Analys

Venezuela is bullish but S&P 500 still looks like the driver

Donald Trump’s call for a regime shift in Venezuela with his outright support for opposition politician Juan Guaidó has led to a gain in the value of government bonds in Venezuela and thus seen as a positive development by bond investors on a general basis. Impacts on Venezuela’s oil production in the short to medium term is however another matter. To us it looks like more chaos and further decline in crude production.

Bjarne Schieldrop, Chief analyst commodities

A ban on oil imports from Venezuela to the US would likely only hurt US refineries which needs the heavy oil from Venezuela to blend with ultralight shale oil. Venezuela’s crude would probably just travel to other parts of the world instead of to the US. So an import ban to the US would probably not tighten the oil market as such. Tighter sanctions towards the Venezuelan economy with the goal of toppling the current Maduro regime would however most likely lead to a further rapid deterioration in Venezuela’s oil production which of course is directly bullish for the oil market. Eventually moving to the other side of chaos with an eventual Juan Guaidó regime holding hands with the US would then of course turn things around again as it would lay the foundation for a revival in crude production in Venezuela again but that seems to be way down the road from here.

As far as we understand it is not at all impossible for the US refineries to process ultralight US shale oil as it is today without blending it with heavy crude from Mexico or Venezuela. It is more that it is not optimal. Many of the US refineries were built for medium sour crude from the Middle East. In such complex refineries there are a lot of expensive post processing units following the division of the oil molecules in the atmospheric and vacuum distillation stage. All these post processing units have specific volume capacities calibrated to the molecule distribution in medium sour crude. So if US refineries process outright ultralight US shale oil in the distillation stage then many of the post processing units will run at sub-par volumes. Even the distillation stage may not be able to run at optimal capacity. I.e. it is technically and economically sub-optimal for these refineries to run shale oil outright but not necessarily difficult. It is mostly about economics. So a lower shale oil crude price versus product prices should facilitate this. The gasoline crack to Brent crude has however crashed to below zero and made it much more difficult. Or said in another way: A yet lower shale oil crude price is needed.

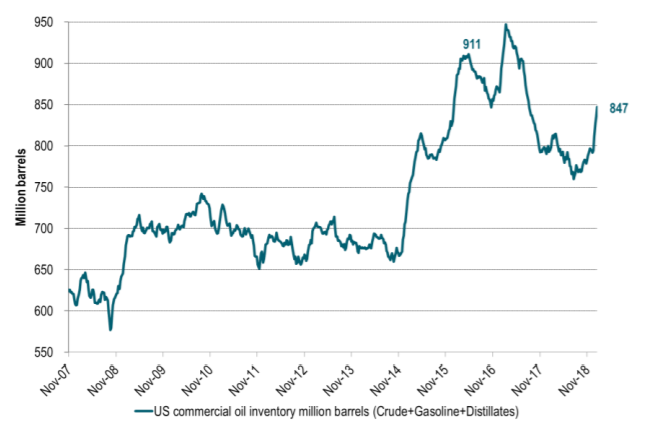

US crude and product inventories have sky-rocketed adding close to 90 m bl since late July last year of which 60 m bl have been added since late December. At the moment the market does not care too much about this since OPEC+ is cutting and production in Iran is falling (with further falls in Venezuela to be expected) while US well completions and rig count has started to decline. So the remedy for the booming inventories is on the way. If however the US S&P 500 recovery sours before the remedy shows signs of working (declining inventories) then crude oil prices would most likely follow the S&P 500 index lower.

A price-path dependent oil market. In our crude oil projection for 2019 we have projected Brent crude to average $55/bl in Q1-19 and we are well above that level now. It is important to note the strong price path dependence of today’s crude oil market. If we get a higher oil price now we’ll have more drilling more well completions and a higher oil production in the following quarters. It may feel good with Brent at $61/bl right now for global oil producers, but it may not be so good for the oil market in H2-19 as it will lead to a higher US crude oil production then.

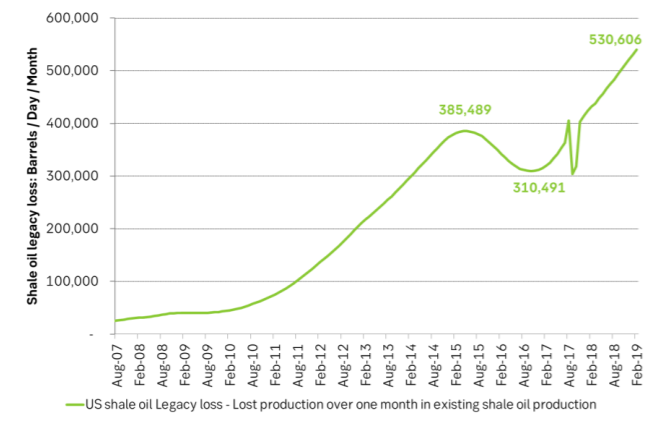

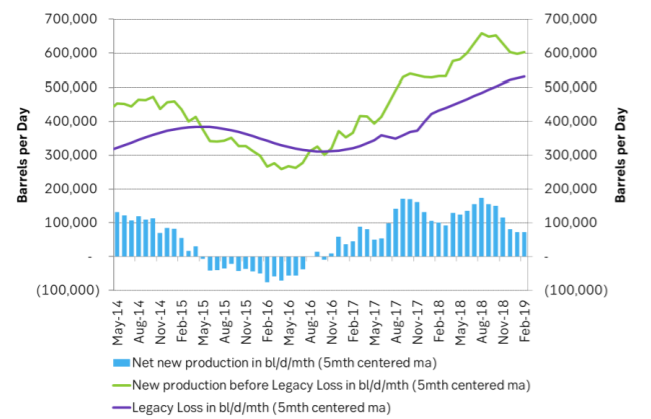

US shale oil production slows. In this week’s US EIA drilling productivity report we see that well completions have come down thus reacting to the decline in crude oil prices in H2-18. Losses in existing production rose to a new high of 530 k bl/d/mth while new production before losses rose to 602 k bl/d/mth for February. Marginal, annualized production growth thus fell to only 0.86 m bl/d/yr as new production growth slowed and moved closer to the rising legacy loss in the existing production.

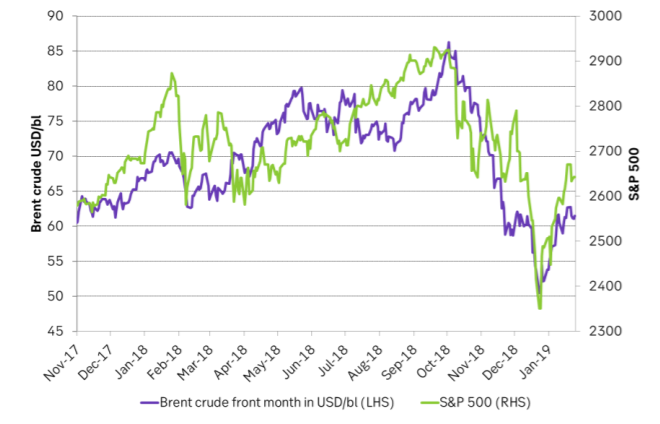

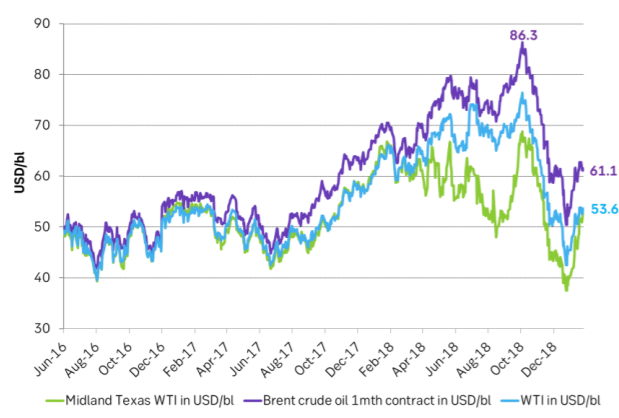

Ch1: Crude prices and the S&P 500 continue hand in hand.

Ch2: US crude and product stocks have rallied. Up close to 90 m bl since late July of which close to 60 m bl since late December. But remedy is on the way with cuts by OPEC+ so the market has not cared too much about this since late December

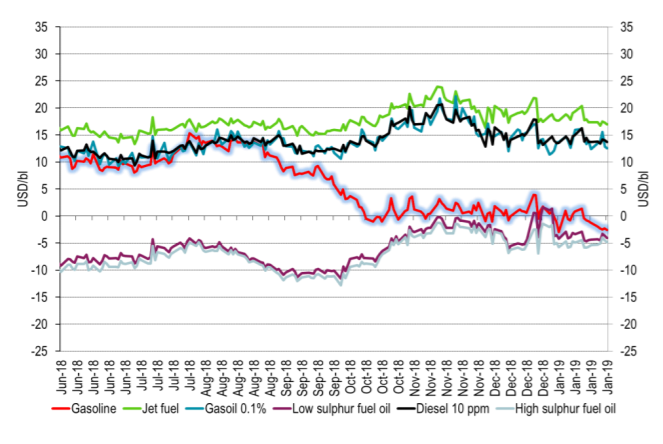

Ch3: Refining margins have been murdered by the crash in the gasoline crack (to Brent). Now gasoil and diesel cracks are also ticking lower as we moves towards the later part of the Nordic hemisphere winter.

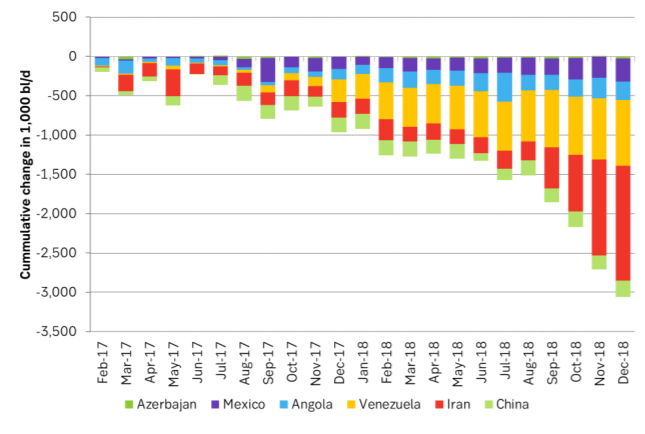

Ch4: Not so difficult to be booming shale oil as long as some 3 m bl/d is removed from supply from other suppliers. Booming US shale oil supply in the US is bad for Iran. The higher it goes the more room it gives Donald Trump to tighten Iran sanctions yet tighter.

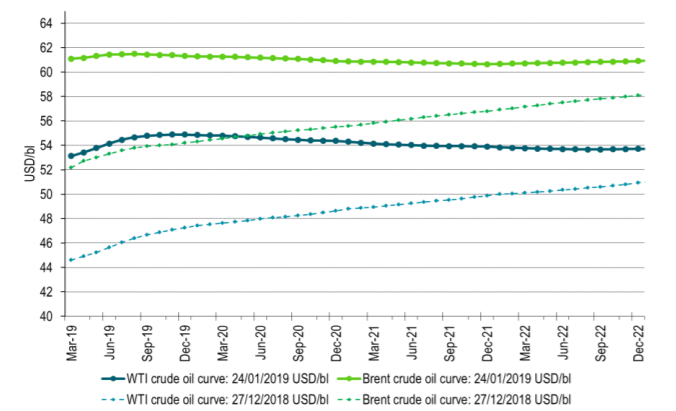

Ch5: Brent crude curve has flattened significantly since the low of 24 December

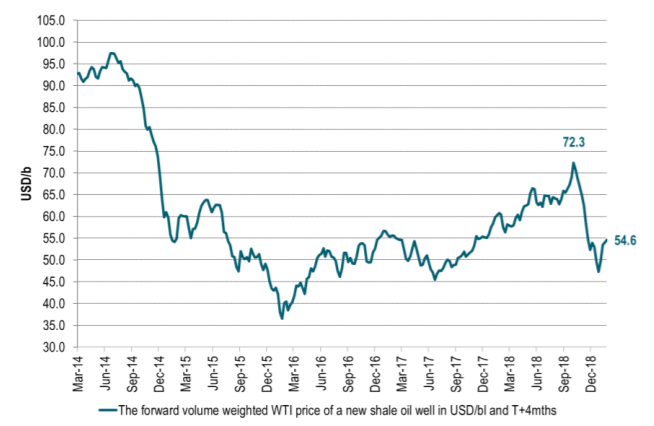

Ch6: The shale oil volume weighted WTI crude price has come down from $72.3/bl. But it has rebounded back to close to $55/bl which would imply “medium shale oil heat” if it stays at that price level. Access to capital is probably just as important as the oil price.

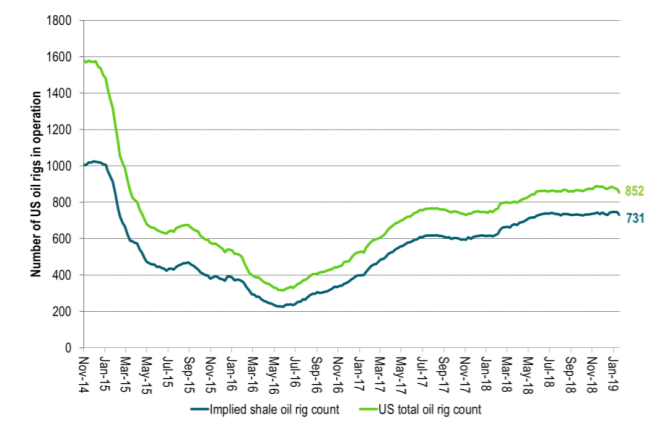

Ch7: US oil rig count has ticked lower but not all that much yet

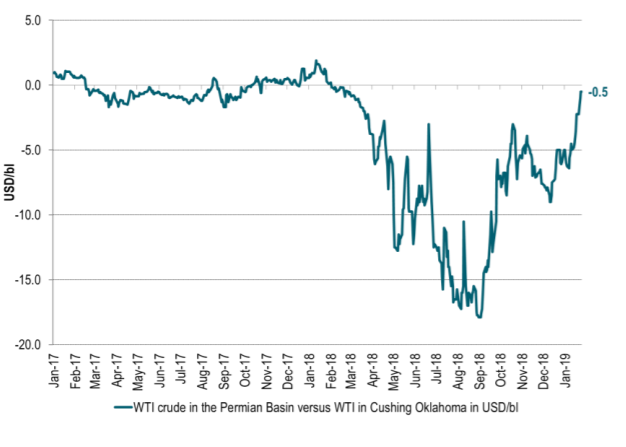

Ch8: The local Permian crude oil price traded at a huge discount versus Brent and WTI at times in 2018 as lack of pipelines out of Permian basin led to land-locked oil in the Permian

Ch9: Permian is obviously no longer very land-locked with respect to getting its oil to Cushing Oklahoma WTI and Permian prices are now almost equal again.

Ch10: Losses in existing US shale oil production will be 530 k bl/d/mth in February according to the US EIA. The most ever. I.e. more and more new wells need to be completed in order to counter this rising loss.

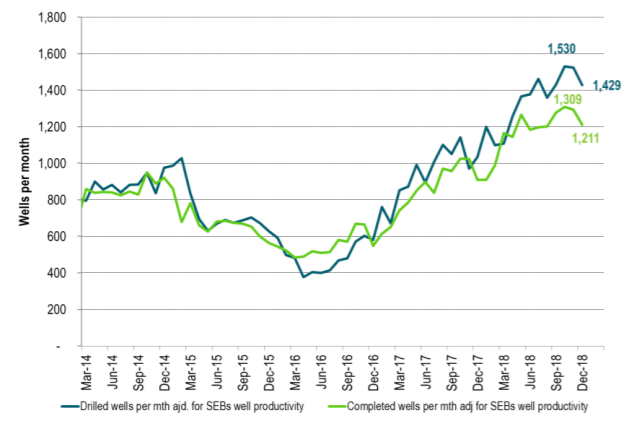

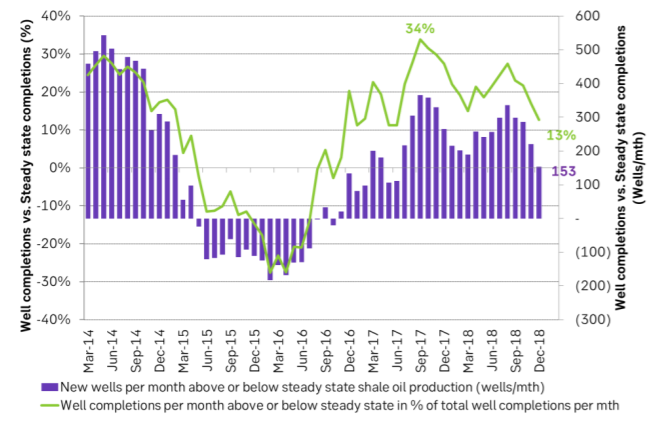

Ch11: Number of completed shale oil wells moved sideways in Oct and Nov and then down in December.

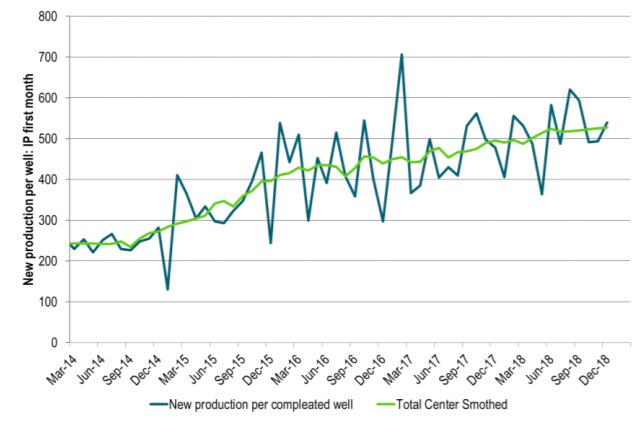

Ch12: A lower level of well completions led to a lower level of “new production”. Losses in existing production continued to increase. The gap between new production and losses thus narrowed so net production growth slowed to lowest growth rate since mid-2017.

Ch13: Well completions per month now only running at 153 (13%) wells above steady state (when US shale oil production growth = 0). That is the lowest since mid-2017. Due to strongly rising legacy loss the well completions only need to decline by another 153 wells per month to drive US shale oil production growth to a halt.

Ch14: Shale players are however still drilling way more than they are able or willing to complete. There is thus probably a significant inventory of DUCs which they can complete without drilling. So there is room for drilling rigs to decline significantly without a comparably significant decline in well completions.

Ch15: Well productivity ticks higher at a pace of about 5-10% per year. But number of completed wells/mth is more important