Analys

Silver outlook to Q4 2021: A year for the hybrid metal

Nitesh Shah, Director, Research, WisdomTree, provides his 2021 outlook for silver, including the potential drivers of performance and the continued recovery of industrial demand.

“After a slow start, silver outpaced gold and most industrial metals in 2020. Initially riding gold’s defensive coattails and then getting a tailwind from its industrial traits, silver was an outperformer, gaining 47% in 2020. That compares to gold (24%), copper (27%) and nickel (21%). Silver’s hybrid status served it well in 2020 and we expect more of the same in 2021. As we articulated in Gold outlook to Q4 2021: at the crossroads of hope and fear, we start 2021 with the hope that COVID-19 vaccines will offer a route out of the malaise that the pandemic has wreaked on the health of the human population and the economies that we operate in. However, as has been abundantly clear in December 2020, the path to the recovery is likely to have many bumps along the road. Silver, playing both a defensive and cyclical role could do very well this year.

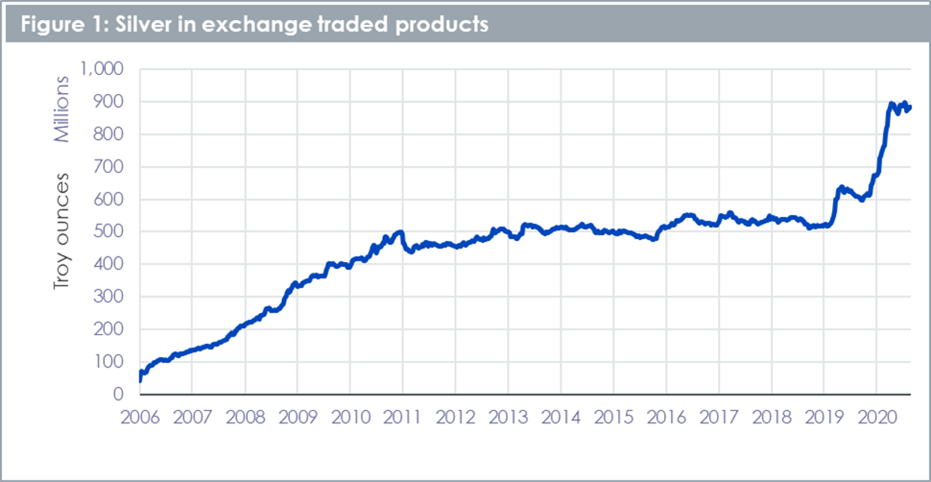

“Silver’s hybrid status has not gone unnoticed by investors. Silver held in exchange traded products (ETPs) rose to an all-time high in 2020 (Figure 1), and more remarkably at a pace never seen before. With 275mn ounces of silver added to silver exchange traded commodities in 2020, the year marks more than double the next highest year of silver ETP gains (2009 with 137mn ounces added). There was strong buying when silver was under-priced relative to gold in the first half of 2020. However, that buying slowed in the second half of the year as silver prices caught up with gold.

Framework

In “Gold and silver: similar, but different”, we argued that silver’s price performance is 80% correlated with gold. In our modelling framework, gold price is therefore the main driver of silver price. However, we also find the following variables as important drivers of silver price:

- Growth in manufacturing activity – more than 50% of silver’s use is in industrial applications (in contrast to gold where less than 10% comes from that sector). We use global manufacturing Purchasing Managers Index (PMI) as a proxy for industrial demand

- Growth in silver inventory – rising inventories signal greater availability of the metal and hence is price negative. We use futures market exchange inventory as a proxy

- Growth in mining capital investment (capex) – the more mines invest, the more potential supply we will see in the future. Thus, we take an 18-month lag on this variable. Given that most silver comes as a by-product of mining for other metals, we look at mining capex across the top 100 miners (not just monoline silver miners).

Gold outlook Q4 2021: at the crossroads of hope and fear

In Gold outlook to Q4 2021: at the crossroads of hope and fear we laid out our forecasts under three scenarios.

- Consensus – based on consensus forecasts for all the macroeconomic inputs and an assumption that investor sentiment towards gold remains flat at where it is today.

- Continued economic uncertainty – further monetary intervention, possibly through yield curve control – limits Treasury yields and the US dollar continues to weaken, while investor sentiment towards gold strengthens.

- Hawkish Fed – despite having adjusted its inflation target, the Federal Reserve (Fed) behaves hawkish and Treasury yields rise substantially, the US dollar appreciates back to where it was in June 2020 and inflation remains way below target. As US dollar debasement fears recede, positioning in gold futures declines.

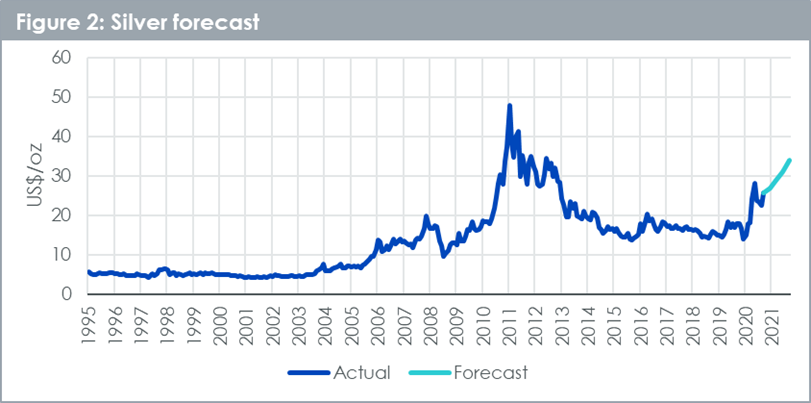

In our silver forecast, we focus on the ‘Continued economic uncertainty scenario’ where the gold price reaches US$2130/oz at the end of the forecast horizon.

Silver forecasts

“We believe in growth terms, silver could outpace gold, reaching US$34/oz in Q4 2021 (33.6% from today’s levels, versus 13.3% for gold. We explain the other drivers to this forecast below.

Industrial demand to continue to recover

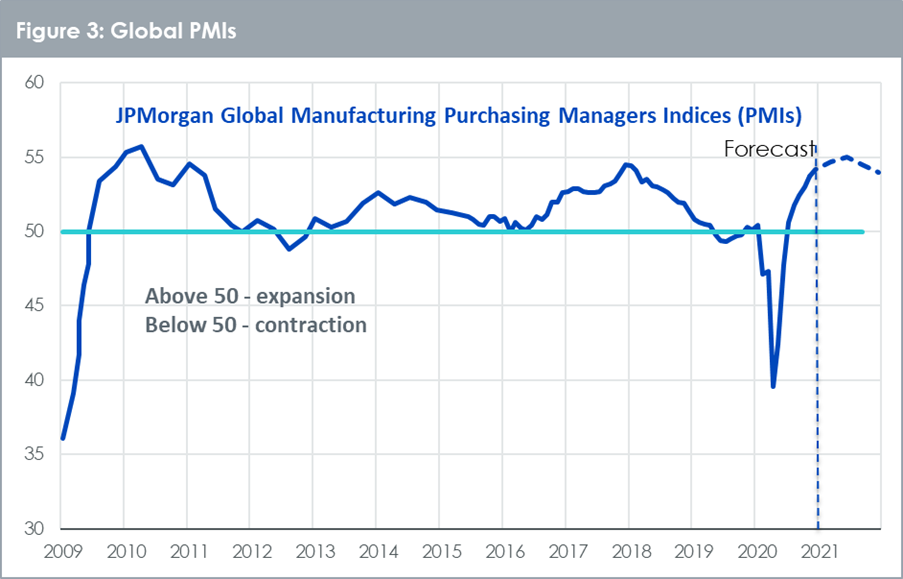

“Manufacturing Purchasing Managers Indices (PMIs) have risen strongly in the past few months and are now in the expansionary post-50 region (Figure 3). Coming from a period of tight lockdowns, it’s unsurprising that the relative recovery from spring 2020 levels for the PMIs was strong as lockdown conditions eased. Renewed lockdowns could temporarily halt the improvement, but in general many businesses – with the support of a monetary and fiscal stimulus – will continue to see improvement. As with most historic recoveries, the pace of rebound is likely to slow in in the second half of the year. However, peaking at over 55, the PMIs indicate plenty of industrial demand for silver to be expected.

Mining supply could expand in 2021

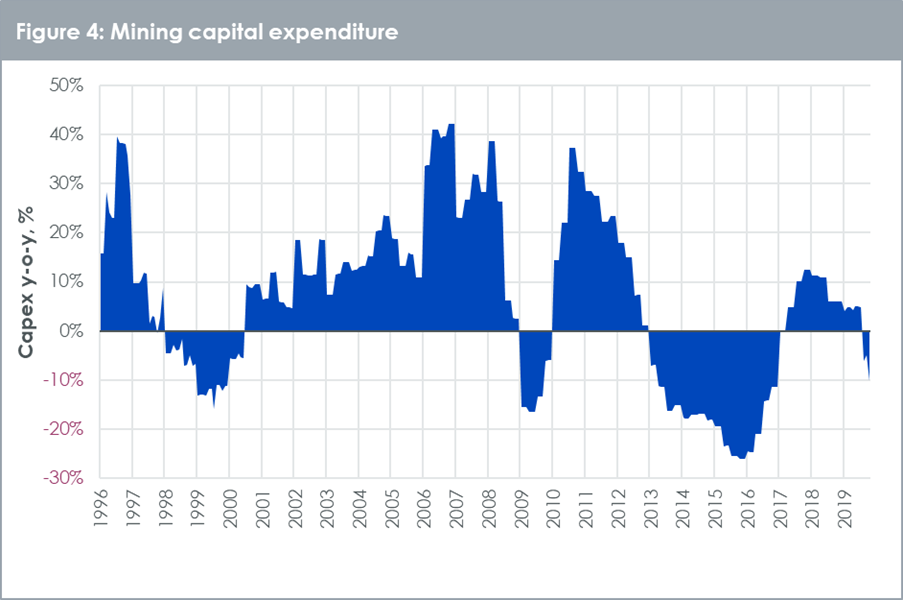

“Our model approach uses the capital expenditure in mines as a proxy for future silver supply. While capital expenditure has declined in the past quarter (Figure 4), given the lag that we apply to this input, the rising capital expenditure we saw before that acts as a headwind for silver prices in our model approach.

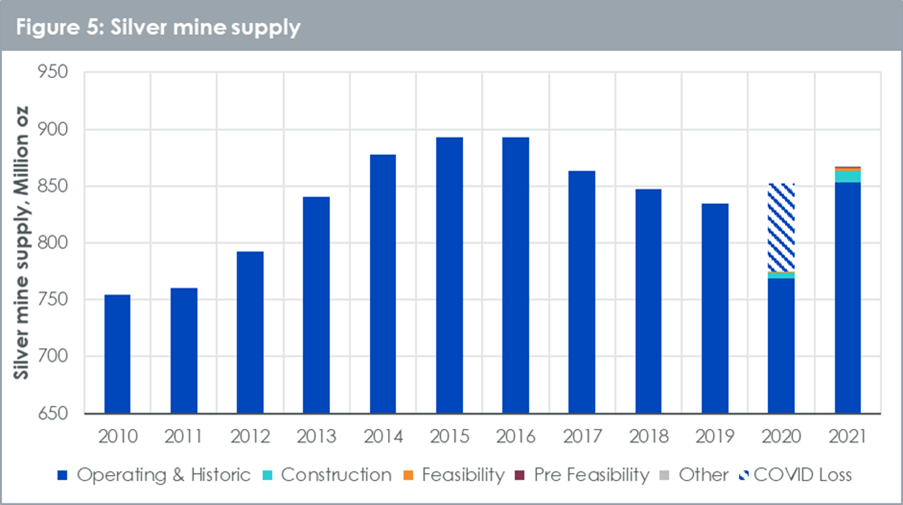

“We know that earlier in 2020 many mines were unable to operate at full capacity due to social distancing and therefore silver mine production has been lower than it would have otherwise been. Figure 5 shows how much these COVID-19 related losses were estimated to be by Metals Focus. Assuming we don’t see lockdowns reintroduced in 2021, we are very likely to see mine production of silver rebound.

Silver exchange inventory rising again

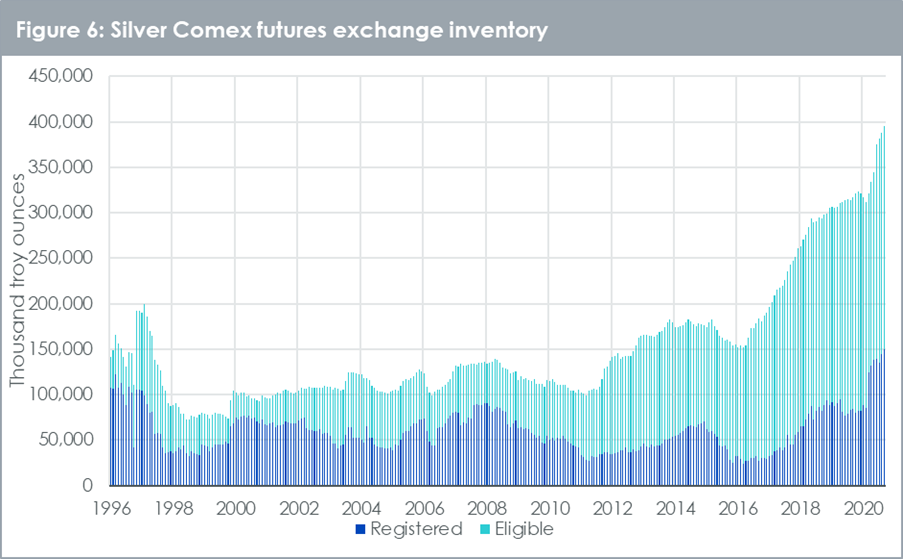

“Silver inventory in Comex warehouses took a dip earlier in 2020 as sourcing metal became difficult under COVID-19 related operational hurdles (including flying metal from refiners in Europe, which became very difficult during lockdown). However, the supply of silver at the futures exchange was always plentiful and did not experience as sharp a dislocation from the over-the-counter spot bullion market as gold did. In recent months silver inventory on exchange has resumed its upward trajectory (Figure 6). We expect this trend to continue, adding some headwinds to silver price.

“We should note that there is a distinction between registered and eligible inventory. Eligible means the metal meets exchange’s requirements but has not been pledged as collateral against a futures market transaction. Registered means the metal meets requirements and has been pledged as collateral for futures market transactions. Eligible can easily be converted into registered, and that is why we look at the aggregate. However, most of the gains in recent years have come in the form of eligible rather than registered. That could simply be the choice of warehousing more in Comex warehouses rather than other warehouses. Nevertheless, the greater source of visible inventory has had a price dampening impact on silver. We expect rising inventory to continue to have this effect in the future.

Silver is not as cheap as it was in 2020

“After spiking to a modern-era high in Q1 2020, the gold-to-silver ratio is now sitting only slightly above its historic average since 1990 (Figure 7). In this regard silver is not as ‘cheap’ as it was in Q1 2020. We still expect silver outperformance over gold this year however, and our current forecasts (under the ‘continued economic uncertainty’ scenario) would put the gold-to-silver ratio at 63 at the end of 2021, just below the historic average of 68.

Conclusion

“Although silver faces some headwinds from potential supply increases, its correlation to gold should act as strong tailwind. Moreover, its hybrid status will allow it to benefit from a cyclical upswing, as we pass the ‘bumps in the road’ in combating the COVID-19 pandemic. Silver has outperformed gold in 2020 and its historic high gold-beta may continue to see it outperform gold when gold is rising.”

Nitesh Shah, Director, Research, WisdomTree