Analys

Oil hurt by trade war concerns but fundamentals are bullish

Bjarne Schieldrop, Chief analyst commodities

There are thus a lot of good reasons to be bullish oil but they are currently all being Trumped by the China – US trade war concerns at the moment. Declining German imports and exports in February out this morning highlights the fact that Europe’s largest economy has hit a soft-patch. The inversion of the one-month US overnight indexed swap rate is also a bad signal from the interest rate market.

Markets are rebounding this morning with the S&P 500 futures gaining 0.6% after Friday’s 1.4% sell-off. Brent crude is also rebounding 0.5% to $67.4/bl following Friday’s 1.8% sell-off.

The market is currently concerned for the escalating China – US trade war tensions. And with good reason since this will be bad for global growth and oil demand growth further down the road. However, oil market fundamentals are tightening and oil prices looks set to be squeezed higher as long as OPEC+ sticks to its cuts.

Global crude and product stocks now in decline – down 18 m bl last week

Global inventories declined 18 m bl last week with declines across the board (US, EU, Sing, floating). Inventories have been rising during the first part of this year as is normal seasonally and as has been the case over the past three weeks as well. Though gains this year has been much smaller than in previous years. Last year inventories rose 112 m bl from the start of the year to mid-March. This year they only increased 43 m bl to mid-March and are now clearly in decline. As long as OPEC+ sticks to its cuts we expect inventories to decline here onwards thus leading to a renewed tightening of the crude oil spot market.

Very strong oil demand growth

Though there are clouds on the economic horizon the latest data on oil demand growth is super strong. News out this morning from the Chinese National Development and Reform commission states that Chinese oil product consumption raises 6.4% y/y for January and February. India’s oil product demand is up close to 9% y/y in February on the back of strong growth in transportation. Also the US is experiencing exceptionally strong oil demand growth due to economic growth and cold winter weather. US Oil product demand grew 6% y/y in February. In comparison the IEA this year expects Chinese oil demand to grow at a much lower pace of 3.4% and India to grow by 6.4%. At the start of the year global oil demand growth looks like it is growing at a pace of around 2.5% y/y. That is at the very high end of oil demand growth projections for 2018. It is higher than our current 1.8% 2018 projection and way higher than IEA’s 1.5% growth projection.

Risks on supply – Venezuela, Iran, Libya and US shale oil pipeline bottlenecks

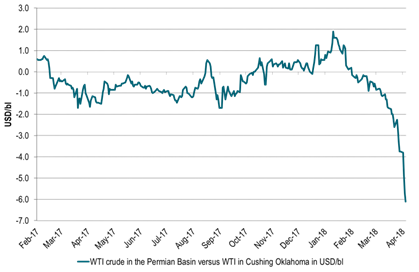

Oil production in Venezuela continued its steep decline in March as it declined from 1.55 to 1.51 m bl/d. That is down 450 k bl/d y/y and the monthly annualized decline rate in March was close to the same at 480 k bl/d. PdV in Venezuela will likely have to close three out of its four refineries due to lack of crude, workers and spare parts. The recent appointment of John Bolton as US national security advisor and Mike Pompeo as US secretary of state makes it highly likely in our view that Donald Trump will revive sanctions towards Iran when it is time to waive the sanctions again on May 12. How much Iranian supply we might loose on this is hard to say but it is at least not positive for Iranian exports and will likely drive Iranian oil exports more strongly towards China and the new renminbi INE oil contract. Libya’s oil exports slipped back in March on the back of disruptions in the southwestern oil filed El Feel. The political situation seems to be deteriorating at the moment with dire political projections for the country. Permian WTI crude prices are trading at deep price discounts versus the US Gulf as oil production is growing much faster than pipeline construction. This is likely to hold back oil flows to market.

Ch1: Weekly oil inventories declined by 18 m bl last week.

Now seems clear they peaked mid-March with decline here onwards

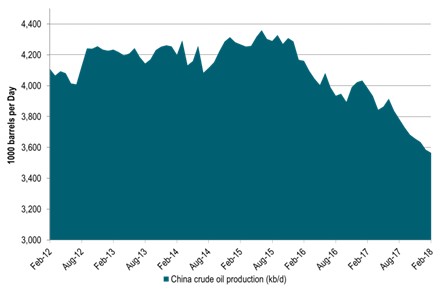

Ch2: Chinese crude production continued lower in February

Ch3: Crude production in Venezuela drops like a rock

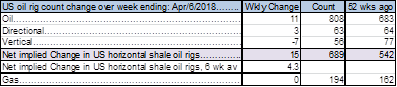

US oil rig count increased by 11 rigs last week to 808

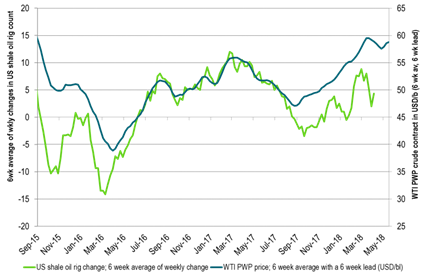

Ch4: US oil rig count keeps rising along with prices

Ch5: Permian price discount deepens as production hits pipe capacity

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking