Analys

Crude oil comment: Iran’s silence hints at a new geopolitical reality

Since the market opened on Monday, November 11, Brent crude prices have declined sharply, dropping nearly USD 2.2 per barrel in just over a day. The positive momentum seen in late October and early November has largely dissipated, with Brent now trading at USD 71.9 per barrel.

Several factors have contributed to the recent price decline. Most notably, the continued strengthening of the U.S. dollar remains a key driver, as it gained further overnight. Meanwhile, U.S. government bond yields showed mixed movements: the 2-year yield rose, while the 10-year yield edged slightly lower, indicating larger uncertainty.

Adding to the downward pressure is ongoing concern over weak Chinese crude demand. The market reacted negatively to the absence of a consumer-focused stimulus package, which has led to persistent pricing in of subdued demand from China – the world’s largest crude importer and second-largest crude consumer. However, we anticipate that China recognizes the significance of the situation, and a substantial stimulus package is imminent once the country emerges from its current balance sheet recession: where businesses and households are currently prioritizing debt reduction over spending and investment, limiting immediate economic recovery.

Lastly, the geopolitical risk premium appears to be fading due to the current silence from Iran. As we have highlighted previously, when a “scheduled” retaliatory strike does not materialize quickly, it reduces any built-in price premium. With no visible retaliation from Iran yesterday, and likely none today or tomorrow, the market is pricing in diminished geopolitical risk. Furthermore, the outcome of the U.S. with a Trump victory may have altered the dynamics of the conflict entirely. It is plausible that Iran will proceed cautiously, anticipating a harsh response (read sanctions) from the U.S. should tensions escalate further.

Looking ahead, the market will be closely monitoring key reports this week: the EIA’s Weekly Petroleum Status Report on Wednesday and the IEA’s Oil Market Report on Thursday.

In summary, we believe that while the demand outlook will eventually stabilize, the strong oil supply continues to act as a suppressing force on prices. Given the current supply environment, there appears to be little room for additional OPEC volumes at this time, a situation the cartel will likely assess continuously on a monthly basis going forward.

With this context, we maintain moderately bullish for next year and continue to see an average Brent price of USD 75 per barrel.

Brent crude prices have remained stable since the sharp price surge on Monday afternoon, when the price jumped from USD 71.5 per barrel to USD 73.5 per barrel – close to current levels (now trading at USD 73.45 per barrel). The initial price spike was triggered by short-term supply disruptions at Norway’s Johan Sverdrup field and Kazakhstan’s Tengiz field.

While the disruptions in Norway have been resolved and production at Tengiz is expected to return to full capacity by the weekend, elevated prices have persisted. The market’s focus has now shifted to heightened concerns about an escalation in the war in Ukraine. This geopolitical uncertainty continues to support safe-haven assets, including gold and government bonds. Consequently, safe-haven currencies such as the U.S. dollar, Japanese yen, and Swiss franc have also strengthened.

U.S. commercial crude oil inventories (excl. SPR) increased by 0.5 million barrels last week, according to U.S DOE. This build contrasts with expectations, as consensus had predicted no change (0.0 million barrels), and the API forecast projected a much larger increase of 4.8 million barrels. With last week’s build, crude oil inventories now stand at 430.3 million barrels, yet down 18 million barrels(!) compared to the same week last year and ish 4% below the five-year average for this time of year.

Gasoline inventories rose by 2.1 million barrels (still 4% below their five-year average), defying consensus expectations of a slight draw of 0.1 million barrels. Distillate (diesel) inventories, on the other hand, fell by 0.1 million barrels, aligning closely with expectations of no change (0.0 million barrels) but also remain 4% below their five-year average. In total, combined stocks of crude, gasoline, and distillates increased by 2.5 million barrels last week.

U.S. demand data showed mixed trends. Over the past four weeks, total petroleum products supplied averaged 20.7 million barrels per day, representing a 1.2% increase compared to the same period last year. Motor gasoline demand remained relatively stable at 8.9 million barrels per day, a 0.5% rise year-over-year. In contrast, distillate fuel demand continued to weaken, averaging 3.8 million barrels per day, down 6.4% from a year ago. Jet fuel demand also softened, falling 1.3% compared to the same four-week period in 2023.

Brent crude is maintaining its gains from Monday and ticking yet higher. Brent crude made a jump of 3.2% on Monday to USD 73.5/b and has managed to maintain the gain since then. Virtually no price change yesterday and opening this morning at USD 73.3/b.

Emerging positive signs from the Chinese economy may lift oil market sentiment. Chinese economic weakness in general and shockingly weak oil demand there has been pestering the oil price since its peak of USD 92.2/b in mid-April. Net Chinese crude and product imports has been negative since May as measured by 3mth y/y changes. This measure reached minus 10% in July and was still minus 3% in September. And on a year to Sep, y/y it is down 2%. Chinese oil demand growth has been a cornerstone of global oil demand over the past decades accounting for a growth of around half a million barrels per day per year or around 40% of yearly global oil demand growth. Electrification and gassification (LNG HDTrucking) of transportation is part of the reason, but that should only have weakened China’s oil demand growth and not turned it abruptly negative. Historically it has been running at around +3-4% pa.

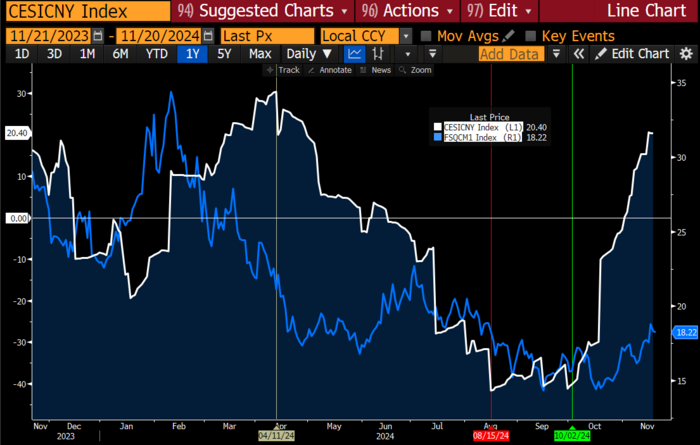

With a sense of ’no end in sight’ for China’ ills and with a trade war rapidly approaching with Trump in charge next year, the oil bears have been in charge of the oil market. Oil prices have moved lower and lower since April. Refinery margins have also fallen sharply along with weaker oil products demand. The front-month gasoil crack to Brent peaked this year at USD 34.4/b (premium to Brent) in February and fell all the way to USD 14.4/b in mid October. Several dollar below its normal seasonal level. Now however it has recovered to a more normal, healthy seasonal level of USD 18.2/b.

But Chinese stimulus measures are already working. The best immediate measure of that is the China surprise index which has rallied from -40 at the end of September to now +20. This is probably starting to filter in to the oil market sentiment.

The market has for quite some time now been staring down towards the USD 60/b. But this may now start to change with a bit more optimistic tones emerging from the Chinese economy.

China economic surprise index (white). Front-month ARA Gasoil crack to Brent in USD/b (blue)

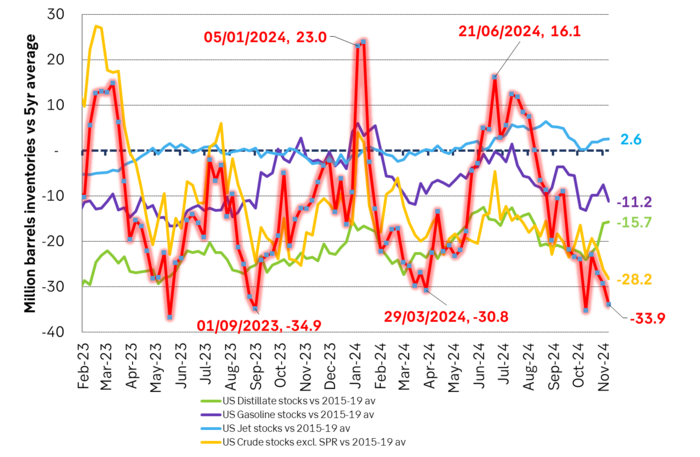

The IEA could be too bearish by up to 0.8 mb/d. IEA’s calculations for Q3-24 are off by 0.8 mb/d. OECD inventories fell by 1.16 mb/d in Q3 according to the IEA’s latest OMR. But according to the IEA’s supply/demand balance the decline should only have been 0.38 mb/d. I.e. the supply/demand balance of IEA for Q3-24 was much less bullish than how the inventories actually developed by a full 0.8 mb/d. If we assume that the OECD inventory changes in Q3-24 is the ”proof of the pudding”, then IEA’s estimated supply/demand balance was off by a full 0.8 mb/d. That is a lot. It could have a significant consequence for 2025 where the IEA is estimating that call-on-OPEC will decline by 0.9 mb/d y/y according to its estimated supply/demand balance. But if the IEA is off by 0.8 mb/d in Q3-24, it could be equally off by 0.8 mb/d for 2025 as a whole as well. Leading to a change in the call-on-OPEC of only 0.1 mb/d y/y instead. Story by Bloomberg: {NSN SMXSUYT1UM0W <GO>}. And looking at US oil inventories they have consistently fallen significantly more than normal since June this year. See below.

Later today at 16:30 CET we’ll have the US oil inventory data. Bearish indic by API, but could be a bullish surprise yet again. Last night the US API indicated that US crude stocks rose by 4.8 mb, gasoline stocks fell by 2.5 mb and distillates fell by 0.7 mb. In total a gain of 1.6 mb. Total US crude and product stocks normally decline by 3.7 mb for week 46.

The trend since June has been that US oil inventories have been falling significantly versus normal seasonal trends. US oil inventories stood 16 mb above the seasonal 2015-19 average on 21 June. In week 45 they ended 34 mb below their 2015-19 seasonal average. Recent news is that US Gulf refineries are running close to max in order to satisfy Lat Am demand for oil products.

US oil inventories versus the 2015-19 seasonal averages.

Since market opening on Monday, November 18, Brent crude prices have climbed steadily. Starting the week at approximately USD 70.7 per barrel, prices rose to USD 71.5 per barrel by noon yesterday. However, in the afternoon, Brent crude surged by nearly USD 2 per barrel, reaching USD 73.5 per barrel, which is close to where we are currently trading.

This sharp price increase has been driven by supply disruptions at two major oil fields: Norway’s Johan Sverdrup and Kazakhstan’s Tengiz. The Brent benchmark is now continuing to trade above USD 73 per barrel as the market reacts to heightened concerns about short-term supply tightness.

Norway’s Johan Sverdrup field, Europe’s largest and one of the top 10 globally in terms of estimated recoverable reserves, temporarily halted production on Monday afternoon due to an onshore power outage. According to Equinor, the issue was quickly identified but resulted in a complete shutdown of the field. Restoration efforts are underway. With a production capacity of 755,000 barrels per day, Sverdrup accounts for approximately 36% of Norway’s total oil output, making it a critical player in the country’s production. The unexpected outage has significantly supported Brent prices as the market evaluates its impact on overall supply.

Adding to the bullish momentum, supply constraints at Kazakhstan’s Tengiz field have further intensified concerns. Tengiz, with a production capacity of around 700,000 barrels per day, has seen output cut by approximately 30% this month due to ongoing repairs, exceeding earlier estimates of a 20% reduction. Repairs are expected to conclude by November 23, but in the meantime, supply tightness persists, amplifying market vol.

On a broader scale, a pullback in the U.S. dollar yesterday (down 0.15%) provided additional tailwinds for crude prices, making oil more attractive to international buyers. However, over the past few weeks, Brent crude has alternated between gains and losses as market participants juggle multiple factors, including U.S. monetary policy, concerns over Chinese demand, and the evolving supply strategy of OPEC+.

The latter remains a critical factor, as unused production capacity within OPEC continues to exert downward pressure on prices. An acceleration in the global economy will be crucial to improving demand fundamentals.

Despite these short-term fluctuations, we see encouraging signs of a recovering global economy and remain moderately bullish. We are holding to our price forecast of USD 75 per barrel in 2025, followed by USD 87.5 in 2026.

Oklart om drill baby drill-politik ökar USAs oljeproduktion

De tre bästa olje- och naturgasaktierna i Kanada

Crude oil comment: US inventories remain well below averages despite yesterday’s build

China is turning the corner and oil sentiment will likely turn with it

Crude oil comment: Europe’s largest oil field halted – driving prices higher

Crude oil comment: A price rise driven by fundamentals

Crude oil comment: Recent ’geopolitical relief’ seems premature

ABB och Blykalla samarbetar om teknikutveckling för små modulära reaktorer

Brent resumes after yesterday’s price tumble

Oljepriset kommer gå upp till 500 USD per fat år 2030

-

Analys3 veckor sedan

Crude oil comment: A price rise driven by fundamentals

-

Analys4 veckor sedan

Crude oil comment: Recent ’geopolitical relief’ seems premature

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanABB och Blykalla samarbetar om teknikutveckling för små modulära reaktorer

-

Analys3 veckor sedan

Brent resumes after yesterday’s price tumble

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOljepriset kommer gå upp till 500 USD per fat år 2030

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMichel Rufli förklarar vad som händer på guldmarknaden

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanTredje staden i Finland som satsar på kärnenergiproducerad fjärrvärme med världens enklaste reaktor

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSilverpriset kan bara gå upp