Nyheter

What’s behind the shrinking difference in crude oil prices?

However, the narrowing is also due to the WTI price. Against the general trend of falling commodity prices, WTI has risen by 2% since the beginning of the year. This is remarkable given that US crude oil stocks rose to an all-time high in May and US oil production reached a 21-year high in the same month. However, newly built transport capacity has made it possible to drain the oversupply in the US Midwest to other parts of the country more quickly. As a result, stockpiles in Cushing – the storage and delivery point for WTI – fell slightly up to the beginning of May.

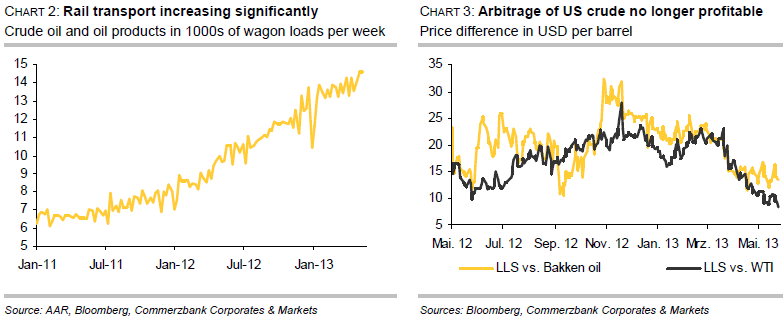

Railway improves the availability of shale oil

The development of rail transport capacity is having an effect. According to the US Railway Association, between the start of the year and mid-May, around 50% more crude oil and oil products were transported by rail than in the same period last year (chart 2). Total goods transport by rail rose by only 1% y-o-y in the same period. The railway makes it possible to transport surplus shale oil from the US Midwest, not only to refineries on the US Gulf Coast, but also to the US East Coast and eastern Canada. The refineries on the US East Coast and in eastern Canada prefer to process light oil. As these refineries gain access to light shale oil from their country’s interior, so their demand for imports from the Atlantic Basin – i.e. from Western Europe or West Africa – diminishes. This in turn puts pressure on the Brent oil price.

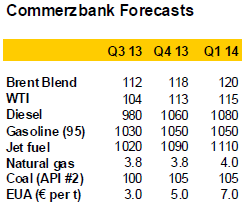

Current price differential barely covers transport costs

Without new US pipeline capacity, continued narrowing of the price differential between Brent and WTI is difficult to justify. The costs of transporting (shale) oil from the US Midwest by rail are more than 12 USD per barrel to the US Gulf Coast and 15 USD per barrel to the US East Coast. Therefore, in view of the current price difference between Light Louisiana Sweet (LLS) as a reference for the US Gulf Coast and shale oil from the Bakken formation, it is barely profitable anymore to transport surplus crude from the Bakken to the US Gulf Coast via rail (chart 3). This applies even more to the transport from Cushing to the US Gulf Coast and from the Bakken to the US East Coast, given the price difference between LLS and WTI and between Brent and Bakken oil, respectively. In recent months, these arbitrage opportunities were a driving factor in the narrowing of the price differential between Brent and WTI. The rise in oil stocks in Cushing since the start of May could already be a sign that arbitrage is declining. We therefore expect that the price differential between Brent and WTI will temporarily widen to 10-12 USD per barrel again in the upcoming weeks.

Commissioning of new pipeline capacity opens up scope for further narrowing

Pipeline capacity is set to rise steadily over the coming months and will provide sufficient relief in the medium-term. A noteworthy example is the reversed Longhorn Pipeline, through which crude oil has been able since mid-April to flow from the Permian Basin in Texas to the Gulf Coast, and no longer as previously to Cushing. During the summer months the capacity of this pipeline will increase by 150,000 barrels per day, which should be enough to balance the increase in oil production in the US Midwest and prevent Cushing stocks from rising. With the expected commissioning of the southern Keystone XL Pipeline in December, capacity will increase by an additional 400,000 barrels per day. Another 100,000 barrels per day will be added as soon as the extended Seaway Pipeline is able to return to full capacity in Q4. The now completed reversal of the Ho-Ho Pipeline plays an important role in this regard. This is able to carry up to 300,000 barrels of oil per day from Houston to Houma in Louisiana. A noticeable decline in Cushing stocks is expected from autumn onwards, which should cause the price differential to shrink to 5 USD per barrel by year-end. Pipeline transport costs are 2-4 USD per barrel. The price differential between Brent and WTI should fall to this level next year.