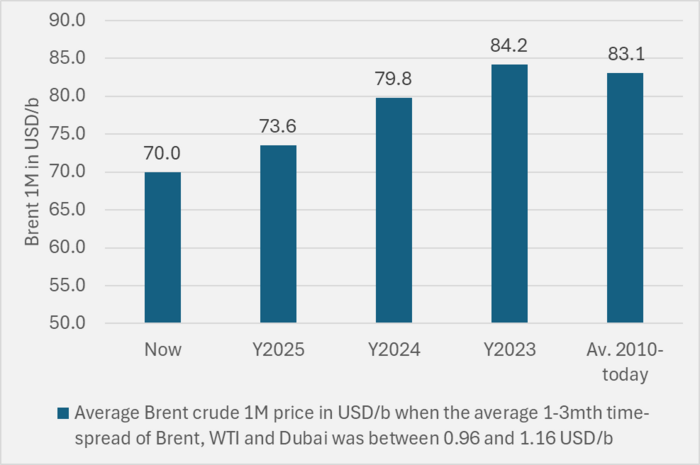

Brent was shaken ydy by the sharp selloff on Wednesday but ticking above the 70-line today. Brent crude inched up 0.2% to USD 69.46/b yesterday following the sharp selloff on Wednesday. The market was clearly still shaken by the sharp selloff on Wednesday when it then traded all the way down to USD 68.33/b and the lowest since Dec 2021. Market ydy didn’t quite dare to make any bets on the upside and basically stayed put. Brent is rising 0.8% this morning to USD 70/b staging a bit more confidence that the recent selloff was a little too much and a little too soon as surplus is not here quite yet. Stronger 1-3mths time-spreads today is also indicating the same. The Brent 1mth price is currently trading very soft versus the 1-3mth time-spreads. So, more rebound is definitely possible given both time-spreads and technically oversold market.

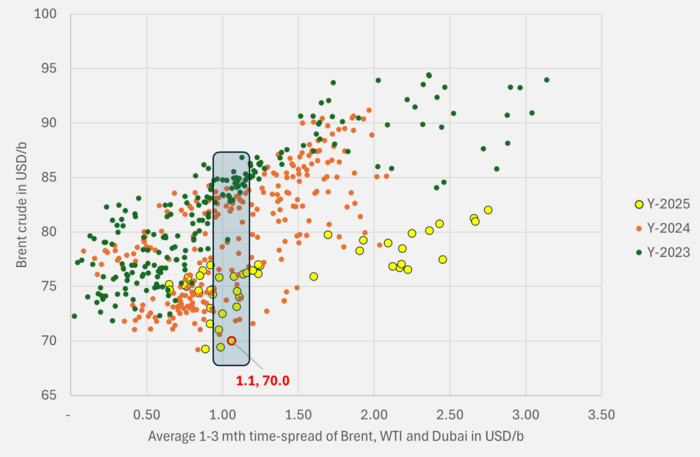

The current average 1-3mth time-spread of Brent, WTI and Dubai is rising to USD 1.06/b this morning. Looking at the relationship between the Brent 1M and these time-spreads so far this year we could possibly see the Brent 1M price rebound to USD 73.5/b given the level of the current time-spread and the fact that Brent is currently technically oversold.

Consolidation around the 70-line for a period, but message from OPEC+ is clear: lower oil price. The message from OPEC+ when they now have decided to lift production in April and into a period of surplus, is explicitly clear: lower oil prices. But the group is still acting in a highly controlled way. This is not a flash-crash but an adjustment. This is probably starting to dawn on the market today as it trades up above the 70-line again today following technically oversold territory. But back down below the 70-line again in the coming weeks and months seems the natural conclusion to draw following what OPEC+ now has decided to do. But given the current oversold state of Brent crude it seems likely that we’ll see some more consolidation around the 70-line before renewed bearish action ensues. Trump Tariff Turmoil of course adds a lot of bearish concerns for the US economy which naturally flavors over to crude oil as well.

Brent crude still very much in oversold territory. So, more consolidation around the 70-line seems likely before more bearish action continuous.

The 1-3 months time-spreads are rebounding a little today. Again, highlighting the fact that surplus is not here quite yet.

Brent 1M flat price is trading very soft vs. the 1-3mth time-spreads.

The average Brent 1M price so far this year when the 1-3mth time-spread has been in the current range is USD 73.6/b. Brent M1 rising to that level would be kind of neutral territory given the level of the time-spreds.

Hurt by US tariffs and more oil from OPEC+. Brent crude fell 2.1% yesterday to USD 71.62/b and is down an additional 0.9% this morning to USD 71/b. New tariff-announcements by Donald Trump and a decision by OPEC+ to lift production by 138 kb/d in April is driving the oil price lower.

The decision by OPEC+ to lift production is a deliberate decision to get a lower oil price. All the members in OPEC+ wants to produce more as a general rule. Their plan and hope for a long time has been that they could gradually revive production back to a more normal level without pushing the oil price lower. As such they have postponed the planned production increases time and time again. Opting for price over volume. Waiting for the opportunity to lift production without pushing the price lower. And now it has suddenly changed. They start to lift production by 138 kb/d in April even if they know that the oil market this year then will run a surplus. Donald Trump is the reason.

Putin, Muhammed bin Salman (MBS) and Trump all met in Riyadh recently to discuss the war in Ukraine. They naturally discussed politics and energy and what is most important for each and one of them. Putin wants a favorable deal in Ukraine, MBS may want harsher measures towards Iran while Trump amongst other things want a lower oil price. The latter is to appease US consumers to which he has promised a lower oil price. A lower oil price over the coming two years could be good for Trump and the Republicans in the mid-term elections if a lower oil price makes US consumers happy. And a powerful Trump for a full four years is also good for Putin and MBS.

This is not the opening of the floodgates. It is not the start of blindly lifting production each month. It is still highly measured and controlled. It is about lowering the oil price to a level that is acceptable for Putin, MBS, Trump, US oil companies and the US consumers. Such an imagined ”target price” or common denominator is clearly not USD 50-55/b. US production would in that case fall markedly and the finances of Saudi Arabia and Russia would hurt too badly. The price is probably somewhere in the USD 60ies/b.

Brent crude averaged USD 99.5/b, USD 82/b and USD 80/b in 2022, 2023 and 2024 respectively. An oil price of USD 65/b is markedly lower in the sense that it probably would be positively felt by US consumers. The five-year Brent crude oil contract is USD 67/b. In a laxed oil market with little strain and a gradual rise in oil inventories we would see a lowering of the front-end of the Brent crude curve so that the front-end comes down to the level of the longer dated prices. The longer-dated prices usually soften a little bit as well when this happens. The five-year Brent contract could easily slide a couple of dollars down to USD 65/b versus USD 67/b.

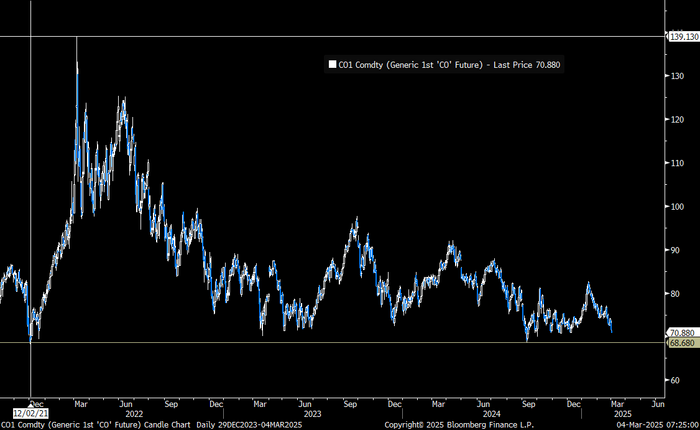

Brent crude 1 month contract in USD/b. USD 68.68/b is the level to watch out for. It was the lowpoint in September last year. Breaking below that will bring us to lowest level since December 2021.

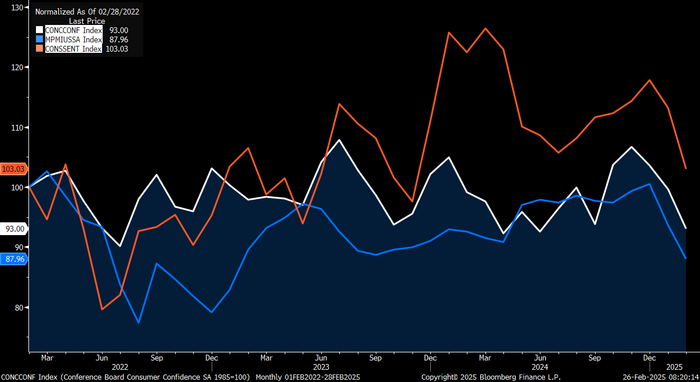

Sharply lower yesterday with negative US consumer confidence. Brent crude fell like a rock to USD 73.02/b (-2.4%) yesterday following the publishing of US consumer confidence which fell to 98.3 in February from 105.3 in January (100 is neutral). Intraday Brent fell as low as USD 72.7/b. The closing yesterday was the lowest since late December and at a level where Brent frequently crossed over from September to the end of last year. Brent has now lost both the late December, early January Trump-optimism gains as well as the Biden-spike in mid-Jan and is back in the range from this Autumn. This morning it is staging a small rebound to USD 73.2/b but with little conviction it seems. The US sentiment readings since Friday last week is damaging evidence of the negative fallout Trump is creating.

Evidence growing that Trump-turmoil are having negative effects on the US economy. The US consumer confidence index has been in a seesaw pattern since mid-2022 and the reading yesterday was reached twice in 2024 and close to it also in 2023. But the reading yesterday needs to be seen in the context of Donald Trump being inaugurated as president again on 20 January. The reading must thus be interpreted as direct response by US consumers to what Trump has been doing since he became president and all the uncertainty it has created. The negative reading yesterday also falls into line with the negative readings on Friday, amplifying the message that Trump action will indeed have a negative fallout. At least the first-round effects of it. The market is staging a small rebound this morning to USD 73.3/b. But the genie is out of the bottle: Trump actions is having a negative effect on US consumers and businesses and thus the US economy. Likely effects will be reduced spending by consumers and reduced capex spending by businesses.

Brent crude falling lowest since late December and a level it frequently crossed during autumn.

White: US Conference Board Consumer Confidence (published yesterday). Blue: US Services PMI Business activity (published last Friday). Red: US University of Michigan Consumer Sentiment (published last Friday). All three falling sharply in February. Indexed 100 on Feb-2022.

Oversold. Rising 1-3mth time-spreads. Possibly rebounding to USD 73.5/b before downside ensues

A deliberate measure to push oil price lower but it is not the opening of the floodgates

OPEC+ börjar öka oljeutbudet från april

Arctic Minerals är ett nordiskt mineralprospekterings- och gruvutvecklingsbolag

Våren inleds med snabba elprissvängningar

Glansen är tillbaka på guldet

Hemp Innovation skriver off-take-avtal för industriell hampafiber

Christian Kopfer om guld, olja och stål

Crude oil comment: Tariffs spark small reactions, but price gains hold steady

I mars offentliggör EU en lista på prioriterade gruvprojekt, betydelsefullt för Norra Kärr

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGlansen är tillbaka på guldet

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanHemp Innovation skriver off-take-avtal för industriell hampafiber

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanChristian Kopfer om guld, olja och stål

-

Analys4 veckor sedan

Crude oil comment: Tariffs spark small reactions, but price gains hold steady

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanI mars offentliggör EU en lista på prioriterade gruvprojekt, betydelsefullt för Norra Kärr

-

Analys2 veckor sedan

Stronger inventory build than consensus, diesel demand notable

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanChristian Kopfer om sällsynta jordartsmetaller, olja, guld, skog och stål

-

Nyheter3 veckor sedan

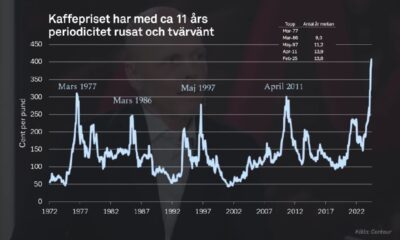

Nyheter3 veckor sedanPriset på kaffe kommer att falla tillbaka i år