Analys

Trump holds the key for commodities

![]()

Starting point is Trump’s politics

Three major President Trump-related developments are having a significant impact on the commodity universe right now. First, the US decision to leave the Iran agreement and impose sanctions in two stages against Tehran laid the ground for a more direct market pricing of any similar actions against other countries.

Second, sanctions were imposed on Russia, and and most recently, US import tariffs on steel and aluminium were doubled on Turkey.

Third, on top of sanctions, developments in the trade war stalled during the summer and the positions of the various sides appeared to become locked.

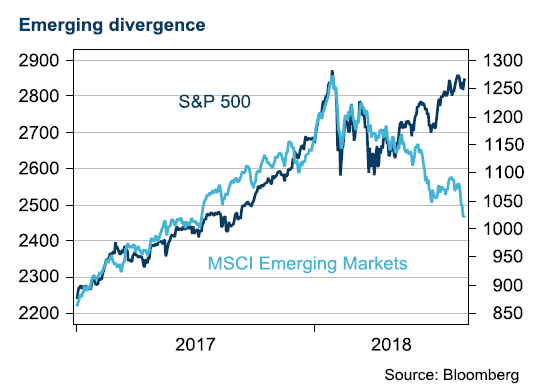

These developments served to illustrate the US approach to emerging markets, in our view, and changed market pricing, kicking off a divergence between the pricing of US assets and those of emerging markets.

Turkey will not spread to Asia

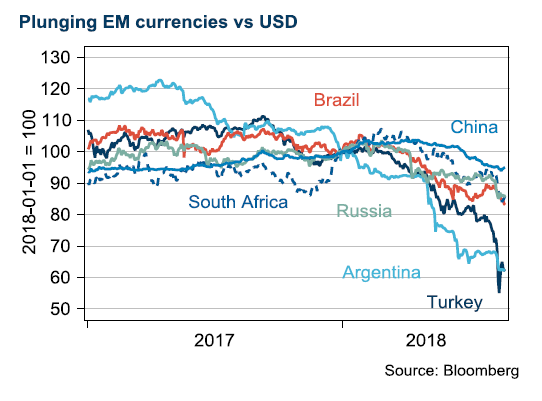

If the Turkish currency crisis is not staved off, the risk of a financial system meltdown and, ultimately, a government debt default is high. But even though Spanish banks are vulnerable, Turkey’s problems should not hurt the overall eurozone economy to a significant degree. Euro weakness and European stock market declines due to the escalation of Turkey’s crisis therefore seem to be overdone. However, Turkey is far from out of the woods yet and the situation might need to worsen still to convince Turkey to adopt a painful, but more sustainable, path toward regaining financial markets’ trust. Other emerging markets with similar challenges, such as South Africa, Argentina and Pakistan, also face tough times ahead.

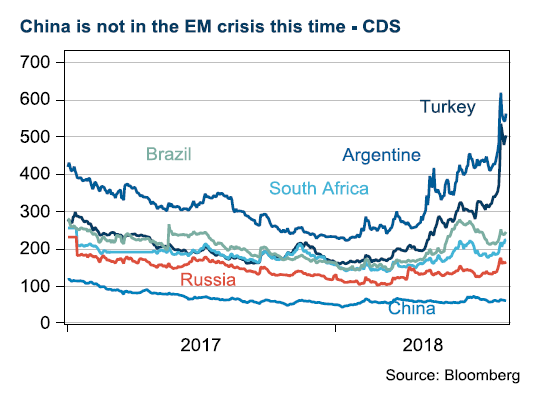

China stands out

What ties the affected emerging market countries together this time is expensive USD financing. China is not among them. This is can be seen clearly by studying developments in the cost of credit default swaps, or CDS.

China has barely moved while Turkey and Argentina have gone through the roof. Among the worst hit are Brazil, South Africa and Russia. These countries have also seen their currencies underperform along with their local equity markets.

Numbers point to a brighter future

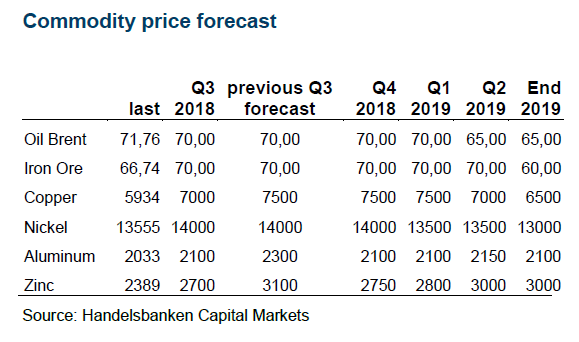

The idea that fear is stronger than greed is relevant here, in our view. We think the first phase of President Trump’s threatening of the emerging markets is over. Running the numbers on the impact of tariffs still points to a bright future. It is hard to prove that tariffs will take a meaningful toll on growth in consumption, we believe. The impact on corporate investment is more difficult to judge. Typically, there are many negative assumptions made ahead of investments decisions. After President Trump’s “flip flop” policies, there is scope for many more multinational companies. Our base case is that President Trump will sign a deal with China in November, in time to influence the midterm elections. In such a scenario, we think base metals would recover, especially copper. Within base metals, it is clear that those more exposed to the Asian construction sector, e.g. copper and zinc, have been the greatest losers, while nickel has done much better, supported by a larger share of demand coming from the US and Europe, posting positive data during the summer.

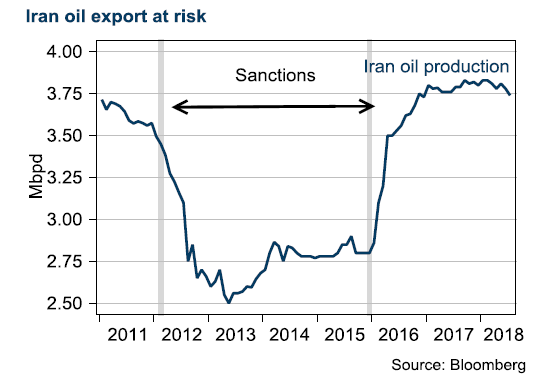

Oil is all about Iran

The first phase of the new US sanctions against Iran came into force in August. Among other things, this means that Iran cannot use USD. However, sanctions on oil exports will not come into effect until November. These sanctions will probably not hit the country as hard as the previous ones, as they do not have the support of the rest of the world.

In the first half of the year, leaders from the EU tried to get the US to remain in the Iran agreement and presented a series of measures to instead put pressure on Iran, including closing down the missile programme. The Trump administration considered the measures to be insufficient, and chose to withdraw from the agreement. Now, the administration has urged Iran to return to the negotiating table to formulate a more comprehensive agreement than the previous one; however, Iran has stated that the US must first revert to the agreement before negotiations can recommence.

In our view, the current sanctions are fully accounted for in the oil price and a certain amount of ‘over-compliance’, such as in the example of Total, is also priced in. However, what has not been included in the oil price, in our view, is the reality of President Trump taking a step further and cutting off Iran from the global economy completely. In that case, for example, China would not be able to import oil from Iran. The latest decrease in the oil price (from around USD 78/barrel in early July to USD 72) can mainly be attributed to the escalating trade war between the US and China, in our view, but this does not mean that the situation with Iran has become any less significant.

Sparkling electricity market