Analys

Crude oil comment: It takes guts to hold short positions

The oil market has experienced a retreat in bullish sentiment over the last few weeks, as shifts in geopolitical tensions have influenced the market. Notably, the anticipation of Israeli military actions, which are now expected to avoid critical Iranian oil infrastructure (though not with 100% certainty), has led to a recalibration of risk assessments.

Despite these geopolitical developments, underlying market fundamentals, including inventory levels and production rates, continue to influence price movements. There appears to be a balancing act between the continuously uncertain geopolitical landscape and concerns over an oil surplus in 2025.

Recent IEA reports suggest that OPEC must cut an additional 0.9 million barrels per day next year to balance the market. This is in contrast to the cartel’s strategy of gradually regaining market share and increasing production by 180,000 barrels per month starting December 2024, culminating in an increase of 2.2 million barrels per day by December 2025.

OPEC will continue to closely monitor market conditions and perform monthly evaluations of their planned production increase, adjusting the production scale as needed to stabilize prices within the mid-70-to-80-dollar range.

We anticipate the planned OPEC December 2024 production increase of 180,000 barrels will occur, which is likely looming in the consciousness of market participants trying to balance the bulls and bears.

However, even though Brent prices have retreated from their largest peaks during the height of the Middle East unrest in early to mid-October, we now see Brent crude prices trading in positive territory since opening on Monday this week, climbing by USD 3 per barrel over the last four days and currently trading at a strong USD 76.2. This returns to the September peaks before the worst escalation in the Middle East.

As zero Israeli retaliation has materialized and with less focus on vital Iranian oil infrastructure, investor sentiment has been impacted, with hedge funds and money managers reducing their long positions in major petroleum contracts. Specifically, there was a notable decrease in positions across Brent (down 28 million barrels) and WTI (down 12 million barrels), reflecting a, so far, relaxed approach to potential supply disruptions.

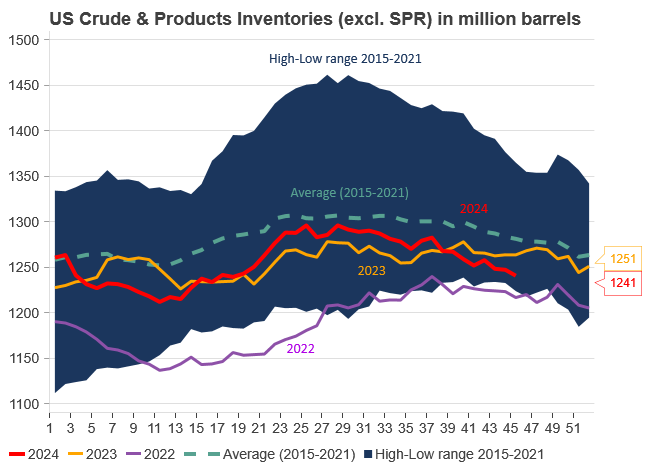

Yesterday evening, we also received a slightly bearish US inventory report from last week’s data. There was a sizeable increase in US commercial crude oil inventories, which rose by 5.47 million barrels. However, keep in mind that total inventories remain about 4% below the five-year average for this time of year, totaling 426.0 million barrels.

Notably, gasoline inventories also experienced a rise, increasing by 0.88 million barrels, yet still tracking approximately 3% below the five-year average. In contrast, distillate (diesel) inventories saw a decrease of 1.14 million barrels yet remain a very bullish 9% below the five-year average. Overall, total commercial petroleum inventories experienced an upward movement, adding 5.9 million barrels over the week. This is slightly bearish indeed, but likely not enough to counter the geopolitical uncertainties ahead.

As market participants monitor the fundamentals, the potential for a hard Israeli retaliation remains an important risk, with possible impacts on Iranian oil facilities still on the table. Such geopolitical risks are juxtaposed with fundamental calculations, such as the enforcement of sanctions and adjustments in OPEC+ production strategies.

In summary, while current market conditions suggest a greater stabilization of prices and concerns for a surplus in 2025 are holding back Brent prices from spiraling, the underlying risks related to geopolitical actions should weigh heavier. The more time that passes without any Israeli retaliation, the more likely the risk premium will fade. Yet, more time also means more Israeli preparation, and the retaliation will likely be well-planned with significant consequences for Iran. In essence, it takes courage to maintain a short position in the current market. Again, the continuous potential for upside risks outweighs the downside risks.

Since market opening yesterday, Brent crude prices have returned close to the same level as 24 hours ago. However, before the release of the weekly U.S. petroleum status report at 17:00 CEST yesterday, we observed a brief spike, with prices reaching USD 73.2 per barrel. This morning, Brent is trading at USD 71.4 per barrel as the market searches for any bullish fundamentals amid ongoing concerns about demand growth and the potential for increased OPEC+ production in 2025, for which there currently appears to be limited capacity – a fact that OPEC+ is fully aware of, raising doubts about any such action.

It is also notable that the USD strengthened yesterday but retreated slightly this morning.

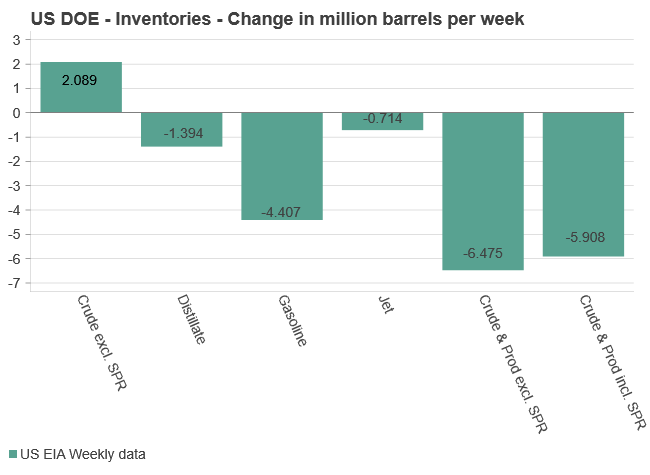

U.S. commercial crude oil inventories increased by 2.1 million barrels to 429.7 million barrels. Although this build brings inventories to about 4% below the five-year seasonal average, it contrasts with the earlier U.S. API data, which had indicated a decline of 0.8 million barrels. This discrepancy has added some downward pressure on prices.

On the other hand, gasoline inventories fell sharply by 4.4 million barrels, and distillate (diesel) inventories dropped by 1.4 million barrels, both now sitting around 4-5% below the five-year average. Total commercial petroleum inventories also saw a significant decline of 6.5 million barrels, helping to maintain some balance in the market.

Refinery inputs averaged 16.5 million barrels per day, an increase of 175,000 barrels per day from the previous week, with refineries operating at 91.4% capacity. Crude imports rose to 6.5 million barrels per day, an increase of 269,000 barrels per day.

Over the past four weeks, total products supplied averaged 20.8 million barrels per day, up 1.8% from the same period last year. Gasoline demand increased by 0.6%, while distillate (diesel) and jet fuel demand declined significantly by 4.0% and 4.6%, respectively, compared to the same period a year ago.

Overall, the report presents mixed signals but leans slightly bearish due to the increase in crude inventories and notably weaker demand for diesel and jet fuel. These factors somewhat overshadow the bullish aspects, such as the decline in gasoline inventories and higher refinery utilization.

Analys

Crude oil comment: Fundamentals back in focus, with OPEC+ strategy crucial for price direction

Since the market close on Monday, November 11, Brent crude prices have stabilized around USD 72 per barrel, after briefly dipping to a monthly low of USD 70.7 per barrel yesterday afternoon. The momentum has been mixed, oscillating between bearish and cautious optimism. This morning, Brent is trading at USD 71.9 per barrel as the market adopts a “wait and see” stance. The continued strength of the US dollar is exerting downward pressure on commodities overall, while ongoing concerns about demand growth are weighing on the outlook for crude.

As we noted in Tuesday’s crude oil comment, there has been an unusual silence from Iran, leading to a significant reduction in the geopolitical risk premium. According to the Washington Post, Israel has initiated cease-fire negotiations with Lebanon, influenced by the shifting political landscape following Trump’s potential return to the White House. As a result, the market is currently pricing in a reduced risk of further major escalations in the Middle East. However, while the geopolitical risk premium of around USD 4-5 per barrel remains in the background, it has been temporarily sidelined but could quickly resurface if tensions escalate.

The EIA reports that India has now become the primary source of oil demand growth in Asia, as China’s consumption weakens due to its economic slowdown and rising electric vehicle sales. This highlights growing concerns over China’s diminishing role in the global oil market.

From a fundamental perspective, we expect Brent crude to remain well above USD 70 per barrel in the near term, but the outlook hinges largely on the upcoming OPEC+ meeting in early December. So far, the cartel, led by Saudi Arabia and Russia, has twice postponed its plans to increase production this year. This decision was made in response to weakening demand from China and increasing US oil supplies, which have dampened market sentiment. The cartel now plans to implement the first in a series of monthly hikes starting in January 2025, after originally planning them for October. Given the current supply dynamics, there appears to be limited room for additional OPEC volumes at this time, and the situation will likely be reassessed at their December 1st meeting.

The latest report from the US API showed a decline in US crude inventories of 0.8 million barrels last week, with stockpiles at the Cushing, Oklahoma hub falling by a substantial 1.9 million barrels. The “official” figures from the US DOE are expected to be released today at 16:30 CEST.

In conclusion, over the past month, global crude oil prices have fluctuated between gains and losses as market participants weigh US monetary policy (particularly in light of the election), concerns over Chinese demand, and the evolving supply strategy of OPEC+. The coming weeks will be critical in shaping the near-term outlook for the oil market.

Since the market opened on Monday, November 11, Brent crude prices have declined sharply, dropping nearly USD 2.2 per barrel in just over a day. The positive momentum seen in late October and early November has largely dissipated, with Brent now trading at USD 71.9 per barrel.

Several factors have contributed to the recent price decline. Most notably, the continued strengthening of the U.S. dollar remains a key driver, as it gained further overnight. Meanwhile, U.S. government bond yields showed mixed movements: the 2-year yield rose, while the 10-year yield edged slightly lower, indicating larger uncertainty.

Adding to the downward pressure is ongoing concern over weak Chinese crude demand. The market reacted negatively to the absence of a consumer-focused stimulus package, which has led to persistent pricing in of subdued demand from China – the world’s largest crude importer and second-largest crude consumer. However, we anticipate that China recognizes the significance of the situation, and a substantial stimulus package is imminent once the country emerges from its current balance sheet recession: where businesses and households are currently prioritizing debt reduction over spending and investment, limiting immediate economic recovery.

Lastly, the geopolitical risk premium appears to be fading due to the current silence from Iran. As we have highlighted previously, when a “scheduled” retaliatory strike does not materialize quickly, it reduces any built-in price premium. With no visible retaliation from Iran yesterday, and likely none today or tomorrow, the market is pricing in diminished geopolitical risk. Furthermore, the outcome of the U.S. with a Trump victory may have altered the dynamics of the conflict entirely. It is plausible that Iran will proceed cautiously, anticipating a harsh response (read sanctions) from the U.S. should tensions escalate further.

Looking ahead, the market will be closely monitoring key reports this week: the EIA’s Weekly Petroleum Status Report on Wednesday and the IEA’s Oil Market Report on Thursday.

In summary, we believe that while the demand outlook will eventually stabilize, the strong oil supply continues to act as a suppressing force on prices. Given the current supply environment, there appears to be little room for additional OPEC volumes at this time, a situation the cartel will likely assess continuously on a monthly basis going forward.

With this context, we maintain moderately bullish for next year and continue to see an average Brent price of USD 75 per barrel.

Crude oil comment: Mixed U.S. data skews bearish – prices respond accordingly

Kommande 25 år behöver vi lika mycket koppar som vi producerat sedan stenåldern

Crude oil comment: Fundamentals back in focus, with OPEC+ strategy crucial for price direction

Silverpriset kan bara gå upp

Michel Rufli förklarar vad som händer på guldmarknaden

Crude oil comment: Market battling between spike-risk versus 2025 surplus

Uniper har säkrat 175 MW elektricitet i Östersund för e-metanol

Guldpriset passerar 2700 USD till sin högsta nivå någonsin

District Metals prospekterar uran i Sverige, nu noteras även aktierna här

Crude oil comment: It takes guts to hold short positions

-

Analys4 veckor sedan

Crude oil comment: Market battling between spike-risk versus 2025 surplus

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanUniper har säkrat 175 MW elektricitet i Östersund för e-metanol

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuldpriset passerar 2700 USD till sin högsta nivå någonsin

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDistrict Metals prospekterar uran i Sverige, nu noteras även aktierna här

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanGuldpriset stiger hela tiden till nya rekord

-

Analys1 vecka sedan

Crude oil comment: A price rise driven by fundamentals

-

Analys2 veckor sedan

Crude oil comment: Recent ’geopolitical relief’ seems premature

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFå råvarupriser påverkar världsekonomin mer än oljans