Analys

Defensive Assets: Gold, a precious ally in the fight against equity drawdown

In the previous instalments of this blog series, we highlighted the defensive behaviour of quality and high dividend equities, long duration government bonds and safe haven currencies as an asset, as well as an overlay to other asset classes. The last few weeks really put investors’ portfolio to the test and the least we can say is that those defensive assets did very well. While Global Equities (MSCI World net TR) lost 17.91% from the most recent tops on 12th February up to 9th March, Long Duration Treasuries (proxied by the Bloomberg Barclays US Treasury 10+) have return an incredible +21.99%. In the same period, Japanese Yen was up 7.54% versus the US Dollar and Quality stocks (proxied by the WisdomTree Global Quality Dividend Growth net TR) did cushion the fall, losing 15.73% and therefore outperforming the market by 2.27%1.

This week, our journey takes us to a fourth asset class, Commodities. Using our defensive framework, we will assess how single commodities or commodity sectors react to equity downturn. In particular, we will highlight how:

- precious metals such as Gold can bring potential diversification and defensiveness to a portfolio as well as act as inflation hedge on the upside. Gold was up 6.96% from 12th February to 9th March 2020;

- Broad commodities could act as a diversifier in a multi asset portfolio.

In the following, we analyse traditional Commodity benchmarks that use front month futures to invest in the different commodities in the universe (being commodities in general or sectors). The only exception are precious metals, were physical investments are considered (physical bullions in vaults for Gold for example). Enhanced commodities are meant to represent “smart beta” in commodities where the strategy can invest further along the curve (i.e. not always in the front month future) to improve the roll yield available to the investor while delivering similar spot and collateral returns. More information on this topic is available on our website. Those strategies have historically delivered strong outperformance over time while keeping the correlation with the benchmark very high.

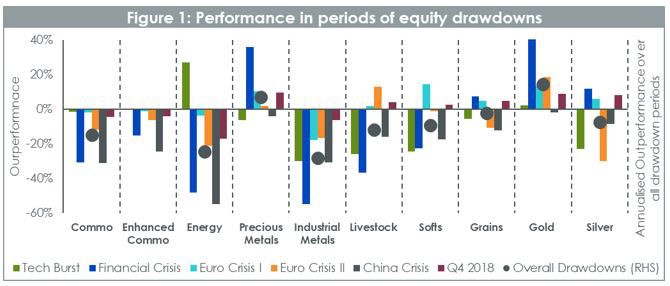

Precious Metals stands out in Commodities

Our framework focuses on 4 characteristics, risk reduction, asymmetry of returns, diversification and valuation. Starting with drawdown protection in Figure 1, it is pretty clear that broad commodities and most commodities sectors are cyclical in nature. Enhanced Commodities fare better than traditional benchmark overall, but the standout defensive asset is precious metals and in particular Gold. In 5 out of the 6 drawdown periods, Gold performed positively, delivering 14.4% per year on average. To put this result in perspective, over those 6 periods, European equities have delivered -35.2%, Min Volatility equities -17.8%, Cash +2.8%, EUR Treasury AAA 8.4% and USD Treasury 11.3%2.

It is worth noting, however, that Energy can also deliver some downside protection when the equity downturn is the result of external shocks such as geopolitical uncertainties. In such, cases Energy and Oil, in particular, tend to react on the upside providing some protection aligned with Gold.

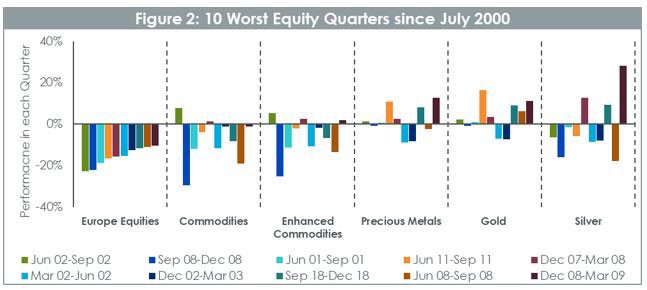

Looking further at the performance of Precious Metals in periods of drawdown we observe in figure 2 that over the 10 worst quarters for European equities in the last 20 years, Gold has 7 quarters of positive performance – a rate of 70%. On average gold outperformed equities by 19% in those quarters. Silver provides results that are more mixed despite outperforming equities by 14% on average. While over the full period commodities didn’t provide a positive return, in 8 of the 10 periods they outperformed equity markets by 8% on average proving that they are still a powerful diversifier. Enhanced Commodities fared even better outperforming equities by 9.6% on average per quarter.

Commodities a chief diversifier

In fact, the rolling 3Y correlation between commodities and equities remains consistently below 50% with long periods where it is nil or even negative. From a pure portfolio construction point of view, this is very exciting as it hands us a diversifying asset that can help reduce the overall volatility of the portfolio.

Gold, a precious tool to build defensive portfolios

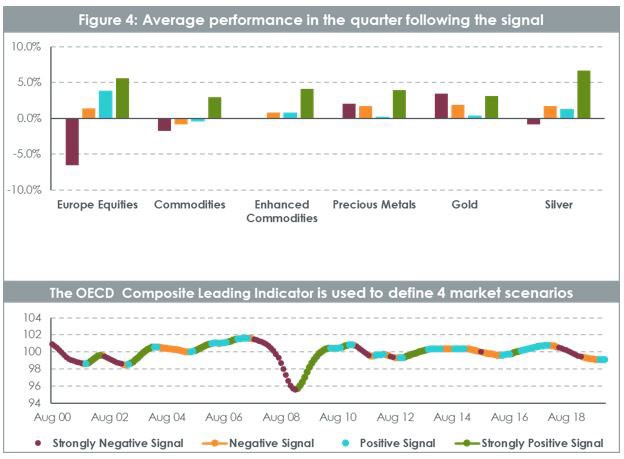

From a more macroeconomic perspective and looking at Commodities performance across business cycles, it is again very clear that Precious Metals offer a protection in economic slowdown or recession. In Figure 3, we have split the last 20 years in 4 types of periods using the Organisation for Economic Co-operation and Development (“OECD”) Composite Leading indicator (“CLI”). The CLI has been designed to decrease a few months before economy start to slow down or increase before the economy restarts. So, a strong decline in CLI tends to indicate a probable downturn in equity markets for example.

Enhanced Commodities behaved very well compared to front month commodities, cutting significantly the downside in negative economic environments and doing better in positive ones. It is worth noting as well the extent to which commodities and enhanced commodities perform when the economic signals are strong. This is linked to the well documented properties of commodities as an inflation hedge. Precious Metals exhibit a very strong and versatile profile driven mainly by gold.

It is interesting to note that Gold has outperformed very strongly in very negative or negative economic scenarios but also has done very well in periods of strong economic rebound, buoyed by its inflation hedge proprieties. This makes Gold a pretty asymmetric asset with strong positive performance in difficult economic periods but also good performance in strong rebound and when yields are expected to increase. Silver, similarly to palladium and platinum, offers also an interesting payoff, behaving part like a precious metal and part like an industrial metal. In periods where the economy is strong, it benefits from being used in the industry and behave more pro cyclically than gold. However, in economic downturn, it benefits from its status as a precious metal and delivers some protection.

This brings us to our fourth pillar in our framework: valuation. WisdomTree issued its quarterly outlook for Gold in January 2020, offering a number of scenarios fo the metal this year. In “Gold: how we value the precious metal”, we explain how we characterise gold’s past behaviour. Unlike other commodities where the balance of physical supply and demand influence the price, gold behaves more like a pseudo currency, driven by more macroeconomic variables like the interest rate environment, inflation, exchange rates and sentiment. Characterising gold’s past behaviour allows us to project where gold could go in the future (assuming it maintains consistent behaviour) using an internal model. In recent weeks, given the sharp rise in volatility of many asset markets and decisive action by a number of central banks across the globe, we are treading a path that looks like the bull case scenario presented our January 2020 outlooks. That scenario would see gold prices head over US$2000/oz by the end of the year. In that scenario, the Federal Reserve of the US embarks on policy easing (which has already started), that drives Treasury yields lower than where they were in December 2019 (Treasury yields have already broken new all-time lows of 0.35% on March 10th 2020). Inflation in that scenario is at an elevated 2.5% (which is in line with the January 2020 actual reading). Lastly, speculative positioning in gold futures markets remains elevated throughout the course of the year (at 350k contracts net long). In February 2020, we saw speculative positioning hit fresh highs (388k) and at the time of writing (10th March 2020), it remains above the 350k. We caution that if the current shock we are experiencing is temporary, we could get the recent interest rate cuts reversed, Treasury yields could rise to 2% and positing in gold futures could head back to more normal levels (closer to 120k). That was what we presented as a base case in January, where gold would end the year at US$1640/oz. So the downside from the levels ate the time of writing is somewhat limited (with gold trading at US$1650/oz at the time of writing) even if we end up in what was the base case.

This concludes our 6 weeks grand tour of the “natural” defensive assets among the main 4 asset classes. Next week we will start focusing on portfolio construction and on different ideas to design defensive and versatile portfolios.

Europe Equities is proxied by the STOXX Europe 600 net total return index. Broad Commodities (Commo) is proxied by the Bloomberg Commodity Total Return Index. Enhanced Commodities is proxied by Optimized Roll Commodity Total Return Index. Energy is proxied by the Bloomberg Energy subindex Total Return Index. Precious Metals is proxied by the Bloomberg Precious Metals subindex Total Return Index. Industrial Metals is proxied by the Bloomberg Industrial Metals subindex Total Return Index. Livestock is proxied by the Bloomberg Livestock subindex Total Return Index. Softs is proxied by the Bloomberg Softs subindex Total Return Index. Grains is proxied by the Bloomberg Grains subindex Total Return Index. Gold is proxied by the LBMA Gold Price PM Index. Silver is proxied by the LBMA Silver Price index.

By: Pierre Debru, Director, Research

Source

1 WisdomTree, Bloomberg. In EUR.

2 WisdomTree, Bloomberg. In EUR. Europe Equities is proxied by the STOXX Europe 600 net total return index. Min Vol is proxied by MSCI World Min Volatility net total return index. Cash Euro is proxied by a series of daily compounded Eonia. EUR Treasury AAA is proxied by the Bloomberg Barclays EUR Aggregate Treasury AAA total return index. USD Treasury is proxied by the Bloomberg Barclays USD Treasury total return index.