Analys

A lower oil price AND a softer USD will lift global appetite for oil

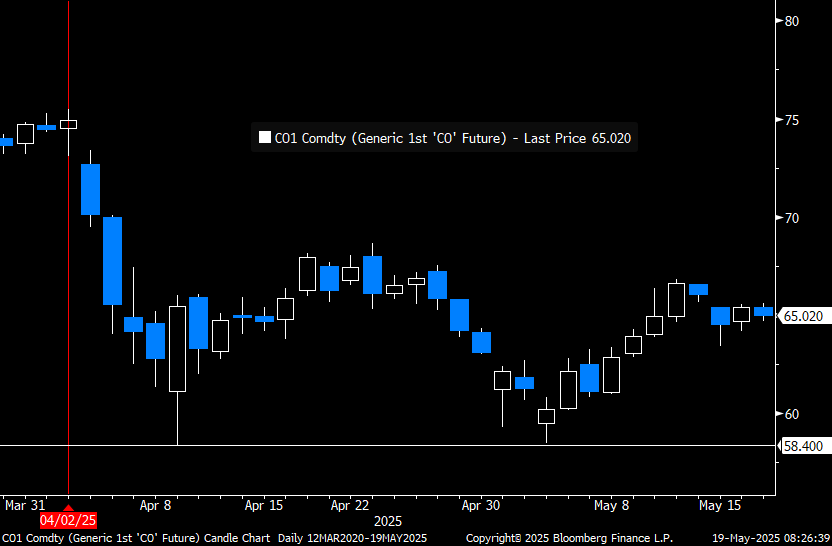

Brent starting in read after a week of 2.4% tariff relief gain. Brent crude gained 2.4% (+USD 1.5/b) last week with a close of USD 65.41/b and traded the week in a range of USD 64.53 – 66.63/b. Price gains last week aligned with dissipating tariff angst as China – US trade tariffs were lowered to 10% and 30% respectively. Down from a staggering 125% and 145% though with the risk for a snap-back after 90 days. The low of the week coincided with rumors that an Iran – US nuclear deal was near at hand. But was later downplayed. Such a deal may not add all that much more oil to the market as most of Iran’s oil probably already is in the market through different pathways. Brent crude is pulling back 0.9% this morning to USD 64.9/b while the USD index is declining 0.5% as well. That is usually a positive for the oil price as it makes oil cheaper for all non-USD based consumers. US equity futures are also down 1% this morning. Chinese new and used housing prices fell 0.12% and 0.41% respectively last month with property investments down 10.3% YTD YoY. All weaker than expected. Chinese industrial production YoY however came in at 6.1% and better than the expected 5.7%. Overall a rather weak start of the week nonetheless.

While down this morning, Brent crude is surprisingly not shedding all that much value given the rather bearish backdrop of US equity futures in the red and everyone and their grandmothers forecasting doom and gloom for the oil price.

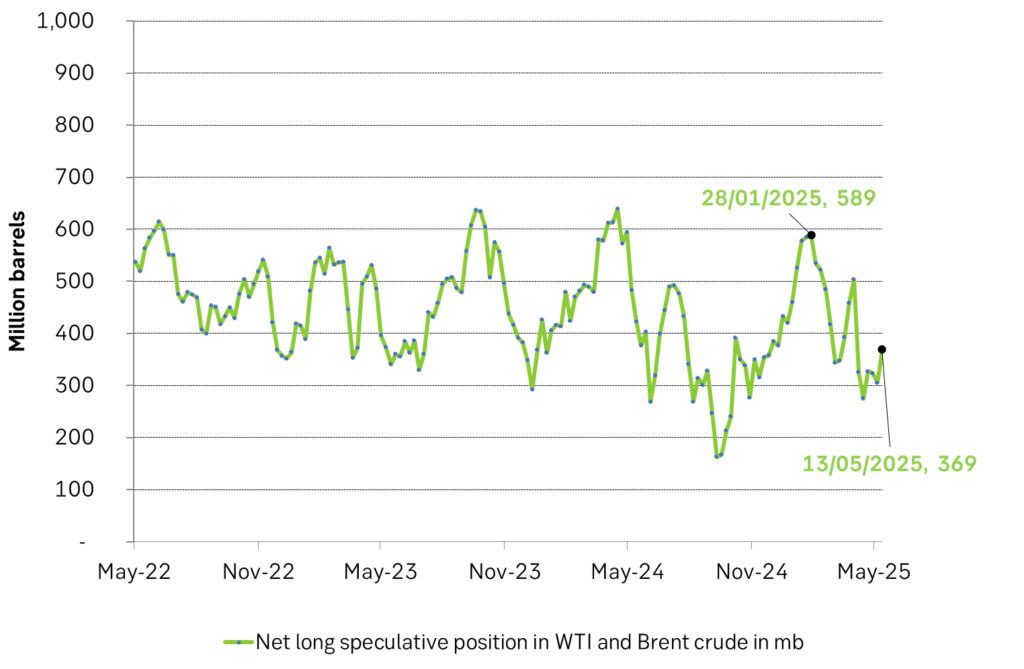

Speculators added 64 mb to net long positions in Brent crude and WTI over the week to last Tuesday. Most likely as a result of US-China tariffs being shifted down to livable levels. Most headlines and forecasts are however overall very bearish for oil. More oil from OPEC+ in the months to come coupled with expectations for a slowdown in global oil demand growth due to the US tariff trade war.

A lower oil price AND a softer USD will likely bolster global oil demand vs very bearish expectations. Global oil demand growth could surprise to the upside amid all the gloom. In EUR/b terms the the current price of Brent crude is now 22% lower than the average price in 2024. A softer oil price AND a softer USD is making oil considerably cheaper in the eyes of the global oil consumer ex-US. And that portion of global oil demand after all accounts for around 80% of global consumption. We could thus quickly see a Brent crude price down 30% versus 2024 average for 80% of the world’s consumers with a little further decline in USD-oil and the USD itself. This will likely help to boost oil demand globally. Remember also that a very important reason for why OPEC+ wanted to lift its oil production in May and June was to meet sharply stronger Middle East summer oil demand. A note on oil demand. India’s road fuel demand was up 5% YoY in April while its PMI rose to 58.2%. The IEA expects India oil demand to rise by only 2.3% to 5.77 mb/d YoY (+130 kb/d) while a 5% demand growth would yield a demand growth of 282 kb/d YoY.

OPEC+ has NOT abandoned market control. This is not 2014/15/16 or 2020. It is important to remember that the group has not abandoned its general plan of adding 2.2 mb/d from April 2025 to December 2026. The path will be decided on a monthly basis and can be moved both up AND down. The group has NOT abandoned market control. Though it is on a gradual pace to retake 2.2 mb/d of market share. US shale oil production has to stand back to make room and global consumers will respond with stronger demand growth in response to a lower oil price made additionally cheaper by a softening USD.

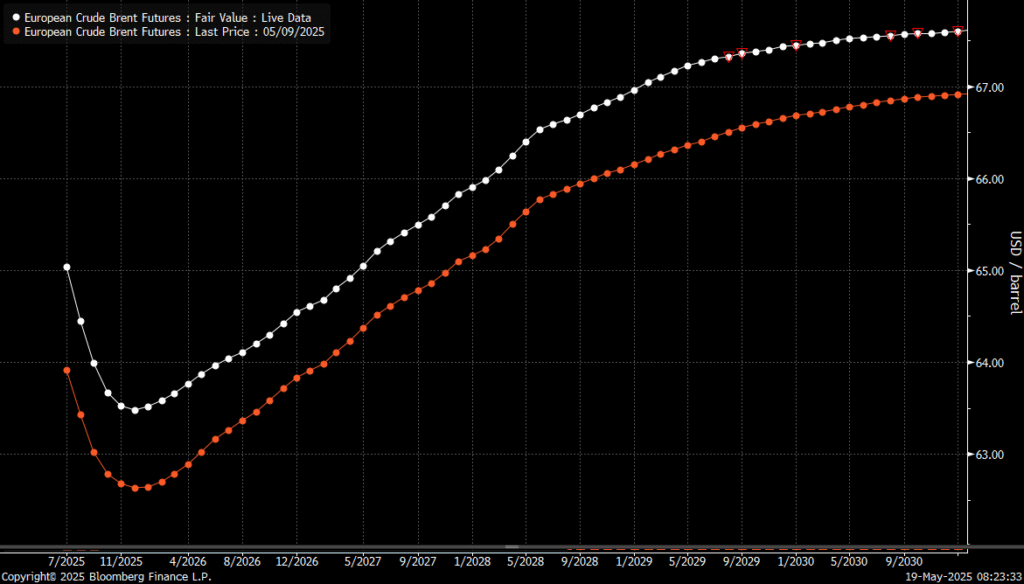

Brent crude forward curve in front-end backwardation. Surplus is not yet here.

Brent crude in USD/b. Little upside conviction to be found anywhere.

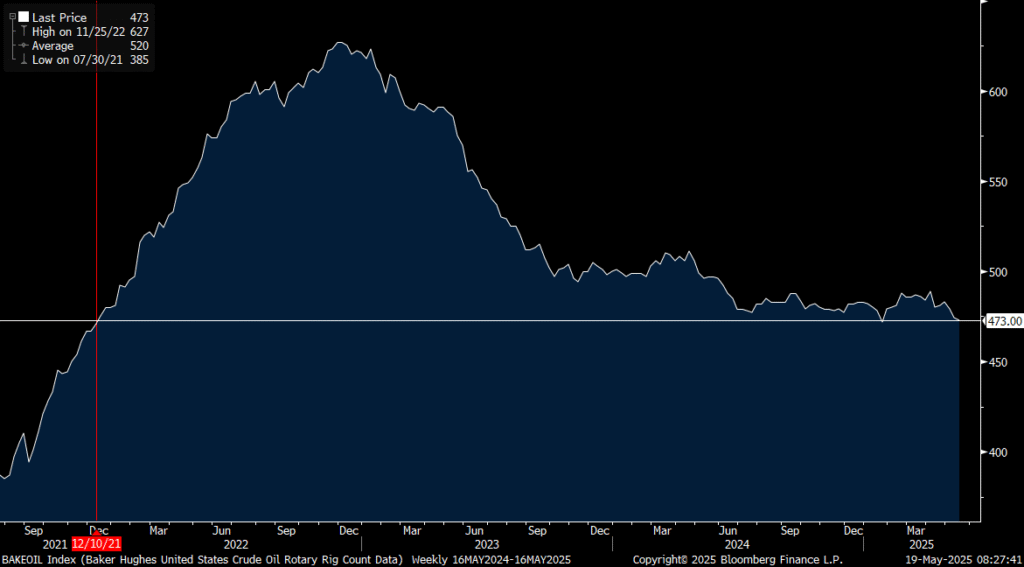

US oil drilling rig count fell by 1 last week to second lowest since December 2021. No real shedding of drilling quite yet. But we’ll likely see a drop of 5-10% over the coming months. It could drop as much as 5-10 rigs per week.

Net long speculative positions in Brent crude + WTI rebounded 64 mb to Tuesday last week.

Brent jumping 2.4% as OPEC+ lifts quota by ”only” 411 kb/d in July. Brent crude is jumping 2.4% this morning to USD 64.3/b following the decision by OPEC+ this weekend to lift the production cap of ”Voluntary 8” (V8) by 411 kb/d in July and not more as was feared going into the weekend. The motivation for the triple hikes of 411 kb/d in May and June and now also in July has been a bit unclear: 1) Cheating by Kazakhstan and Iraq, 2) Muhammed bin Salman listening to Donald Trump for more oil and a lower oil price in exchange for weapons deals and political alignments in the Middle East and lastly 3) Higher supply to meet higher demand for oil this summer. The argument that they are taking back market share was already decided in the original plan of unwinding the 2.2 mb/d of V8 voluntary cuts by the end of 2026. The surprise has been the unexpected speed with monthly increases of 3×137 kb/d/mth rather than just 137 kb/d monthly steps.

No surplus yet. Time-spreads tightened last week. US inventories fell the week before last. In support of point 3) above it is worth noting that the Brent crude oil front-end backwardation strengthened last week (sign of tightness) even when the market was fearing for a production hike of more than 411 kb/d for July. US crude, diesel and gasoline stocks fell the week before last with overall commercial stocks falling 0.7 mb versus a normal rise this time of year of 3-6 mb per week. So surplus is not here yet. And more oil from OPEC+ is welcomed by consumers.

Saudi Arabia calling the shots with Russia objecting. This weekend however we got to know a little bit more. Saudi Arabia was predominantly calling the shots and decided the outcome. Russia together with Oman and Algeria opposed the hike in July and instead argued for zero increase. What this alures to in our view is that it is probably the cheating by Kazakhstan and Iraq which is at the heart of the unexpectedly fast monthly increases. Saudi Arabia cannot allow it to be profitable for the individual members to cheat. And especially so when Kazakhstan explicitly and blatantly rejects its quota obligation stating that they have no plans of cutting production from 1.77 mb/d to 1.47 mb/d. And when not even Russia is able to whip Kazakhstan into line, then the whole V8 project is kind of over.

Is it simply a decision by Saudi Arabia to unwind faster altogether? What is still puzzling though is that despite the three monthly hikes of 411 kb/d, the revival of the 2.2 mb/d of voluntary production cuts is still kind of orderly. Saudi Arabia could have just abandoned the whole V8 project from one month to the next. But we have seen no explicit communication that the plan of reviving the cuts by the end of 2026 has been abandoned. It may be that it is simply a general change of mind by Saudi Arabia where the new view is that production cuts altogether needs to be unwinded sooner rather than later. For Saudi Arabia it means getting its production back up to 10 mb/d. That implies first unwinding the 2.2 mb/d and then the next 1.6 mb/d.

Brent would likely crash with a fast unwind of 2.2 + 1.6 mb/d by year end. If Saudi Arabia has decided on a fast unwind it would meant that the group would lift the quotas by 411 kb/d both in August and in September. It would then basically be done with the 2.2 mb/d revival. Thereafter directly embark on reviving the remaining 1.6 mb/d. That would imply a very sad end of the year for the oil price. It would then probably crash in Q4-25. But it is far from clear that this is where we are heading.

Brent needs to fall to USD 58/b or lower to make it unprofitable for Kazakhstan to cheat. To make it unprofitable for Kazakhstan to cheat. Kazakhstan is currently producing 1.77 mb/d versus its quota which before the hikes stood at 1.47 kb/d. If they had cut back to the quota level they might have gotten USD 70/b or USD 103/day. Instead they choose to keep production at 1.77 mb/d. For Saudi Arabia to make it a loss-making business for Kazakhstan to cheat the oil price needs to fall below USD 58/b ( 103/1.77).

Tariffs or no tariffs played ping pong with Brent crude yesterday. Brent crude traded to a joyous high of USD 66.13/b yesterday as a US court rejected Trump’s tariffs. Though that ruling was later overturned again with Brent closing down 1.2% on the day to USD 64.15/b.

US commercial oil inventories fell 0.7 mb last week versus a seasonal normal rise of 3-6 mb. US commercial crude and product stocks fell 0.7 mb last week which is fairly bullish since the seasonal normal is for a rise of 4.3 mb. US crude stocks fell 2.8 mb, Distillates fell 0.7 mb and Gasoline stocks fell 2.4 mb.

All eyes are now on OPEC V8 (Saudi Arabia, Iraq, Kuwait, UAE, Algeria, Russia, Oman, Kazakhstan) which will make a decision tomorrow on what to do with production for July. Overall they are in a process of placing 2.2 mb/d of cuts back into the market over a period stretching out to December 2026. Following an expected hike of 137 kb/d in April they surprised the market by lifting production targets by 411 kb/d for May and then an additional 411 kb/d again for June. It is widely expected that the group will decide to lift production targets by another 411 kb/d also for July. That is probably mostly priced in the market. As such it will probably not have all that much of a bearish bearish price impact on Monday if they do.

It is still a bit unclear what is going on and why they are lifting production so rapidly rather than at a very gradual pace towards the end of 2026. One argument is that the oil is needed in the market as Middle East demand rises sharply in summertime. Another is that the group is partially listening to Donald Trump which has called for more oil and a lower price. The last is that Saudi Arabia is angry with Kazakhstan which has produced 300 kb/d more than its quota with no indications that they will adhere to their quota.

So far we have heard no explicit signal from the group that they have abandoned the plan of measured increases with monthly assessments so that the 2.2 mb/d is fully back in the market by the end of 2026. If the V8 group continues to lift quotas by 411 kb/d every month they will have revived the production by the full 2.2 mb/d already in September this year. There are clearly some expectations in the market that this is indeed what they actually will do. But this is far from given. Thus any verbal wrapping around the decision for July quotas on Saturday will be very important and can have a significant impact on the oil price. So far they have been tightlipped beyond what they will do beyond the month in question and have said nothing about abandoning the ”gradually towards the end of 2026” plan. It is thus a good chance that they will ease back on the hikes come August, maybe do no changes for a couple of months or even cut the quotas back a little if needed.

Significant OPEC+ spare capacity will be placed back into the market over the coming 1-2 years. What we do know though is that OPEC+ as a whole as well as the V8 subgroup specifically have significant spare capacity at hand which will be placed back into the market over the coming year or two or three. Probably an increase of around 3.0 – 3.5 mb/d. There is only two ways to get it back into the market. The oil price must be sufficiently low so that 1) Demand growth is stronger and 2) US shale oil backs off. In combo allowing the spare capacity back into the market.

Low global inventories stands ready to soak up 200-300 mb of oil. What will cushion the downside for the oil price for a while over the coming year is that current, global oil inventories are low and stand ready to soak up surplus production to the tune of 200-300 mb.

Following the rebound on Wednesday last week – when Brent reached an intra-week high of USD 66.6 per barrel – crude oil prices have since trended lower. Since opening at USD 65.4 per barrel on Monday this week, prices have softened slightly and are currently trading around USD 64.7 per barrel.

This morning, oil prices are trading sideways to slightly positive, supported by signs of easing trade tensions between the U.S. and the EU. European equities climbed while long-term government bond yields declined after President Trump announced a pause in new tariffs yesterday, encouraging hopes of a transatlantic trade agreement.

The optimisms were further supported by reports indicating that the EU has agreed to fast-track trade negotiations with the U.S.

More significantly, crude prices appear to be consolidating around the USD 65 level as markets await the upcoming OPEC+ meeting. We expect the group to finalize its July output plans – driven by the eight key producers known as the “Voluntary Eight” – on May 31st, one day ahead of the original schedule.

We assign a high probability to another sizeable output increase of 411,000 barrels per day. However, this potential hike seems largely priced in already. While a minor price dip may occur on opening next week (Monday morning), we expect market reactions to remain relatively muted.

Meanwhile, the U.S. president expressed optimism following the latest round of nuclear talks with Iran in Rome, describing them as “very good.” Although such statements should be taken with caution, a positive outcome now appears more plausible. A successful agreement could eventually lead to the return of more Iranian barrels to the global market.

Brookfield ska bygga ett AI-datacenter på hela 750 MW i Strängnäs

Tradingfirman XTX Markets bygger datacenter i finska Kajana för 1 miljard euro

Sommaren inleds med sol och varierande elpriser

Brent needs to fall to USD 58/b to make cheating unprofitable for Kazakhstan

OPEC+ ökar oljeproduktionen trots fallande priser

Rebound to $65: trade tensions ease, comeback in fundamentals

Nystart för koppargruvan Viscaria i Kiruna – en av Europas största

Förenade Arabemiraten siktar på att bygga ett datacenter på 5 GW, motsvarande fem stora kärnkraftsreaktorer

Oil slips as Iran signals sanctions breakthrough

A lower oil price AND a softer USD will lift global appetite for oil

-

Analys3 veckor sedan

Rebound to $65: trade tensions ease, comeback in fundamentals

-

Nyheter4 veckor sedan

Nyheter4 veckor sedanNystart för koppargruvan Viscaria i Kiruna – en av Europas största

-

Analys3 veckor sedan

Oil slips as Iran signals sanctions breakthrough

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanFörenade Arabemiraten siktar på att bygga ett datacenter på 5 GW, motsvarande fem stora kärnkraftsreaktorer

-

Analys4 veckor sedan

Whipping quota cheaters into line is still the most likely explanation

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanStark affär för Pan American – men MAG Silvers aktieägare kan bli förlorare

-

Nyheter2 veckor sedan

Nyheter2 veckor sedanSamtal om när oljepriserna vänder och gruvindustrins största frågor

-

Nyheter3 veckor sedan

Nyheter3 veckor sedanAnton Löf kommenterar industrimetaller, tillståndsprocesser och svenska gruvor