Nyheter

Additional cuts is positive for the market and a gift to US/Canada

Additional cuts of 1.2 m bl/d in June from Saudi/Kuwait/UAE yesterday failed to rejoice the oil market and the Brent crude oil price fell 4.3% instead. Today though oil prices are firming a little but the price action (Brent) seems to be centered around the $30/bl mark right now. A depressing thought for OPEC+ must be that side-lined production in the magnitude of 3.5 – 4.5 m bl/d in the US/Canada will be the first to reap the rewards of the production cuts by OPEC+.

The Brent crude July contract yesterday moved to an intraday high of $31.47/bl (+1.6%) on the announcement that Saudi Arabia will cut an additional 1 m bl/d in June with Kuwait and UAE also chipping in additional cuts of about 100 k bl/d each. The joy didn’t last and in the end the contract fell back 4.3% on the day to a close of $29.63/bl along with negative equities and concerns over renewed virus outbreaks.

This morning Brent is inching 1.7% higher to $30.1/bl with the June WTI contract a little bit feistier gaining 2.7% to $24.8/bl. Overall market sentiment is on the negative side with lower equities and metals so oil is mostly going up on its own today. Market is obviously far from certain that the additional cuts announced yesterday will be able to drive the oil price materially higher but is today the conclusion that yes, the additional cuts are naturally positive on the margin.

The announcement yesterday was that Saudi/Kuwait/UAE will together make an additional 1.2 m bl/d cut in June versus already pledge cuts with Saudi cutting 1 m bl/d more to 7.5 m bl/d, Kuwait 0.08 m bl/d to 2.1 m bl/d and UAE 0.1 m bl/d to 2.35 m bl/d. Political pressure from the US, strained state finances in Saudi/Kuwait/UAE and a wish to re-balance the oil market and revive oil prices as quickly as possible lay behind the announcement.

It is very difficult to cut production with good results if you haven’t got a tailwind of strengthening oil demand to help you. The demand part of the equation is still a big uncertainty. Oil demand is now naturally coming back from the abyss in March/April as we get gradual reopening. But these re-openings look like they will be riddled with start/stop issues as virus infections blossom up again. How fast and how far back towards normal demand we can get is today the biggest uncertainty and a key ingredient for OPEC+ success. But demand will of course rebound both back to 100 m bl/d and beyond eventually. The key question now is how much and how fast.

But deepening production cuts now is also tricky for OPEC+. If they are successful in balancing the market, flattening the crude oil price curve and thus drive the front-month crude oil price higher then this will likely very quickly revive the 3.5 – 4.5 m bl/d of side-lined supply in the US & Canada. Thus, all Saudi/Kuwait/UAE will have achieved by cutting an additional 1.2 m bl/d is to let side-lined production in the US & Canada back into the market. Again, without being able to drive the oil price much higher.

This poses a key question: Who shall be first out to put volumes back into the market as demand revives? Side-lined US & Canadian oil wells or OPEC+ production cuts? Right now, it looks like OPEC+ or at least Saudi/Kuwait/UAE are following a strategy where shut-in production outside of OPEC+ are to be placed back in the market first.

Then on to the next step. Will OPEC+ then hold on to production cuts in order to opt for price rather than volume once the oil price moves back to $50/bl thus once again chase the oil price to $60/bl and $70/bl by holding back supply? If so, this would again give preference to shale oil volume rebound in exchange for a higher oil price to OPEC+. Such a next step looks much less likely because Russia made it very clear in March that they are basically done chasing price in exchange for gradual loss of market share to OPEC+ and more market share to US shale oil.

It is hard to conclude otherwise than that the global oil market is gradually mending with rebounding demand on the one hand and cuts to production, lost supply or shut in supply on the other.

But a sense of futility must clearly be felt by Saudi/Kuwait/UAE the moment in time when 3.5 – 4.5 m bl/d of side-lined production in the US/Canada are placed back into the market in response to their deepening production cuts. Because that is likely now what is going to happen as they ”succeed” with their cuts.

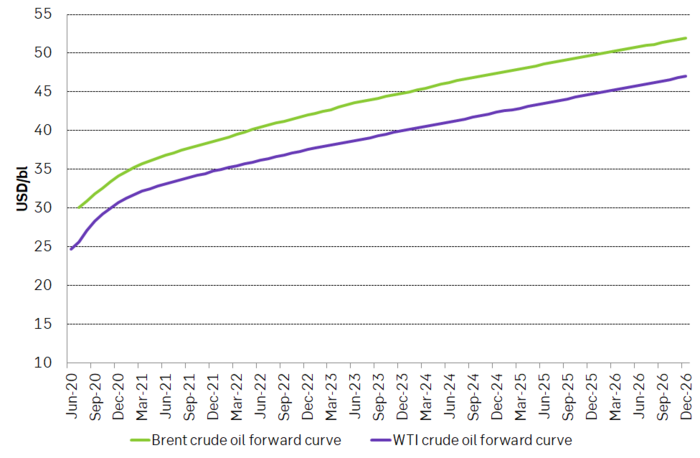

Forward crude oil curves for Brent and WTI. As the oil market starts to balance and inventories starts to draw down the front-end of these curves will move higher and the curves will flatten. This will help to revive side-lined production in the US/Canada in the magnitude of 3.5 – 4.5 m bl/d.