Analys

Hitting $70/bl – Are there any buyers left?

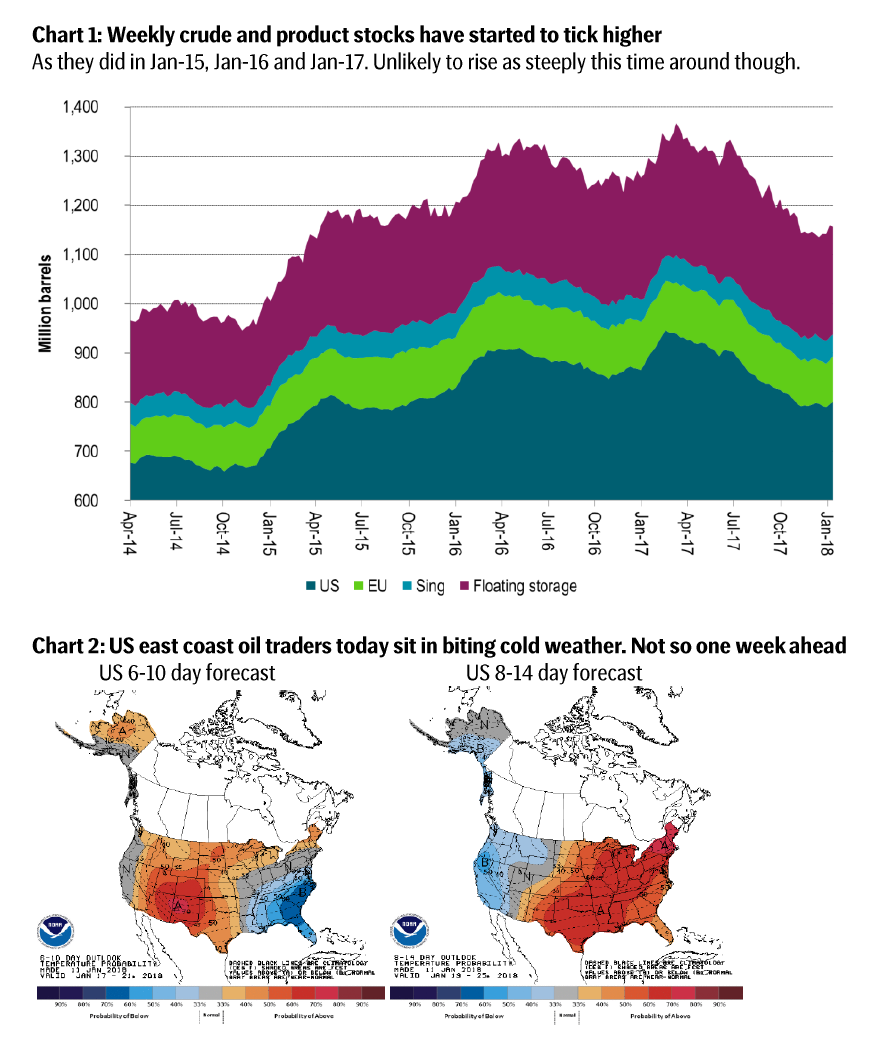

We have had an almost uninterrupted crude oil price rally since June 21st last year supported by declining inventories, declining USD Index, rising global PMIs, disruptions of important oil pipelines, renewed promises by OPEC & Co, no uptick in US oil rig count, increasing risk for renewed sanctions towards Iran and lastly biting cold US weather.

This relentless bull-rally has attracted more and more speculative money into the front end of the crude oil curve while producers have utilized the opportunity to sell further out.

This has led to an increasing steepening backwardation of the Brent crude oil curve. This has attracted yet more speculative money into oil because of the increasing positive roll-yield. Investors are now hand a marginal annualized return of 8% even if Brent spot only goes sideways. Backwardation and rising speculative positions typically feed on it selves.

Today the net long speculative position in Brent and WTI crude is record high in contract and at or very close to record positioning in dollar terms at close to $80bn.

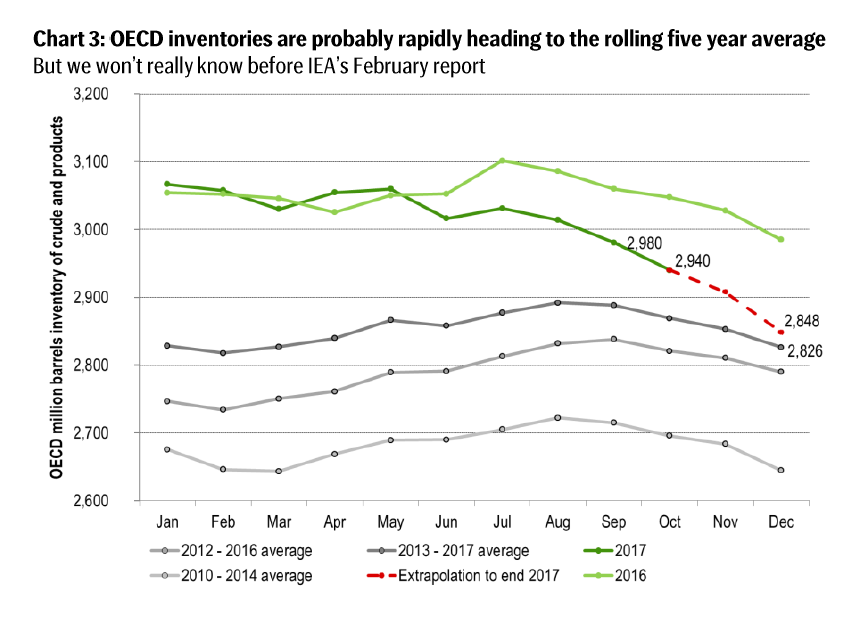

While US east coast oil traders today are shrouded in bitter cold weather they will in 10 days’ time be sitting in above normal temperatures again.

Next week we’ll have the US EIA drilling productivity report (Jan 16) which we expect will show that US shale oil production will grow by close to 100 k bl/d/mth from Jan to Feb which is equal to a marginal annualized production growth rate of 1.2 m bl/d. Thus US shale oil production is growing strongly due to a high and increasing completion of wells.

Later in the week on Fri 19th we’ll have the IEA report which is likely to show that the OECD inventories are getting increasingly closer to the rolling 5-year average. OPEC & Co has promised the market to bring inventories down to the 5-year average but has not explicitly stated which 5-year normal. The market expects cuts to be maintained to the end of 2018. However, if the target is reached then OPEC & Co could gradually increase production.

Do remember Iran’s oil minister earlier in the week stating that OPEC does not want Brent above $60/bl since they fear it will stimulate US shale oil production too much. Well, next week we are likely going to see evidence of continued strongly growing US shale oil production and OECD inventories getting rapidly closer to the rolling 5-year average.

Bjarne Schieldrop

Chief Commodity Analyst

SEB