Analys

SEB – Råvarukommentarer, 15 april 2013

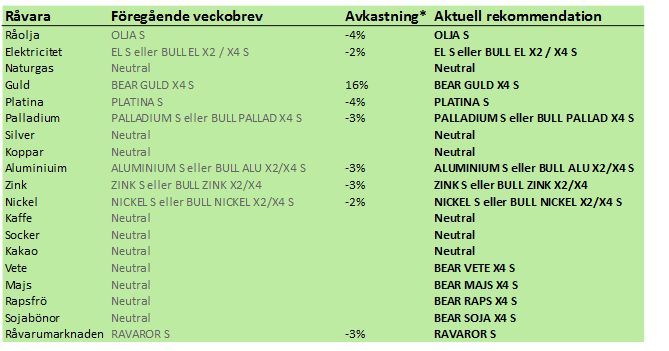

Rekommendationer

*) Avkastningen avser 1:1 råvarucertifikat där de ingår i rekommendationen. I den aktuella tabellen ovan har jag tagit prisförändringen den senaste veckan sedan det förra veckobrevet publicerades.

Inledning

Förra veckan avslutades med stor dramatik då alla råvarusparares “favoritråvara” guld, föll kraftigt. Råoljan noterade också stora prisfall. Många råvaror befinner sig i fallande trender – antingen i början eller (förmodligen) i slutet som kaffe och socker.

Vi ligger huvudsakligen kort råvarumarknaden. Efter de tunga rapporternas från det amerikanska jordbruksdepartemetet ligger vi köpta BEAR på vete, majs och sojabönor. Guldet ligger vi kort och om silver bryter nedåt under 26 dollar ligger vi kort den också.

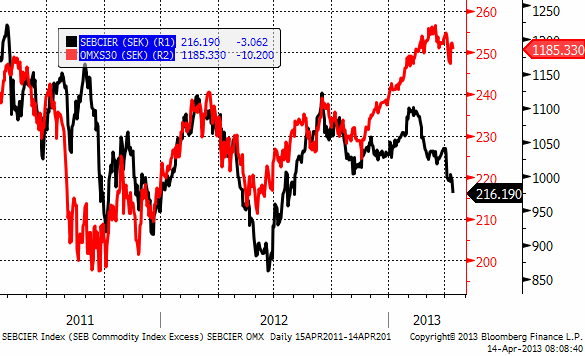

Råvaruindex

I diagrammet nedan ser vi SEB:s råvaruindex i svenska kronor och OMXS30 aktieindex. Vi ser att de gått åt helt olika håll. Man ska naturligtvis inte köpa in i fallande råvarumarknad, men det kan vara en god idé att så småningom vikta upp råvaror (som ju tappar vikt i en portfölj som tidigare investerat i både aktier och råvaror). Yale / NBER –forskarna Gorthon och Rouwenhorst visade ju redan i sin artikel från 2004 att råvarumarknaden tenderar att vara sencyklisk i förhållande till aktier.

Den som vill investera i indexet och den investeringsstrategi som ligger bakom kan läsa mer om certifikatet RAVAROR S.

Råolja – Brent

Oljeprisets nedgång från 120 dollar accellererade och ledde till fritt fall i fredags när priset var nere på strax över 101 dollar per fat. Fram till stängning repade sig dock marknaden och stängde på 103 dollar. Det är inte helt ovanligt i fallande marknader att fyndköpare kommer in på slutet av dagen. Det brukar följas av förnyade nedgångar när börsen öppnar igen nästa handelsdag.

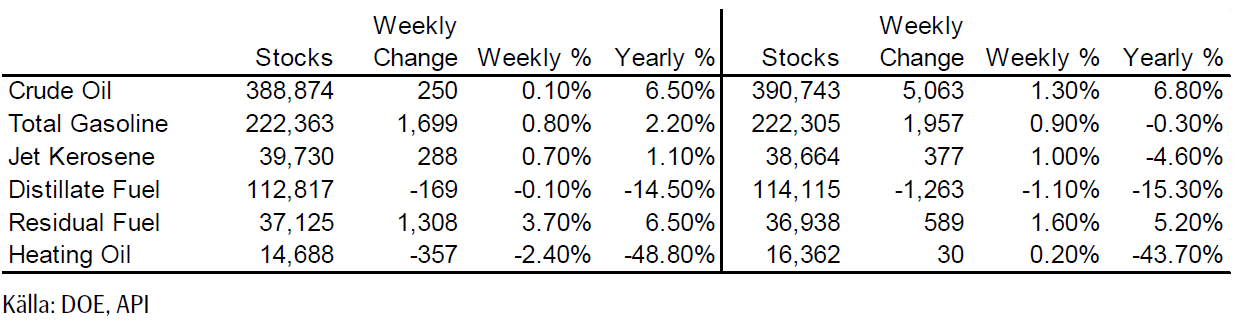

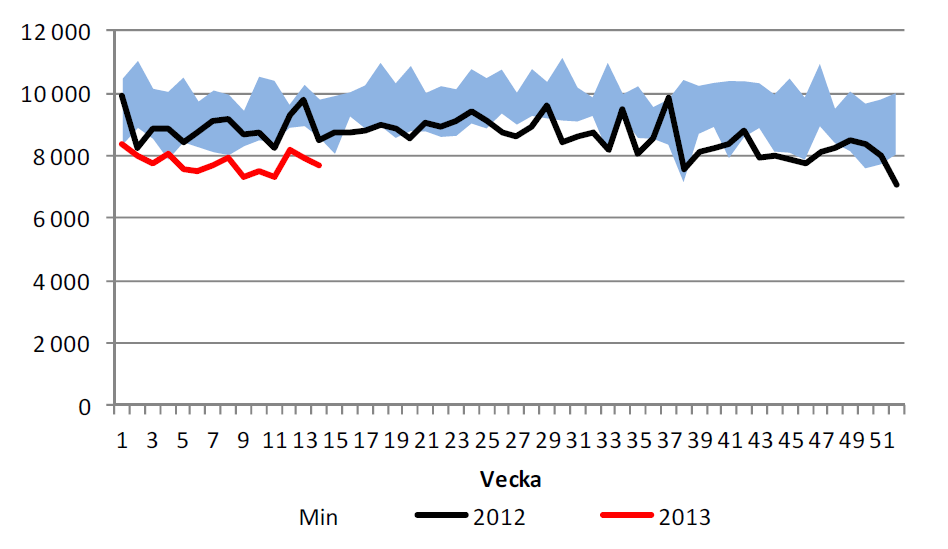

Lagren och lagerförändringarna i USA den senaste rapportveckan ser vi nedan, enligt Department of Energy och American Petroleum Institute.

Nedan ser vi amerikanska råoljelager enligt DOE i tusen fat. Den svarta kurvan är 2012 års lagernivåer vecka för vecka och den lilla röda linjen är 2013 års nivå. Vi ser att lagernivåerna fortsätter att vara högre än de varit sedan 2007 för den här tiden på året. Säsongsmässigt är det tid för lagerökningar och de senaste veckornas lagerökning har varit lite mindre än den årets tidigare trend skulle ha medfört. Detta borde i sig vara ”bullish”.

Importen har minskat och ligger återigen under 8 mbbl/dag.

Vi rekommenderar köp av OLJA S, men inte av BULL OLJA S. Anledningen till denna skillnad och att vi rekommenderar köp av OLJA S är för att rabatten på terminerna innebär en stadig intäkt om ca 6% till 7% per år + ränta på kapitalet. Just nu är marknaden så svag överlag att jag tycker att man ska vänta med nya köp.

Elektricitet

Priset på el som var uppe på över 40 euro per MWh, rekylerade ner till stödet (gamla motståndet) i veckan som gick. Betydligt blötare väder har kommit in i prognoserna.

Den hydrologiska balansen har fortsatt att falla, men detta är inte detsamma som prognosen.

Om priset kommer ner kan det vara läge att gå in och köpa. Tekniskt är den långsiktiga trenden uppåtriktad och nedgångar ska – än så länge – betraktas som rekyler och köptillfällen.

Naturgas

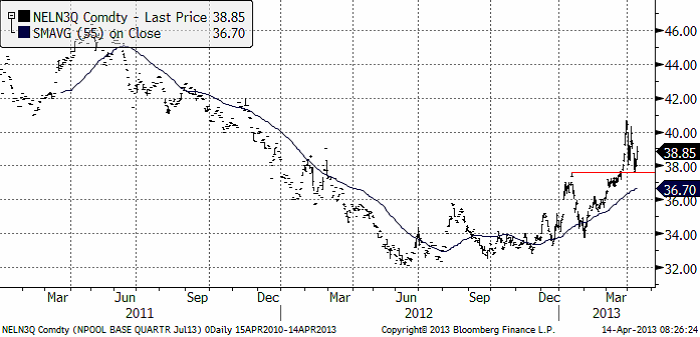

Det är kallt även i USA och naturgaspriset har påverkats av detta även där. Naturgasterminen på NYMEX (maj 2013) har handlats upp ordentligt och testar nu 4 dollar, där priset vänt ner två gånger tidigare. Vi fortsätter att hålla oss neutralt till naturgasen – men skulle ett brott ske av 4 dollar – är det en tydlig köpsignal. Vi ser kursdiagrammet nedan:

Nedan ser vi juli-kontraktet på naturgas i USA. Medan ”mainstream” media börjar uppmärksamma utbudseffekten från den nya tekniken som kallas för hydraulic fracturing eller ”fracking” tillämpad på gasförande skifferlager, har priset börjat bete sig påtagligt ”bullish”. Baserat på tekniska analys och det faktum att uppgången sker när mainstream media skriver om för evigt låga gaspriser, rekommenderar vi köp av BULL NATGAS X4 S.

Guld och Silver

Fredagen slutade i mega-baisse för ädelmetaller. Att fallet blev så kraftigt beror till stor del på att ett avgörande tekniskt stöd bröts. Man kunde nästan se hur säljare tryckte på för att pressa ner priset under stödet och hur fallet för några ögonblick hejdades en bit under när dessa säljare täckte en del av den korta positionen. Skådespelet gick fort och priset tog stora kliv nedåt på minutbasis.

Cypern ska sälja 10 ton guld, värderat till 400 miljoner euro, sade EU Kommissionen den 9 april. Cyperns centralbank svarade att man inte ens diskuterat en försäljning av det mesta av landets 13.9 ton. Nyheten landade inte heller väl i guldmarknaden. ECB.s Mario Draghi sade i fredags att pengarna måste användas för att täcka förlusterna på akuta lån till cypriotiska banker. En försäljning rycker alltså allt närmare. Den här nyheten togs som motiv till att knäcka stödet på guldet. 10 ton hit eller dit är ändå ganska lite i sammanhanget. Förra året köpte centralbanker 534.6 ton guld till sina valutareserver enligt the World Gold Council. Det är den högsta nivån sedan 1964.

Och är det bullish eller bearish att centralbankerna senfärdigt börjat köpa guld? Ser vi den senaste gången de började köpa guld, 1980, signalerade det slutet på 70-talets hausse, när priset på guld (i dollartermer) 20-faldigades. Centralbanker var nettosäljare genom hela uppgången från 1973 till 1980. Man kan därför inte rakt av tolka det som positivt för guldpriset att de mest långsamma aktörerna börjat köpa.

Trots dramatiken finns ändå tekniska stöd precis på den nivå som prisfallet stannade på i fredags, som vi ser i diagrammet. Det finns också stöd precis under fredagens nivå. Det mest sannolika tror jag ändå är att prisfallet stannar upp och vi får se ”sidledes” kursutveckling den närmaste tiden, men kanske med lite större dagsrörelser än vanligt. Naturligtvis ligger vi kvar i BEAR GULD X4 S. Dynamiken är helt klart på nedsidan.

Elektroniskt handlat guld är likvitt, till skillnad från tackor och mynt. Förändringar i sentimentet till det sämre för guld kan idag snabbt leda till stora flöden. Nedan ser vi antalet utestående fondandelar till det börshandlade och fysiskt backade depåbeviset GLD – och guldpriset.

Minskningen av antalet utestående depåbevis av GLD är den starkaste de senaste fem åren. Till viss del beror detta på att placerare konverterat sina depåbevis till tackor, en säkrare form om man liksom italienare är orolig för en skatt på finansiellt sparande som hände på 90-talet i Italien och nu sker på Cypern. Det hände även i Sverige, när staten tog ut ”överskottsmedel” (samma ord som EU Kommissionen använder för Cyperns guldreserv) från AP-fonderna för några år sedan. En stor del av minskningen av GLD-depåbevis är sannolikt också rena försäljningar, som alltså lett till försäljning av guld på London Bullion Market.

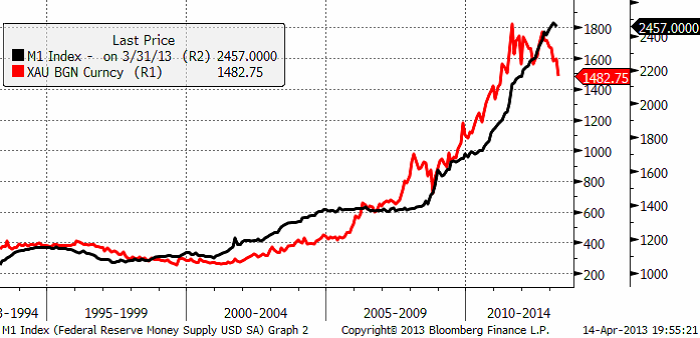

Guld är trots allt en värdebevarare i inflationsskyddad mening och eftersom penningmängden ökar så kraftigt i alla stora och sparkapitalsfulla ekonomier, borde guld vara en attraktiv tillgång. Traditionell monetarism säger att om man inte förändrar antalet varor, men ökar mängden pengar, måste priset i dessa pengar stiga på varorna. Nedan ser vi M1 i USA. M1 är den smalaste måttet på penningmängd och mäter bara mynt, sedlar och bankinlåning som har betalningsmöjligheter kopplade till sig (checkar eller kort).

Vi ser att det tycks finnas ett bra samband mellan M1 och guldpriset, trots att vi bara ser till M1 i USA.

Nedan ser vi kursdiagrammet för silver i dollar per troy ounce. Silverpriset föll till 26 dollar, precis på det tekniska stödet från 2011. Ett brott av det stödet skulle ge en möjlighet, enligt den tekniska analysen, för en nedgång till 20 dollar.

I den här typen av lägen är det svårt att lämna en rekommendation nu, utan den måste bli beroende på om 26 dollar bryts eller håller. Vi har haft en neutral rekommendation, men om stödet bryts köper vi BEAR SILVER X4 S.

Platina & Palladium

Platinapriset ligger strax över stödet på 1550 dollar, som testades – och höll – i veckan som gick. Om 1525 – 1550 byts på nedsidan är nästa stöd 1400.

Palladium föll ner till 709 dollar per ozt. Vi ser att 700 dollar. Så länge den nivån håller fortsätter vi vara köpta PALLADIUM S.

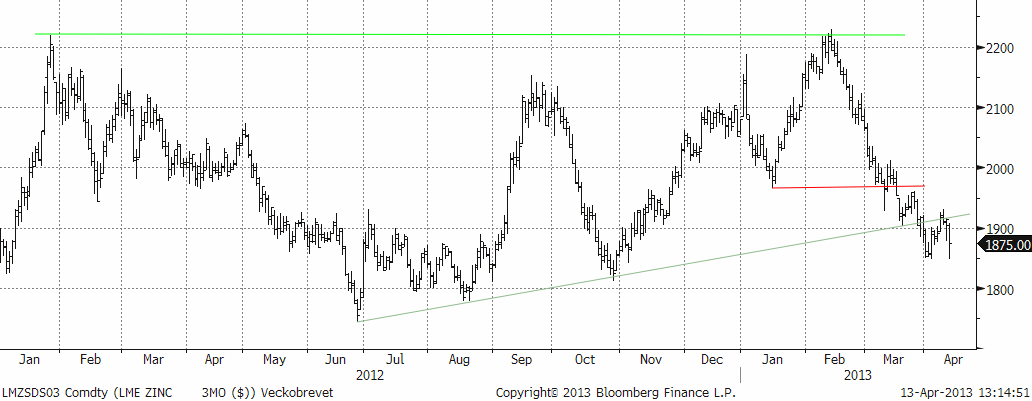

Basmetaller

Veckan avslutades med ett relativt kraftigt prisfall för industriella råvaror. Energi och basmetaller föll på bred front. Utlösande faktor var ädelmetallernas plötsliga kollaps (guldet föll med 5 % bara under fredagshandeln). Den Cypriotiska centralbankens förväntade utförsäljning oroar marknaden. Inte så mycket för volymen, utan mer om det kan vara en omsvängning av trenden av nettoköpande centralbanker. Veckan inleddes annars med en rekyl uppåt (för basmetallerna) på ett par procent, vilken således raderades ut under fredagen. Netto på veckan är priserna ner 0,5-1 %.

Koppar

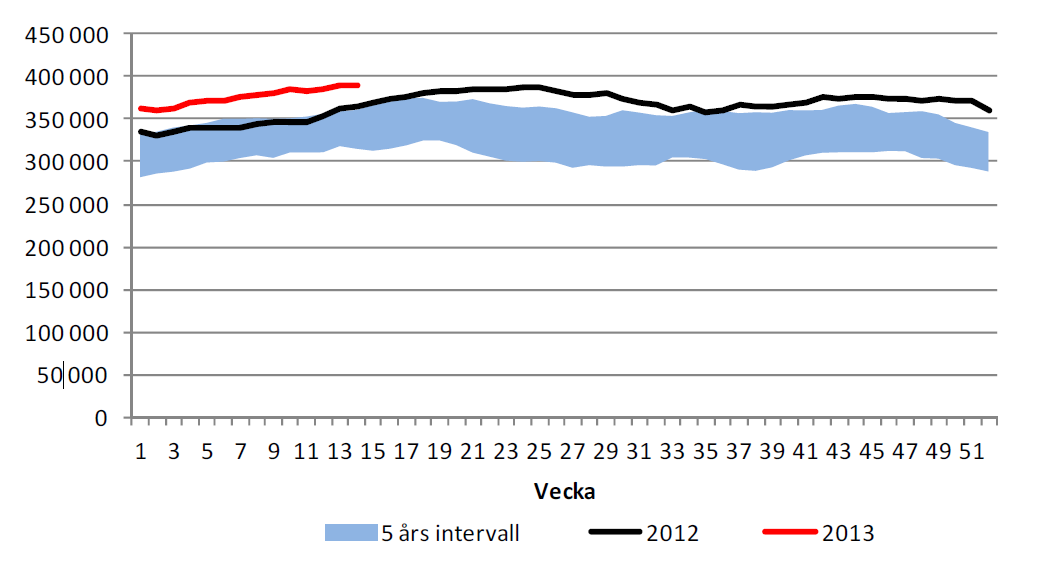

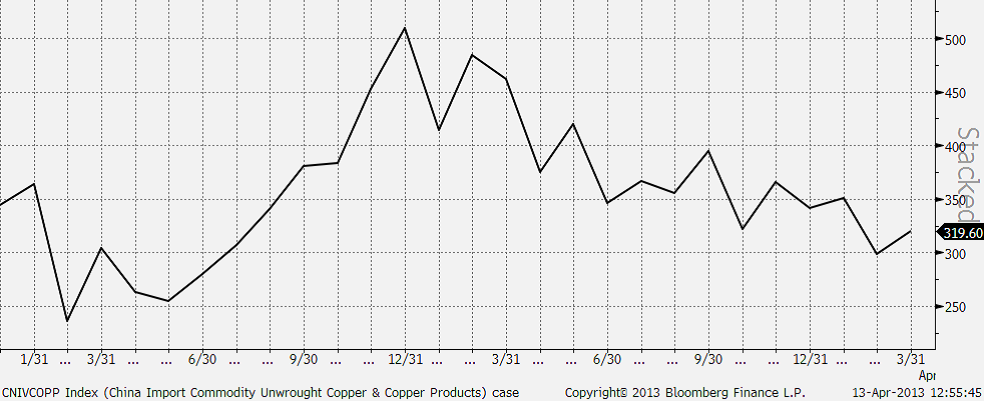

”Upp som en sol, ner som en pannkaka” skulle man kunna beskriva veckan. 3-månaderspriset på LME steg från $7400-nivån upp 7650, med stöd av ökad riskaptit på Kinas positiva handelsstatistik i mitten av veckan. Inflationen kom också in lägre än väntat. Kopparimporten steg men har fortfarande en bit kvar till vad som kan betraktas som stark (se diagramet nedan).

Den stora årliga CESCO-konferensen i Chile har gått av stapeln i veckan. Diskussionerna har handlat mer om premienivåer än faktiskt prisnivåer. Marknaden bedöms vara relativt balanserad, till ett mindre överskott, efter flera år av ”kroniska” underskott. Premiediskussionen kretsar kring farhågorna att kopparn skall erfara samma sak som aluminium och zink, d.v.s. att överskottsmaterial placeras i LME-lager uppknutet i finansierings affärer (där man köper spot och säljer på termin för att utnyttja terminspåslaget). De långa utlastningstiderna i LME-lager gör att material blir otillgängligt för konsumenter och därmed stiger premierna. LME diskuterar olika påtryckningsmedel för att förmå lagerhusen att öka utlastningskapaciteten.

Den tekniska bilden ger stöd till vår neutrala position. Vi är positiva till basmetaller på sikt men avvaktar bättre köptillfällen alternativt väljer någon annan basmetall. Priset kommer nu ner i ett intressant stödområde mellan $7200 och $7300.

Som vi skrivit tidigare tyder mycket på ökat utbud för koppar, vilket riskerar att begränsa uppgångspotentialen. Vi rekommenderar fortsatt en neutral position. För den som vill satsa på ett starkare tillväxtscenario (än konsensus) i Kina är koppar däremot alltid ett intressant alternativ.

Aluminium

Som vi skrivit tidigare ligger aluminium väldigt ”fast” i ett relativt stort handelsintervall. Nivåer kring $1800-1900 utgör ur ett kostnadsperspektiv starkt stöd. Samtidigt lägger det stora utbudet ett ”tak” på nivåer kring $2300. Den senaste uppgången i februari mötte stora säljordrar från producenter som passade på att ”låsa” framtida priser, vilket satte press på marknaden. Nu när priserna fallit tillbaka ser vi stora intressen från köpsidan (fysiska förbrukare). För den ”trading-benägne” utgör det stora spannet goda vinstmöjligheter. Vi närmar oss nu ”den sista utposten”, kring $1830. Det allmänt negativa stämningsläget för de industriella råvarorna under fredagen kan ge en tillfällig press under nivån. På lite sikt (6-12 mån) är dock detta en mycket intressant nivå för öka exponeringen mot basmetaller.

Zink

Priset följde kopparn under veckan, och den inledande rekylen upp till $1930 kom av sig rejält. Scenariot påminner om det för aluminium, där vi nu kommer ned till väldigt attraktiva nivåer. Den negativa tendensen från i fredags kan mycket väl fortsätta under veckans inledning. Fundamentalt är zinken ”billig” ur ett kostnadsperspektiv och nuvarande nivåer är mycket intressanta på lite längre sikt (6-12 månader).

Nickel

Marknaden är fortsatt tveksam till den fundamentala situationen. Vi har tidigare bl.a. hänvisat till kommentarer från fysiska aktörer som indikerar att ”det finns gott om nickel”, samtidigt som rapporter gör gällande att exporten av nickelmalm från Indonesien till Kina ökar igen, vilket riskerar att öka utbudet av s.k. Nickel Pig Iron i Kina (vilket i sin tur minskar efterfrågan på nickelbärande skrot och primärnickel). För några veckor sedan ryktades det om en omsvängning, då kinesiska producenter är snabba att ställa om produktionen, vilket ger ett naturligt stöd till nickelmarknaden. Nya rykten gör dock gällande att Kina börjat exportera Nickel Pig Iron. LME-lagret är på all time high. Så det är svårt att bli vara väldigt ”bullish” på nickel just nu. Nivån är attraktiv ur ett kostnadsperspektiv, men det allmänna stämningsläget just nu riskerar att sätta ytterligare press. Det stora stödet ligger kring $15 000. Precis som för aluminium och zink bedömer vi dock nickel som mycket köpvärd på 6-12 månaders sikt.

Vi rekommenderar köp av NICKEL S eller BULL NICKEL X2 / X4 S för den som vill ta mer risk. Vi varnade för en rekyl, och den kom. Priset har fallit mer än ”befarat”, men är nu på väldigt attraktiva nivåer.

Kaffe

Kaffepriset (maj 2013) fortsatte ner i veckan som gick och fortsatte därmed den fallande trenden. Vi tror att en trendvändning är nära förestående, men det är ingen idé att köpa KAFFE S innan trenden har vänt.

Marknaden diskonterar högre priser i framtiden, som vi ser av terminskurvan nedan. För att man ska tjäna pengar genom att köpa terminer måste uppgången vara större än vad marknaden redan har diskonterat.

Socker

Sockerpriset (september 2013) föll i slutet av mars under 18 cent per pund. De senaste dagarna har priset rekylerat upp mot det motståndet, men inte orkat igenom. Trenden är alltjämt nedåtriktad. Vi fortsätter med neutral rekommendation.

Guld är trots allt en värdebevarare i inflationsskyddad mening och eftersom penningmängden ökar så kraftigt i alla stora och sparkapitalsfulla ekonomier

Brent M1 moving below the 200 dma of $78.7/b. Brent crude continued its move lower yesterday with a decline of 3.3% to $77.9/b. This morning it is adding another drop of 1.4% to $76.8/b. Israel bombing Lebanon during the weekend was a violence of the MoU and Iran was quick to declare the SoH closed again. But the willingness to move forward by both the US and Iran obviously trumped the bombing in Lebanon making the event more of a hiccup on the road of further negotiations.

The US has now waived sanctions against Iranian oil exports for two months allowing Iran to sell its oil all over the world, though sanctions instated in Europe will take more time to unwind. Oil from Iran, Russia as well as Venezuela can for the time being be sold across the world without any sharp discount due to sanctions. Chinese Tea-pot refineries will suffer as they previously could buy rebated crude while selling products at market prices.

Crude oil is no flowing out of the SoH with latest number close to 7 mb/d on a three day moving average. That is still well below the 14 mb/d of crude and 6 mb/d of products normally flowing out of the SoH. Latest estimate is that there is around 80 mb of crude on water inside the Persian Gulf and maybe another 80 mb of oil products on water as well. If crude is exiting the SoH at a rate of around 7 mb/d, then the 80 mb of crude would be depleted within 10-15 days and there after the flow would rely on new crude tankers entering, loading and then exiting the SoH to continue further flows. Given the uncertainties surrounding the status of the SoH with Iran stating that it was closed again as recent as this weekend, there is likely an asymmetry here where ships and oil stranded in the SoH for months are much more eager to exit than new ships are eager to enter.

For now Brent crude keeps falling like a rock with the front-end Brent contract now only trading at a premium of $7.6/b above the five year contract. Quickly heading towards parity. The Brent M1 contract has now broken below its 200 dma of $78.7/b and is closing in on the Fibo-level at $74.7/b. Below that there is not much more supporting levels to be found before $73/b which would close the gap from February 3.

Brent crude M1 technical levels

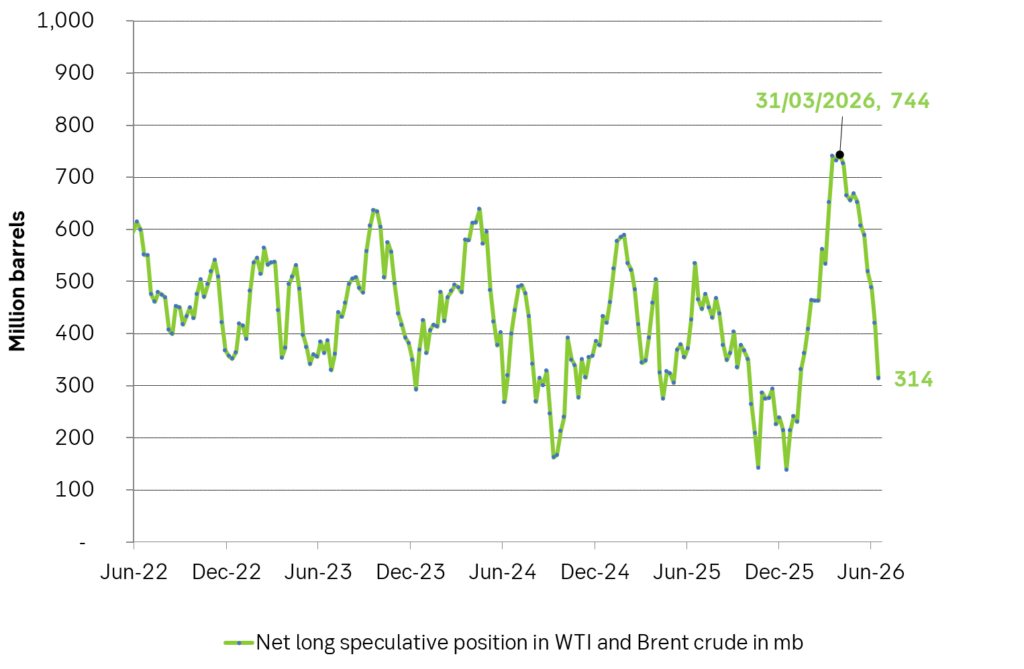

Net long speculative positions are also falling like a rock and as of Tuesday last week the net long positioning in Brent and WTI together summed to 314 million barrels and falling fast.

Will there be a rebound? A possible combination could be an exhaustion of the oil blob caught within the SoH within 1-2 weeks if exits continue at current rate while new ships entering are much more cautious, more Israeli bombardments in Lebanon as Netanyahu fights for re-election, a temporary closure of the SoH again while speculative short positions take cover buying back and covering their positions.

US and Israeli stands versus Iran could harden beyond elections so 2027 surplus is far from given. But Iran and the US are all in all moving towards a set of solutions with both clearly eager to reopen the SoH and keep it open. And that is what the market is pricing along with sharply falling prices. The ongoing discussions will likely take months and last beyond both the upcoming Israeli election (before 27 oct) and the US midterm elections on 3 Nov. Beyond those dates the stance by both Israel and the US may harden again versus Iran. But Iran knows that and is most likely preparing for such a hardening turn. Thus a surplus of oil and global oil stock rebuilding in 2027 (as now is mostly projected) is far from given.

Selling down on a ”deal”. Brent crude fell 6.2% last week with accelerated weakness towards the end of the week. Close of the week at $87.33/b and low of the week (and on Friday) of $85.8/b. Brent is falling another 4% this morning to $83.7/b on confirmation by Iran that a MoU text has been reached and that it will be signed on Friday this week.

So what is this ”deal” worth? Talk on the desk here this morning is that it is much like ”putting lipstick on a pig” where Trump has to sell this at home as a victory where ”the SoH has reopened”, the nuclear issue will be ironed out over the coming 60 days (or maybe 600 days?) and US consumers are getting a lower gasoline price and maybe US republicans survives the midterm elections.

The importance for Iran is that it emerges as the defacto winner of this war in the eyes of the non-US public world. That Iran now onwards is the ”ruler of the SoH” (combo of geography and new weapons systems like drones) or more softer: ”the guarantor of safe passage through the SoH”.

Iran doesn’t need nuclear weapons any more. Nuclear deterrence doesn’t work any more. Ukraine has made many attacks deep into Russia without being nuked in return. Plenty of Iranian ballistic rockets blasts over Israel but Iran wasn’t nuked in return.

There is no trust between the US and Iran. We don’t know all the details yet of the MoU. But what we do know is that there is no trust between the US and Iran what so ever. This is probably more like a descriptive text on how they can cooperate in a way where both sides keeps tactical leverage. Neither side makes irreversible concessions. Violations can be punished quickly. Cooperation produces immediate benefits.

This is a fragile structure. It can easily break down. There may be details which cannot be overcome. To be seen on Friday. The US has to show that it is willing put enough force behind managing and restraining Israel versus Hezbollah in Lebanon. We have seen that Netanyahu hasn’t listened all that much to Trump’s directives and wishes. This could be a major obstacle.

A gradual reopening is tactically preferable for Iran. A tactical leverage for Iran right now is that global oil stocks have been drawn down towards painful and increasingly dangerous levels with increasing risks for oil price spikes in mid-July to August. This together with US midterm elections on 3 November gives tactical leverage to Iran. Iran probably doesn’t want to fully give up on that leverage. A rapid, full reopening where global stocks are able to refill over the coming 60 days will significantly erode that leverage. If Iran reinstates a closure of the SoH after 60 days (if talks break down again), then the effect won’t be that impactful in terms of prices and the US midterm elections.

So a gradual and partial reopening where global markets gets the oil they need while they are unable to rebuild stocks could be a practical middle way for both parties. Trump can sell it as ”the SoH has reopened” and get affordable gasoline for US consumers. Iran can sell it as ”the SoH has fully reopened, but there is some friction” so flow is only 60-80% of normal.

Not much real demand destruction below $100/b. What we do know is that there is not much real price pain demand destruction for oil globally at an oil price below $100/b. A lot of demand-shock destruction. Fear. But demand should now come roaring back towards normal with fear for exceptionally high prices now is rapidly receding.

Sudden China demand destruction due to EVs? Bullocks. EV share of total Chinese carpool now around 13%. Share of new sales of EVs has reached 50%. This is a very gradual process. It doesn’t make oil demand fall like a rock over night. When EV new sales share reaches 100%, then the gasoline car pool will contract by some 5-10% per year. But that is only gasoline. Sudden reduction in Chinese oil demand is more about shock and risk.

Chinese crude oil imports will come roaring back. At what price? Today’s ”neutral” oil price is $70/b. That is the five year price which has steadily traded around the $70/b mark over the past 3-4 years. With still a risky picture one would think that China and the rest of the world will be big buyers of oil in the range of $70-85/b.

Global demand will likely snap back towards normal, forecasted demand and growth at such prices.

Physical reopening is a gradual process. The physical and practical reopening of the SoH will likely be gradual rather than sudden. And that probably suites Iran tactically as well.

Brent M1 price versus the Brent 5-yr (today’s ”normal” price)

Market is starting to take US/Iran headlines with a pinch of salt. Brent crude rose $2.8/b yesterday to an official close of $112.1/b. But after that it traded as low as $108.05/b before ending late night at around $109.7/b. Through the day it traded in a range of $106.87 – 112.72/b amid a flurry of news or rumors from Iran and the US. ”US temporary sanctions during negotiations” (falls alarm). ”We will bomb Iran” (not anyhow),… etc. While the market is still fluctuating to this kind of news flow, it is starting to take such headlines with a pinch of salt.

We’ll see. Maybe, maybe not. The Brent M1 contract is trading at $110.2/b this morning which very close to the average ticks through yesterday of $110.4/b.

Trump with bearish, verbal intervention whenever Brent trades above $110/b it seems. What seems to be a pattern is that Trump states something like ”very good negotiations going on with Iran”, ”New leaders in Iran are great,..”, ”Great progress in negotiations,…”, ”Deal in sight,..” etc whenever the Brent M1 contract trades above $110/b. An effort to cool the market. These hot air verbal interventions from Trump used to have a heavy bearish impact on prices, but they now seems to have less and less effect unless they are backed by reality.

As far as we can see there has been no real progress in the negotiations between the US and Iran with both sides still standing by their previous demands.

Iran is getting stronger while the cease fire lasts making a return to war for Trump yet harder. Iran is naturally in constant preparation for a return to war given Trump’s steady threats of bombing Iran again. Iran is naturally doing what ever is possible to prepare for a return to war. And every day the cease fire lasts it is better prepared. This naturally makes it more and more difficult and dangerous for the US to return to warring activity versus Iran as the consequences for energy infrastructure in the Persian Gulf will be more and more severe the longer the cease fire lasts. Israel seems to see it this way as well. That the war is not won and that current frozen state of a cease fire gives Iran opportunity to rebuild military and politically.

Global inventories are drawing down day by day. How much? In the meantime the Strait of Hormuz stays closed. There is varying measures and estimates of how much global inventories are drawing down. Our rough estimate, back of the envelope, is that global inventories are drawing down by at least some 10 mb/d or about 300 mb/d in a balance between loss of supply versus demand destruction. Other estimates we see are a monthly draw of 250-270 mb/d. The IEA only ’measured’ a draw in global observable stocks of 117 mb in April with oil on water rising 53 mb while on shore stocks fell 170 mb. But global stocks are hard to measure with large invisible, unmeasured stocks. As such a back of the envelope approach may be better.

Oil products is what the world is consuming. Oil product prices likely to rise while product stocks fall. Strategic Petroleum Reserves (SPR) are predominantly crude oil. Discharging oil from OECD SPR stocks, a sharp reduction in Chinese crude imports and a reduction in global refinery throughput of 6-7 mb/d has helped to keep crude oil markets satisfactorily supplied. But global inventories are drawing down none the less. And oil products is really what the world is consuming. So if global refinery throughput stays subdued, then demand will eventually have to match the supply of oil products. The likely path forward this summer is a steady draw down in jet fuel, diesel and gasoline. Higher prices for these. Then, if possible, higher refinery throughput and higher usage of crude in response to very profitable refinery margins. And lastly sharper draw in crude stocks and higher prices for these. But some 6 mb/d of oil products used to be exported through the Strait of Hormuz. And it may not be so easy to ramp up refinery activity across the world to compensate. Especially as Ukraine continues to damage Russian refineries as well as Russian crude production and export facilities.

Watch oil product stocks and prices as well as Brent calendar 2027. What to watch for this summer is thus oil product inventories falling and oil product premiums to crude rising. Another measure to watch is the Brent crude 2027 contract as it rises steadily day by day as the Strait of Hormuz stays closed and global oil inventories decline. The latter is close to the highest level since the start of the war and keeps rising.

The Brent M1 contract and the Brent 2027 prices and current price of jet fuel in Europe (ARA). All in USD/b

Our back of the envelope calculation of the global shortage created by the closure of the Strait of Hormuz. Note that 3.5 mb/d of discharge from SPR is also a draw. Note also that ’Forced demand loss’ of 2.5 mb/d is probably temporary and will fall back towards zero as logistics are sorted out leaving ’Price demand loss’ to do the job of balancing the market. Thus a shortfall of at least 9 mb/d created by the closure. More if SPR discharge is included and more if Forced demand loss recedes.

Brent falling like a rock with oil likely to flow from SoH until at least 3 November

Vattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

Selling down on a ”deal”

Sommarväder skapar prisrally på elbörsen

Oil product price pain is set to rise as the Strait of Hormuz stays closed into summer

Sommarväder skapar prisrally på elbörsen

Vattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

Selling down on a ”deal”

Brent falling like a rock with oil likely to flow from SoH until at least 3 November

-

Nyheter3 veckor sedan

Sommarväder skapar prisrally på elbörsen

-

Nyheter1 vecka sedan

Nyheter1 vecka sedanVattenfalls och Industrikrafts kärnkraftsbolag Videberg Kraft har valt Rolls-Royce SMR

-

Analys1 vecka sedan

Selling down on a ”deal”

-

Analys14 timmar sedan

Brent falling like a rock with oil likely to flow from SoH until at least 3 November