Nyheter

David Hargreaves on Precious Metals, week 8 2014

The World Gold Council Speaks. The WGC has delivered its definitive analysis on 2013, an indicative year for the metal. Now, whilst demand patterns matter, price rules. It fell heavily even as mined supply nudged up, real demand was down but over the counter transactions (OTC) burgeoned. Since year end we have seen a significant price bounce (like 10% in less than 8 weeks), so where to now? Major events were:

Demand. India, the long time biggest consumer, was reined in by its government on balance of payment fears, but was replaced by the apparently insatiable Chinese appetite.

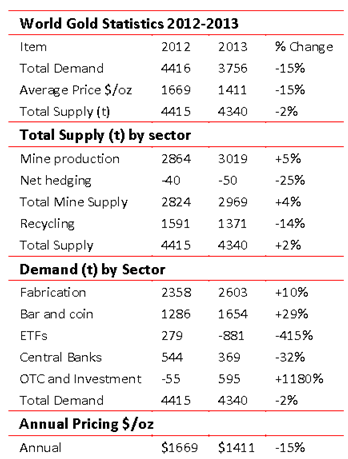

Mine supply was marginally up (+5.4%) and as ever, recycled gold made up the supply-demand shortfall. We speak of c.4400t total demand, an immediate deficit of c.1500t and a calculated surface stockpile of c.150,000t. So we could carry on at this rate for 100 years.

Then the imponderables. Increasingly, they drive the nearby market. We have exchange traded funds (ETFs) which do physical and can buy or sell on a whim plus OTCs plus stock flows. Together, it all presented this picture:

What do the numbers tell us?

Newly mined supply is relatively steady at c.2800-3000tpy although it may retreat in 2014 as the price sags and major companies cut expenditure.

Total demand shows some discrepancies across the WGC tables. We have used that showing it balancing supply at 4340t. As such it shows a full 50% increase, low to high, in the period since 2004 (10 years). Thu table 13: Demand 20014=3046t, 2011=4589t. Given relatively steady new supply levels, the difference is made up by recycling, which is price driven. Given that in the 2004-13 period, the price has moved from $325 to $1700/oz, this is some driver.

Demand by sector shows major shifts

Bar and coin investment increased 29%. These are small, portable collaterals which appeal in times of uncertainty.

Exchange Traded Funds (ETFs), the recent phenomenon saw a mass exodus as the price fell. They look set to become a major influence in nearby supply and demand.

Central Bank transactions are becoming a tinkering exercise, bar for China, where there is an increasing curiousity, bordering on concern, that the true holdings are far in excess of the stated 1054t. Our close correspondents subscribed to this. Unlike India, no gold escapes from China. No jewellery of note, no hallmarked bars. So where does over 1000 per year go to?

Over the Counter (OTC) and investment. By its own admission, WGC tells us this is a grey area, almost a balancer. In the period 2012-13, it was meaningful, swinging from -55 to +595t or 14% of total demand. This, in a falling market.

Conclusions? Mine supply will not leap skywards, it might even fall as the major producers cut back. There is sufficient recyclable gold in the system to satisfy projected demand. It will become available on either a rising or falling price basis. The West has fallen out of love with the metal, but has been replaced by China. India is at a crossroads.

WIM still sees $1200 or lower, but the major miners taking at least another year to regroup before returning to an aggressive stance.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.