Nyheter

David Hargreaves on Precious Metals week 37 2013

Mining Journal held its Gold and Precious Metals Seminar in London September 6th, its second of the year. A panel of precious metal gurus concurred on the long-term shifts in attitudes towards the precious, particularly gold. The geographical emphasis switches from West to East. China and India now account for over a half of the purchases of the metal. Importantly these transactions put it into ‘safe’ long term hands. An intriguing question left hanging was whether the government of China will make a move towards increasing its relatively small holdings as a preliminary step towards breaking its link with the US dollar. A full report of the seminar, written by David Hargreaves, who chaired the meeting, will appear in next week’s Mining Journal.

Evidence, perhaps, of the East-West shift is that the demand for US gold coins fell to a six year low, down 77% in August to just 11,500oz, from 39,000oz in like 2012 and 55,500 in July. The sales of silver eagle coins also dropped 17.75% to 3.6 million ounces. Gold Eagle sales ran at 100,000 per month in the first seven months of 2013. Much, say those who claim to know, rests on will the US or will it not, intervene in Syria. More in Countries. But no stopping China. Despite being the largest miner of gold it is now eclipsing India as the major importer. Customs reports show an intake of 493 tonnes in H1 (2012, H1 = 239t). Total domestic consumption for H1 was reported 706t, a jump of 54%. Annualised, this is over a half of world newly mined supply. Total demand, which amounts to c 4000t worldwide, is made up of c. 2800t new and 1200t recycled. Much of the latter arises in the West.

WIM says: This is a fluid situation. There is a direct contrast between the Chinese government clearly encouraging gold holding by its citizens but India, for balance-of-payments reasons, actively discouraging it.

Where Will Lie the Balance in Supply and Demand? When the price of gold was fixed at $35/oz in 1934, most trade transactions had the backing of the metal. For that to happen again the price would now have to be c. $10,000/oz.

The prospect is encouraging new production despite the travails of major mines such as Barrick, Newmont and Anglo. Australia’s mines upped their output 6% in Q4 2013 to 67t, making 259t for the year, almost 10% of total mined. Star performers included Evolution, St. Barbara and Newcrest.

India’s balance of payments problem cannot, unlike gold, be swept under the bed. It is a unique case. The country has long been the major importer but also manufactures jewellery which it exports at added value. Sadly, much of the imported gold goes under and stays under, the bed. India has further problems with imports (see Countries) but is targeting gold, big time. The Reserve Bank (RBC) is tightening the screws like a demented carpenter. It is trying to restrict imports by increasing taxation and regulating flows. Whilst this may have a net effect, it is encouraging illicit dealing, smuggling and like skulduggery. Perversely, it is hurting exports of jewellery. These fell 70% in July because of a shortage of gold. They were $441M compared with $1500M in like 2012.

Gold and Local Currencies. We have not awarded a SOTBO* for some time, but here we go. A well-known and offquoted correspondent on Mineweb says if selected currencies cheapen, the price of gold in these countries will rise.

Have we missed something? He also says it will affect silver. Hadn’t thought of that.

South Africa’s Gold Wage Negotiations, we report on in more detail in Countries. Suffice here to say they are reaching a compromise at c. 8%.

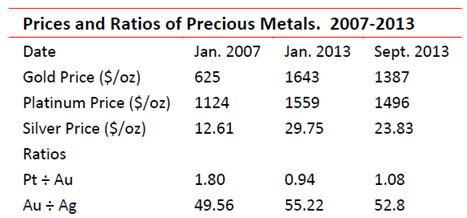

Platinum sees its premium to gold slipping, but it has been there before.

To remind:

Reasons for the swings abound. Platinum and silver have an industrial component; gold does not. The rise in the use of Pt and Pd in autocatalysis created a shortage. This was progressively filled by aggressive expansion in the major producing country, South Africa plus copious supplies from Russia. Silver, despite its supporting remains hostage to the gold price.

WIM says: Given that industrial peace may be returning to RSA, we expect Pt and Ad to slip to discount to gold once more, particularly if the Middle East problems escalate.

*SOTBO: Statement of the Blinding Obvious.

[hr]

About David Hargreaves

David Hargreaves

David Hargreaves is a mining engineer with over forty years of senior experience in the industry. After qualifying in coal mining he worked in the iron ore mines of Quebec and Northwest Ontario before diversifying into other bulk minerals including bauxite. He was Head of Research for stockbrokers James Capel in London from 1974 to 1977 and voted Mining Analyst of the year on three successive occasions.

Since forming his own metals broking and research company in 1977, he has successfully promoted and been a director of several public companies. He currently writes “The Week in Mining”, an incisive review of world mining events, for stockbrokers WH Ireland. David’s research pays particular attention to steel via the iron ore and coal supply industries. He is a Chartered Mining Engineer, Fellow of the Geological Society and the Institute of Mining, Minerals and Materials, and a Member of the Royal Institution. His textbook, “The World Index of Resources and Population” accurately predicted the exponential rise in demand for steel industry products.