Analys

Crude oil comment: Europe’s largest oil field halted – driving prices higher

Since market opening on Monday, November 18, Brent crude prices have climbed steadily. Starting the week at approximately USD 70.7 per barrel, prices rose to USD 71.5 per barrel by noon yesterday. However, in the afternoon, Brent crude surged by nearly USD 2 per barrel, reaching USD 73.5 per barrel, which is close to where we are currently trading.

This sharp price increase has been driven by supply disruptions at two major oil fields: Norway’s Johan Sverdrup and Kazakhstan’s Tengiz. The Brent benchmark is now continuing to trade above USD 73 per barrel as the market reacts to heightened concerns about short-term supply tightness.

Norway’s Johan Sverdrup field, Europe’s largest and one of the top 10 globally in terms of estimated recoverable reserves, temporarily halted production on Monday afternoon due to an onshore power outage. According to Equinor, the issue was quickly identified but resulted in a complete shutdown of the field. Restoration efforts are underway. With a production capacity of 755,000 barrels per day, Sverdrup accounts for approximately 36% of Norway’s total oil output, making it a critical player in the country’s production. The unexpected outage has significantly supported Brent prices as the market evaluates its impact on overall supply.

Adding to the bullish momentum, supply constraints at Kazakhstan’s Tengiz field have further intensified concerns. Tengiz, with a production capacity of around 700,000 barrels per day, has seen output cut by approximately 30% this month due to ongoing repairs, exceeding earlier estimates of a 20% reduction. Repairs are expected to conclude by November 23, but in the meantime, supply tightness persists, amplifying market vol.

On a broader scale, a pullback in the U.S. dollar yesterday (down 0.15%) provided additional tailwinds for crude prices, making oil more attractive to international buyers. However, over the past few weeks, Brent crude has alternated between gains and losses as market participants juggle multiple factors, including U.S. monetary policy, concerns over Chinese demand, and the evolving supply strategy of OPEC+.

The latter remains a critical factor, as unused production capacity within OPEC continues to exert downward pressure on prices. An acceleration in the global economy will be crucial to improving demand fundamentals.

Despite these short-term fluctuations, we see encouraging signs of a recovering global economy and remain moderately bullish. We are holding to our price forecast of USD 75 per barrel in 2025, followed by USD 87.5 in 2026.

Up 4.7% last week on US Iran hawkishness and China stimulus optimism. Brent crude gained 4.7% last week and closed on a high note at USD 74.49/b. Through the week it traded in a USD 70.92 – 74.59/b range. Increased optimism over China stimulus together with Iran hawkishness from the incoming Donald Trump administration were the main drivers. Technically Brent crude broke above the 50dma on Friday. On the upside it has the USD 75/b 100dma and on the downside it now has the 50dma at USD 73.84. It is likely to test both of these in the near term. With respect to the Relative Strength Index (RSI) it is neither cold nor warm.

Lower this morning as China November statistics still disappointing (stimulus isn’t here in size yet). This morning it is trading down 0.4% to USD 74.2/b following bearish statistics from China. Retail sales only rose 3% y/y and well short of Industrial production which rose 5.4% y/y, painting a lackluster picture of the demand side of the Chinese economy. This morning the Chinese 30-year bond rate fell below the 2% mark for the first time ever. Very weak demand for credit and investments is essentially what it is saying. Implied demand for oil down 2.1% in November and ytd y/y it was down 3.3%. Oil refining slipped to 5-month low (Bloomberg). This sets a bearish tone for oil at the start of the week. But it isn’t really killing off the oil price either except pushing it down a little this morning.

China will likely choose the US over Iranian oil as long as the oil market is plentiful. It is becoming increasingly apparent that exports of crude oil from Iran is being disrupted by broadening US sanctions on tankers according to Vortexa (Bloomberg). Some Iranian November oil cargoes still remain undelivered. Chinese buyers are increasingly saying no to sanctioned vessels. China import around 90% of Iranian crude oil. Looking forward to the Trump administration the choice for China will likely be easy when it comes to Iranian oil. China needs the US much more than it needs Iranian oil. At leas as long as there is plenty of oil in the market. OPEC+ is currently holds plenty of oil on the side-line waiting for room to re-enter. So if Iran goes out, then other oil from OPEC+ will come back in. So there won’t be any squeeze in the oil market and price shouldn’t move all that much up.

Analys

Brent crude inches higher as ”Maximum pressure on Iran” could remove all talk of surplus in 2025

Brent crude inch higher despite bearish Chinese equity backdrop. Brent crude traded between 72.42 and 74.0 USD/b yesterday before closing down 0.15% on the day at USD 73.41/b. Since last Friday Brent crude has gained 3.2%. This morning it is trading in marginal positive territory (+0.3%) at USD 73.65/b. Chinese equities are down 2% following disappointing signals from the Central Economic Work Conference. The dollar is also 0.2% stronger. None of this has been able to pull oil lower this morning.

”Maximum pressure on Iran” are the signals from the incoming US administration. Last time Donald Trump was president he drove down Iranian oil exports to close to zero as he exited the JCPOA Iranian nuclear deal and implemented maximum sanctions. A repeat of that would remove all talk about a surplus oil market next year leaving room for the rest of OPEC+ as well as the US to lift production a little. It would however probably require some kind of cooperation with China in some kind of overall US – China trade deal. Because it is hard to prevent oil flowing from Iran to China as long as China wants to buy large amounts.

Mildly bullish adjustment from the IEA but still with an overall bearish message for 2025. The IEA came out with a mildly bullish adjustment in its monthly Oil Market Report yesterday. For 2025 it adjusted global demand up by 0.1 mb/d to 103.9 mb/d (+1.1 mb/d y/y growth) while it also adjusted non-OPEC production down by 0.1 mb/d to 71.9 mb/d (+1.7 mb/d y/y). As a result its calculated call-on-OPEC rose by 0.2 mb/d y/y to 26.3 mb/d.

Overall the IEA still sees a market in 2025 where non-OPEC production grows considerably faster (+1.7 mb/d y/y) than demand (+1.1 mb/d y/y) which requires OPEC to cut its production by close to 700 kb/d in 2025 to keep the market balanced.

The IEA treats OPEC+ as it if doesn’t exist even if it is 8 years since it was established. The weird thing is that the IEA after 8 full years with the constellation of OPEC+ still calculates and argues as if the wider organisation which was established in December 2016 doesn’t exist. In its oil market balance it projects an increase from FSU of +0.3 mb/d in 2025. But FSU is predominantly part of OPEC+ and thus bound by production targets. Thus call on OPEC+ is only falling by 0.4 mb/d in 2025. In IEA’s calculations the OPEC+ group thus needs to cut production by 0.4 mb/d in 2024 or 0.4% of global demand. That is still a bearish outlook. But error of margin on such calculations are quite large so this prediction needs to be treated with a pinch of salt.

Brent crude prices have shown a solid recovery this week, gaining USD 2.9 per barrel from Monday’s opening to trade at USD 73.8 this morning. A rebound from last week’s bearish close at USD 70.9 per barrel, the lowest since late October. Brent traded in a range of USD 70.9 to USD 74.28 last week, ending down 2.5% despite OPEC+ delivering a more extended timeline for reintroducing supply cuts. The market’s moderate response underscores a continuous lingering concern about oversupply and muted demand growth.

Yet, hedge funds and other institutional investors began rebuilding their positions in Brent last week amid OPEC+ negotiations. Fund managers added 26 million barrels to their Brent contracts, bringing their net long positions to 157 million barrels – the highest since July. This uptick signals a cautiously optimistic outlook, driven by OPEC+ efforts to manage supply effectively. However, while Brent’s positioning improved to the 35th percentile for weeks since 2010, the WTI positioning, remains in historically bearish territory, reflecting broader market skepticism.

According to CNPC, China’s oil demand is now projected to peak as early as 2025, five years sooner than previous estimates by the Chinese oil major, due to rapid advancements in new-energy vehicles (NEVs) and LNG for trucking. Diesel consumption peaked in 2019, and gasoline demand reached its zenith in 2022. Economic factors and accelerated energy transitions have diminished China’s role as a key driver of global crude demand growth, and India sails up as a key player accounting for demand growth going forward.

Last week’s bearish price action followed an OPEC+ decision to extend the return of 2.2 million barrels per day in supply cuts from January to April. The phased increases – split into 18 increments – are designed to gradually reintroduce sidelined barrels. While this strategy underscores OPEC+’s commitment to market stability, it also highlights the group’s intent to reclaim market share, limiting price upside potential further out. The market continues to find support near the USD 70 per barrel line, with geopolitical tensions providing occasional rallies but failing to shift the overall bearish sentiment for now.

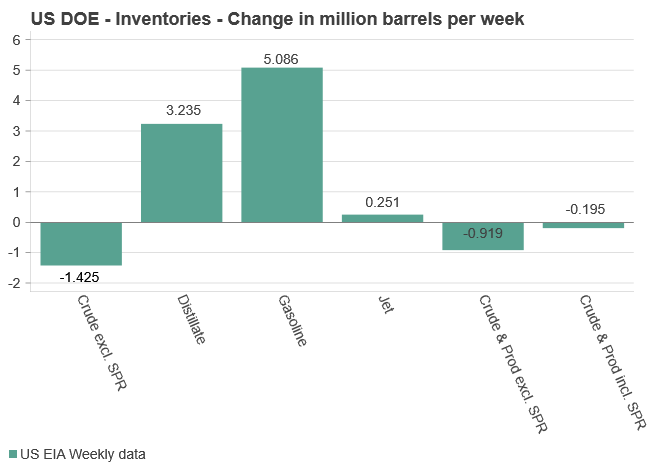

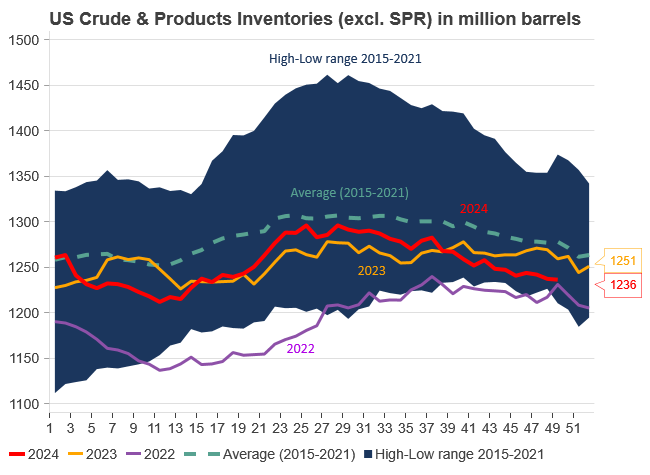

Yesterday, we received US DOE data covering US inventories. Crude oil inventories decreased by 1.4 million barrels last week (API estimated 0.5 million barrels increase), bringing total stocks to 422 million barrels, about 6% below the five-year average for this time of year. Meanwhile, gasoline inventories surged by 5.1 million barrels (API estimated a 2.9 million barrel rise), and distillate (diesel) inventories rose by 3.2 million barrels (API was at a 1.5 million barrel decline). Despite these increases, total commercial petroleum inventories dropped by 0.9 million barrels. Refineries operated at 92.4% capacity, and imports declined significantly by 1.3 million barrels per day. Overall, the inventory development highlights a tightening market here and now, albeit with pockets of a strong supply of refined products.

In summary, Brent crude prices have staged a recovery this week, supported by improving investor sentiment and tightening crude inventories. However, structural shifts in global demand, especially in China, and OPEC+’s cautious supply management strategy continue to anchor market expectations. As the market approaches the year-end, attention will continue to remain on crude and product inventories and geopolitical developments as key price influencers.

Kärnkraft och litet inslag av solenergi ger den billigaste elektriciteten i Japan

Kinas produktion av kol slår nytt rekord

Atnorth ska etablera ett mega-datacenter i Långsele

Oil falling only marginally on weak China data as Iran oil exports starts to struggle

USA öppnar sin 8:e exportterminal för LNG

Guldpriset kommer stå i 3000 USD i slutet av 2025

Crude oil comment: OPEC+ meeting postponement adds new uncertainties

De tre bästa olje- och naturgasaktierna i Kanada

Crude oil comment: Europe’s largest oil field halted – driving prices higher

Crude oil comment: US inventories remain well below averages despite yesterday’s build

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuldpriset kommer stå i 3000 USD i slutet av 2025

-

Analys3 veckor sedan

Crude oil comment: OPEC+ meeting postponement adds new uncertainties

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanDe tre bästa olje- och naturgasaktierna i Kanada

-

Analys4 veckor sedan

Crude oil comment: US inventories remain well below averages despite yesterday’s build

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanOklart om drill baby drill-politik ökar USAs oljeproduktion

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanBixias vinterprognos – Låga elpriser, men inte hela tiden

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanVad den stora uppgången i guldpriset säger om Kina

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMeta vill vara med och bygga 1-4 GW kärnkraft, begär in förslag från kärnkraftsutvecklare