Analys

Brent sideways on sanctions and peace talks

Brent crude is currently trading around USD 66.2 per barrel, following a relatively tight session on Monday, where prices ranged between USD 65.3 and USD 66.8. While expectations of higher OPEC+ supply continue to weigh on sentiment, recent headlines have been dominated by geopolitics – particularly developments in Washington.

At the center is the White House meeting between Trump, Zelenskyy, and several key European leaders. During the meeting, Trump reportedly placed a direct call to Putin to discuss a potential bilateral sit-down between Putin and Zelenskyy, which several European officials have said could take place within two weeks.

While the Kremlin’s response remains vague, markets have interpreted this as a modestly positive signal, with both equities and global oil prices holding steady. Brent is marginally lower since yesterday’s close, while U.S. and Asian equity markets remain broadly flat.

Still, the political undertone is shifting, and markets may be underestimating the longer-term implications. According to the NY times, Putin has proposed a peace plan under which Russia would claim full control of the Donbas in exchange for dropping demands over Kherson and Zaporizhzhia – territories it has not yet seized.

Meanwhile, discussions around Ukraine’s long-term security framework are starting to take shape. Zelenskyy appeared encouraged by Trump’s openness to supporting a post-war security guarantee for Ukraine. While the exact terms remain unclear, U.S. special envoy Steve Witkoff stated that Putin had signaled willingness to allow Washington and its allies to offer Kyiv a NATO-style collective defense guarantee – a move that would significantly reshape the regional security landscape.

As diplomatic efforts gain momentum, markets are also beginning to assess the potential consequences of a partial or full rollback of U.S. sanctions on Russian energy. Any unwind would likely be gradual and uneven, especially if European allies resist or delay alignment. The U.S. could act unilaterally by loosening financial restrictions, granting Russian firms greater access to Western capital and services, and effectively neutralizing the price cap mechanism. However, the EU embargo on Russian crude and products remains a more immediate constraint on flows – particularly as it continues to tighten.

Even if the U.S. were to ease restrictions, Moscow would remain heavily reliant on buyers like India and China to absorb the majority of its crude exports, as European countries are unlikely to quickly re-engage in energy trade. That shift is already playing out. As India pulls back amid newly doubled U.S. tariffs – a response to its ongoing Russian oil purchases – Chinese refiners have stepped in.

So far in August, Chinese imports of Russia’s Urals crude – typically shipped from Baltic and Black Sea ports – have nearly doubled from the YTD average, with at least two tankers idling off Zhoushan and more reportedly en route (Kpler data). The uptick is driven by attractive pricing and the absence of direct U.S. trade penalties on China, which remains in a delicate tariff truce with Washington.

Indian refiners, by contrast, are notably more cautious – receiving offers but accepting few. The takeaway is clear: China is acting as the buyer of last resort for surplus Russian barrels, likely directing them into strategic storage. While this may temporarily cushion the effects of sanctions relief, it cannot fully offset the constraints imposed by Europe’s ongoing absence.

As a result, any meaningful boost to global supply from a rollback of U.S. sanctions on Russia may take longer to materialize than headlines suggest.

Oil prices are likely to fall for a fourth straight year as OPEC+ unwinds cuts and retakes market share. We expect Brent crude to average USD 55/b in Q4/25 before OPEC+ steps in to stabilise the market into 2026. Surplus, stock building, oil prices are under pressure with OPEC+ calling the shots as to how rough it wants to play it. We see natural gas prices following parity with oil (except for seasonality) until LNG surplus arrives in late 2026/early 2027.

Oil market: Q4/25 and 2026 will be all about how OPEC+ chooses to play it

OPEC+ is in a process of unwinding voluntary cuts by a sub-group of the members and taking back market share. But the process looks set to be different from 2014-16, as the group doesn’t look likely to blindly lift production to take back market share. The group has stated very explicitly that it can just as well cut production as increase it ahead. While the oil price is unlikely to drop as violently and lasting as in 2014-16, it will likely fall further before the group steps in with fresh cuts to stabilise the price. We expect Brent to fall to USD 55/b in Q4/25 before the group steps in with fresh cuts at the end of the year.

Natural gas market: Winter risk ahead, yet LNG balance to loosen from 2026

The global gas market entered 2025 in a fragile state of balance. European reliance on LNG remains high, with Russian pipeline flows limited to Turkey and Russian LNG constrained by sanctions. Planned NCS maintenance in late summer could trim exports by up to 1.3 TWh/day, pressuring EU storage ahead of winter. Meanwhile, NE Asia accounts for more than 50% of global LNG demand, with China alone nearing a 20% share (~80 mt in 2024). US shale gas production has likely peaked after reaching 104.8 bcf/d, even as LNG export capacity expands rapidly, tightening the US balance. Global supply additions are limited until late 2026, when major US, Qatari and Canadian projects are due to start up. Until then, we expect TTF to average EUR 38/MWh through 2025, before easing as the new supply wave likely arrives in late 2026 and then in 2027.

Price action contained withing USD 2/b last week. Likely muted today as well with US closed. The Brent November contract is the new front-month contract as of today. It traded in a range of USD 66.37-68.49/b and closed the week up a mere 0.4% at USD 67.48/b. US oil inventory data didn’t make much of an impact on the Brent price last week as it is totally normal for US crude stocks to decline 2.4 mb/d this time of year as data showed. This morning Brent is up a meager 0.5% to USD 67.8/b. It is US Labor day today with US markets closed. Today’s price action is likely going to be muted due to that.

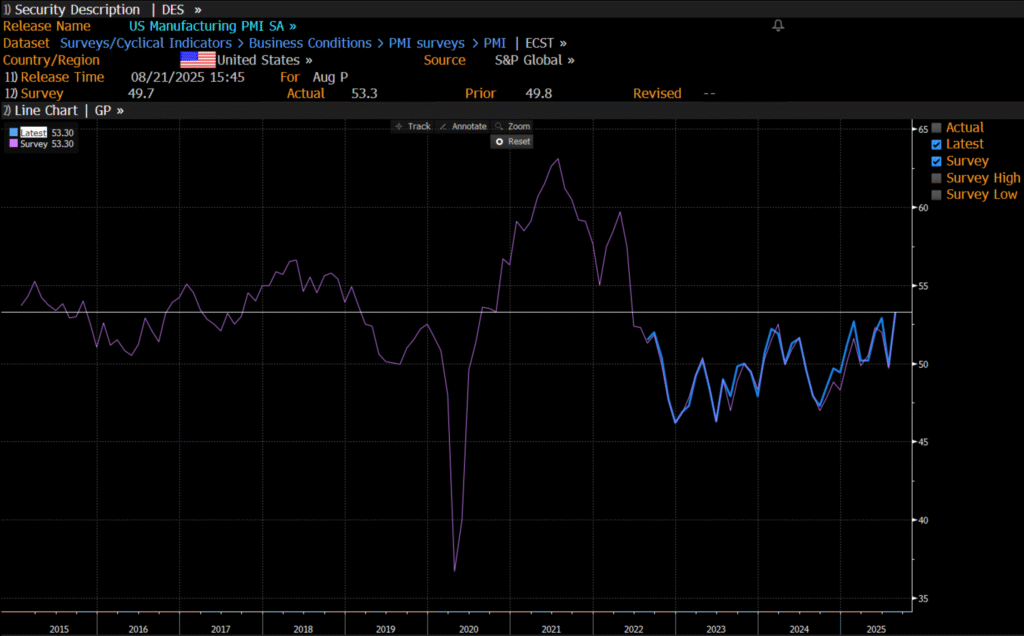

Improving manufacturing readings. China’s manufacturing PMI for August came in at 49.4 versus 49.3 for July. A marginal improvement. The total PMI index ticked up to 50.5 from 50.2 with non-manufacturing also helping it higher. The HCOB Eurozone manufacturing PMI was a disastrous 45.1 last December, but has since then been on a one-way street upwards to its current 50.5 for August. The S&P US manufacturing index jumped to 53.3 in August which was the highest since 2022 (US ISM manufacturing tomorrow). India manufacturing PMI rose further and to 59.3 for August which is the highest since at least 2022.

Are we in for global manufacturing expansion? Would help to explain copper at 10k and resilient oil. JPMorgan global manufacturing index for August is due tomorrow. It was 49.7 in July and has been below the 50-line since February. Looking at the above it looks like a good chance for moving into positive territory for global manufacturing. A copper price of USD 9935/ton, sniffing at the 10k line could be a reflection of that. An oil price holding up fairly well at close to USD 68/b despite the fact that oil balances for Q4-25 and 2026 looks bloated could be another reflection that global manufacturing may be accelerating.

US manufacturing PMI by S&P rose to 53.3 in August. It was published on 21 August, so not at all newly released. But the US ISM manufacturing PMI is due tomorrow and has the potential to follow suite with a strong manufacturing reading.

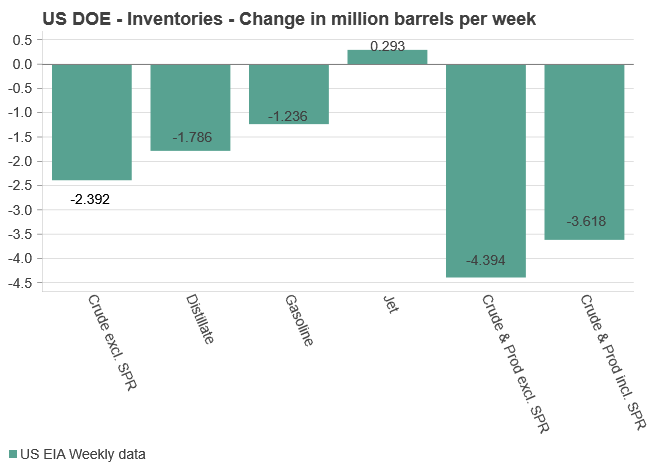

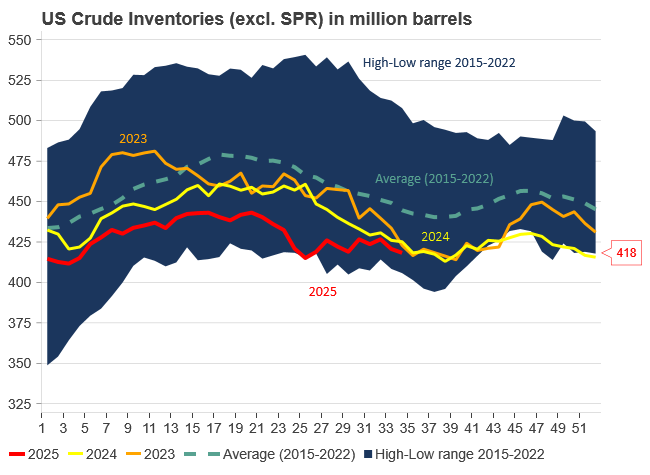

U.S. commercial crude inventories posted another draw last week, falling by 2.4 million barrels to 418.3 million barrels, according to the latest DOE report. Inventories are now 6% below the five-year seasonal average, underlining a persistently tight supply picture as we move into the post-peak demand season.

While the draw was smaller than last week’s 6 million barrel decline, the trend remains consistent with seasonal patterns. Current inventories are still well below the 2015–2022 average of around 449 million barrels.

Gasoline inventories dropped by 1.2 million barrels and are now close to the five-year average. The breakdown showed a modest increase in finished gasoline offset by a decline in blending components – hinting at steady end-user demand.

Diesel inventories saw yet another sharp move, falling by 1.8 million barrels. Stocks are now 15% below the five-year average, pointing to sustained tightness in middle distillates. In fact, diesel remains the most undersupplied segment, with current inventory levels at the very low end of the historical range (see page 3 attached).

Total commercial petroleum inventories – including crude and products but excluding the SPR – fell by 4.4 million barrels on the week, bringing total inventories to approximately 1,259 million barrels. Despite rising refinery utilization at 94.6%, the broader inventory complex remains structurally tight.

On the demand side, the DOE’s ‘products supplied’ metric – a proxy for implied consumption – stayed strong. Total product demand averaged 21.2 million barrels per day over the last four weeks, up 2.5% YoY. Diesel and jet fuel were the standouts, up 7.7% and 1.7%, respectively, while gasoline demand softened slightly, down 1.1% YoY. The figures reflect a still-solid late-summer demand environment, particularly in industrial and freight-related sectors.

Råvaror har nästan aldrig varit så här billiga

Världens största sandbatteri invigt i Finland

Gurkodling får 3 MW el-effekt i södra Sverige

Eurobattery Minerals satsar på kritiska metaller för Europas självförsörjning

Ett samtal om guld, silver, uran, koppar och olja

Omgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

Meta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

Guld stiger till över 3500 USD på osäkerhet i världen

What OPEC+ is doing, what it is saying and what we are hearing

Aker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanOmgående mångmiljardfiasko för Equinors satsning på Ørsted och vindkraft

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanMeta bygger ett AI-datacenter på 5 GW och 2,25 GW gaskraftverk

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanGuld stiger till över 3500 USD på osäkerhet i världen

-

Analys4 veckor sedan

What OPEC+ is doing, what it is saying and what we are hearing

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanAker BP gör ett av Norges största oljefynd på ett decennium, stärker resurserna i Yggdrasilområdet

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanEtt samtal om koppar, kaffe och spannmål

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanSommarens torka kan ge högre elpriser i höst

-

Analys2 veckor sedan

Brent edges higher as India–Russia oil trade draws U.S. ire and Powell takes the stage at Jackson Hole