Analys

US shale oil production growth slowing sharply

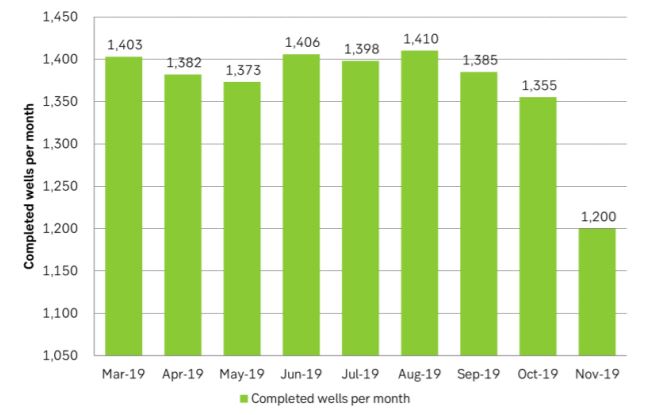

The US EIA yesterday released its monthly drilling and productivity data. It showed that US shale oil production is slowing down even faster than they assumed just one week ago in their monthly STEO oil market outlook. All through 2019 we have seen an ongoing sharp decline in drilling. The slowdown in production growth has however been much more muted as producers have been able to tap a large inventory of drilled but uncompleted wells (DUCs). The well-completion rate has been holding out at around 1350 to 1400 wells per month but now it suddenly fell off a cliff in November.

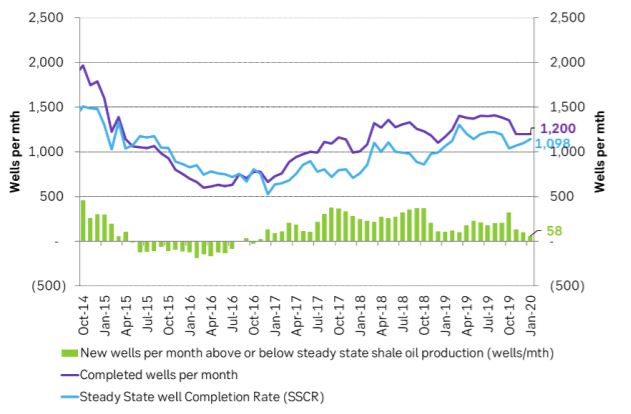

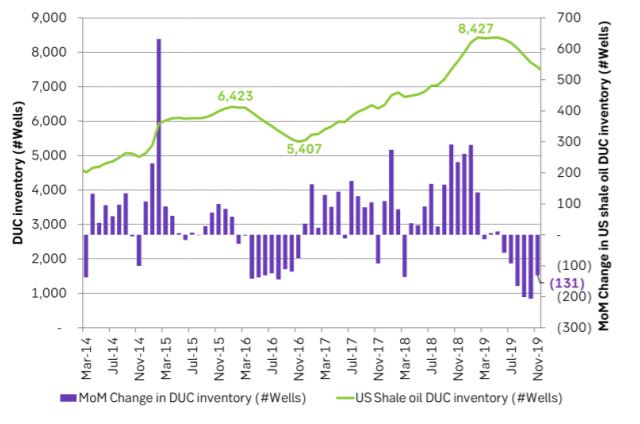

The number of usable wells in the DUC inventory has always been highly uncertain. We had expected the well-completion rate to hold out at around 1350 to 1400 until Feb/Mar next year before producers would be forced to reduce the completion rate in lack of usable wells in the DUC inventory. But now it is happening already in November. This could be noise, or it could be a sign that number of useful wells in the DUC inventory are fewer than expected.

Losses in existing production is still on the rise while new monthly production is in decline as fewer wells are completed. US shale oil production is now projected to grow by only 30 k bl/d in January (360 k bl/d annualized rate) and it is rapidly moving towards zero growth. If the well completion rate falls another 50-100 wells, we’ll have zero production growth in US shale oil production. Last week the US EIA projected that US shale oil production will be in contraction at the end of 2020 but still hold out at a 50 k bl/d production growth rate MoM through the first five months of 2020. Yesterday’s drilling and productivity data is probably indicating that these assumptions are too high, and that production is slowing down even faster than projected just one week ago. Our view is still that the US EIA is estimating drilling productivity at too high a level because the DUC inventory is being drawn down and thus crates an image of high production per drilling rig in operation.

In a nutshell the number of drilled wells went down by 79 wells, completed wells went down by 155, the DUC inventory declined by 131 wells, production growth fell in 5 out of 7 regions with only one region slightly higher and one unchanged. Non-Permian production will decline by 18 k bl/d MoM in January (216 k bl/d annualized decline rate) and total US shale oil production will only grow by 30 k bl/d in January (360 k bl/d annualized rate).

Across the raw material space, the mantra today is “profit, not volume”, so also in shale oil. It is lack of profitability which is driving down the activity in US shale oil production. It is not lack of ability to produce.

Yesterday’s data and reports from the US EIA is truly great reading for OPEC+. It makes the task of controlling the supply/demand balance in the global oil market next year so much easier. Rather than US shale oil flooding into the market at an increasing rate it is now instead rapidly moving towards zero growth. That makes it much more controllable for OPEC+.

The great thing about US shale oil seen in the eyes of OPEC is the sharp underlying decline rate. OPEC can at any time get back its lost market share probably within a year or so. All it needs to do is to let the oil price drop down deep for 6-12 months. US shale oil production would crash, demand would boom on low prices and voila OPEC’s market share would be back to normal.

So, in terms of market share OPEC has nothing to worry about. It can easily and quickly get it back again anytime it wants to. This would not have been the case if the new oil supply in the US had been more like classic oil which typically never goes away before 10 years or more have passed. A lower price would of course be the price to pay for getting back the lost market share. But time of getting it back would be quick.

Ch1: The number of completed shale oil wells in the US fell off a cliff in November. Much sooner than expected.

Ch2: If US shale oil producers reduce the number of completed wells by another 58 wells then US shale oil production will have zero growth in January rather than a projected growth rate of 30 k bl/d MoM as projected by the US EIA yesterday

Ch3: The US EIA is over-estimating the drilling productivity due to the DUC inventory draw

Ch4: The US shale oil DUC inventory is drawing down. We had expected that the draw down rate should accelerate with the DUC inventory then bottoming out at around 5,500 where it bottomed out last time. But the draw down slowed in November. Lack of good wells in the DUC inventory?

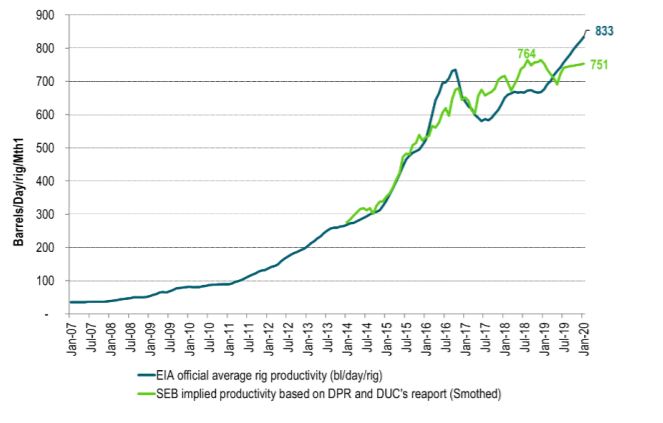

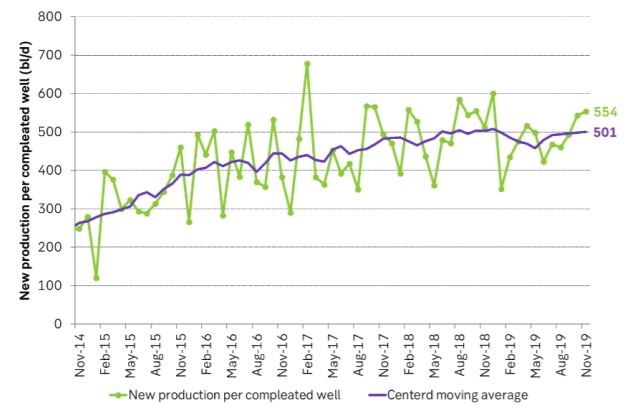

Ch5: SEB well productivity estimate

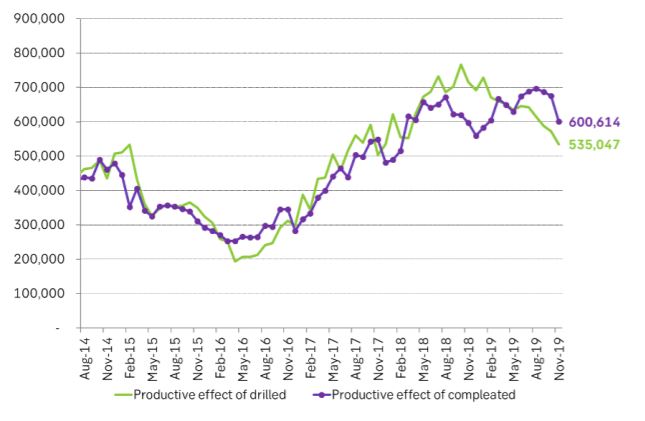

Ch6: The productive value of drilled wells has fallen for a long time as the number of drilled wells per month has declined along with a lower drilling rig count. New in November was that the completion rate also declined sharply. It was bound to happen sooner or later but now it happened sooner.

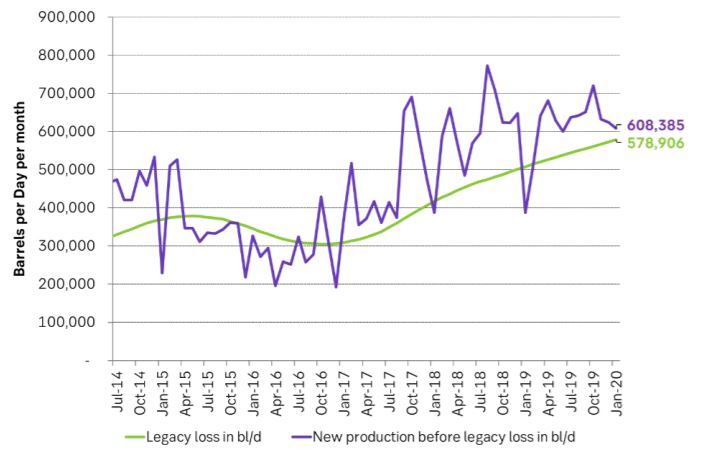

Ch7: Losses in existing production continued to rise while new production is declining. When they meet overall production growth will be zero and then rapidly decline as new production goes below losses in existing production. It’s like breaking off a stick in terms of production. That’s what we saw back in early 2015.

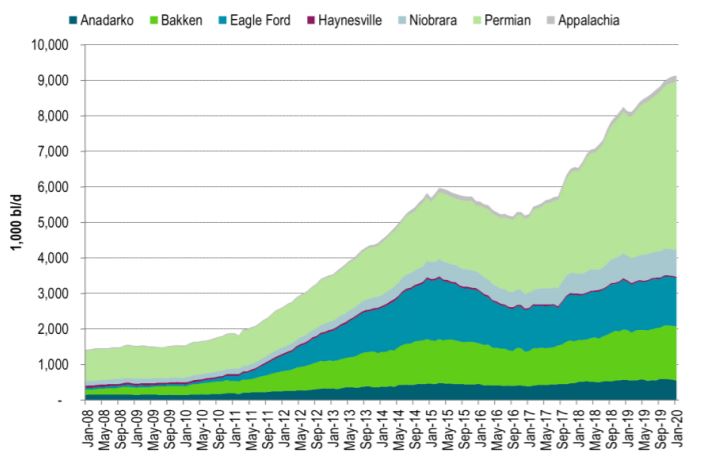

Ch8: US production growth is slowing down. Non-Permian shale oil production is now in decline by a marginal, annualized rate of 216 k bl/d/yr.