Analys

Reloading the US ’oil-gun’ (SPR) will have to wait until next downturn

Brent crude traded down 0.4% earlier this morning to USD 91.8/b but is unchanged at USD 92.2/b at the moment. Early softness was probably mostly about general market weakness than anything specific to oil as copper is down 0.7% while European equities are down 0.3%. No one knows the consequences of what a ground invasion of Gaza by Israel may bring except that it will be very, very bad for Palestinians, for Middle East politics for geopolitics and potentially destabilizing for global oil markets. As of yet the oil market seems to struggle with how to price the situation with fairly little risk premium priced in at the moment as far as we can see. Global financial markets however seems to have a clearer bearish take on this. Though rallying US rates and struggling Chinese property market may be part of that.

The US has drawn down its Strategic Petroleum Reserves (SPR) over the latest years to only 50% of capacity. Crude oil prices would probably have to rally to USD 150-200/b before the US would consider pushing another 100-200 m b from SPR into the commercial market. As such the fire-power of its SPR as a geopolitical oil pricing tool is now somewhat muted. The US would probably happily re-load its SPR but it is very difficult to do so while the global oil market is running a deficit. It will have to wait to the next oil market downturn. But that also implies that the next downturn will likely be fairly short-lived and also fairly shallow. Unless of course the US chooses to forgo the opportunity.

The US has drawn down its Strategic Petroleum Reserves (SPR) to only 50% of capacity over the latest years. Most of the draw-down was in response to the crisis in Ukraine as it was invaded by Russia with loss of oil supply from Russia thereafter.

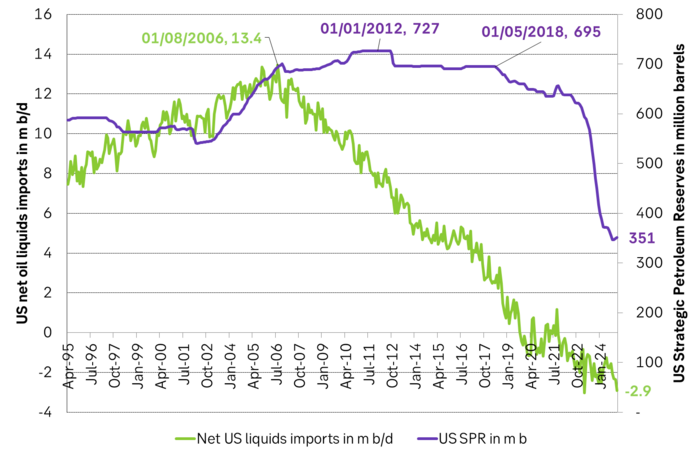

The US has however no problems with security of supply of crude oil. US refineries have preferences for different kinds of crude slates and as a result it still imports significant volumes of crude of different qualities. But overall it is a net exporter of hydrocarbon liquids. It doesn’t need all that big strategic reserves as a security of supply any more. Following the oil crisis in the early 70ies the OECD countries created the International Energy Agency where all its members aimed to have some 100 days of forward oil import coverage. With US oil production at steady decline since the 70ies the US reached a peak in net imports of 13.4 m b/d in 2006. As such it should have held an SPR of 1340 million barrels. It kept building its SPR which peaked at 727 m b in 2012. But since 2006 its net imports have been in sharp decline and today it has a net export of 2.9 m b/d.

Essentially the US doesn’t need such a sizable SPR any more to secure coverage of its daily consumption. As a result it started to draw down its SPR well before the Russian invasion of Ukraine in February 2022. But then of course it fell fast and is today at 351 m b or about 50% of capacity.

The US is the largest oil consumer in the world. As such it is highly vulnerable to the price level of oil. The US SPR today is much more of a geopolitical tool than a security of supply tool. It’s a tool to intervene in the global oil market. To intervene in the price setting of oil. The US SPR is now drawn down to 50% but it still holds a sizable amount of oil. But it is little in comparison to the firepower of OPEC. Saudi Arabia can lower its production by 1 m b/d for one year and it will have eradicated 365 million barrels in global oil inventories. And then it can the same the year after and then the year after that again.

The US has now fired one big bullet of SPR inventory draws. It really helped to balance the global oil market last year and prevented oil prices from going sky high. With 350 m b left in its SPR it can still do more if needed. But the situation would likely need to be way more critical before the US would consider pushing yet another 100-200 m b of oil from its SPR into the global commercial oil market. An oil price of USD 150-200/b would probably be needed before it would do so.

With new geopolitical realities the US probably will want to rebuild its SPR to higher levels as it is now an important geopolitical tool and an oil price management tool. But rebuilding the SPR now while the global oil market is running a deficit is a no-go as we see it.

An oil market downturn, a global recession, a global oil market surplus where OPEC no longer want to defend the oil price with reduced supply is needed for the US to be able to refill its SPR again unless it wants to drive the oil price significantly higher.

But this also implies that the next oil price downturn will likely be short-lived and shallow as the US will have to use that opportunity to rebuild its SPR. It’s kind off like reloading its geopolitical oil gun. If it instead decides to forgo such an opportunity then it will have to accept that its geopolitical maneuverability in the global oil market stays muted.

Net US oil imports in m b/d and US Strategic Petroleum Reserves (SPR) in million barrels. The US doesn’t need strategic petroleum reserves for the sake of security of supply any more. But it is a great geopolitical energy-tool to intervene in the price setting of oil in the global market place.

Analys

Brent edges higher as India–Russia oil trade draws U.S. ire and Powell takes the stage at Jackson Hole

Best price since early August. Brent crude gained 1.2% yesterday to settle at USD 67.67/b, the highest close since early August and the second day of gains. Prices traded to an intraday low of USD 66.74/b before closing up on the day. This morning Brent is ticking slightly higher at USD 67.76/b as the market steadies ahead of Fed Chair Jerome Powell’s Jackson Hole speech later today.

No Russia/Ukraine peace in sight and India getting heat from US over imports of Russian oil. Yesterday’s price action was driven by renewed geopolitical tension and steady underlying demand. Stalled ceasefire talks between Russia and Ukraine helped maintain a modest risk premium, while the spotlight turned to India’s continued imports of Russian crude. Trump sharply criticized New Delhi’s purchases, threatening higher tariffs and possible sanctions. His administration has already announced tariff hikes on Indian goods from 25% to 50% later this month. India has pushed back, defending its right to diversify crude sourcing and highlighting that it also buys oil from the U.S. Moscow meanwhile reaffirmed its commitment to supply India, deepening the impression that global energy flows are becoming increasingly politicized.

Holding steady this morning awaiting Powell’s address at Jackson Hall. This morning the main market focus is Powell’s address at Jackson Hole. It is set to be the key event for markets today, with traders parsing every word for signals on the Fed’s policy path. A September rate cut is still the base case but the odds have slipped from almost certainty earlier this month to around three-quarters. Sticky inflation data have tempered expectations, raising the stakes for Powell to strike the right balance between growth concerns and inflation risks. His tone will shape global risk sentiment into the weekend and will be closely watched for implications on the oil demand outlook.

For now, oil is holding steady with geopolitical frictions lending support and macro uncertainty keeping gains in check.

Oil market is starting to think and worry about next OPEC+ meeting on 7 September. While still a good two weeks to go, the next OPEC+ meeting on 7 September will be crucial for the oil market. After approving hefty production hikes in August and September, the question is now whether the group will also unwind the remaining 1.65 million bpd of voluntary cuts. Thereby completing the full phase-out of voluntary reductions well ahead of schedule. The decision will test OPEC+’s balancing act between volume-driven influence and price stability. The gathering on 7 September may give the clearest signal yet of whether the group will pause, pivot, or press ahead.

Brent crude is currently trading around USD 66.2 per barrel, following a relatively tight session on Monday, where prices ranged between USD 65.3 and USD 66.8. While expectations of higher OPEC+ supply continue to weigh on sentiment, recent headlines have been dominated by geopolitics – particularly developments in Washington.

At the center is the White House meeting between Trump, Zelenskyy, and several key European leaders. During the meeting, Trump reportedly placed a direct call to Putin to discuss a potential bilateral sit-down between Putin and Zelenskyy, which several European officials have said could take place within two weeks.

While the Kremlin’s response remains vague, markets have interpreted this as a modestly positive signal, with both equities and global oil prices holding steady. Brent is marginally lower since yesterday’s close, while U.S. and Asian equity markets remain broadly flat.

Still, the political undertone is shifting, and markets may be underestimating the longer-term implications. According to the NY times, Putin has proposed a peace plan under which Russia would claim full control of the Donbas in exchange for dropping demands over Kherson and Zaporizhzhia – territories it has not yet seized.

Meanwhile, discussions around Ukraine’s long-term security framework are starting to take shape. Zelenskyy appeared encouraged by Trump’s openness to supporting a post-war security guarantee for Ukraine. While the exact terms remain unclear, U.S. special envoy Steve Witkoff stated that Putin had signaled willingness to allow Washington and its allies to offer Kyiv a NATO-style collective defense guarantee – a move that would significantly reshape the regional security landscape.

As diplomatic efforts gain momentum, markets are also beginning to assess the potential consequences of a partial or full rollback of U.S. sanctions on Russian energy. Any unwind would likely be gradual and uneven, especially if European allies resist or delay alignment. The U.S. could act unilaterally by loosening financial restrictions, granting Russian firms greater access to Western capital and services, and effectively neutralizing the price cap mechanism. However, the EU embargo on Russian crude and products remains a more immediate constraint on flows – particularly as it continues to tighten.

Even if the U.S. were to ease restrictions, Moscow would remain heavily reliant on buyers like India and China to absorb the majority of its crude exports, as European countries are unlikely to quickly re-engage in energy trade. That shift is already playing out. As India pulls back amid newly doubled U.S. tariffs – a response to its ongoing Russian oil purchases – Chinese refiners have stepped in.

So far in August, Chinese imports of Russia’s Urals crude – typically shipped from Baltic and Black Sea ports – have nearly doubled from the YTD average, with at least two tankers idling off Zhoushan and more reportedly en route (Kpler data). The uptick is driven by attractive pricing and the absence of direct U.S. trade penalties on China, which remains in a delicate tariff truce with Washington.

Indian refiners, by contrast, are notably more cautious – receiving offers but accepting few. The takeaway is clear: China is acting as the buyer of last resort for surplus Russian barrels, likely directing them into strategic storage. While this may temporarily cushion the effects of sanctions relief, it cannot fully offset the constraints imposed by Europe’s ongoing absence.

As a result, any meaningful boost to global supply from a rollback of U.S. sanctions on Russia may take longer to materialize than headlines suggest.

U.S. commercial crude inventories posted a 3-million-barrel build last week, according to the DOE, bringing total stocks to 426.7 million barrels – now 6% below the five-year seasonal average. The official figure came in above Tuesday’s API estimate of a 1.5-million-barrel increase.

Gasoline inventories fell by 0.8 million barrels, bringing levels roughly in line with the five-year norm. The composition was mixed, with finished gasoline stocks rising, while blending components declined.

Diesel inventories rose by 0.7 million barrels, broadly in line with the API’s earlier reading of a 0.3-million-barrel increase. Despite the weekly build, distillate stocks remain 15% below the five-year average, highlighting continued tightness in diesel supply.

Total commercial petroleum inventories (crude and products combined, excluding SPR) rose by 7.5 million barrels on the week, bringing total stocks to 1,267 million barrels. While inventories are improving, they remain below historical norms – especially in distillates, where the market remains structurally tight.

Brent edges higher as India–Russia oil trade draws U.S. ire and Powell takes the stage at Jackson Hole

Meta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

Aker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

Sommarens torka kan ge högre elpriser i höst

Brent sideways on sanctions and peace talks

Kopparpriset i fritt fall i USA efter att tullregler presenterats

Lundin Gold rapporterar enastående borrresultat vid Fruta del Norte

Stargate Norway, AI-datacenter på upp till 520 MW etableras i Narvik

Mängden M1-pengar ökar kraftigt

Lundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanKopparpriset i fritt fall i USA efter att tullregler presenterats

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanLundin Gold rapporterar enastående borrresultat vid Fruta del Norte

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanStargate Norway, AI-datacenter på upp till 520 MW etableras i Narvik

-

Nyheter4 veckor sedan

Mängden M1-pengar ökar kraftigt

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanLundin Gold hittar ny koppar-guld-fyndighet vid Fruta del Norte-gruvan

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanGuld stiger till över 3500 USD på osäkerhet i världen

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanOmgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAlkane Resources och Mandalay Resources har gått samman, aktör inom guld och antimon