Analys

Brent rebound is likely as Biden-sanctions are creating painful tightness

Bearish week last week and dipping lower this morning on China manufacturing and Trump-tariffs. Brent crude traded down 4 out of five days last week and lost 2.8% on a Friday-to-Friday basis with a close of USD 78.5/b. It hit the low of USD 77.8/b on Friday while it managed to make a small 0.3% gain at the end of the week with a close that was marginally below the 200dma. This morning it is trading down 0.4% at USD 78.2/b amid general market bearishness. China manufacturing PMI down to 49.1 for January versus 50.1 in December is pulling copper down 1.3%. Trump threatening Colombia with tariffs.

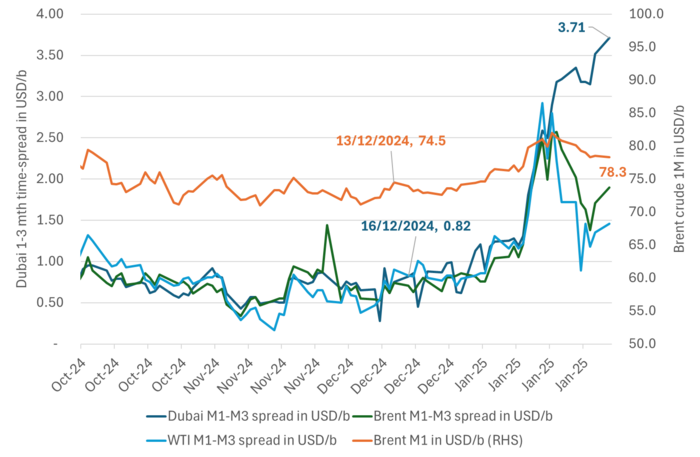

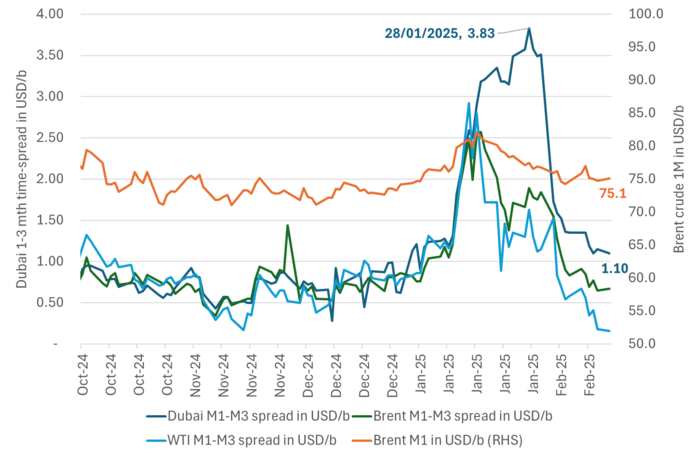

Rebound in crude prices likely as Dubai time-spreads rises further. The Dubai 1-3mth time-spread is rising to a new high this morning of USD 3.7/b. It is a sign that the Biden-sanctions towards Russia is making the medium sour crude market very tight. Brent crude is unlikely to fall much lower as long as these sanctions are in place. Will likely rebound.

Asian buyers turning to the Mid-East to replace Russian barrels. Amin Nasser, CEO of Saudi Aramco, said that the new sanctions are affecting 2 out of 3.4 mb/d of Russian seaborne crude oil exports. Strong bids for Iraqi medium and heavy crudes are sending spot prices to Asia to highest premiums versus formula pricing since August 2023. And Europe is seeing spot premiums to formula pricing at highest since 2021 (Argus).

Strong rise in US oil production is a losing hand. A lot of Trump-talk about a 3 mb/d increase in US oil production. Occidental Petroleum CEO Vicki Hollub commented in Davos that it is possible given the US resource base, but it is not the right thing to do since the global market is oversupplied (Argus). Everyone knows that OPEC+ has a spare capacity of 5-6 mb/d on hand. The comfort zone is probably to have a spare capacity of around 3 mb/d. FIRST the group needs to re-deploy some 3 mb/d of its current spare capacity and THEN the US and the rest of non-OPEC+ can start to think about acceleration in supply growth again. Vicki Hollub understands this and highly likely all the other oil CEOs in the US understands this as well. Donald Trump calling for more US oil will not be met before market circumstances allows it. Even sanctions on Iran forcing 1.5-2.0 mb/d of its crude exports out of the market will first be covered by existing surplus spare capacity within OPEC6+ and not the US.

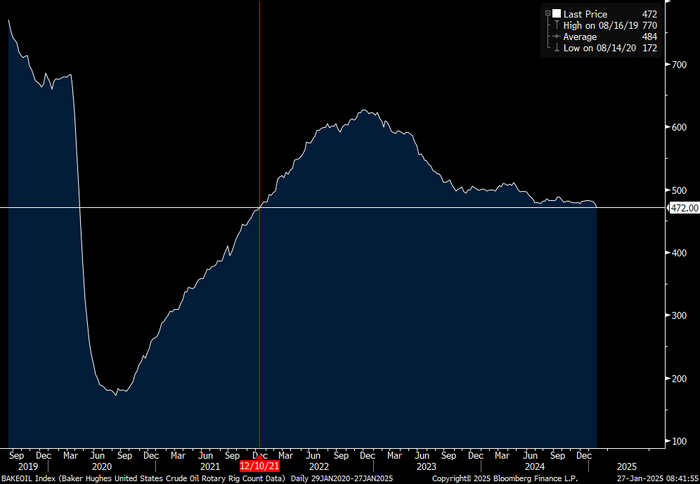

US oil drilling rig count fell by 6 to 472 last week and lowest since October 2021. Current decline could be due to winter weather in the US but could also be like Hollub commented in Davos arguing that US oil production growth is not the right thing to do.

1-3mth time-spreads in USD/b. Dubai to yet higher level this morning. Even Brent and WTI are rebounding. Could be some extra spike since we are moving towards the end of the month. But it is still indicating a very tight market for medium sour crude as a result of the latest Biden-sanctions.

US oil drilling rig count down 6 last week to lowest level since October 2021

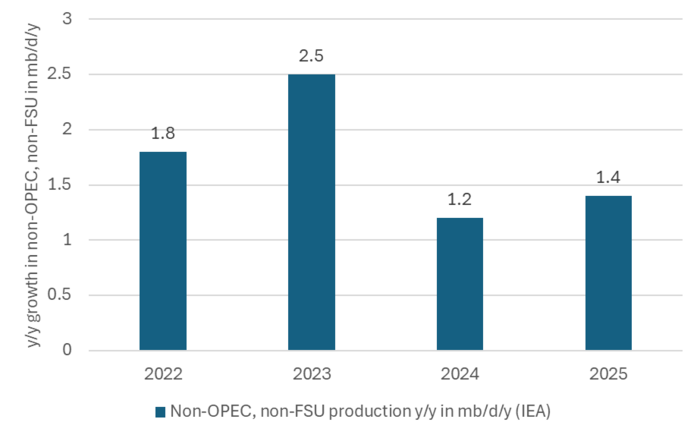

Non-OPEC, non-FSU production to grow 1.4 mb/d in 2025. Third weakest in 4 years. Though still a bit more than total expected global oil demand growth of 1.1 mb/d/y (IEA)

Yesterday’s US DOE report revealed an increase of 4.6 million barrels in US crude oil inventories for the week ending February 14. This build was slightly higher than the API’s forecast of +3.3 million barrels and compared with a consensus estimate of +3.5 million barrels. As of this week, total US crude inventories stand at 432.5 million barrels – ish 3% below the five-year average for this time of year.

In addition, gasoline inventories saw a slight decrease of 0.2 million barrels, now about 1% below the five-year average. Diesel inventories decreased by 2.1 million barrels, marking a 12% drop from the five-year average for this period.

Refinery utilization averaged 84.9% of operable capacity, a slight decrease from the previous week. Refinery inputs averaged 15.4 million barrels per day, down by 15 thousand barrels per day from the prior week. Gasoline production decreased to an average of 9.2 million barrels per day, while diesel production increased to 4.7 million barrels per day.

Total products supplied (implied demand) over the last four-week period averaged 20.4 million barrels per day, reflecting a 3.7% increase compared to the same period in 2024. Specifically, motor gasoline demand averaged 8.4 million barrels per day, up by 0.4% year-on-year, and diesel demand averaged 4.3 million barrels per day, showing a strong 14.2% increase compared to last year. Jet fuel demand also rose by 4.3% compared to the same period in 2024.

Analys

Higher on confidence OPEC+ won’t lift production. Taking little notice of Trump sledgehammer to global free trade

Ticking higher on confidence that OPEC+ won’t lift production in April. Brent crude gained 0.8% yesterday with a close of USD 75.84/b. This morning it is gaining another 0.7% to USD 76.3/b. Signals the latest days that OPEC+ is considering a delay to its planned production increase in April and the following months is probably the most important reason. But we would be surprised if that wasn’t fully anticipated and discounted in the oil price already. News this morning that there are ”green shots” to be seen in the Chinese property market is macro-positive, but industrial metals are not moving. It is naturally to be concerned about the global economic outlook as Donald Trump takes a sledgehammer smashing away at the existing global ”free-trade structure” with signals of 25% tariffs on car imports to the US. The oil price takes little notice of this today though.

Kazakhstan CPC crude flows possibly down 30% for months due to damaged CPC pumping station. The Brent price has been in steady decline since mid-January but seems to have found some support around the USD 74/b mark, the low point from Thursday last week. Technically it is inching above the 50dma today with 200dma above at USD 77.64/b. Oil flowing from Kazakhstan on the CPC line may be reduced by 30% until the Krapotkinskaya oil pumping station is repaired. That may take several months says Russia’s Novak. This probably helps to add support to Brent crude today.

The Brent crude 1mth contract with 50dma, 100dma, 200dma and RSI. Nothing on the horizon at the moment which makes us expect any imminent break above USD 80/b

Analys

Brent looks to US production costs. Taking little notice of Trump-tariffs and Ukraine peace-dealing

Brent crude hardly moved last week taking little notice of neither tariffs nor Ukraine peace-dealing. Brent crude traded up 0.1% last week to USD 74.74/b trading in a range of USD 74.06 – 77.29/b. Fluctuations through the week may have been driven by varying signals from the Putin-Trump peace negotiations over Ukraine. This morning Brent is up 0.4% to USD 75/b. Gain is possibly due to news that a Caspian pipeline pumping station has been hit by a drone with reduced CPC (Kazaksthan) oil flows as a result.

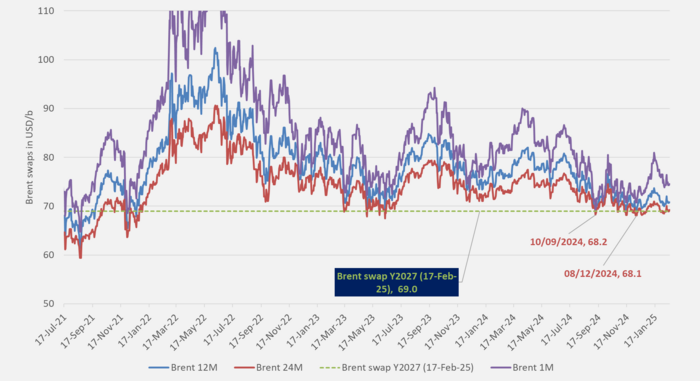

Brent front-month contract rock solid around the USD 75/b mark. The Brent crude price level of around USD 75/b hardly moved an inch week on week. Fear that Trump-tariffs will hurt global economic growth and oil demand growth. No impact. Possibility that a peace deal over Ukraine will lead to increased exports of oil from Russia. No impact. On the latter. Russian oil production at 9 mb/band versus a more normal 10 mb/d and comparably lower exports is NOT due to sanctions by the EU and the US. Russia is part of OPEC+, and its production is aligned with Saudi Arabia at 9 mb/d and the agreement Russia has made with Saudi Arabia and OPEC+ under the Declaration of Cooperation (DoC). Though exports of Russian crude and products has been hampered a little by the new Biden-sanctions on 10 January, but that effect is probably fading by the day as oil flows have a tendency to seep through the sanction barriers over time. A sharp decline in time-spreads is probably a sign of that.

Longer-dated prices zoom in on US cost break-evens with 5yr WTI at USD 63/b and Brent at USD 68-b. Argus reported on Friday that a Kansas City Fed survey last month indicated an average of USD 62/b for average drilling and oil production in the US to be profitable. That is down from USD 64/b last year. In comparison the 5-year (60mth) WTI contract is trading at USD 62.8/b. Right at that level. The survey response also stated that an oil price of sub-USD 70/b won’t be enough over time for the US oil industry to make sufficient profits with decline capex over time with sub-USD 70/b prices. But for now, the WTI 5yr is trading at USD 62.8/b and the Brent crude 5-yr is trading at USD 67.7/b.

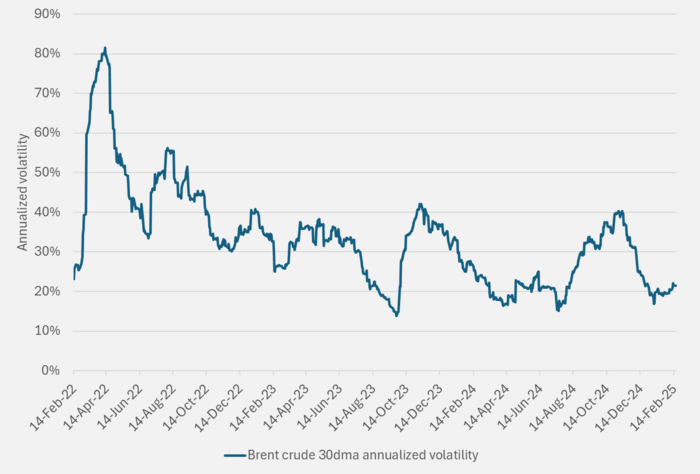

Volatility comes in waves. Brent crude 30dma annualized volatility.

1 to 3 months’ time-spreads have fallen back sharply. Crude oil from Russia and Iran may be seeping through the 10 Jan Biden-sanctions.

Brent crude 1M, 12M, 24M and Y2027 prices.

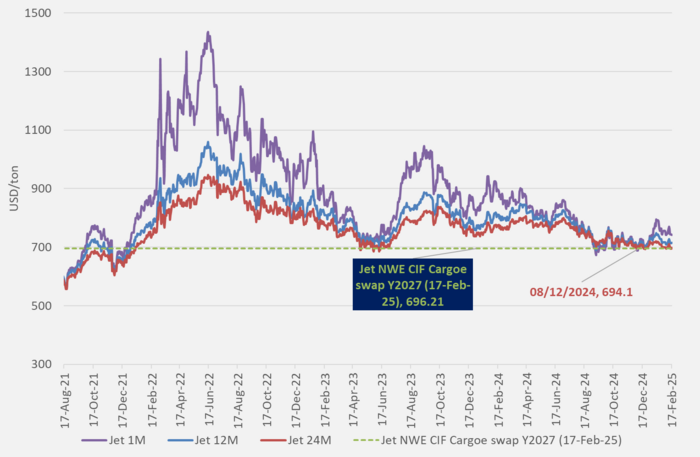

ARA Jet 1M, 12M, 24M and Y2027 prices.

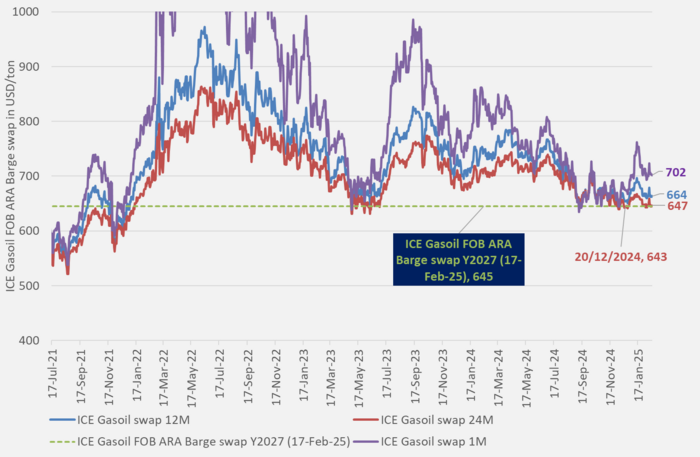

ICE Gasoil 1M, 12M, 24M and Y2027 prices.

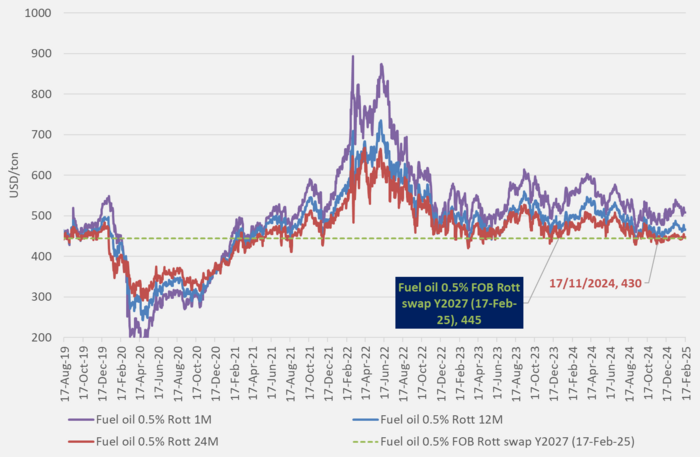

Rotterdam Fuel oil 0.5% 1M, 12M, 24M and Y2027 prices.

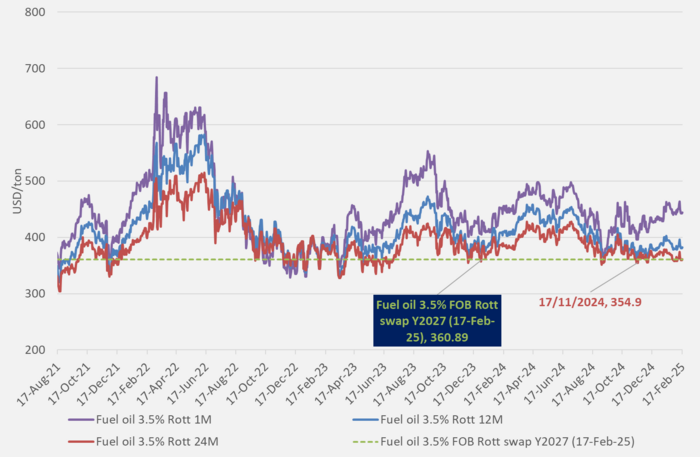

Rotterdam Fuel oil 3.5% 1M, 12M, 24M and Y2027 prices.

Stronger inventory build than consensus, diesel demand notable

Hemp Innovation skriver off-take-avtal för industriell hampafiber

Vizsla Silver går från prospektering till utveckling

Eric Strand kommenterar vad som händer med guld och silver

Higher on confidence OPEC+ won’t lift production. Taking little notice of Trump sledgehammer to global free trade

Belgien gör en u-sväng, går från att lägga ner kärnkraft till att bygga ny

Fondförvaltare köper aktier i kanadensiska guldproducenter när valutan faller

Brent rebound is likely as Biden-sanctions are creating painful tightness

Prisskillnaden mellan råoljorna WCS och WTI vidgas med USA:s tariffkrig

Priset på arabica-kaffebönor är nu över 4 USD per pund för första gången någonsin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanBelgien gör en u-sväng, går från att lägga ner kärnkraft till att bygga ny

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanFondförvaltare köper aktier i kanadensiska guldproducenter när valutan faller

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanPrisskillnaden mellan råoljorna WCS och WTI vidgas med USA:s tariffkrig

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanPriset på arabica-kaffebönor är nu över 4 USD per pund för första gången någonsin

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanPå lördag inför USA tariff på 25 procent för import från Kanada, olja kan dock undantas

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanVirke, råvaran som är Kanadas trumfkort mot USA

-

Analys3 veckor sedan

The Damocles Sword of OPEC+ hanging over US shale oil producers

-

Analys3 veckor sedan

Crude oill comment: Caught between trade war fears and Iranian supply disruption risk