Analys

Will OPEC drop the ball in 2018?

The IEA estimated that the need for OPEC’s oil was 32.1 mb/d in H1-17. This is more or less exactly what Bloomberg statistics tells us that OPEC produced on average year to May 2017. Thus no inventory draws or gains of any magnitude in H1-17.

For the second half of 2017 the IEA calculates that the market will need 33.4 mb/d of oil from OPEC, a full 1.3 mb/d higher than in H1-17 due to seasonal demand effects and refining maintenance seasonality. Maintenance of refineries has been unusually high so far this year. But these are now coming back in operation.

If we assume that OPEC keeps production at current production of 32.2 mb/d through H2-17 (baring potentially further production revival in Libya and Nigeria) then this will drive inventories some 200 mb lower in H2-17. OECD inventories currently have a surplus of some 300 mb above normal. Thus a drawdown of some 200 mb (if taken out of the OECD inventories) would drive inventories a good way towards normality and lead to a flatter crude oil price curve.

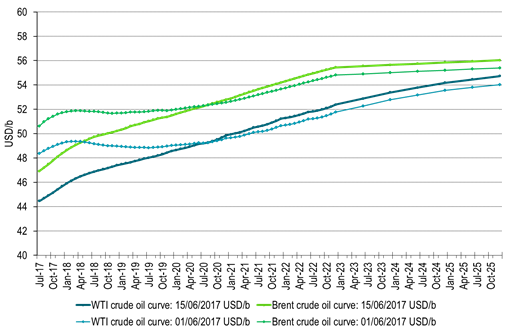

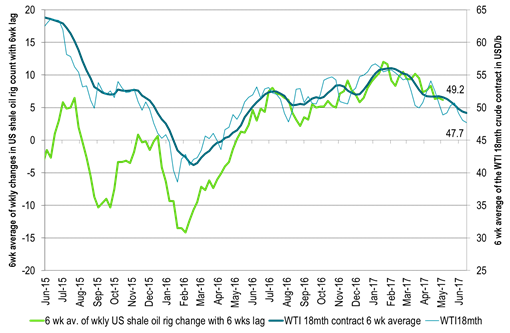

As we have argued many times it is the medium term WTI forward curve which tells the US shale oil players what kind of cash flow they can lock in with a forward hedge if they decide to drill an additional well. The medium term WTI forward curve (proxy 18 mth contract) is the real incentive lever.

Except for a brief flash sell-off in August 2016, the 18 mth forward WTI price has not touched down to $47/b since April 2016. It was when this forward contract broke enduringly above $47/b for more than 6 weeks last spring that the US oil rig count started to rise and has been rising continuously since then.

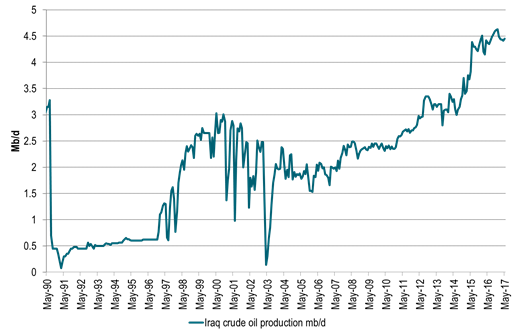

While the IEA implicitly predicts a substantial inventory draw in H2-17 they see a different picture for 2018 where they estimate that the need for OPEC’s oil is no more than 32.6 mb/d. OPEC now produces 32.2 mb/d while it holds back 1.2 mb/d and thus has a natural production of 33.4 mb/d. Thus OPEC will need to hold back at least 0.8 mb/d all through 2018 in order to prevent inventories from rising again. And if Iraq’s production capacity rises to 5 mb/d by the end of 2017 versus current production of 4.45 mb/d or if Libya’s and Nigeria’s production revives even further then OPEC will have to hold back more.

The IEA basically says that inventories will draw substantially in H2-17 due to OPEC cuts. Then however in 2018 OPEC will have to maintain more or less the same size of cuts just in order to prevent inventories from rising again.

Drawdown in inventories is likely to flatten the forward curve in H2-17. Currently there is a $3/b discount for the 1mth contract versus the 18 mth contract WTI crude. By the end of the year the 1mth contract is likely to trade much closer to the 18 mth contract or even above depending of the magnitude of drawdown.

The level of the WTI 18 mth contract which now currently trades at $47.5/b is however the big question. Will it shift higher as well? Usually the whole forward curve shifts higher when inventories draw down and the spot market firms up.

However, IEA is prediction that OPEC needs to cut production all through 2018 as well in order to prevent growing OECD inventories. Thus for every additional shale oil rig being activated through the next 6-12 months means that OPEC will have to hold back even more of its production in 2018.

In our view, while we have a more positive view of the supply/demand balance in 2018 than the IEA, we do not see the need for a single additional shale oil rig to be activated in the US over the next 12 months. In order for this to happen the WTI 18 mth contract needs to stay put at around $47/b over the next 6-12 months. Thus fundamentally, the WTI 18mth contract should not rise above the $47/b level over the next 12 months.

Every additional rig in the US over the next 12 mths is increasing the production-cut burden for OPEC in 2018. It is also increasing the need for the market to believe that OPEC will cut production all through 2018.

The market fear is that the production-cut burden will in the end become too large for OPEC and that it will drop the ball in 2018. Not prolonging the cuts beyond March 2018 and instead opt for volume over price again just as it did in 2014. That is an open question which is itching in the back head of the market.

Ch1: Deeper contango for crude curves

But front end likely to firm in H2-17 as inventories draw down

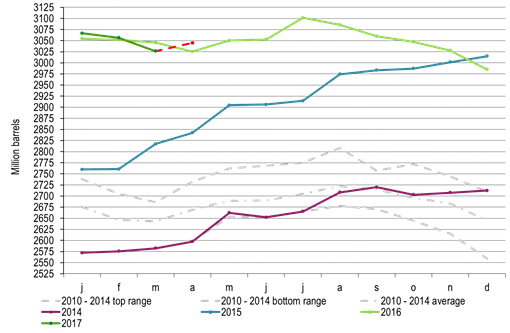

Ch2: OECD inventories increased in April – big dissapointment

Will decline substantially in H2-17

Ch3: Iraq crude production

It says that its production capacity will reach 5 mb/d end of 2017

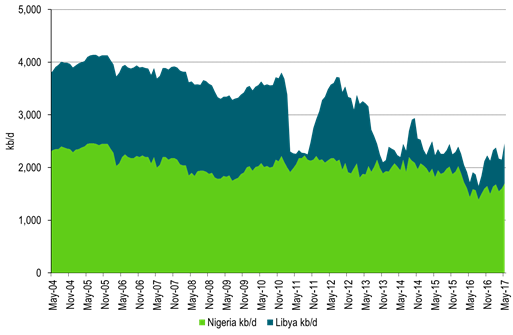

Ch4: Nigeria and Libya crude production reviving

Libya NOC says more to come

Ch5: WTI 18 mth forward crude price heads for the US shale oil “price floor” (or rig versus price inflection point) from one year ago.

Is the inflection point still there or is it higher or lower?

The market is asking US shale oil players to stop adding more rigs.

How low will the price need to move in order to make them listen?

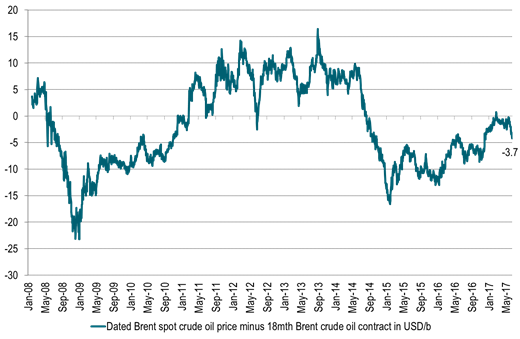

Ch6: Deeper rebate for 1mth to 18 mth Brent lately.

Likely to firm in H2-17

Kind regards

Bjarne Schieldrop

Chief analyst, Commodities

SEB Markets

Merchant Banking