Analys

Risk hedges in favour on heightened geopolitical risks

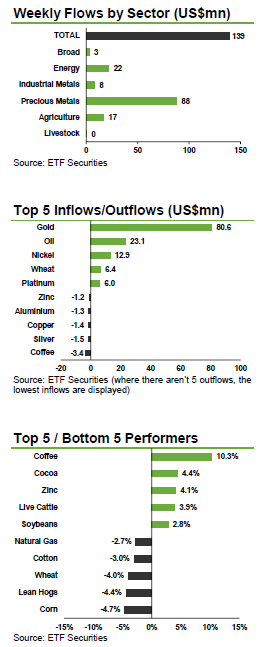

Long platinum ETPs record US$6mn of inflows on relative value prospects. The platinum to palladium ratio is standing at the lowest level since 2002, despite a South African strike that took over 1moz of platinum off the market. While palladium price is better positioned to benefit from a pick-up in global growth, investors deem the current platinum undervaluation excessive and anticipate platinum playing catch up to palladium.

Expectations of a prolonged ore export ban in Indonesia drive inflows into ETFS Nickel (NICK) to an 8-week high of US$12.8mn. Joko Widodo won the Indonesian presidential election and is due to be sworn into office on the 20th October. While his election might bring a relaxation of the export ban in place since January 2014, it is unlikely that any change will be carried out before next year, meaning that nickel market will remain tight for some time. With Indonesian industrial metal supply substantially reduced by the ban we expect industrial metals to continue being supported as global demand begins to pick up. Cyclical commodities demand is being driven by the Chinese government’s stimulus measures and a quickening pace in the US recovery.

Wheat ETPs see US$6.4mn of inflows as the recent price correction is deemed excessive. The Australian Bureau of Meteorology expects below average rainfall in the north-eastern and south-eastern wheat growing areas over the next few months. Investors are building positions in the hope that the large surpluses forecasted by the USDA prove wrong, which could lead to the next price rally. At the same time, profit taking drove US$2.5mn out of ETFS Daily Leveraged Coffee (LCFE), as the Arabica coffee price jumped by over 10% last week. Heavy rains at the tail end of the harvest in Brazil, the biggest producer, could lower the quality of the coffee beans that are currently being harvested.

Key events to watch this week. While investors focus will likely remain on the evolving situation in the Ukraine and the Middle East, a number of key economic statistics for the US and China will also be monitored to gather the strength in momentum in those economies. July Manufacturing PMIs for China, the US and the UK will be coming out this week, together with Q2 US GDP growth and July non-farm payrolls. The US FOMC rate decision will also be watched closely as investors try to identify the future path for rates in the US.

[box]Denna analys är producerad av ETF Securities och publiceras med tillstånd på Råvarumarknaden.se.[/box]

This communication has been provided by ETF Securities (UK) Limited (“ETFS UK”) which is authorised and regulated by the United Kingdom Financial Conduct Authority (the “FCA”).

This communication is only targeted at qualified or professional investors.

The products discussed in this communication are issued by ETFS Commodity Securities Limited (“CSL”), ETFS Hedged Commodity Securities Limited (“HCSL”), ETFS Hedged Metal Securities Limited (“HMSL”), Swiss Commodity Securities Limited (“SCSL”), ETFS Foreign Exchange Limited (“FXL”), ETFS Industrial Metal Securities Limited (“IML”), ETFS Metal Securities Limited (“MSL”), ETFS Oil Securities Limited (“OSL”), Gold Bullion Securities Limited (“GBS” and, together with CSL, HCSL, HMSL, SCSL, FXL, IML, MSL and OSL, the “Issuers”) and ETFX Fund Company plc (the “Company”). Each Issuer (apart from SCSL) is regulated by the Jersey Financial Services Commission. The Company is an open-ended investment company with variable capital having segregated liability between its sub-funds (each a “Fund”) and is organised under the laws of Ireland. The Company is regulated, and has been authorised as a UCITS by the Central Bank of Ireland (the “Financial Regulator”) pursuant to the European Communities (Undertaking for Collective Investment in Transferable Securities) Regulations, 2003 (as amended).