Analys

Shale producers ramp up production as pipes to Gulf opens

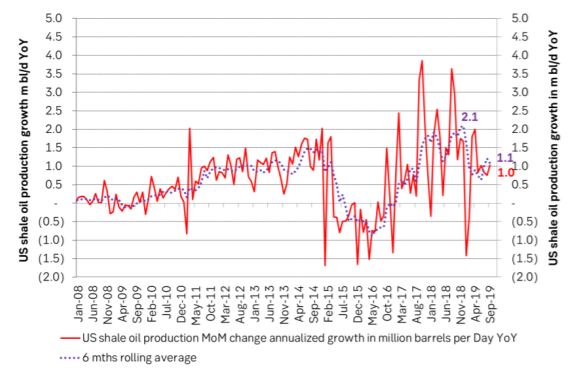

Yesterday’s report on US shale oil drilling from the EIA was mostly depressing reading for global oil producers. It showed that the completion of wells rose to 1411 wells in July (+19 MoM) and the highest nominal level since early 2015. As a result the marginal, annualized US shale oil production growth rate rose to a projected 1.0 m bl/d in September which was up from a growth rate of 0.6 m bl/d.

Shale oil producers drilled fewer wells (down 31 to 1311 wells) which is consistent with the ongoing decline in drilling rigs which have declined by 124 rigs to 764 oil rigs since November last year. With a productivity of about 1.5 drilled wells per drilling rig in operation this means that close to 200 fewer wells are being drilled today.

Instead producers are focusing on completing wells. Drilling less and completing more meant that the number of drilled but uncompleted wells declined by 100 wells to 8,108. The DUC inventory is still 2,850 wells higher than the low point in late 2016. This means that producers can continue to throw out drilling rigs while still maintaining or increasing the number of wells completed per month and thus increase production.

The hope has been that the declining drilling rig count which now has been ongoing for 9 months with investors rioting against producers losing money demanding spending discipline, positive cash flow and profits would now start to materialize into a declining rate of well completions as well. This would naturally lead to softer production growth or even production decline.

In the previous report the estimated marginal, annualized production growth rate was only 0.6 m bl/d. We estimated then that it would only take a reduction in monthly well completions of 109 wells in order to drive US shale oil production to zero growth. I.e. it would not take much to drive growth to zero. Well completions per month would only have to decline from 1383 in June to 1274 and voila US shale oil production growth would have halted to zero. That did not happen. Instead the well completion rose to 1411 in July thus driving estimated the marginal, annualized production growth rate to 1.0 m bl/d in September.

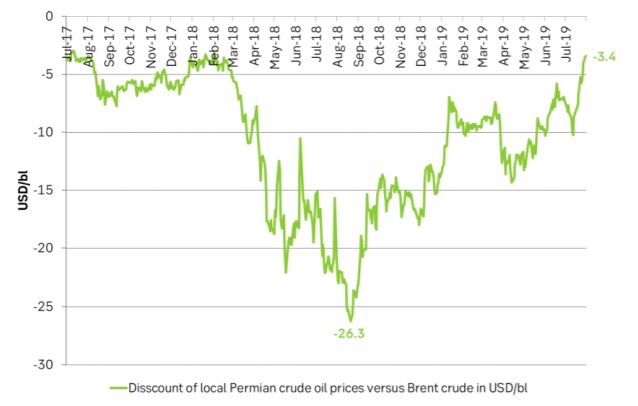

Last year we witnessed that the local, Permian (Midland) crude oil price traded at a discount of as much as $26/bl below the Brent crude oil price as production was locked in both Permian and Cushing. So far this year the discount has mostly been varying between -$15/bl and -$5/bl. The writing on the wall for Permian shale oil producers has been that if they accelerated completions and production they would just kill the local price and the marginal value of production.

Now however transportation capacity out of the Permian is rapidly opening up to the US Gulf. The Cactus II (670 k bl/d) from the Permian to Corpus Christi (US Gulf) opened in early August and much more is coming later this year and early next year. As a result the local Permian crude oil price is now only -$3.4/bl below the Brent crude oil price. And even more important is that Permian producers now know that they can ramp up well completions and production without killing the local crude oil price.

Permian producers are moving from an obvious price setter position locally in the Permian to a perceived global oil price taker. Though in fact they will in the end also be the price setter in the global market place if they just ramp up well completions and production.

Our fear as well as OPEC’s fear and global oil producers fear is that Permian shale oil producers now will focus intensely on well completions. They have 3,999 drilled but uncompleted wells to draw down and they can now accelerate production without the risk of killing the local oil price. Well completions are after all equal to production and production is money in the pocket while drilling in itself is only spending.

There were a few positive elements in yesterday’s numbers seen from the eyes of global oil producers. Increased well completion was basically a Permian thing with completions on average declining elsewhere. Productivity of new wells continued to decline. This is counter to the headline productivity numbers from the US EIA. EIA is calculating drilling rig productivity and not well productivity. In addition they are not adjusting for a build or a draw in the DUC inventory. When the number of DUCs is increasing they under estimate drilling productivity and when the number of DUCs is declining they over estimate drilling productivity. They do not specify well productivity though which is declining in our numbers.

Ch1: The local Permian crude oil price discount to Brent crude has rapidly evaporated as the Cactus II from Permian to Corpus Christi has opened up. Now Permian producers can ramp up well completions without the risk of killing the local oil price.

Ch2: Drilling continued to decline but well completions rose to the highest nominal rate since early 2015. When drilling has declined long enough it is clear that well completions will have to decline as well. With a large DUC inventory we do however seem to be far from that point in time yet. The US DUC inventory stood at 8,108 in July, up 2,850 since late 2016.

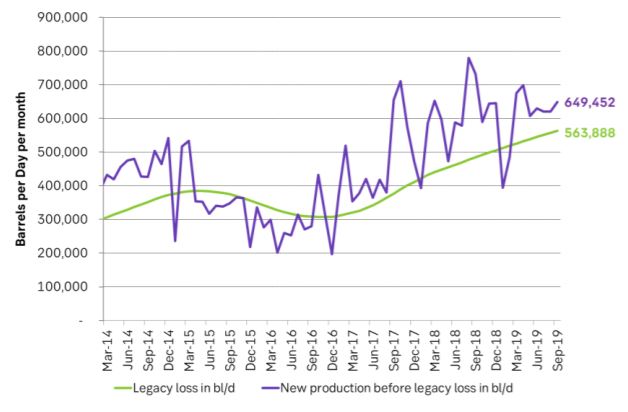

Ch3: This is driving estimated new production in September up and away from losses in existing production. Thus marginal annualized production growth accelerated to 1.0 m bl/d in September.

Ch4: Marginal, annualized shale oil production growth rose to an estimated 1.0 m bl/d per year. Clearly down from the extremely strong production growth last year of up to 2 m bl/d growth rate. But still up versus last months report of a rate of 0.6 m bl/d per year with hopes then that the rate would decline further.

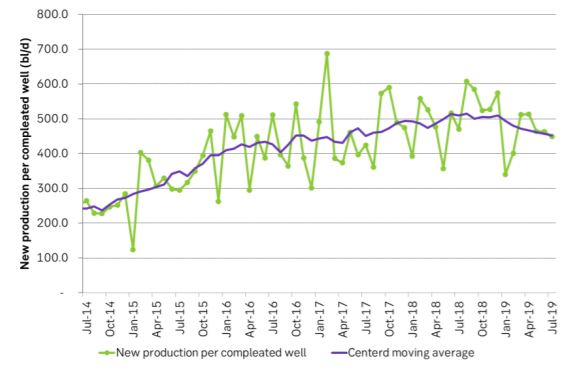

Ch5: Overall well productivity continued to deteriorate with latest 7 data points all below the average of the previous 7 points. This could be a function of the DUC inventory draw down. When the inventory rose producers took every 10th well and put it into the DUC inventory. It is logical that producers threw the 10% least promissing wells into the DUC inventory. This then led to an overestimation of the well productivity. Now that the DUC inventory is drawing down producers will have a 20% share of less performing wells. Thus further DUC inventory draw should lead to further overall well productivity.

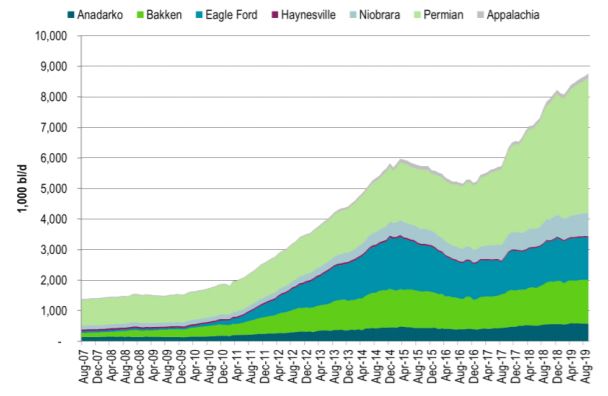

Ch6: US shale oil production growth has slowed. Could it accelerate again now that pipes out of the Permian are opening up?